I wanted to test the correlations and interrelations on Japan. As it went through a different experience to the USA over the last half a century, did the same correlations in assets and the economy hold true? Data history is more limited than for the US, but sufficient to test. Correlation coefficients over +0.5 are considered strong positive correlations between two datasets, and some datasets have been scaled to share the same chart, where e.g. *3 or /10 is shown. Click on a chart to see it larger.

Firstly, I found the same five-way block correlation between interest rates, bond yields, money velocity, real commodities and inflation. Here are two pairings from that group:

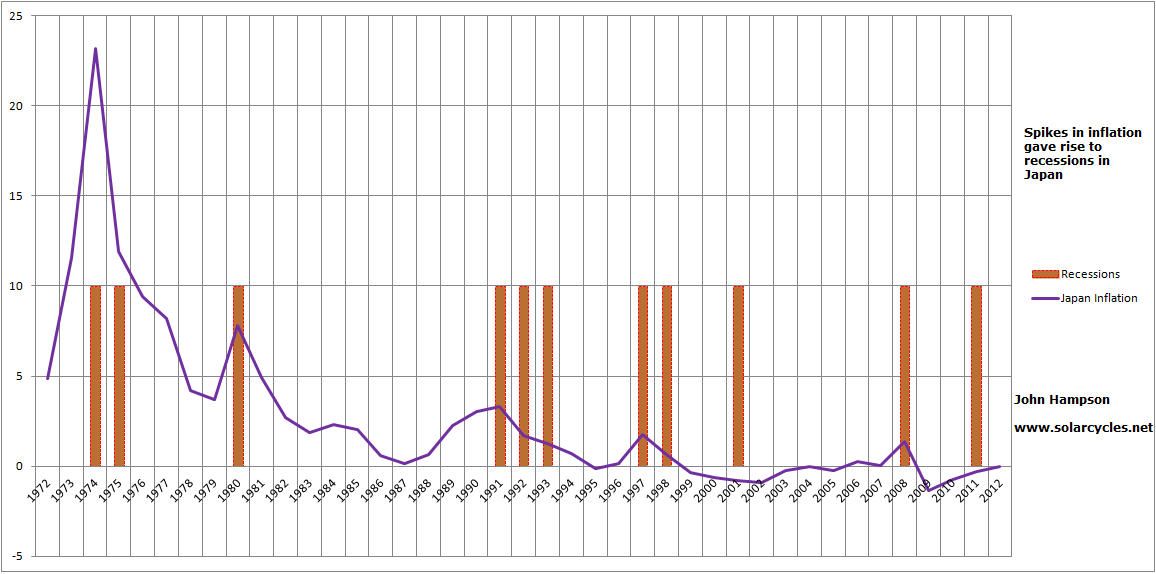

Note that the level of inflation was overall at a lower level than in the US over the last 3 decades but the relationship between real commodities and inflation is still clear.

Note that the level of inflation was overall at a lower level than in the US over the last 3 decades but the relationship between real commodities and inflation is still clear.

As per for the US, I found this five-way block then produced the correlated-two of recession and unemployment. Below it can be seen how recession followed spikes in inflation, even if the spikes were low.

I also discovered the asset pairings are again found in Japan, with bond yields and commodities related, whilst real house prices and real equities go their own shared path. I show here real stocks and real house prices:

Uniting those two assets into a composite in the next chart, demographic trends again appear to have played a key role in their secular trending.

That Japan did not participate in the secular stocks bull through to 2000 and the secular housing bull through to 2005 that the USA did, makes sense in light of the demographic trends in the period from 1990 to 2005. Additionally, the speculative peaks in Japanese stocks and housing circa 1989/1990 (around the human excitement solar maximum of 1989) were fairly extreme ‘greed’ overthrows, which then need time to washout on the other side.

That Japan did not participate in the secular stocks bull through to 2000 and the secular housing bull through to 2005 that the USA did, makes sense in light of the demographic trends in the period from 1990 to 2005. Additionally, the speculative peaks in Japanese stocks and housing circa 1989/1990 (around the human excitement solar maximum of 1989) were fairly extreme ‘greed’ overthrows, which then need time to washout on the other side.

However, demographic trends overall collectively turned up again from around 2005 and should continue positively until circa 2020. Japanese equities effectively made a triple nominal bottom in 2003, 2008/9 and 2011/12, whilst real estate has been basing since 2010, but a sustained rise in risk assets in Japan did not materialise until November 2012 onwards and I believe this sharp move is a belated catch up to the demographics. If 2013-to-date was added to the above chart we would see a significant pull-up in the stocks/housing composite.

Drawing in bond yields and real commodities to make a 4-way risk asset composite, and as per the USA comparing against the quadruple-agent composite of sunspots, geomagnetism, demographics and real interest rates, there is again a notable mapping between the two (again, 2013 should provide a belated pull-up to the model: a divergence being rectified):

Generating the forecast into the future, but with the caveat of using assumptions and historic rhymes, we get this:

Generating the forecast into the future, but with the caveat of using assumptions and historic rhymes, we get this:

The prediction will be refined over time to validate or invalidate those underlying assumptions and patterns, but the overall uptrend is due to the demographic trends that stand to boost risk assets until circa 2020 and then the next solar maximum should continue the upwards pull until circa 2025, implying there is a good chance of an overall secular bull in stocks and real estate in Japan for the years ahead.

The prediction will be refined over time to validate or invalidate those underlying assumptions and patterns, but the overall uptrend is due to the demographic trends that stand to boost risk assets until circa 2020 and then the next solar maximum should continue the upwards pull until circa 2025, implying there is a good chance of an overall secular bull in stocks and real estate in Japan for the years ahead.

I therefore suggest that the government’s recent doubling down on stimulus is in fact not required, and so it has the potential to supercharge proceedings. So far the yen has dropped sharply, bonds yields have taken off and inflation expectations have risen significantly:

Source: BusinessInsider

Source: BusinessInsider

As Japan is a net commodity importer, the sharp drop in the Yen pushes up import prices for energy and other resources, so they already have commodity price inflation despite commodities recently underperforming. If commodities now rise, as per my forecasts, then there is a danger that Japan suffers major commodity-based inflation, which should be correlated with money velocity soaring, and an inflationary feedback spiral develops. The government should then accordingly raise rates, but cannot raise them too fast or too far because of the record debt servicing. That, collectively, is why there is a hyperinflation risk. If problematic inflation does erupt then eventually the risk is of a stock market crash. However, until then (and maybe it does not come to pass), stocks are likely to do well based on demographics and a belated catch up, and they should also perform well under ‘some’ inflation. So the question is whether stocks will pullback sufficiently to offer an opportunity to get in or add more. I am long the Nikkei, but do not feel comfortable adding more on the long side at this point when stocks have risen almost 100% in 6 months. Conversely, despite the trade doing very well at the moment, I do not wish to take profits as I believe the major rally to be justified, and expect more gains ahead. So I stay put for now and we’ll see how things develop.

Japan’s ageing workforce has an enormous deflationary impact on the economy. In the last inflationary episode back in 2007-08, Japanese CPI was still fairly low by Western standards. Due to the reluctance of Japanese governments to allow high immigration, the demographic picture is likely to be fairly accurate into the future. Japanese GDP for Q1 was decent, but to prove that Abenomics is putting Japan on the right track, we’d need to see growth maintain this kind of momentum into year’s end. The wealth effect might end up creating a virtuous circle, as a result of the strong rally the Nikkei has posted since 2012.

On the subject of commodity prices, there’s been a recent scandal involving possible price rigging of Oil for well over a decade. The overall accusation is that prices have been forced upwards, which in turn has pushed up inflation and eroded consumer purchasing power.

Thanks Pete

Models updated this morning.

The sunspots rally of the last couple of months looks more promising for a solar peak ahead: https://solarcycles.files.wordpress.com/2012/02/a299.png

Geomagnetism divergence is now apparent on several stock indices:

John, thanks for the update; especially at this critical juncture. I had read about

those events and also wondered if it might be the first positive sign for your solar peak ahead theory.

A contributor brought this to my attention today.

Not In Kansas Anymore by John P. Hussman

An excerpt:

“The chart below highlights each point in history that we’ve observed the following conditions: Overvalued: Shiller P/E anywhere above 18; Overbought: S&P 500 at least 7% above its 12-month average, within 3% of its upper Bollinger bands on weekly and monthly resolutions, and to capture a mature advance, the S&P 500 well over 50% above its lowest point in the prior 4 years; Overbullish: a two-week average of advisory bulls more than 52%, and advisory bears less than 28%. Rising yields: 10-year Treasury yields higher than 6-months earlier. The instance in 1929 is based on imputed sentiment data, as bullish and bearish sentiment is correlated with the extent and volatility of prior market fluctuations.”

Ready for the results?

http://www.hussman.net/wmc/wmc130520.htm

And there’s more, much more. It’s a masterful piece.

Investors Intelligence jumped to 55.2 this week. That should be worth a 1000 pt correction.

I’m reminded of a crash of a Boeing 737 jetliner that occurred in the early 1990’s in Pittsburgh. When the pilot took the plane off of autopilot, which they do when they’re preparing to land, the plane rolled over and flew into the ground at over 300 miles per hour. After reviewing the data, Boeing crash investigators said that during the flight the autopilot had continued making small adjustments to the flight control surfaces such that the airplane was in a very unstable condition at the time the autopilot was turned off. May have been only a slight gust of wind that hit the plane at that critical moment that caused it roll over and dive into the ground.

CB’s continue to tweak and tweak, attempting to fine tune their economies, but by doing so they may moving their economies deeper and deeper into very unstable conditions. A slight gust of wind, and their economy rolls over and flies into the ground at 300 miles per hour.

Hi John,

Do you know the name of the paper/book by Milton Friedman that you have mentioned a few times – where he writes investors did not trust the rally because of government support back between 45 and 47?

Thank you in advance.

Dan

It was a paper written in 1963 titled A Monetary History of the United states, 1867-1960, authors Milton Friedman and Anna Schwartz