Secular bull or bear markets in both equities and real estate are in essence demographic bull or bear markets, with equities and real estate correlating fairly well with each other over time, and in turn with demographics. In other words, slow moving trends in demographics make for the longer term ‘secular’ bull or bear markets in stocks and housing, within which there are cyclical bulls and bears. To enable this relationship in any particular country, certain fundamental conditions are required: sufficient levels of sanitation and education, social discipline and peace, a sufficiently diversified economy and good infrastructure, i.e. what we would generally find in developed countries but may be lacking in positive-demographic but raw frontier nations.

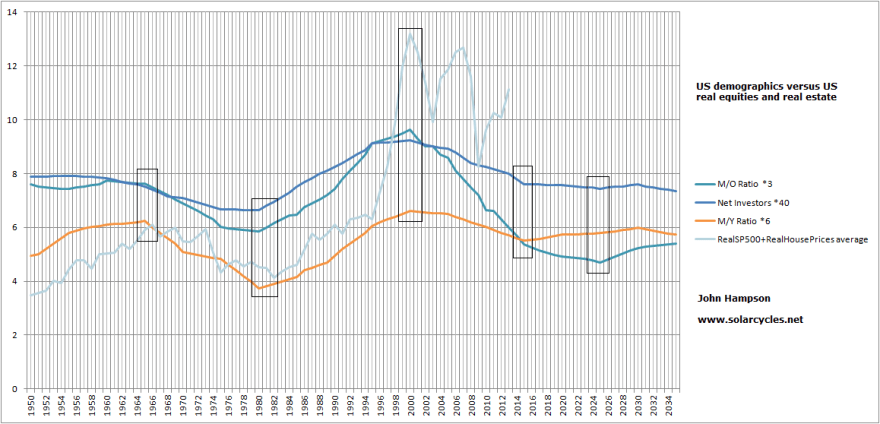

The first chart shows US demographics, using middle-old, middle-young and net investor ratios, modelled against a composite of real stock prices and real house prices. The composite topped along with demographics circa 1965, then bottomed together around 1980, then topped again around 2000.

All three demographic measures swung fairly closely over that 50 year period, which perhaps explains why the composite tracked so well. We might note that the composite peak in 2000 was fairly extreme, suggesting an episode of excess greed that subsequently required wash-out, and also that the secondary peak circa 2005-7 was counter new demographic trends, and thus liable to the steep crash that then followed in the composite.

All three demographic measures swung fairly closely over that 50 year period, which perhaps explains why the composite tracked so well. We might note that the composite peak in 2000 was fairly extreme, suggesting an episode of excess greed that subsequently required wash-out, and also that the secondary peak circa 2005-7 was counter new demographic trends, and thus liable to the steep crash that then followed in the composite.

Looking forward, net investors stops falling as of around this year, the middle-young ratio bottoms circa 2015 and the middle-old ratio after 2020. This suggests there is scope for new ‘secular’ bull markets in stocks and housing, but it is unclear when they might kick off. Note though that the composite has again made a counter rally to the demographics from 2009 to 2013, which suggests another leg down in real terms would be appropriate before any new secular bull. Note also that we don’t see strong uptrends or all three measures united again, like from 1980-2000, which suggests future secular bulls in the USA may not be as powerful.

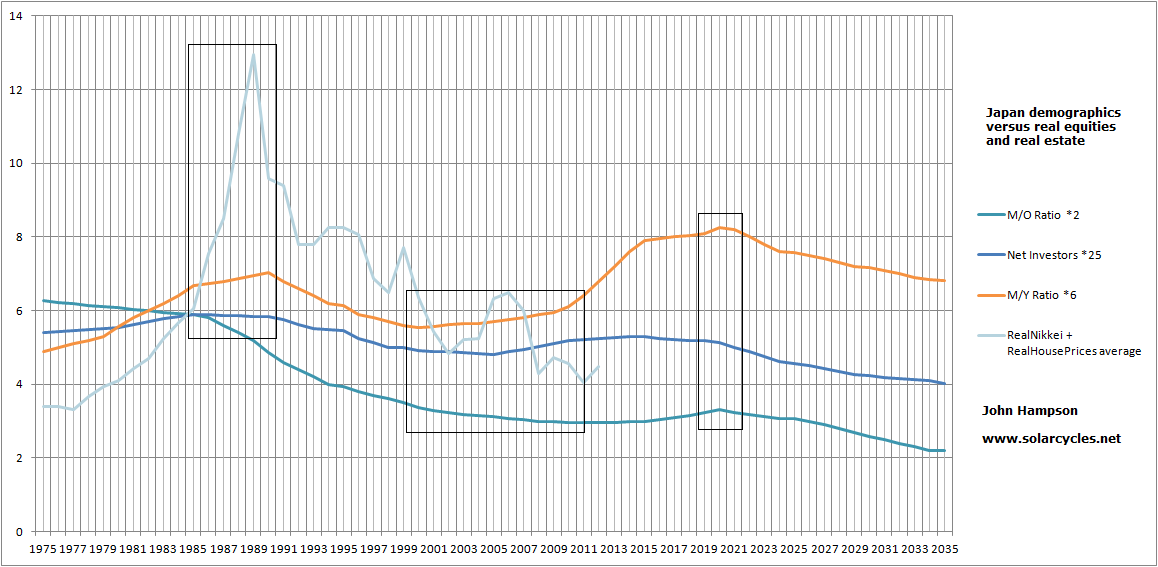

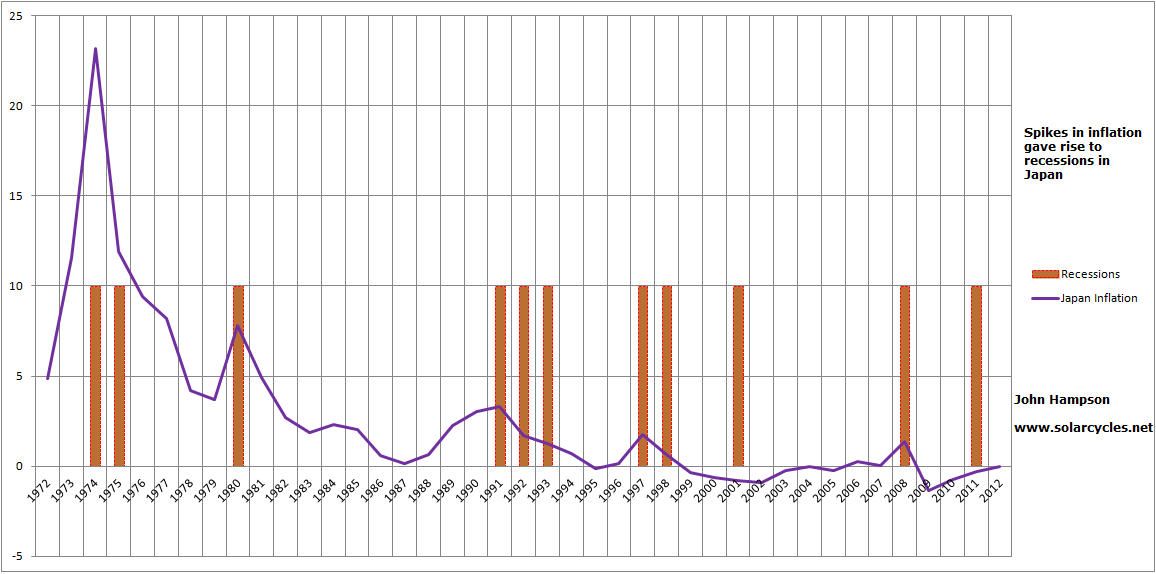

Next up is the same chart for Japan, but not stretching back as far in time. Again the equities and real estate composite peaked with the demographic measures in the late 80s, and again with a fairly excessive greed peak and subsequent harsh wash out.

The composite has belatedly taken off again only in the last 6 months, with net investors and middle-young having turned positive again around 2002, continuing until around 2020. There has thus been a 10 year delay in Japanese stocks and housing in turning back up with demographics. However, this period coincides with the wash-out negative-demographic period in the USA, the largest economy in the world, which suggests Japanese risk asset markets were infected by situation in the USA.

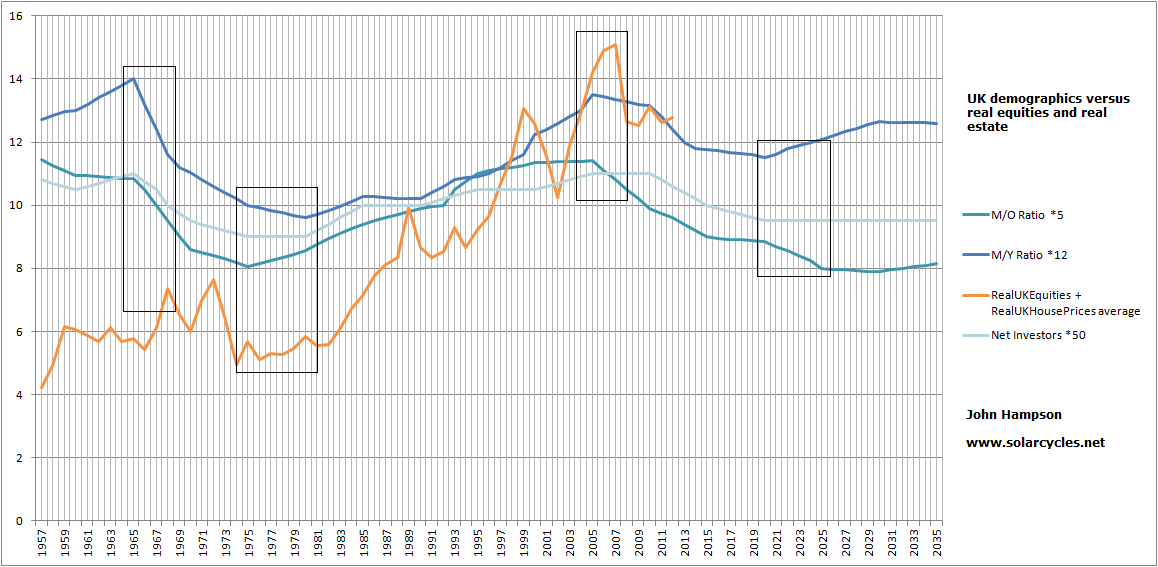

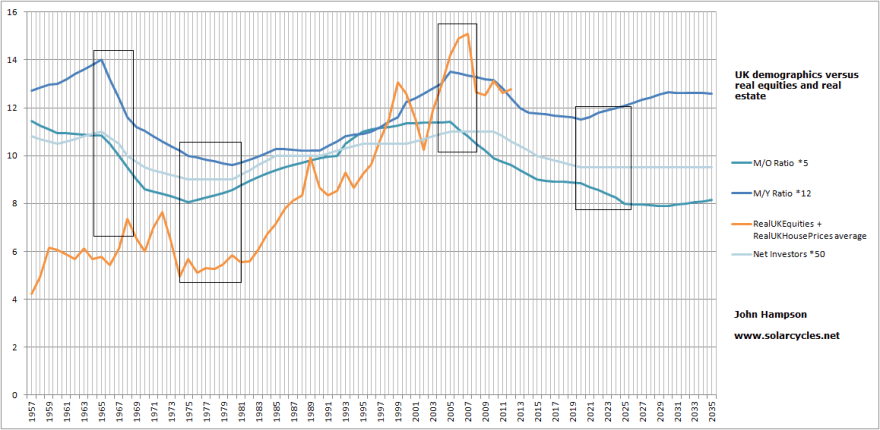

The third chart shows the same modelling for the UK. The demographics for the UK topped out in the late 1960s and the stocks/housing composite made a top around then but went on to eek out a slight higher peak circa 1972. So again we saw belated adjustment as this was then rectified to a combined low in the late 1970s. Demographics and the composite then made a strong secular bull until the 2000s.

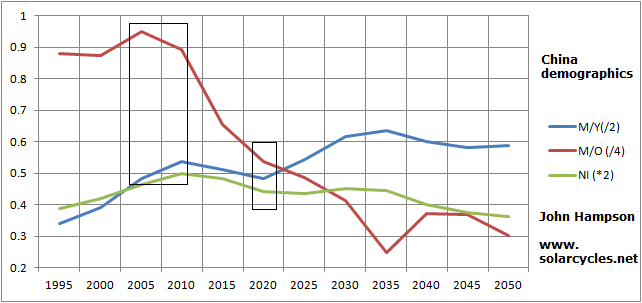

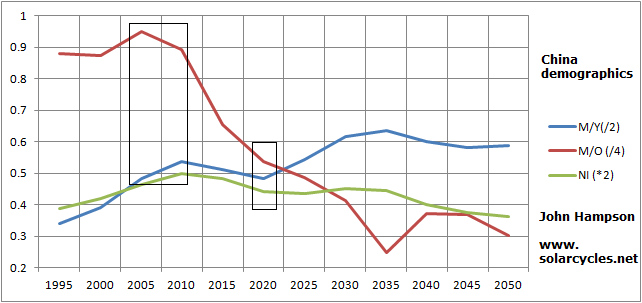

The peak in the composite for the UK was around 2007, in line with the demographic peak. For the UK this peak was higher than in 2000 and justified by the demographics. The US peak circa 2005-7 was a lower peak than in 2000 and fittingly its demographics were already on the decline. The later demographic peak in the UK was reflected in other major nations and thus possibly ‘infected’ the USA in pulling the US composite up into a decent 2005-7 peak despite the falling demographics. Looking forward, the UK faces demographic downtrends until around 2020-2025 which suggests a secular bear could be in play until then. However, we need to look at the demographic positions of the other major economies of the world so see the overall picture as evidence of cross-infection and lags are at work. To that end, here are the three demographic measures as used above for China, Germany, France and India.

China made an excess-greed peak in equities and real estate circa 2007, tying in with the topping of demographic trends. It now faces difficulties until circa 2020.

Germany faces similar headwinds until around 2020, or potentially even around 2035.

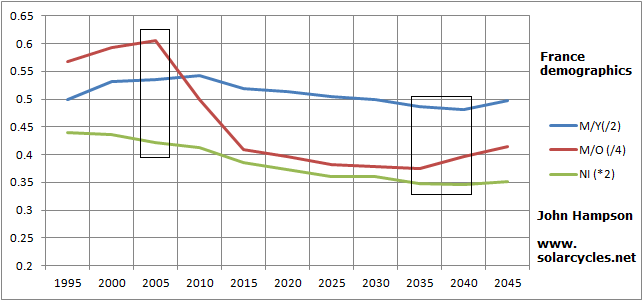

France is in a united downtrend until circa 2035.

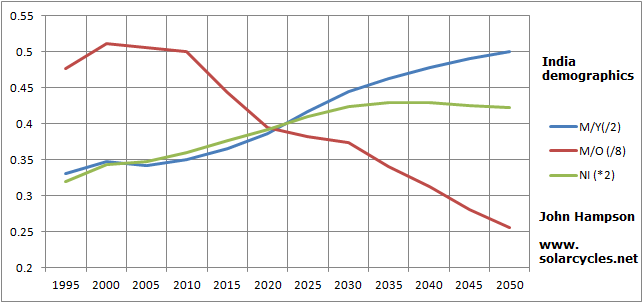

India is in an ongoing uptrend in two measures, and the middle-old ratio is a little deceptive as India is starting from a very small older population which is growing. For that reason there is a downtrend in the ratio, but it is still fairly benign compared to the more developed countries above.

The chart for Brazil looks very similar to India, ongoing positive, and if we round out the top 10 major economies of the world, Italy is similar to the other European countries with unfavourable demographic trends, whilst Russia has a positive period from now until circa 2025. The caveat for Russia would be that is may not score as highly on the criteria for the relationship to fulfill, for example the stock market quite closely tracks the prices of energy commodities due to the economy not being as diversified.

So with a view of the next 10 years, the largest economy in the world, the US, has fairly flat demographics and is unclear. The second economy, China, is at risk of a secular bear until circa 2020 but then improves. The third economy, Japan, is in a positive period until around 2020, and is in fact playing catch up to demographics. The fourth largest economy, Germany, is negative until around 2020 but has better potential after that. The UK, France and Italy are part of an unfavourably-demographed Europe, whilst Brazil and India are ripe for long bull markets.

In short, from now until around 2020 Japan, India and Brazil are in positions to rally but China and most of Europe are pulling down, with the USA unclear. From circa 2020 to 2025, Germany, USA and China are in better positions for secular bulls, whilst Japan’s window closes. On balance, that suggests a global secular bull with many participants has better odds in the second part of the decade, so the question is what is going to happen between now and then, i.e. select secular bulls in those countries with favourable demographics only, or ‘infection’ from the larger economies to the others.

Most of the major economies of the world, listed above, enjoyed positive demographic trends from circa 1980 until circa 2000 or 2005. That made it easy for the world to embrace a collective strong secular bull on the whole. Looking forward, there is a large pool of countries with strong demographics for the next 20 years, but they are largely ’emerging’ countries, including Brazil, India, Turkey and Malaysia. That suggests there will be a global shift in performance over time away from the old developed world to these countries and others. However, currently, USA, China, Japan and Germany make up almost half the global GDP, which means their fortunes affect the world. It will take a long time for the emerging countries to alter this in a significant way.

This is my suggestion. If US stocks and real estate (and in turn global stocks and real estate) can make another cyclical bear leg down to bring the composite down to the demographics, and put them at better relative cheapness to other assets, by circa 2015, then there will be better odds of a global secular bull beginning 2015 and strengthening from around 2020-2025.

Now I need to bring in solar cycles at this point, because something is going on with them, which further shapes the picture.

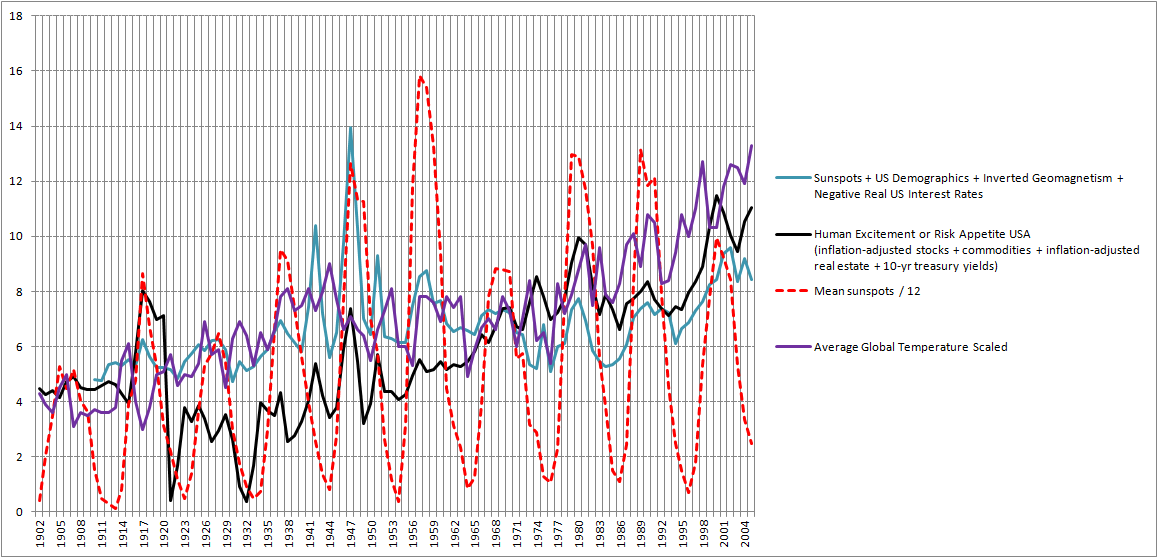

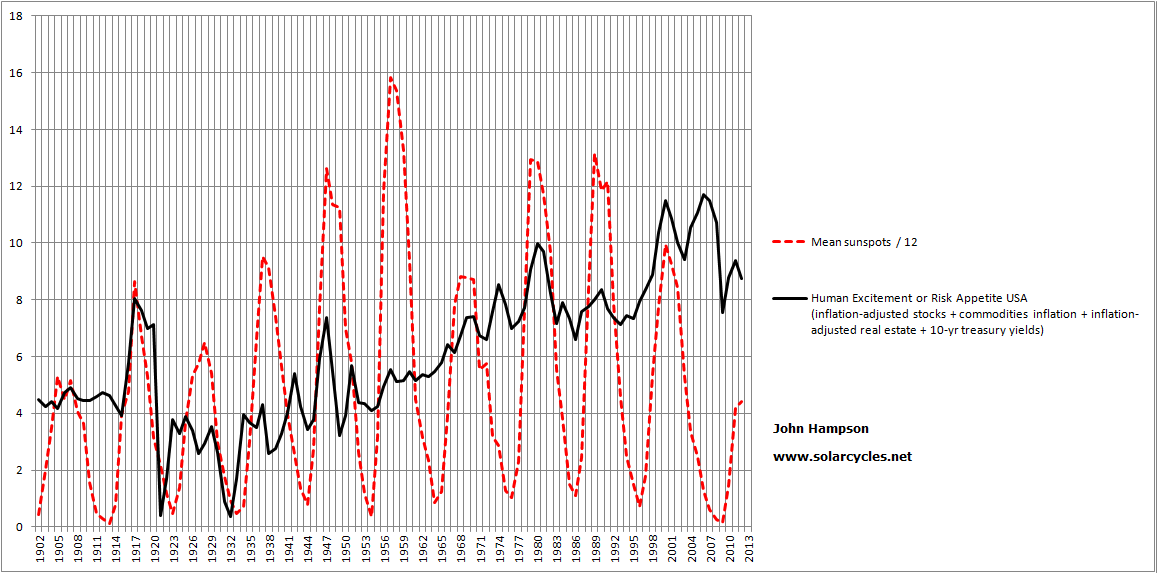

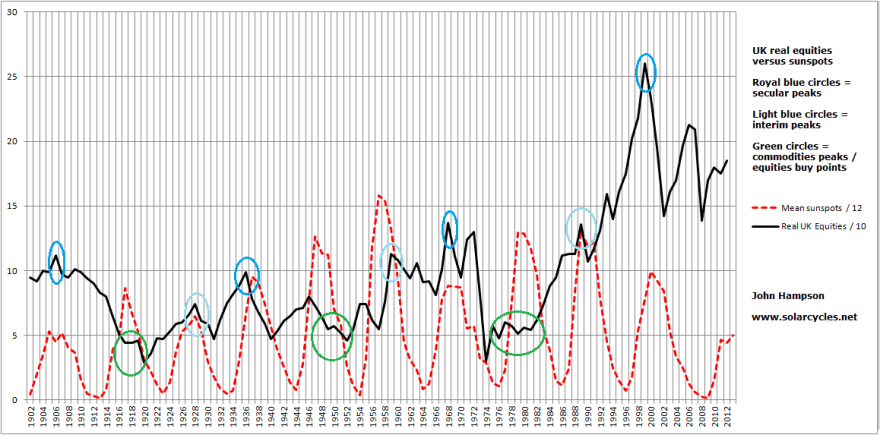

Here is the UK real equities chart versus sunspot cycles. The three major peaks in equities coincided with every third solar peaks. Inbetween interim peaks were made, also at 3-cycle intervals. And commodities also made secular peaks every third solar cycle, which were the buy points for equities.

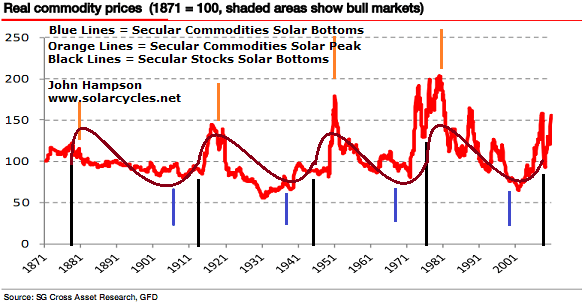

We know the performance in equities largely correlates with demographic trends, and from research in my recent posts, we know that there is a solar cycle influence on demographics. However, is that ‘every third’ solar cycle rhythm just an accident, or is it a ‘natural’ sine wave? The long term real Nikkei chart reveals links with solar peaks but no such repeating rhythm. However, commodities have made a secular bull once again over the last decade, in alignment with the pattern.

We know that over time, real commodities have gone nowhere, and have been no long term investment. They just enjoy bursts of interest.

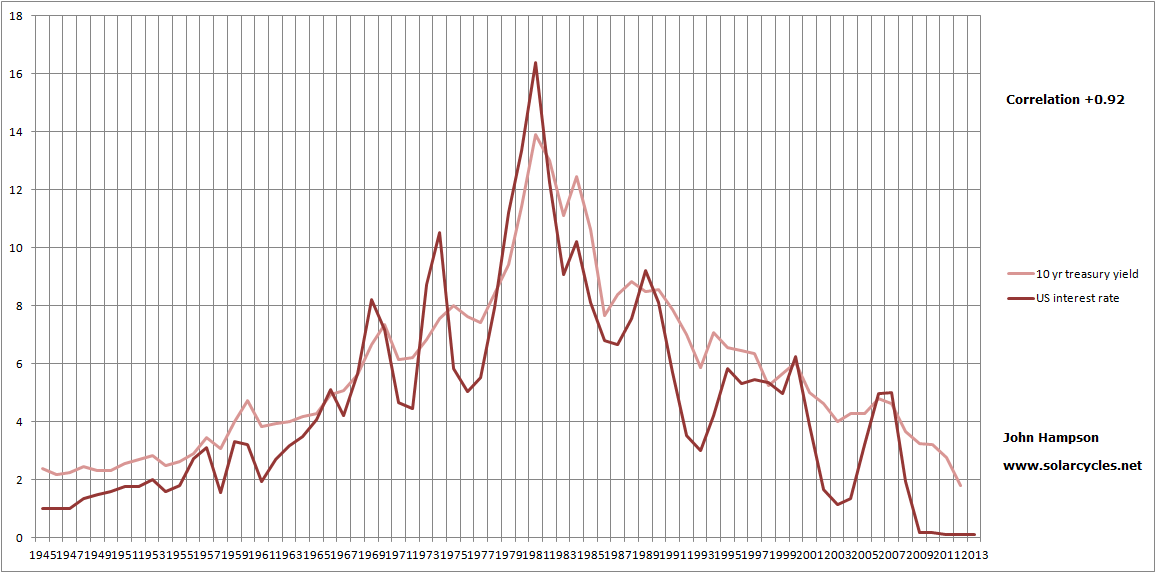

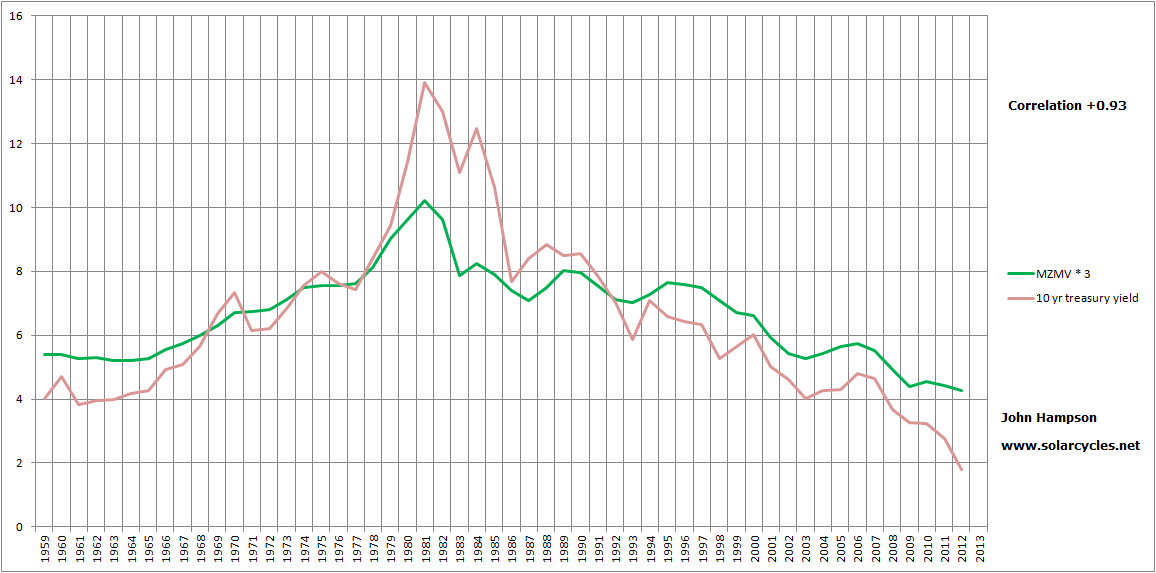

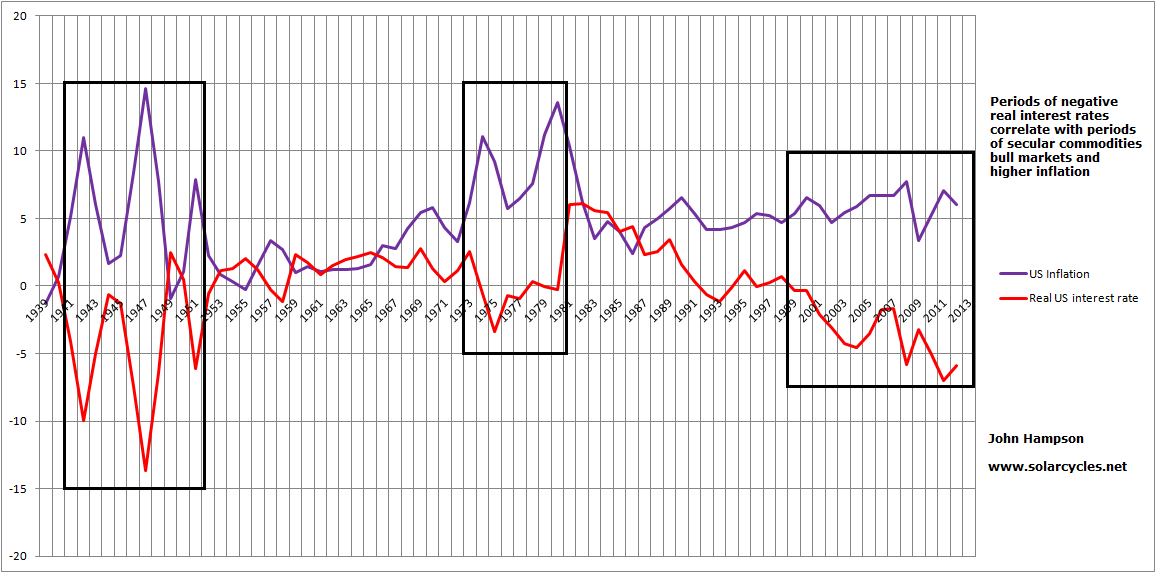

We know that they do not correlate with demographics, but rather tend to make secular peaks and troughs that are fairly opposite to equities. So do they just come into favour when stocks and real estate are out of favour? There must be more to it than that. Real negative interest rates unite the periods in which commodities soared, however, commodities are closely correlated with inflation, so their rises cause the negative real interest rates. In the 1970s interest rates were high, but real interest rates were still negative due to very high inflation.

We know that they do not correlate with demographics, but rather tend to make secular peaks and troughs that are fairly opposite to equities. So do they just come into favour when stocks and real estate are out of favour? There must be more to it than that. Real negative interest rates unite the periods in which commodities soared, however, commodities are closely correlated with inflation, so their rises cause the negative real interest rates. In the 1970s interest rates were high, but real interest rates were still negative due to very high inflation.

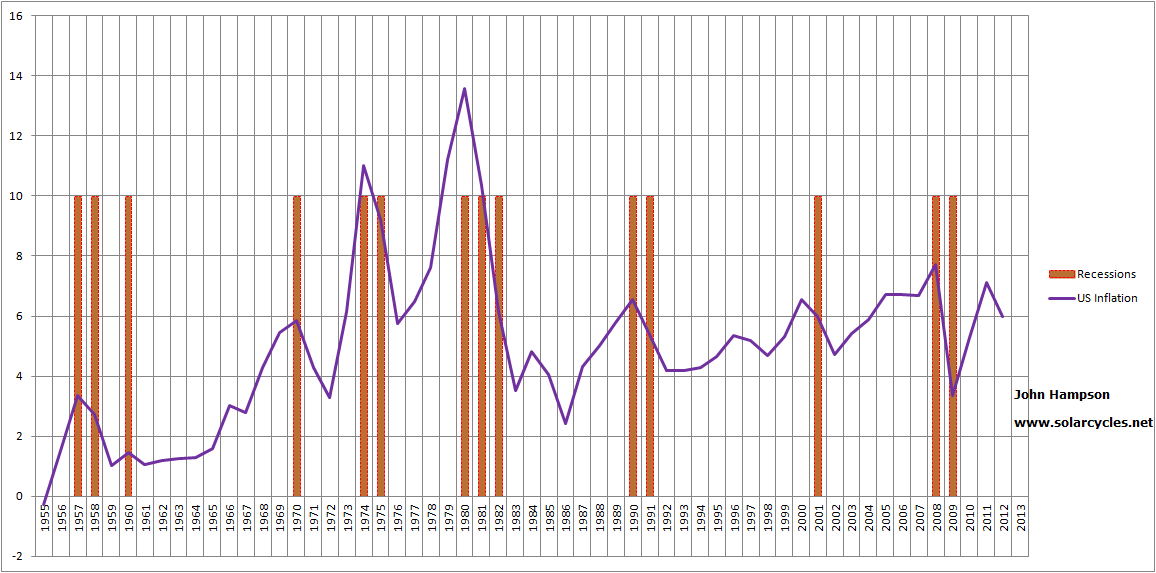

The period into 1917 was similar to 1980: high yields rates and velocity, high commodities and inflation. 1947 similar to today: low yields rates and velocity, high commodities and inflation. Right now we have only mild inflation, but there have been bursts of problematic inflation, particularly in 2008 and 2011. This chart shows those sets of relationships in the US, and the UK experienced very similar.

So the four commodities secular bull periods are only all united by two things: high commodities and high inflation (with the inflation being notably higher than rates, to create negative real rates). As commodities are the key driver of inflation, we are left with one uniting feature: escalating commodity prices. So what causes these periods of escalating commodity prices?

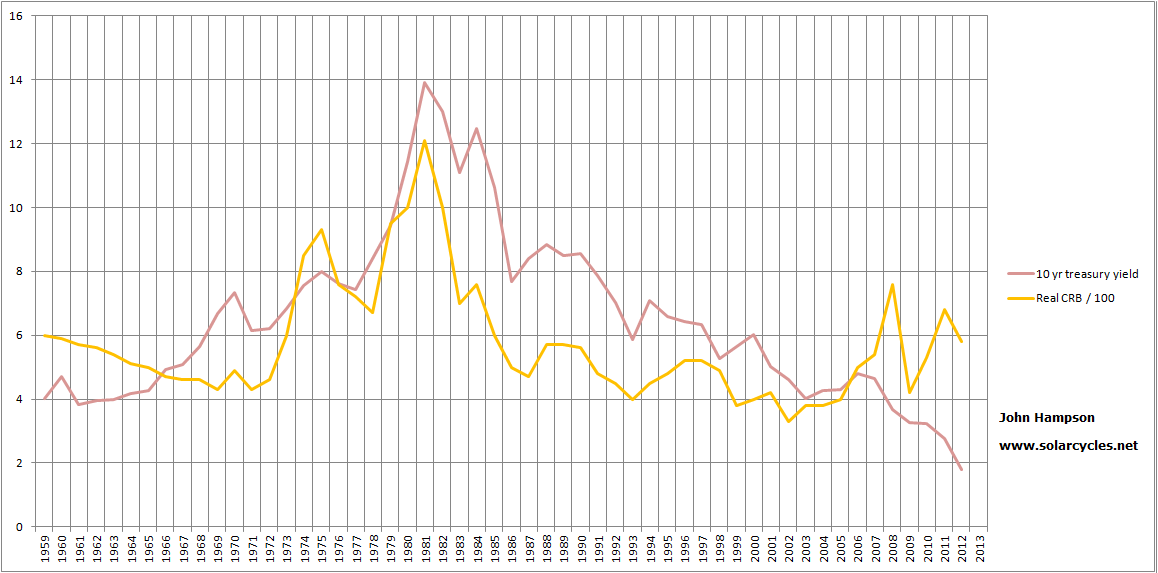

I believe it’s a multi-part answer. Supply lags is one known. It can take 10 years for a new mine or energy field to come into production. That can create a decade-long demand and supply inbalance, as periods of lower commodities demand can close down projects and therefore create problems of inelastic supply further along in time. Commodities come into favour when their relative pricing to other assets is historically low, and this occurs at the end of secular bull runs in stocks / housing (as evidenced in dow-gold or real estate-gold ratios). Demand for commodities can also increase as more countries develop and urbanise,which can occur from economic boom periods. In today’s environment of ultra low rates and yields – similar to 1947 – investors look beyond cash and bonds for returns, putting commodities in favour. Conversely in the 1970s and 1910s, investors looked to hard assets (commodities) as hedges against supply-side inflation. Common to all, stocks and housing were in down trends due to demographic trend changes so commodities then became the go-to investment.

Following a decade long commodities bull market we have reached the point today whereby commodities are relatively historically expensive to stocks and real estate, peaking in this regard so far in 2011, and whereby new supply has been catching up and coming on stream in the last few years. However, real interest rates and yields remain negative and so maintain commodities interest, whilst demographics for the major nations largely remain in downtrends which should keep equities and real estate under pressure to the benefit of commodities. It’s therefore a balanced picture, but recall that commodities have been a terrible long term investment, so if the balance tipped further towards stocks and real estate then we should expect an end to the commodities bull.

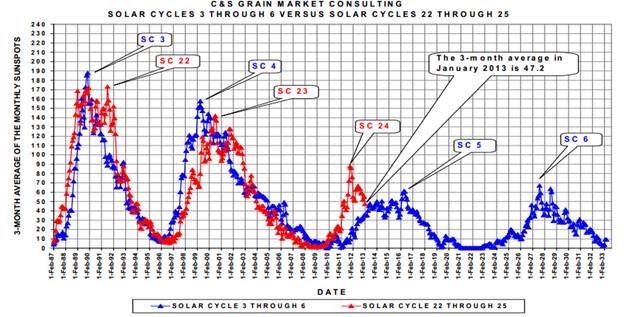

With all that in mind, this is my view on what is most likely to happen. Commodities ought to make one last bull rally, in keeping with solar cycle history: excitement and inflation into and around the peak. Both equities and commodities have a history of making major peaks near to the solar maximums, regardless of cyclical patterns. That should tip the world into a recession and equities into a bear, to take off again from yet lower relative value levels circa 2015 once demographics are bottoming out more in the US. For stocks and real estate to be already in secular bull trends at this point – say, from 2011 – is rather counter the collective demographics. This fundamental downward pressure on stocks and real estate (in certain key countries) ought to reassert itself shortly and money flows ought to move into commodities (for likely one last time) under conditions of negative real interest rates.

If there is another cyclical bear in the US, then as per the cyclical bears of 2001 and 2008, the other major country stock indices are likely to participate – i.e. all moving as one. However it ought to be shallower in those countries with more favourable demographics.

A decent sensitivity.

A decent sensitivity. A pretty good tracking of the model.

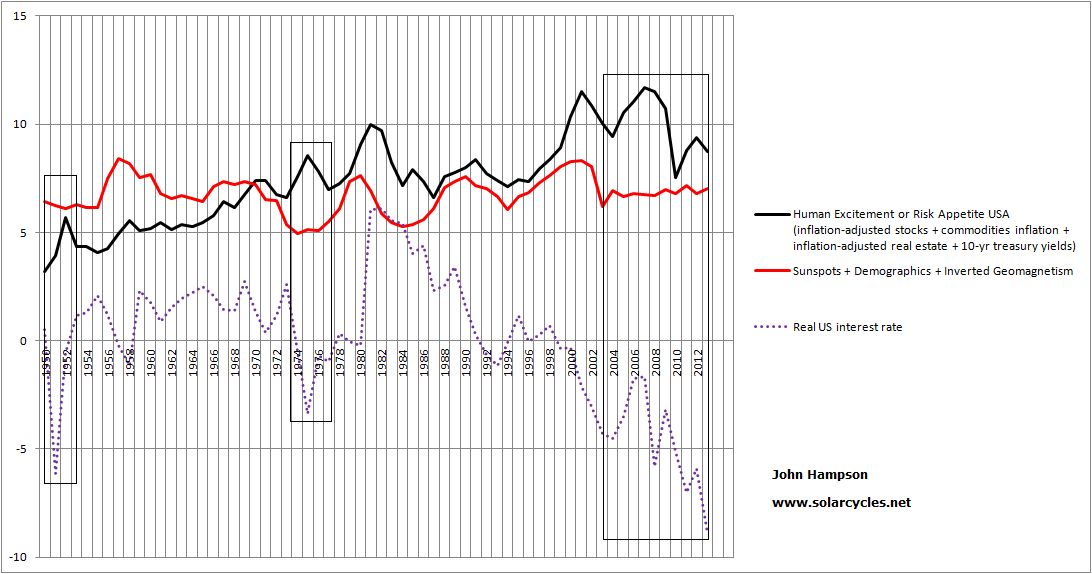

A pretty good tracking of the model. There is now a notable divergence which could spell a trend change in stocks or a topping process beginning imminently. However, rising into the solar maximum has previously encouraged speculation and into the 2000 peak the market pulled away from the geomagnetic model, as the speculation overruled. So two competing things to consider, but in short the low-geomagnetism support for the market has been pulled away.

There is now a notable divergence which could spell a trend change in stocks or a topping process beginning imminently. However, rising into the solar maximum has previously encouraged speculation and into the 2000 peak the market pulled away from the geomagnetic model, as the speculation overruled. So two competing things to consider, but in short the low-geomagnetism support for the market has been pulled away.