The big picture looks like this:

Source: Stockcharts

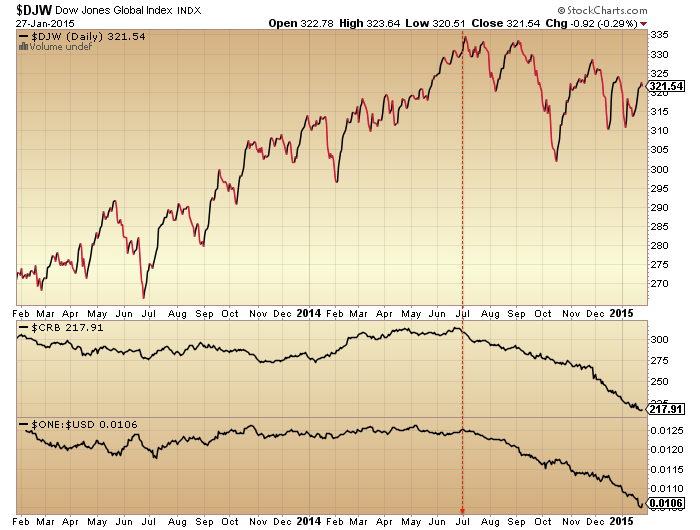

Global stocks, commodities and the world’s reserve currency turning in unison at the end of June 2014.

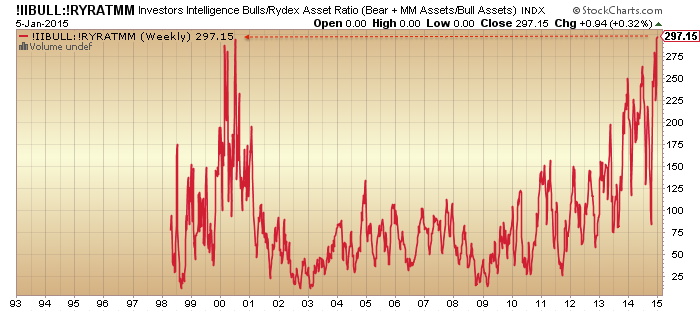

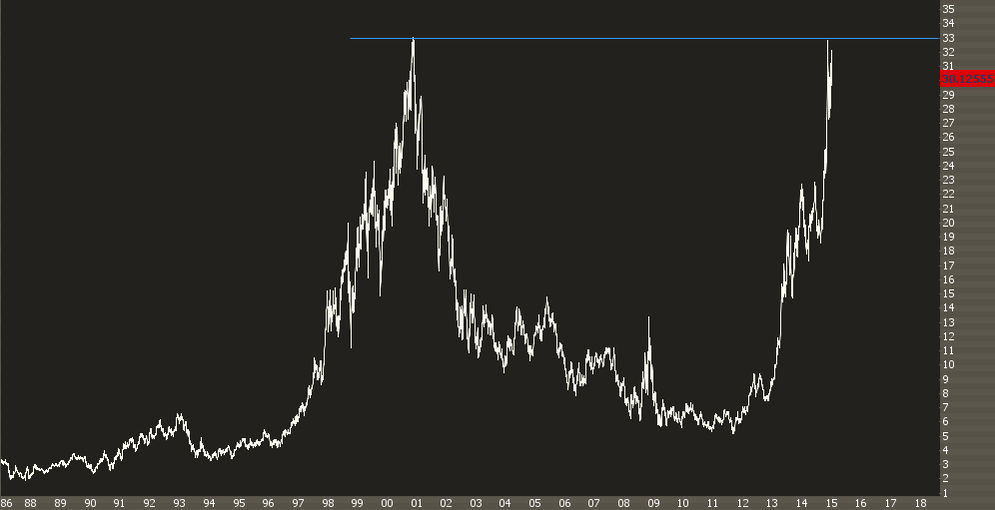

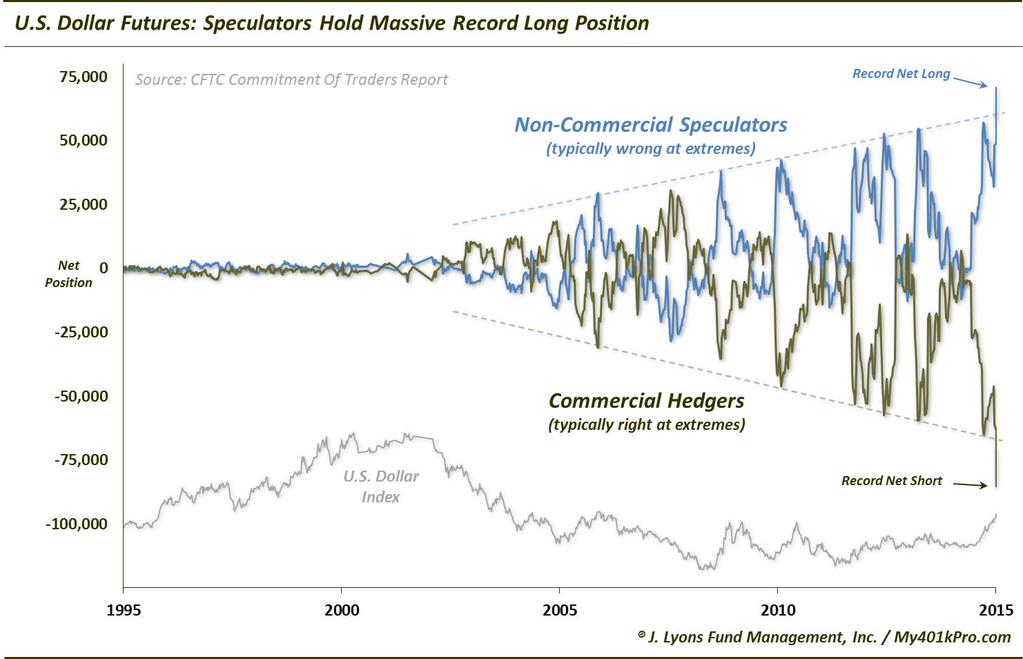

Extreme lop-sided positioning in the US dollar suggests a reversal should be close at hand. I expect gold to be a beneficiary.

Source: J Lyons

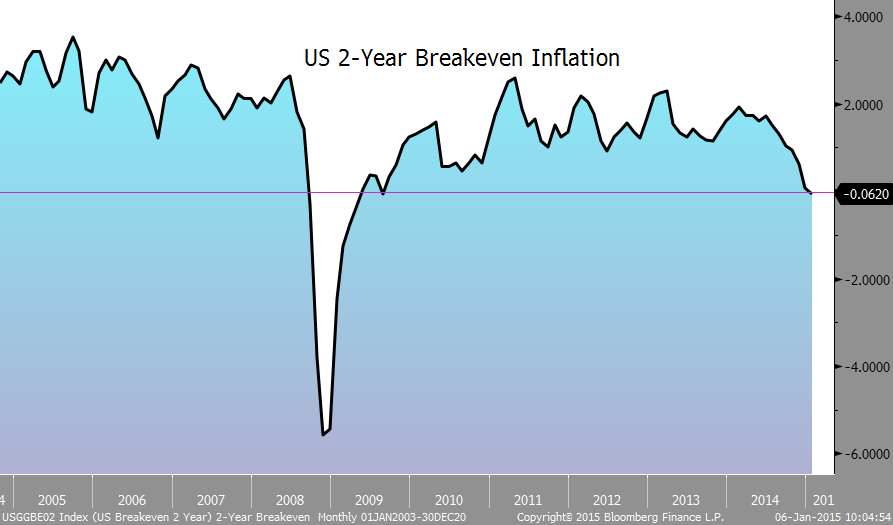

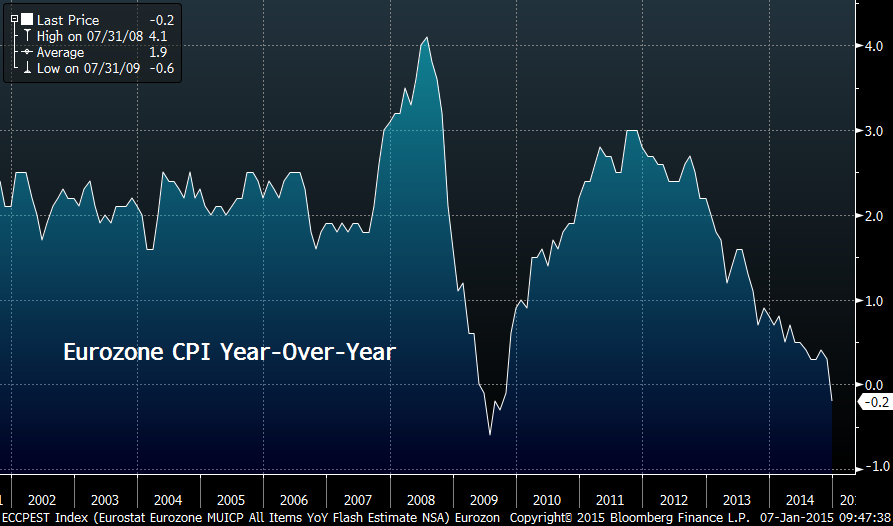

Tying in with this, economic surprises have crossed fortunes in the US and Europe:

Source: Moneymovesmarkets

Therefore, the Euro should be due a bounce versus the Dollar.

US leading indicators remain mired negative.

Source: Dshort / ECRI

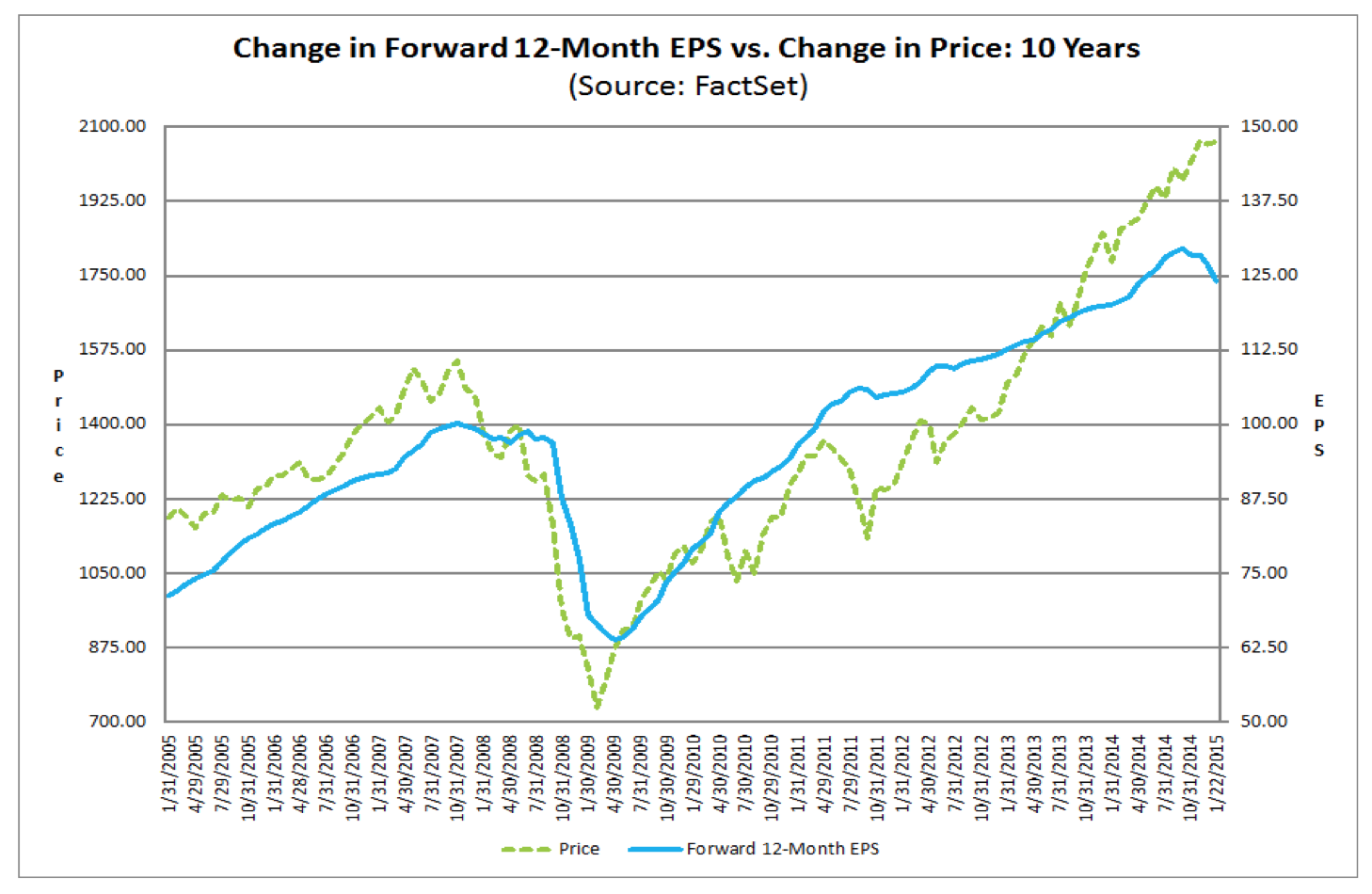

And so far, Q4 earnings have disappointed, as predicted by a rising dollar and falling oil. Here we can see the key turn down in earnings per share:

Source: Factset

Source: Factset

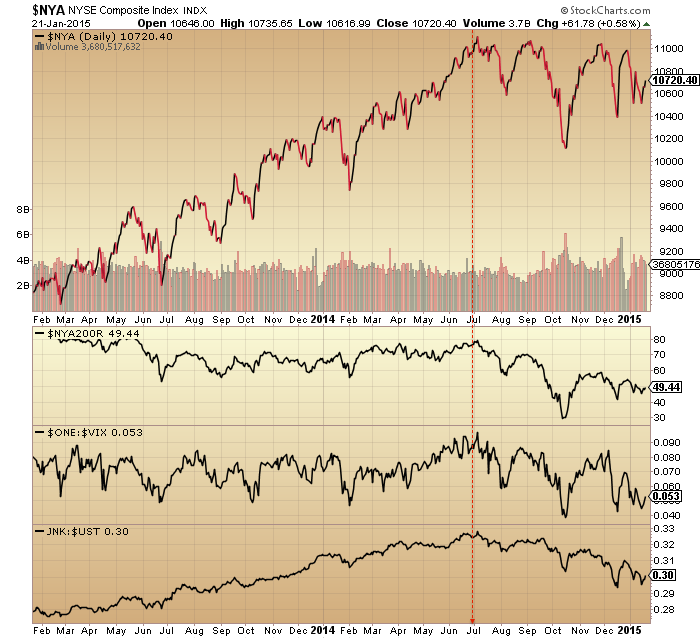

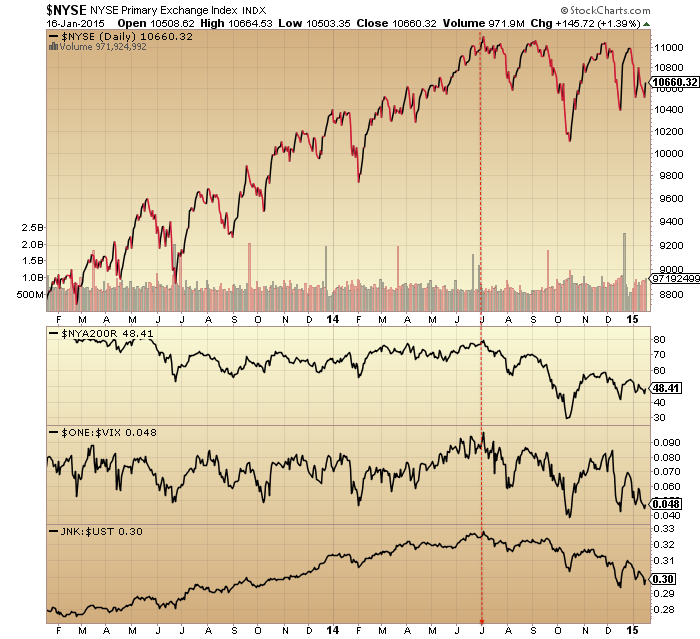

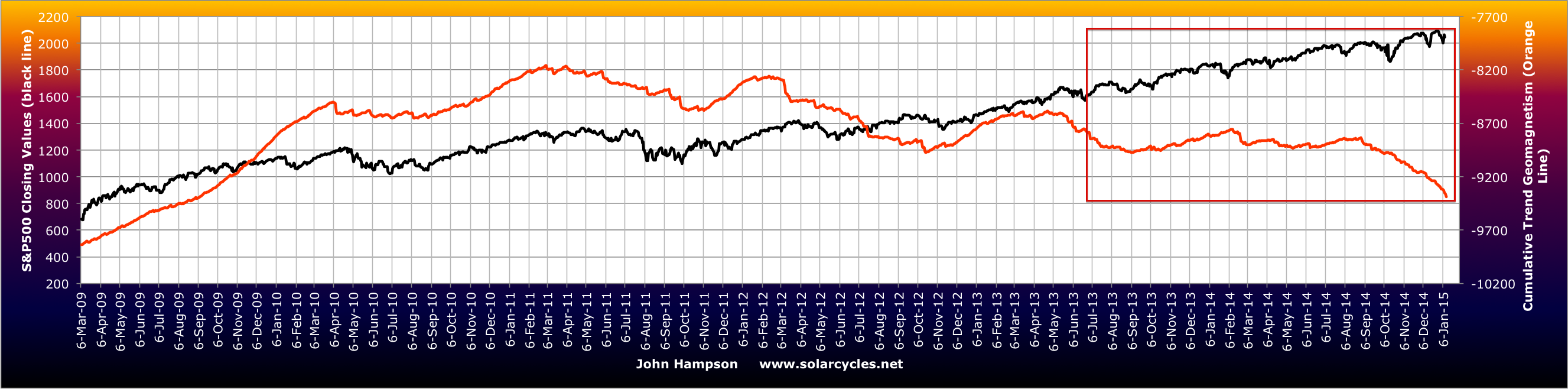

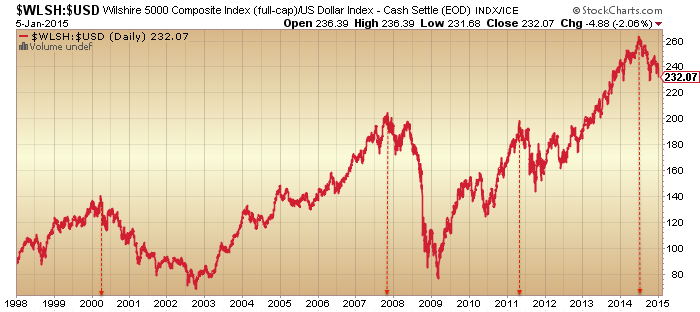

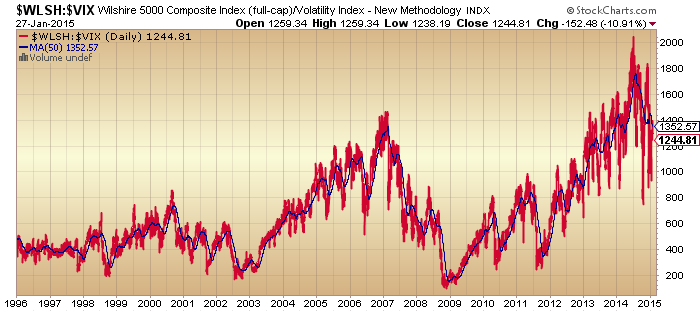

The SP500 looks on borrowed time since the end of June 2014, when we look behind price:

The stocks:volatility ratio also turned down at that time, and resembles key changes in 2000 and 2007:

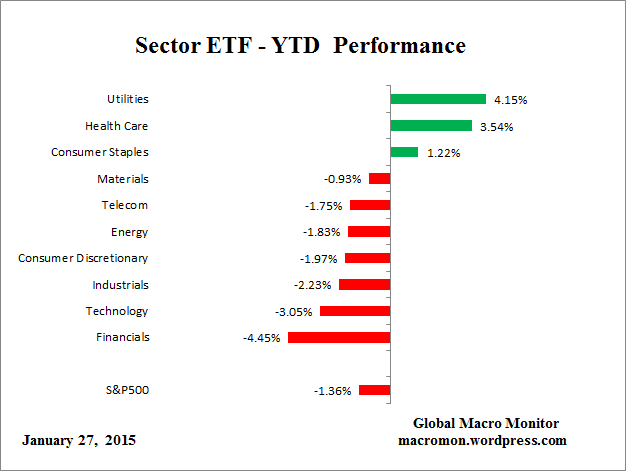

The sector performance tale in 2015 is the same as 2014: defensives lead as they tend to post-peaks:

The sector performance tale in 2015 is the same as 2014: defensives lead as they tend to post-peaks:

Source: Macromon

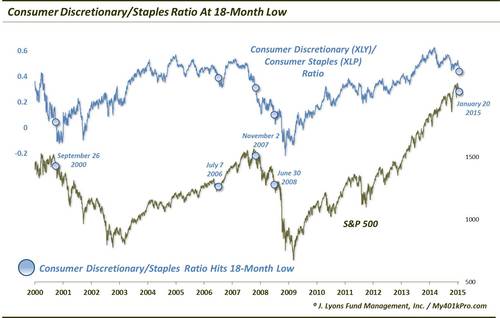

Source: J Lyons

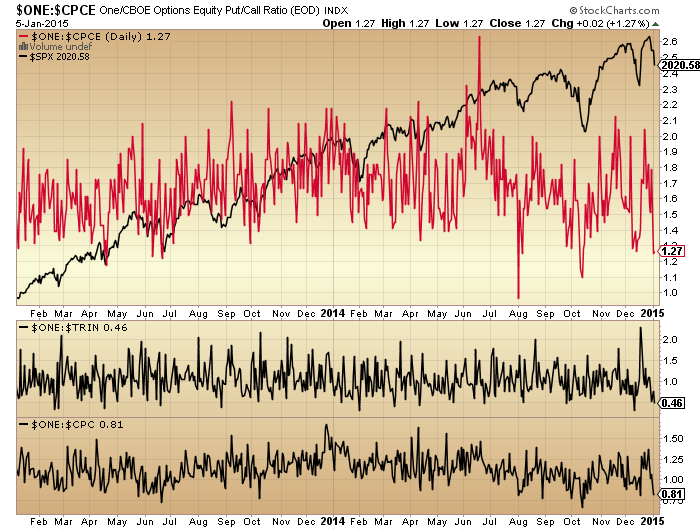

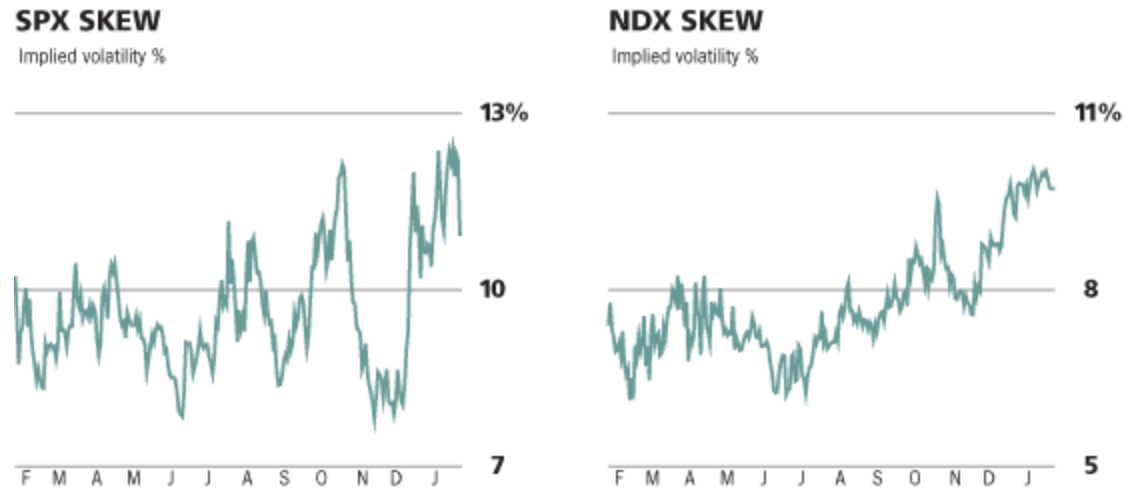

Skew remains persistently high, warning of a potential big move in the markets:

Source: Barrons

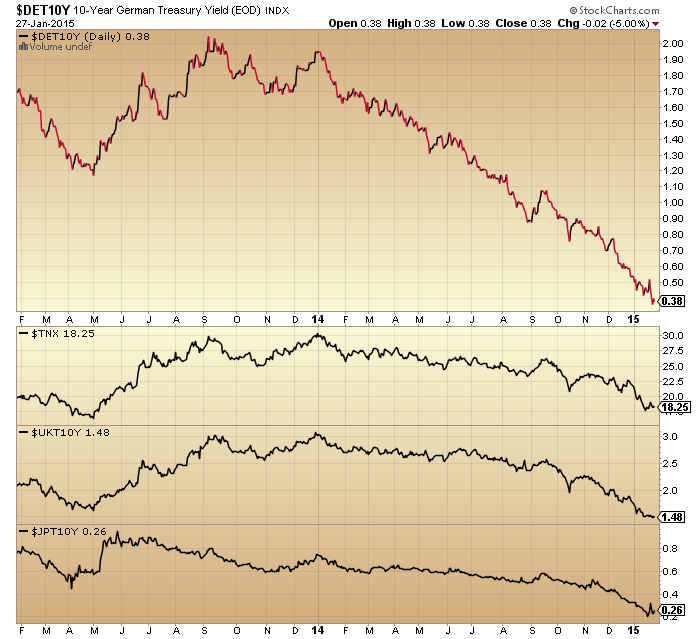

Money continues to pour into government bonds, with Swiss 10 year yields now amazingly paying holders a negative return:

Source: SoberLook

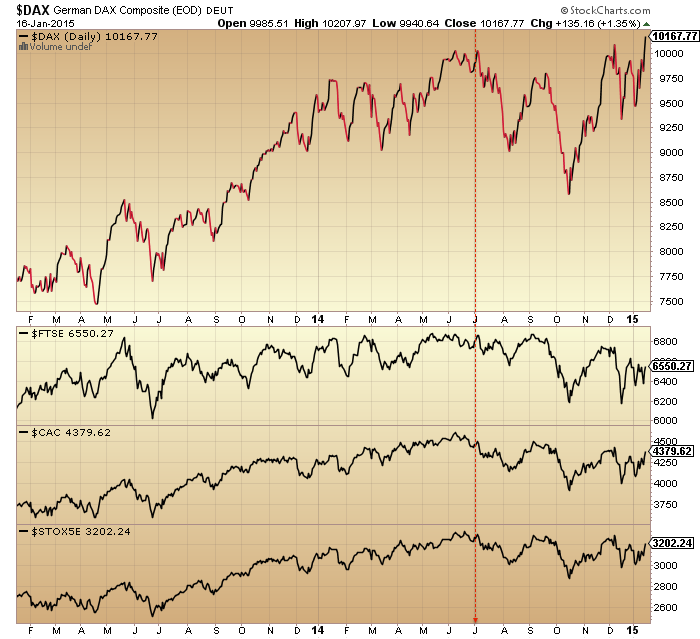

The bullish development in equities is in Europe where various indices have broken upwards on the QE news, with Germany the leader. There is a 12 month divergence in breadth, which I would tie in to the bigger picture above which would suggest Europe may be experiencing a blow-off top.

Source: Indexindicators

If that is not the case, then we should see risk-on firm up again globally, making repairs to the various asset and indicator downtrends that I present. As things stand though, the balance of evidence is still weighted to the global peak being in the past, and if my three key dates are correct, then US stocks should not exceed their December peaks, with European stocks shortly falling into line. Which way this triangle resolves will tell us the answer: