The Fed announced tapering of QE as of 2014, subject to developments of course. It will first need to taper out its QE to zero before rates can rise from ZIRP. Rates will then likely be raised slowly as in the 1950s due to high government debt. Together this means easy monetary conditions will persist until US demographics bottom out 2014-2019. I suggest that is broadly necessary to counter the demographic downtrend and could mean that we see continued low growth with more asset bubbles appearing and then popping.

What would change this course of action? If inflation became problematic and yields rose too far too fast. Currently inflation is benign as global growth remains fairly soft. History reveals that a low growth low inflation low rates environment is good for equities. It took the last 12 months for investors to really gain confidence in economic growth persisting (if soft) and with a gradual bottoming in government bond yields:

Source: Bloomberg

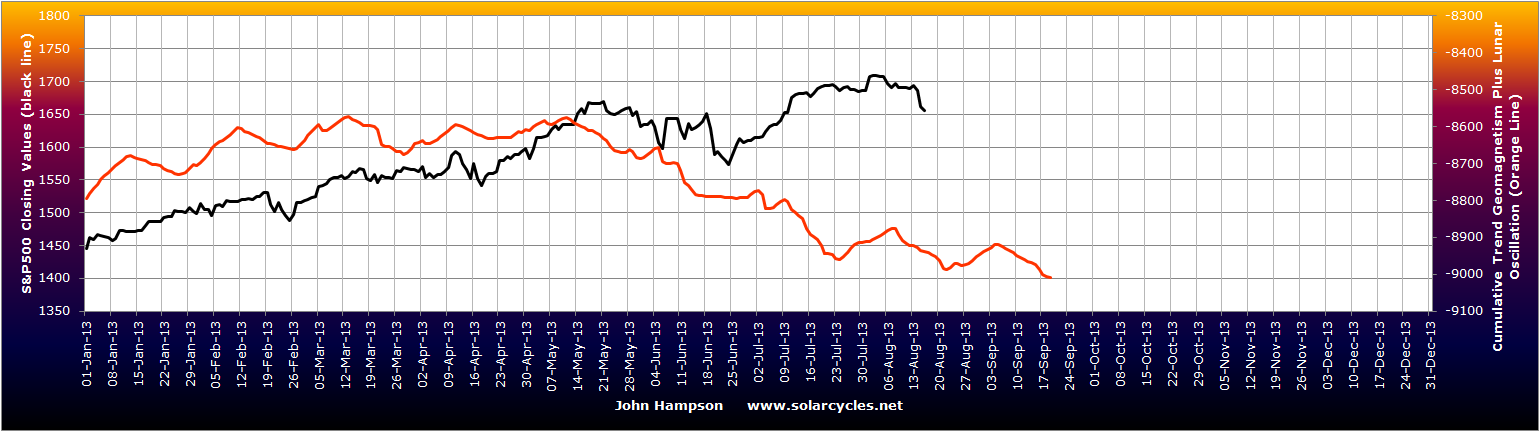

At those record low yields, investors were making a guaranteed real loss, yet money flows were still attracted into government bonds – with the assistance of QE in USA, UK and Japan – due to fear of greater losses in other asset classes. Recently that has changed, and it is because low economic growth has persisted long enough with some of the main worries (e.g. Euro debt, sovereign default) deflated. That does not preclude new crises emerging, but there has been a gradual process of repair since 2008, and I suspect we have seen the bottom in bond yields.

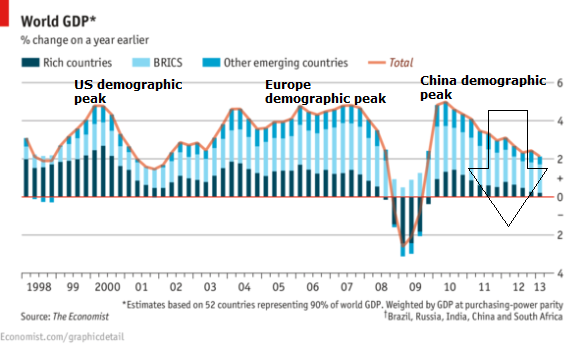

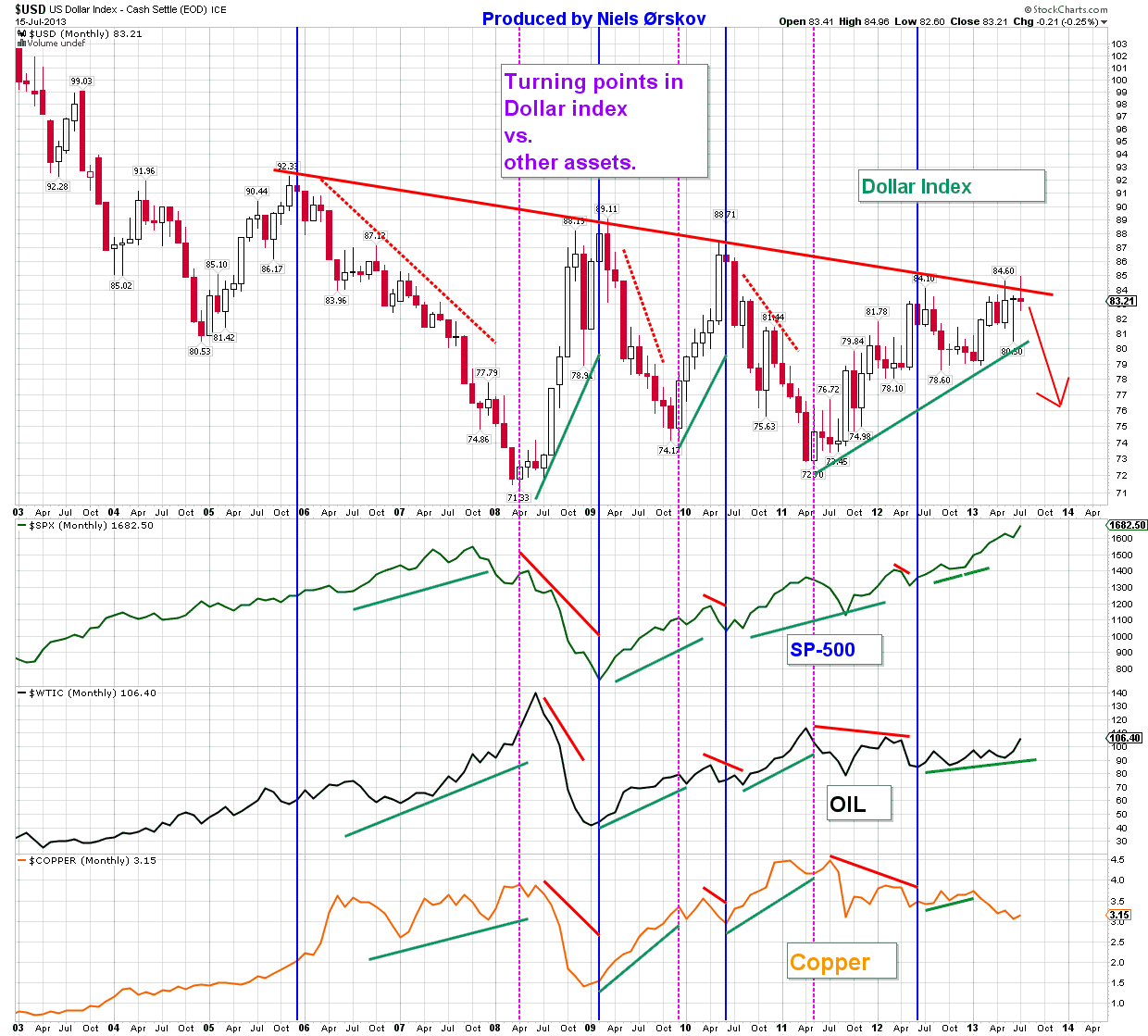

Because we are currently in demographic downtrends for the USA, China and Europe, I suggest it makes sense that only low growth is the current norm and that easy monetary conditions are likely to be maintained until a collective demographic improvement as of around 2020. Gains in real estate and equities should be capped by the demographic downtrends, but supported by the easy money conditions. Commodities have historically performed well during demographic downtrends, but could struggle to make large gains if soft growth holds down demand. Money should continue to flow out of government bonds, with any of those three classes the recipient, unless real yields rise too high for bonds to become attractive again. Yields cannot be allowed to rise too high because of high debt servicing and negative economic impacts. Combined, that makes for a fine balancing act between all four asset classes.

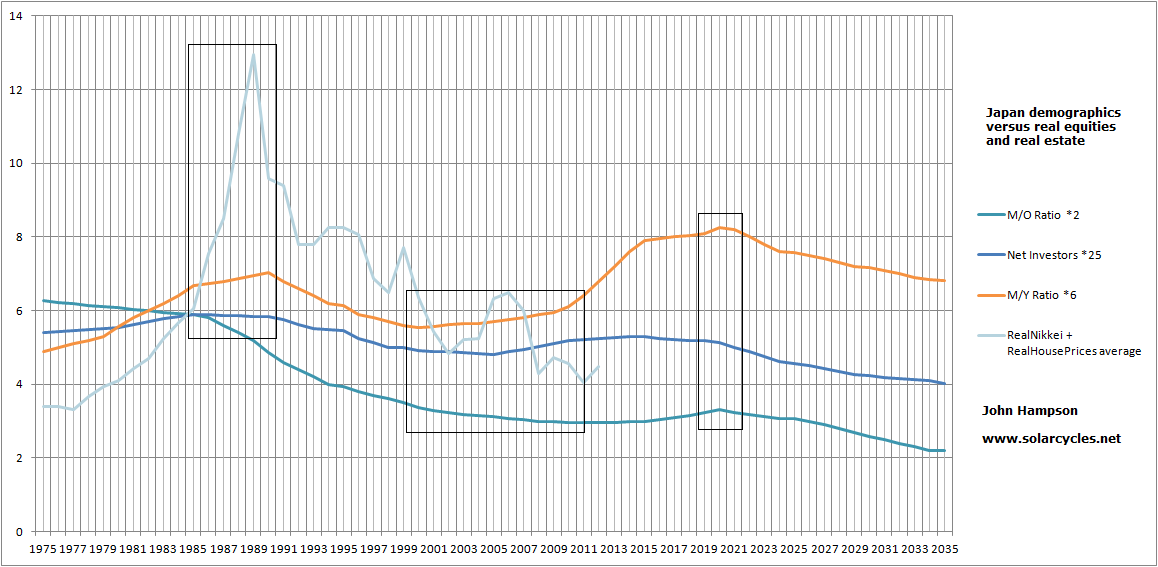

Japan is one economic giant that is in a demographic uptrend and I believe the recent surge in equities there is a belated catch up to that trend.

I believe Japan was ripe to bottom around 2002, along with demographics, but was then pulled back down again with the global crisis in 2007/8. The H1 2013 Nikkei rally was stopped at the long term declining resistance, but I think this time it will burst through it successfully, in due course:

The Japanese government has declared it will do whatever it takes to re-inflate the economy and assets including buying equities. The question is how long it will take to break through. If US equities are beginning a topping process then it would seem unlikely that Japanese equities break out at this point. If emerging markets are heading into a crisis, as Russel Napier believes, then a global sell-off would likely take place again.

There are 3 possibilities here for US equities. One is that they have run up in an eiffel tower parabolic formation and will collapse now down the other side. Two is that they have begun a topping process whereby we should see an overall sideways volatile range over several months whilst negative divergences appear. Three is that they are consolidating before further gains.

Because of the sharp run up and the demographic headwinds, I have my doubts about option three. However, cyclical stocks bulls usually end with commodities and inflation rising to become problematic and helping tip the economy into recession. Inflation rises, yields rise and the higher input costs and higher rates squeeze the economy. Bonds top first, then equities, then commodities. At this point we appear to have seen a top in bonds, but do not yet see commodities or inflation rising. Therefore we don’t see the usual historic pressures to pull down equities. Low growth, low inflation, low rates: good for equities.

For option 1, a harsh collapse, some analysts are referring to a 1987 overlay, predicting a crash. I can’t rule it out, I can just refer to that current environment again – it differs significantly from 1987 where yields and rates were much higher. We know that flash crashes can happen, where automated selling begets automated selling, but I suspect we’d need a swift change of status quo to bring it about. Something like the possible emerging markets crisis.

For option 2, a topping process, we would have time. There is no rush to short until we need more technical evidence of a topping range and negative divergences in breadth and leading indicators begin to appear.

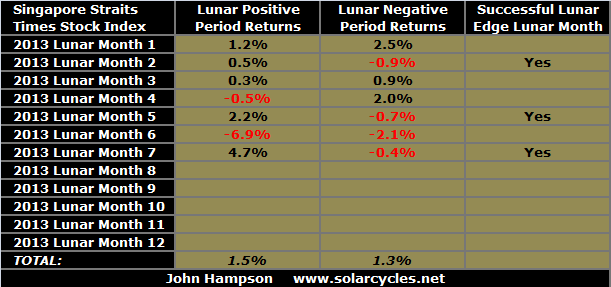

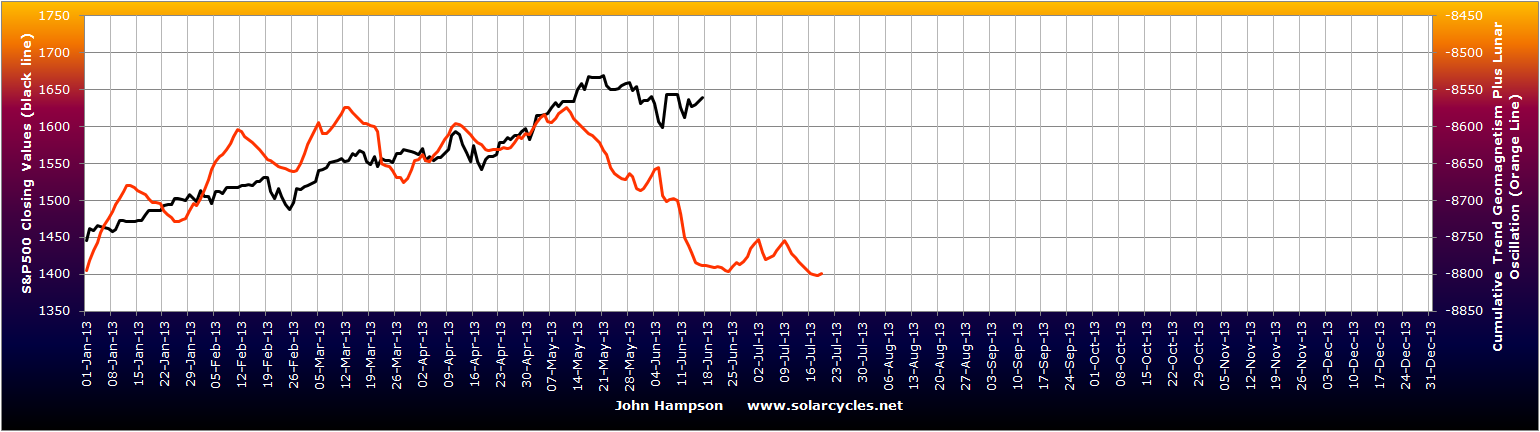

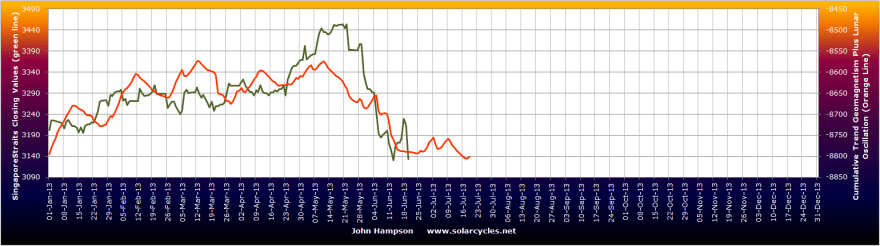

In the short term, I believe we could be reaching a point this weekend whereby equities rally up again. Passing through the full moon together with a possible bottoming out in geomagnetic disturbance – the Singapore STI shown here mapping very closely to the model:

Plus, low Nymo and bullish percent / call put readings in US equities suggest a bounce imminently.

If equities do bounce then crude oil has a chance of holding its breakout, which it is currently backtesting. If crude cannot, and falls back into the triangle, then the textbook action to follow would be a breakdown out of the bottom of the triangle, which would likely spell prolonged doom for the commodities complex.

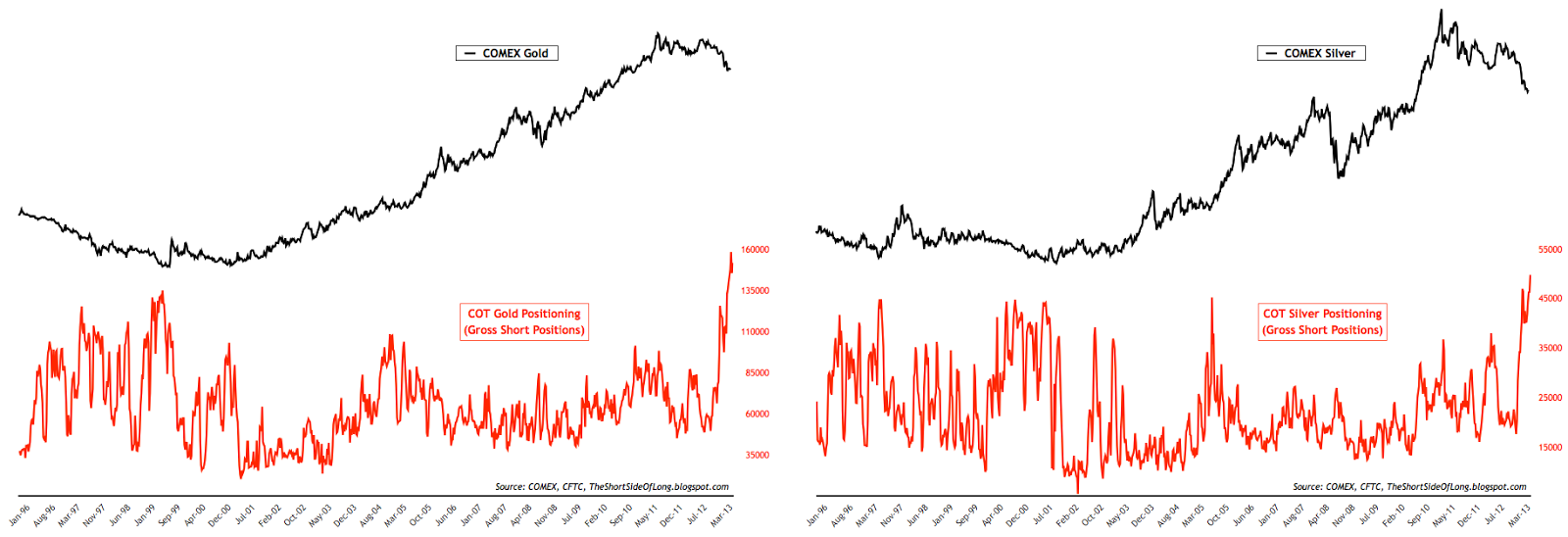

So will commodities come again? I believe they will. Nothing goes up or down in a straight line. Mean reversions eventually occur, if not something more juicy. What could give them momentum? A top in equities or concerns about the economy functioning without QE could spur money into precious metals as safety again, with a short squeeze possible on record short interest. Geopolitical developments can affect oil prices and in turn wider commodities and protests/wars are common at solar maxima. Global warming and global wierding remain risks to agricultural commodities, with May having come in at the 3rd hottest on record globally and Jan-May the 8th hottest on record. Global temperatures have historically peaked around solar maxima.

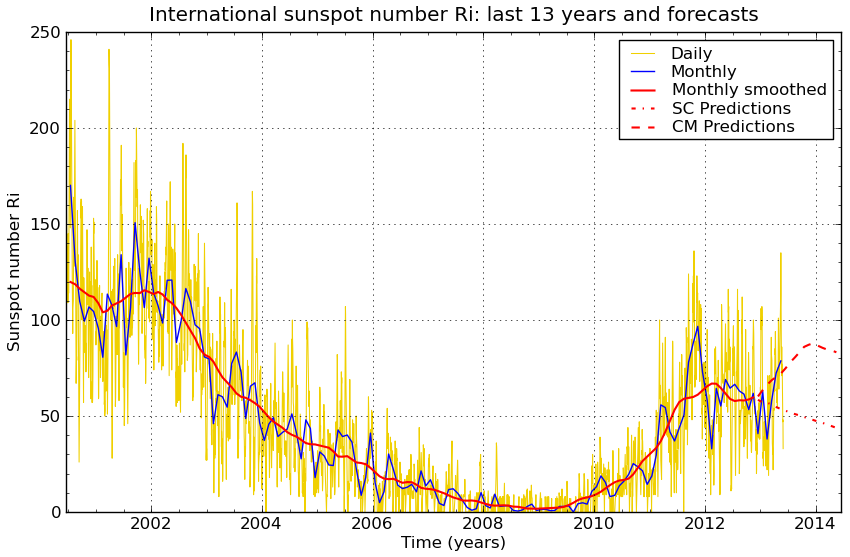

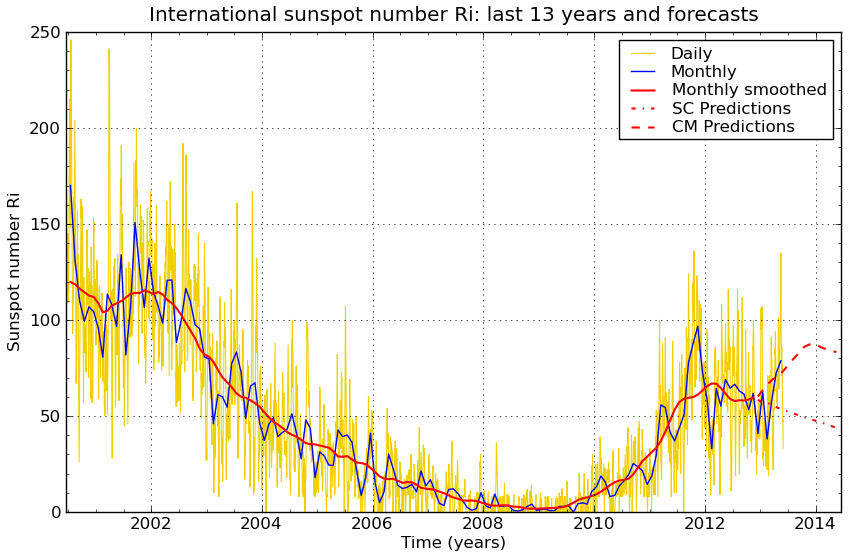

The latest on solar peak prediction is that NASA believe a summer peak in 2013 is likely, NOAA a Nov/Dec 2013 peak, and SIDC running with two options as shown:

Source: SIDC

Source: SIDC

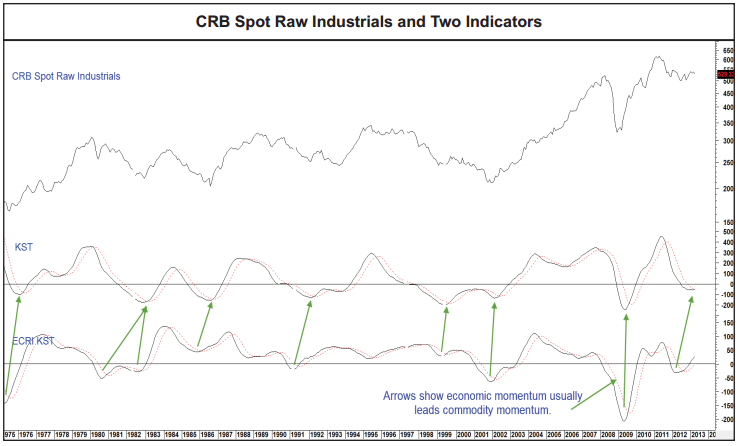

Averaging, we could look to a late 2013 smoothed maximum. Historically, secular asset peaks have been made close to solar maxima, along with inflation peaks. We should allow around 12 months for commodities to rise up and make a ‘secular’ peak and an associated inflationary peak if it is to happen along with this solar maximum, so it should be the theme from here into 2014 if it is to occur. With bonds having likely topped and equities having rallied hard, we are also ripe for outperformance to emerge in commodities. However, economic data out of China, increasing inventories, depressed sentiment in the class, and strength in the USD are some reasons why this is not occurring. Until this collective picture changes in some way, I have to remain open to the possibility that commodities will underperform through the solar maximum, and this could mean a different asset class is bid up to a speculative peak if the solar maximum is still ahead.

From my recent Dow-gold ratio analysis, I suggested two likely bottoms in the ratio: 2014 or 2025 (approx). Either a swift run up to a speculative peak in gold into next year, or a mid-point currently on the way to a bigger gold peak a decade away at the next solar max. From the same analysis, demographics in the main nations no longer offer clear support for either equities or gold going forward, which I suggest means we are likely to see less wild swings between the two, and alternating shorter bulls. So I remain happy to average down in gold and other commodities, particularly with my new cash injection, and await either a mean reversion rally or a possible momentum move into commodities once a trigger emerges. I also would add to long Japan equities on any further drops. I am tempted by the weakness in positive-demographic Brazil and India to build more of a long positive there, but each are currently experiencing their own economic or social problems which could yet worsen so I am going to hold off. I would look to add short equities if a topping process becomes clearer with negative divergences. I remain short treasuries.

I believe the greatest risk currently to my portfolio is some kind of sharp global sell-off, a collapse in US equities infecting all pro-risk. However, I really can’t call a winner from the three options I outlined above for US equities at the moment, so await further flags and developments. If pushed, I still place greatest likelihood by a historically normal unfolding of events, namely that bonds have topped and we will see equities top as commodities outperform, with commodities topping last, helping tip the world into recession and end the equities bull; that the solar maximum will inspire speculative peak and that peak will be in commodities (or precious metals at least) due to the collective demographic downtrends aside Japan. However, I am nowadays ultimately of the view that there is complex interaction between demographics, solar cycles, fundamentals, government intervention and more, that make it a difficult calculation. I believe anomalies can occur if several of these factors conspire together to produce one, which is why there is no holy grail. However, I expect clearer ‘probabilities’ to emerge from here, one step and development at a time.

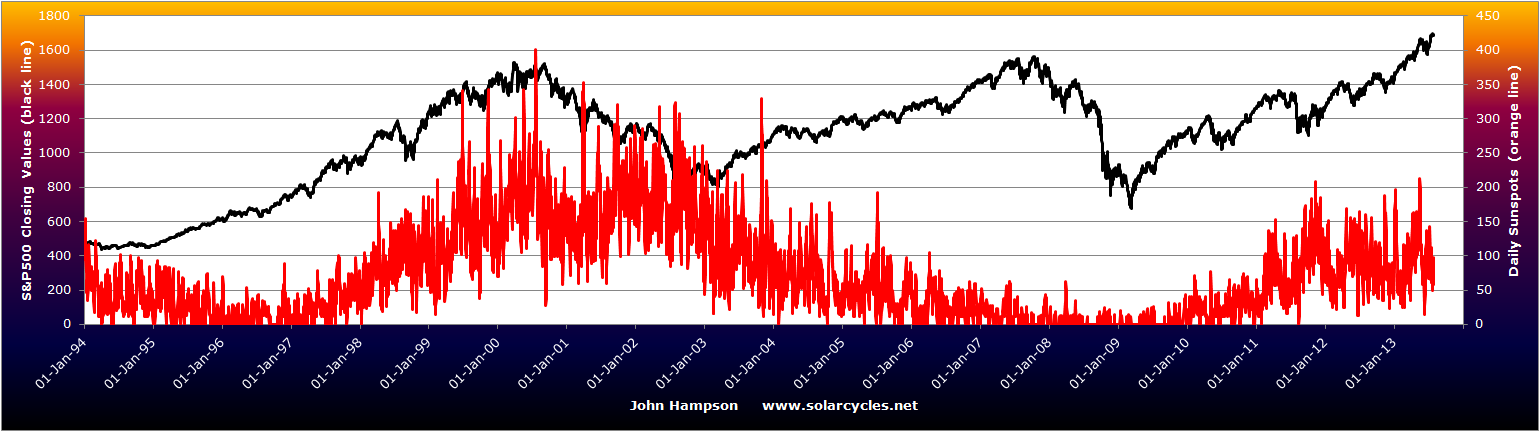

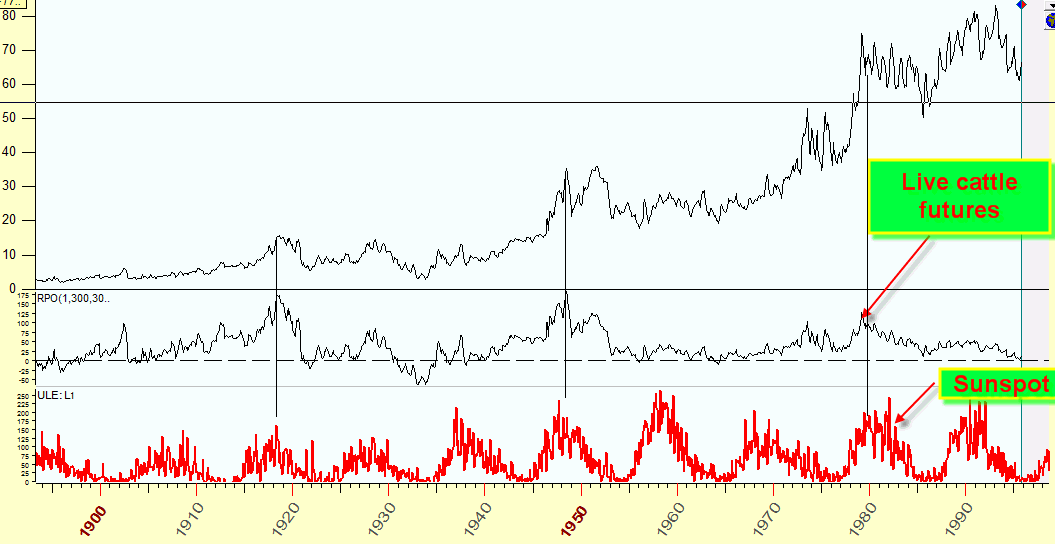

2. Sunspots – up again currently but still no clear trend:

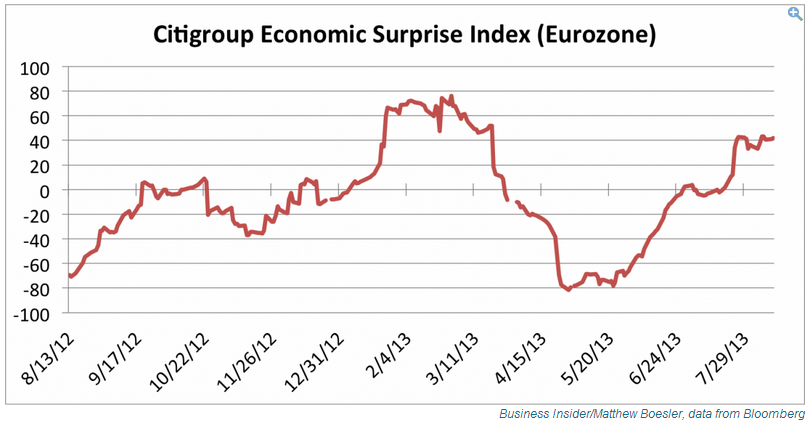

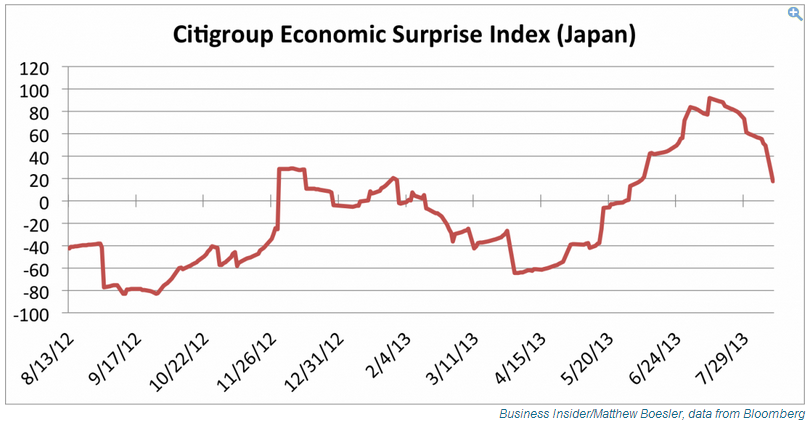

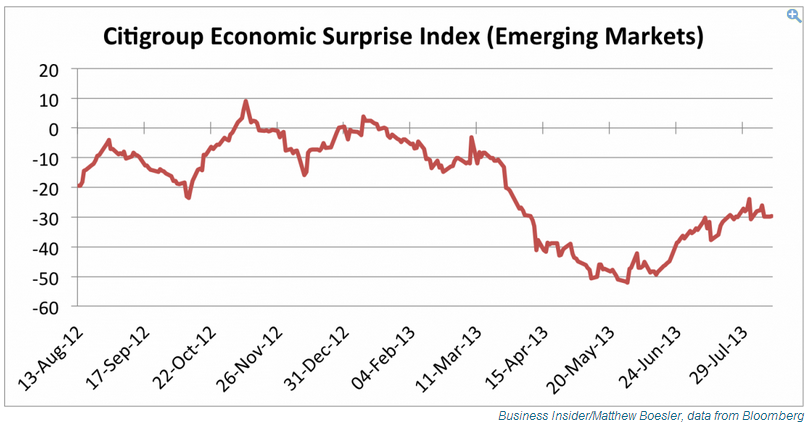

2. Sunspots – up again currently but still no clear trend: 3. Economic surprises – coincident data positive in USA and Europe, improving in China, disappointing in Japan and languishing in emerging markets:

3. Economic surprises – coincident data positive in USA and Europe, improving in China, disappointing in Japan and languishing in emerging markets:

4. Leading indicators – weakening of late:

4. Leading indicators – weakening of late: