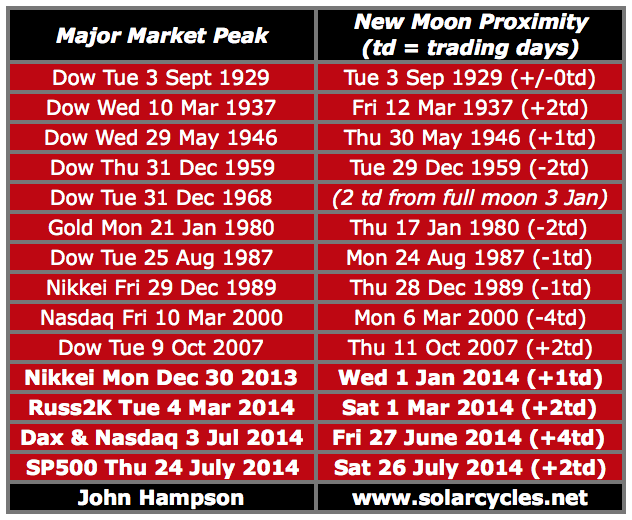

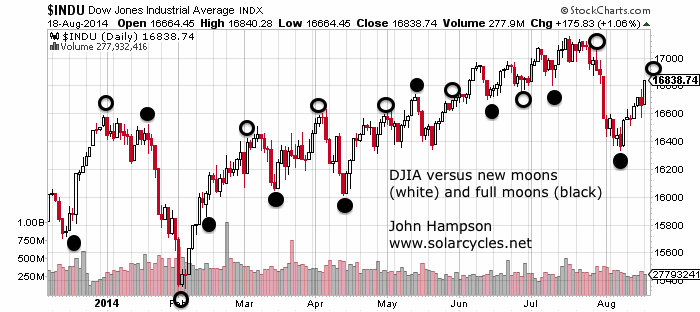

As we wait for the ECB decision and market reaction, I see 3 exact dates being revealed that align with my ‘triple confluence peaks’ idea, i.e. we are seeing major market peaks form at the new moons closest to the geomagnetic seasonal highs (inverted) closest to the smoothed solar maximum.

The smoothed solar max is likely to have been around April 2014.

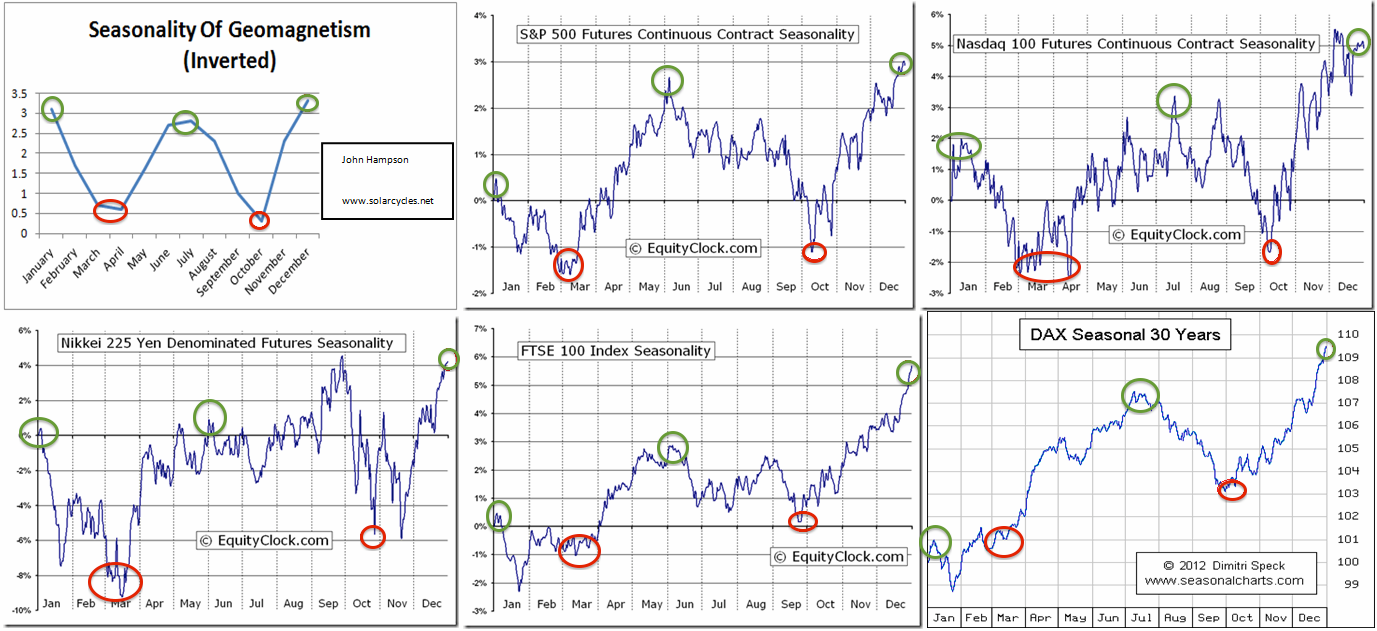

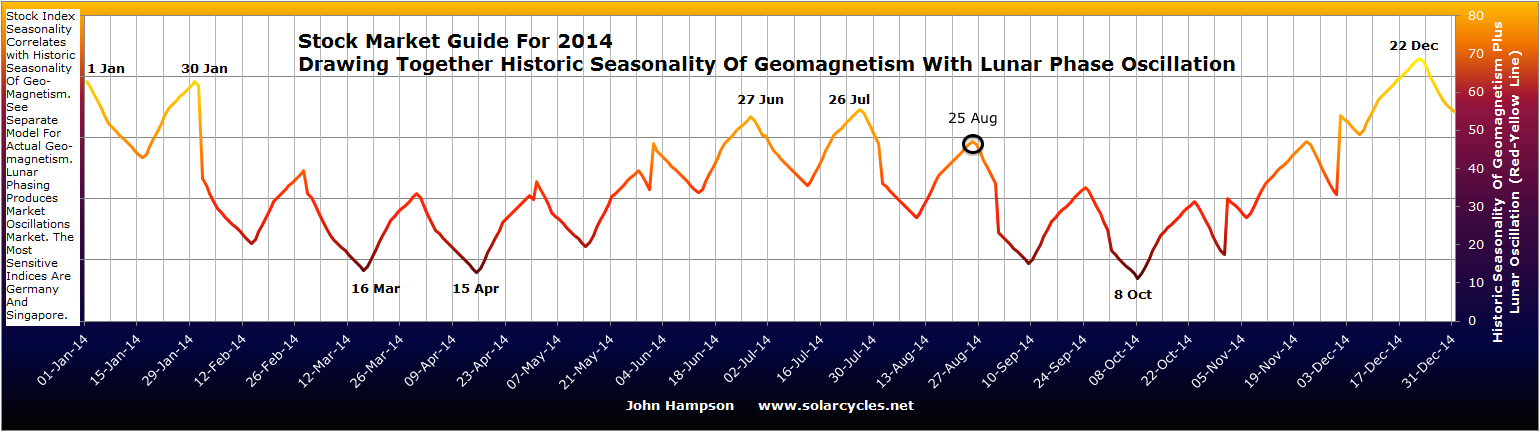

The seasonal peaks (inverted geomagnetism) fall at the turn of the year and mid-year.

The new moons closest to these seasonal peaks were 1 January 2014, 27 June 2014 and 22 December 2014, so it follows that we should see major speculation peaks at these dates in the year of the solar maximum, 2014.

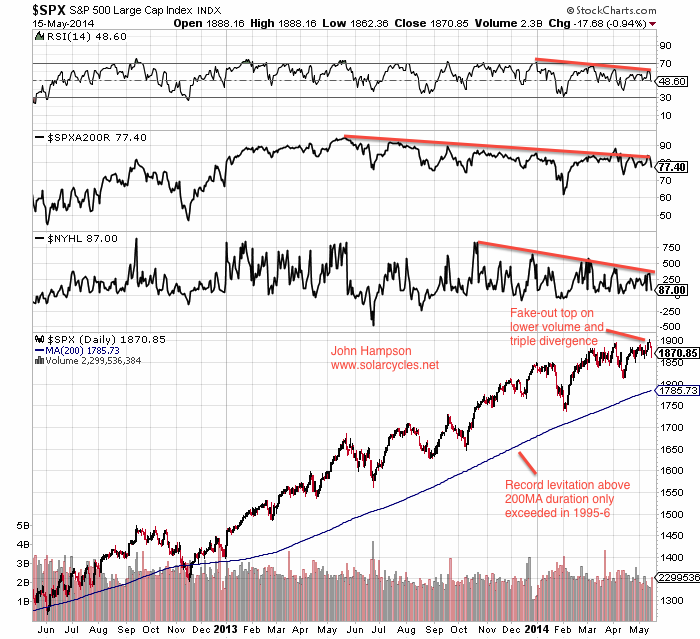

Bullish percent to call/put, cyclicals to defensives, high yield to treasuries and small cap equities to bonds all peaked very close to the 1 January 2014 date.

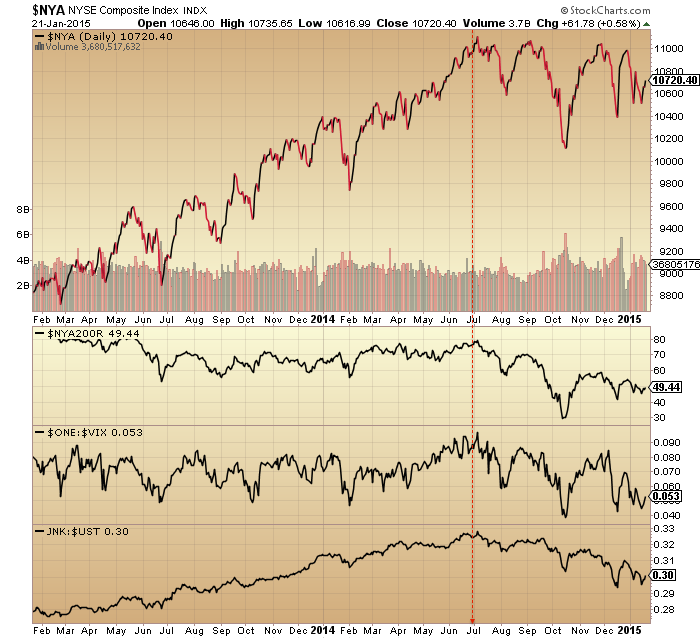

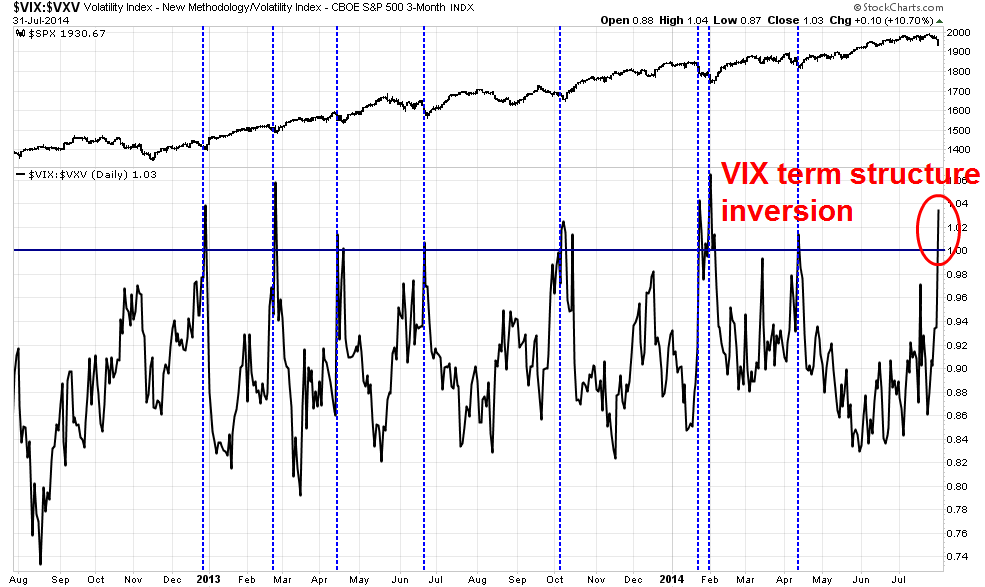

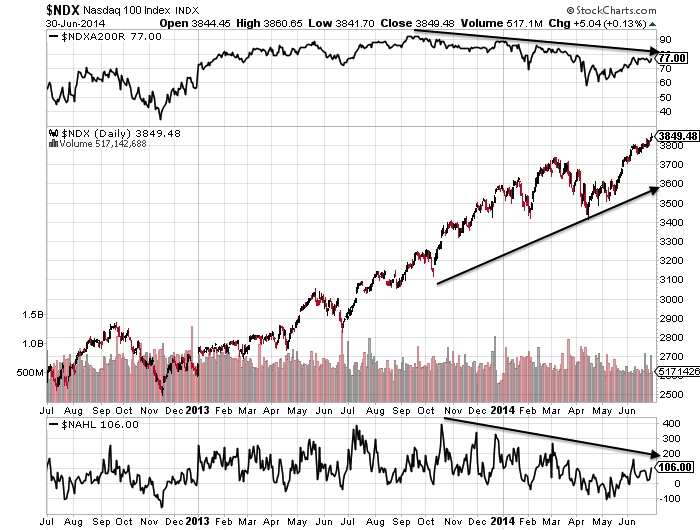

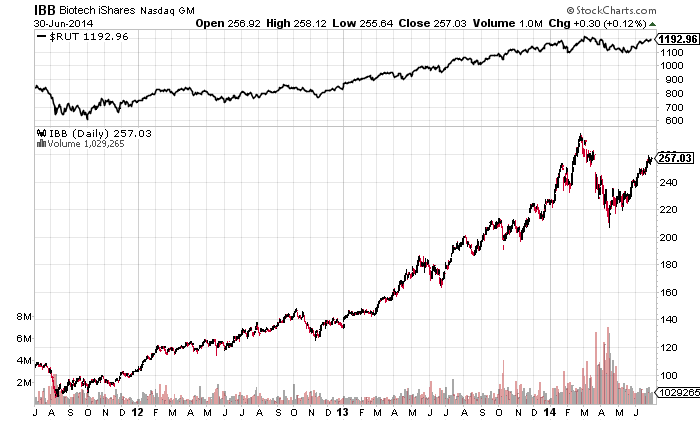

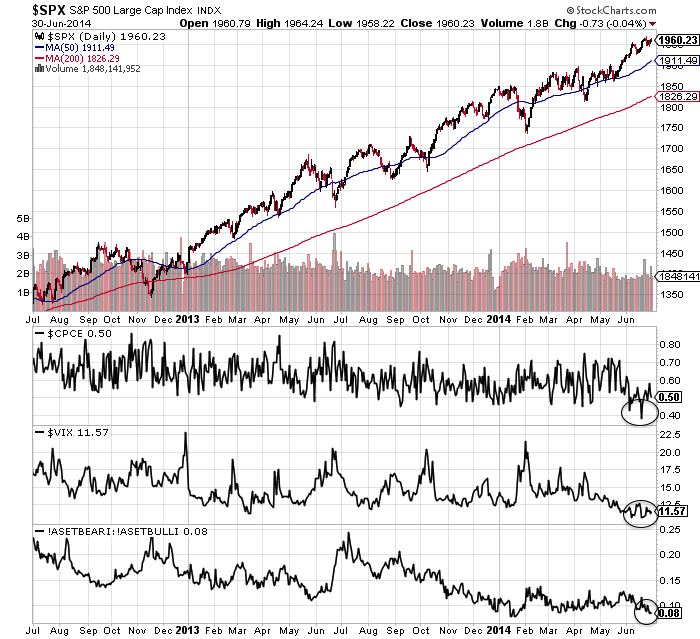

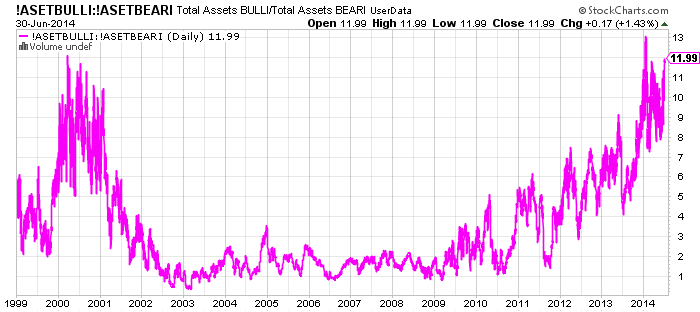

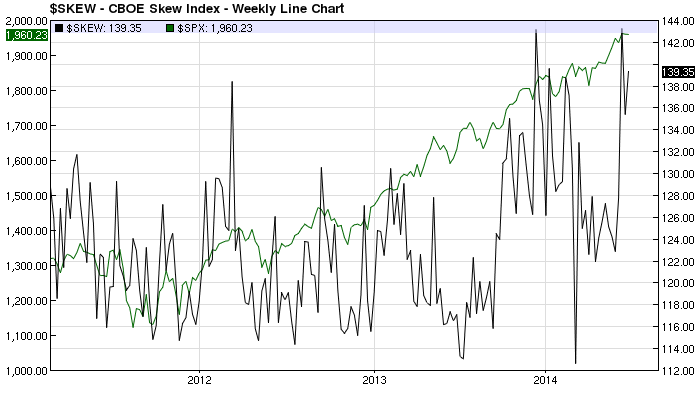

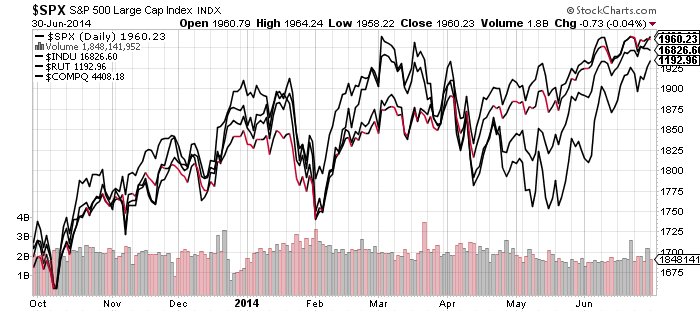

Stocks:dollar, stocks:bonds, FTSE Eurostox and NYSE composite indices, NSYE breadth, volatility and junk:treasury bonds, oil, US dollar (inverted), leveraged loans and junk bonds all peaked very close to the 27 June 2014 date.

Stocks:dollar, stocks:bonds, FTSE Eurostox and NYSE composite indices, NSYE breadth, volatility and junk:treasury bonds, oil, US dollar (inverted), leveraged loans and junk bonds all peaked very close to the 27 June 2014 date.

The final date, 22 December, has tentatively topped out the remaining key indices and speculation measures, namely SP500, Dow and Wilshire 5000 (plus an associated bottom in gold) and a blow-off top in sentiment and allocations.

If this ‘dumb’ model of the markets is correct then we should make no new highs from here but rather collapse to a March/April initial bear market bottom (first leg down).

If this ‘dumb’ model of the markets is correct then we should make no new highs from here but rather collapse to a March/April initial bear market bottom (first leg down).

If an anomaly is at hand and the solar max is still ahead or speculation somehow extends further in time, then the next logical peak would be mid-year 2015, likely June 16. However, I rate this possibility as negligible. Look again at the risk measures that changed course Jan 1 2014: they remain in downtrends ever since. Add to these the large range of assets and indicators that peaked June 27 and remain in downtrends ever since too. Then consider the change in market and cross-asset behaviour since the final date, Dec 22, together with that capitulation in sentiment and allocations. This has to be game over, in my opinion. However, if we consider it a game in which central banks can cheat and change the rules, then maybe, just maybe, natural forces can less freely flow through the markets. I don’t think this is likely as central bank members are solar subjects too. However, this is subject to confirmation in a critical real time test in 2014-2015. Market reaction over the next few days to the ECB announcement will be a key tell.

{kind=link}

{kind=link}