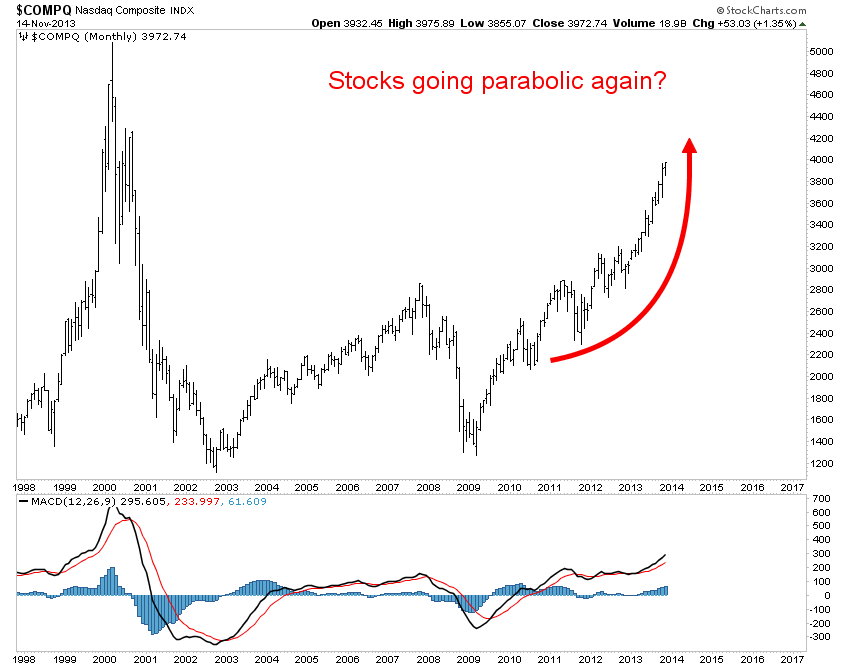

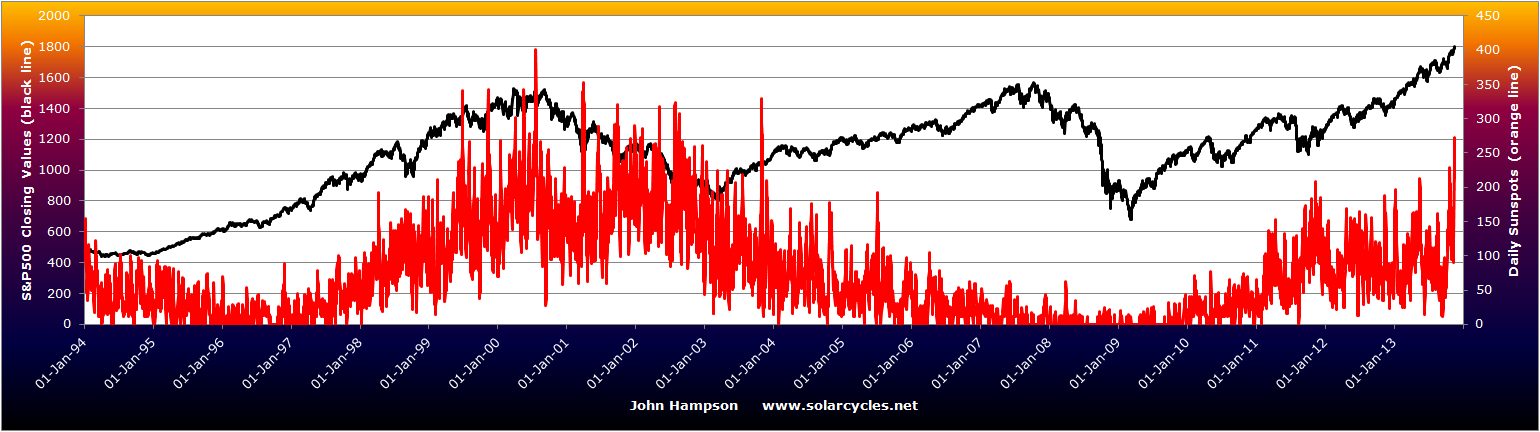

If the smoothed solar maximum for solar cycle 24 is occurring around now, and equities are the speculative target of solar inspired human excitement, and the Nasdaq remains the leading stock index, then we have evidence of such a speculative mania in the Nasdaq composite with a parabolic gaining traction, as referred to in the last post. Below is the longer term Nasdaq composite showing the last two solar peaks closely correlated in timing with Nasdaq peaks:

Underlying Source: Stockcharts

Underlying Source: Stockcharts

Nasa predict the solar pole flip will be complete by Nov/Dec 2013, which typically signifies the solar max is complete, whilst SIDC have a sunspot projection showing a max around April 2013. Drawing those together with the possibility of a correlated Nasdaq peak, we have a window for the Nasdaq to peak out, in parabolic fashion, between now and June 2014.

If we look at the biggest four Nasdaq composite companies by market capitalisation, Amazon has at this point gone to crazy valuations under a steep parabolic, whilst Apple, Google and Microsoft are more contained. Google is the most expensive of the three at 23.9 forward p/e, whilst Apple and Microsoft are at 12.2 and 14.1 respectively. IF the Nasdaq is heading for a parabolic speculative peak (solar maxima in the past have typically correlated with parabolics in assets) then I suggest we probably would need at least another of these leaders to go to dizzy valuations like Amazon.

Now to lessons from Japan, and specifically, can the US and Europe avoid deflation or is it unavoidable?

By my research, Japan’s ‘lost decade’ was due to demographics, and with US (since circa 2000), Europe (since circa 2005) and China (since circa 2010) demographics now united in an unprecedented downtrend, I believe deflation is inevitable. BUT, Japan did make some ‘mistakes’, in belatedly adopting QE, and only keeping loose monetary policy once the economy entered periods of deflation, withdrawing once back into inflation. I say ‘mistakes’, because that is up for debate. Austrians and Monetarists argue that stimulus actually has a negative effect, for example government intervention quashes private economic activity and savers and retirees see their income quashed under ZIRP so actually cut consumption. Regardless, Japan’s massive QE and government spending programmes even failed to inflate their economy against a positive global backdrop of strong growth in the 1990s. Today, 10 out of the biggest 13 economies of the world are in demographic downtrends, making for that aforementioned unprecedented collective negative backdrop.

Analysts point to several other contributory factors for Japan’s failure.

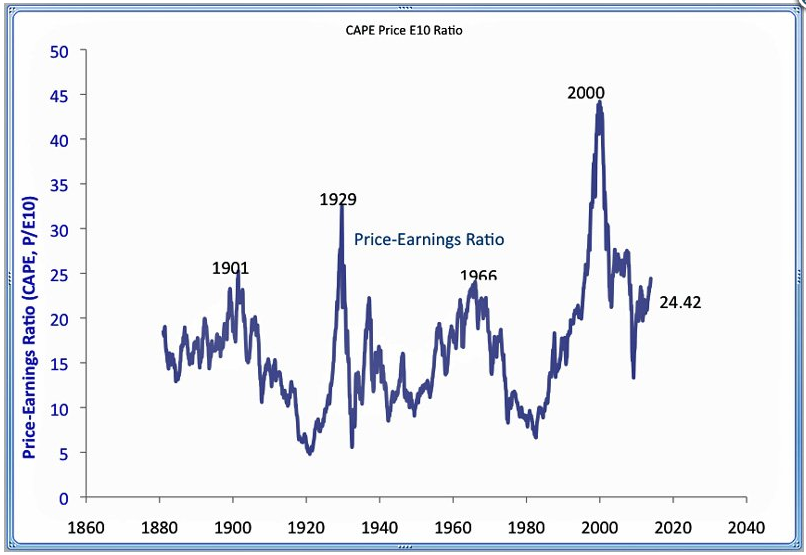

One is the starting point of a bubble in stocks and housing prices, i.e. excesses that needed washing out. We can identify something similar leading us into the current situation for US and Europe, with a stocks bubble in 2000 and a housing bubble around 2006.

Two is associated with one, as the bursting of the bubbles encouraged households and businesses thereafter to pay down debt and not borrow, and to do so despite interest rates being brought down to negligible levels. Today we see the same occurring:

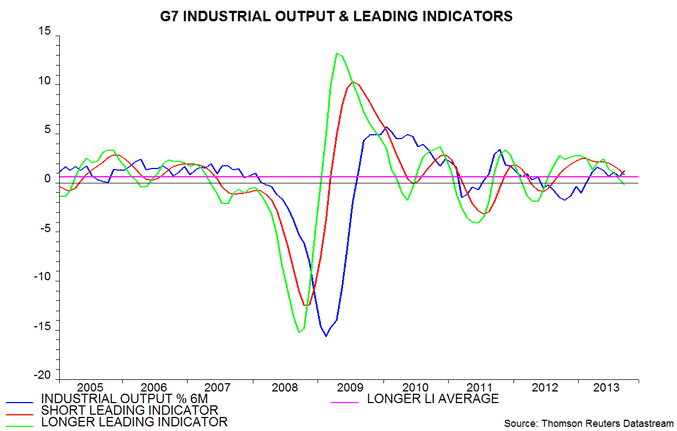

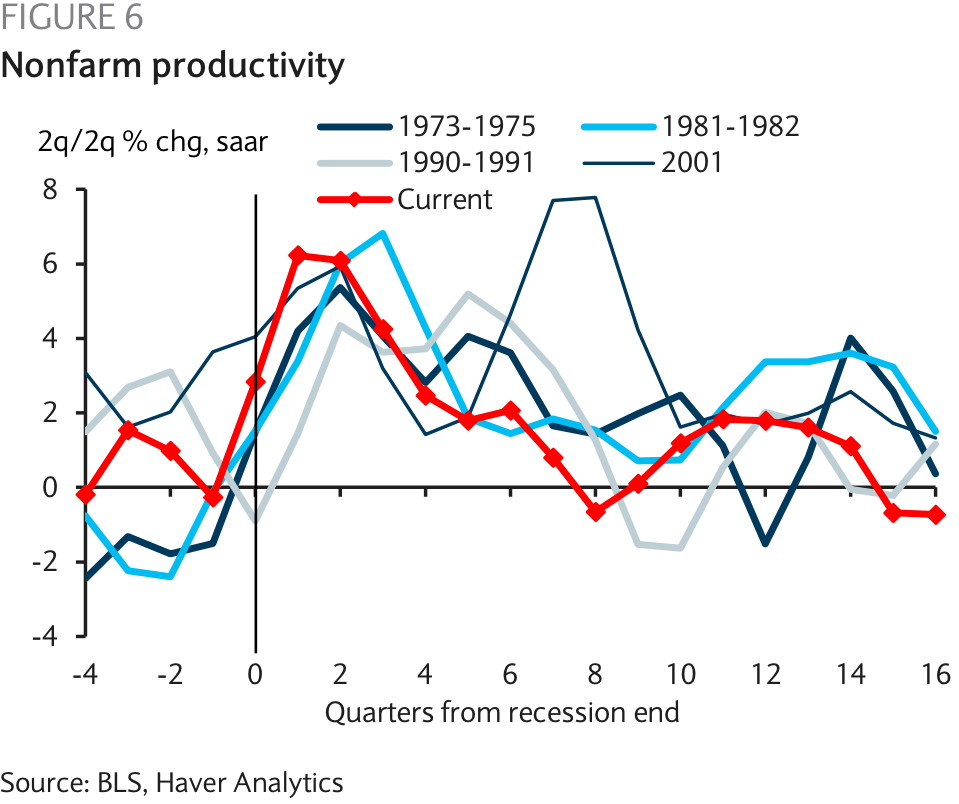

Three, low productivity, low capital expenditure and excessive capacity. Again, repeated today:

Three, low productivity, low capital expenditure and excessive capacity. Again, repeated today:

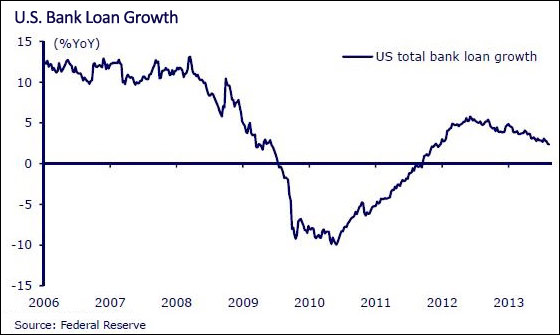

In fact, there is a theme in that US data of some key economic indicators being lower currently than at historic recession start points, and you can find the same phenomenon in data ranging from real US GDP growth to real US retail sales growth to National Activity (Chicago Fed). On which note, an inverted yield curve has historically been a reliable leading indicator of recessions in the US and the health of the curve suggests no recession on the horizon. However, the suppression of yields by the Gov/Fed essentially makes this indicator redundant, as Japan three times entered recession with a normal yield curve under the same suppression intervention.

In fact, there is a theme in that US data of some key economic indicators being lower currently than at historic recession start points, and you can find the same phenomenon in data ranging from real US GDP growth to real US retail sales growth to National Activity (Chicago Fed). On which note, an inverted yield curve has historically been a reliable leading indicator of recessions in the US and the health of the curve suggests no recession on the horizon. However, the suppression of yields by the Gov/Fed essentially makes this indicator redundant, as Japan three times entered recession with a normal yield curve under the same suppression intervention.

Four, persistent fear. The financial crisis lingered in the mind, causing consumers to continue to distrust banks and feel pessimistic about the economic future, which translated into holding back on investment and spending. Below we similarly see how US consumer confidence has never really recovered since the 2008 financial crisis (whilst Eurozone consumer confidence also languishes negative, with the latest reading -15.4):

Source: Dshort

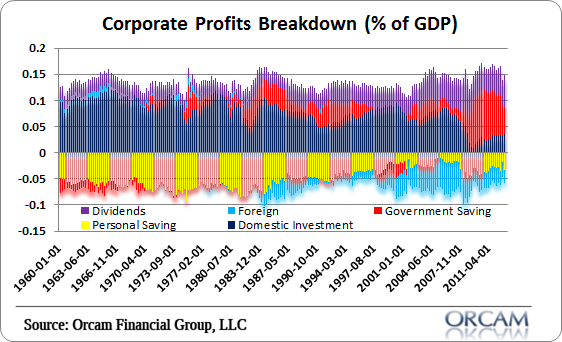

And I shared charts in previous posts showing how private investment has dried up whilst the government has backfilled.

In short, there are broad similarities between 1990s Japan and the US and Eurozone today. But what actually tipped Japan into deflation? It didn’t happen straight away, it occurred once Japan attempted fiscal consolidation, trying to contain its ballooning public debt and high government spending. Which is where the US is today: back at the debt ceiling / fiscal cliff, aware it needs to reduce the massive QE debt ballooning. But it is in a QE trap, which Richard Koo explains like this:

The QE “trap” happens when the central bank has purchased long-term government bonds as part of quantitative easing.

- Initially, long-term interest rates fall much more than they would in a country without such a policy, which means the subsequent economic recovery comes sooner.

- But as the economy picks up, long-term rates rise sharply as local bond market participants fear the central bank will have to mop up all the excess reserves by unloading its holdings of long-term bonds.

- Demand then falls in interest-rate-sensitive sectors such as automobiles and housing, causing the economy to slow and forcing the central bank to relax its policy stance.

- The economy heads towards recovery again, but as market participants refocus on the possibility of the central bank absorbing excess reserves, long-term rates surge in a repetitive cycle I have dubbed the QE “trap.”

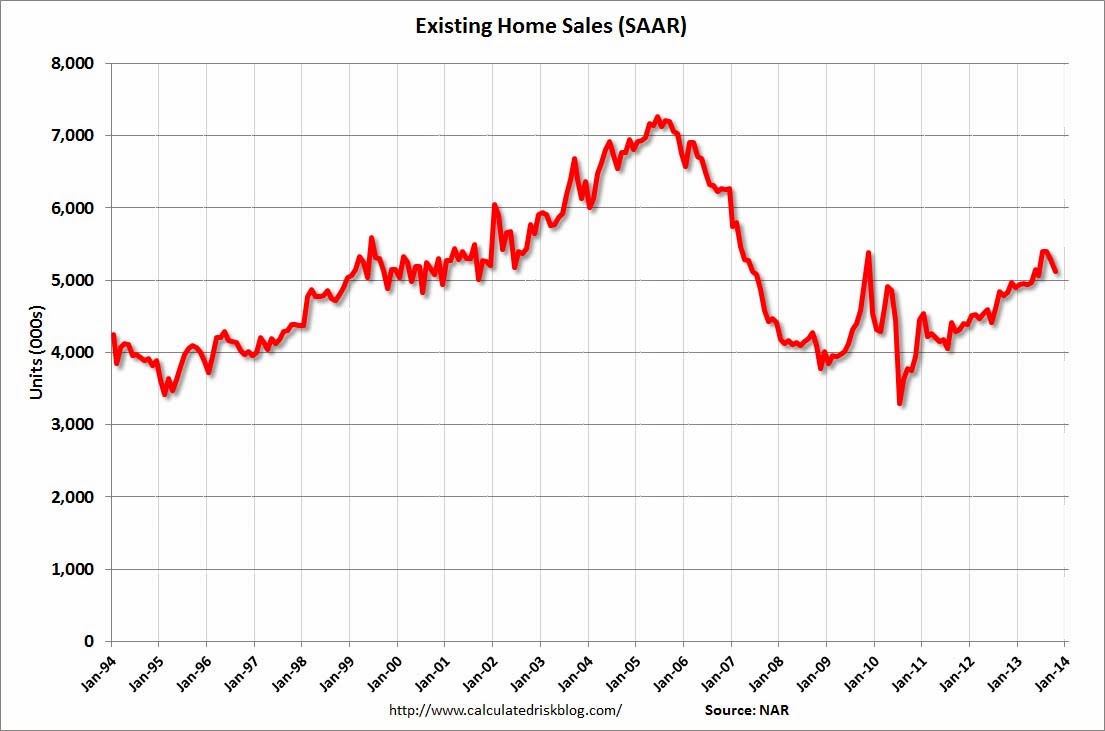

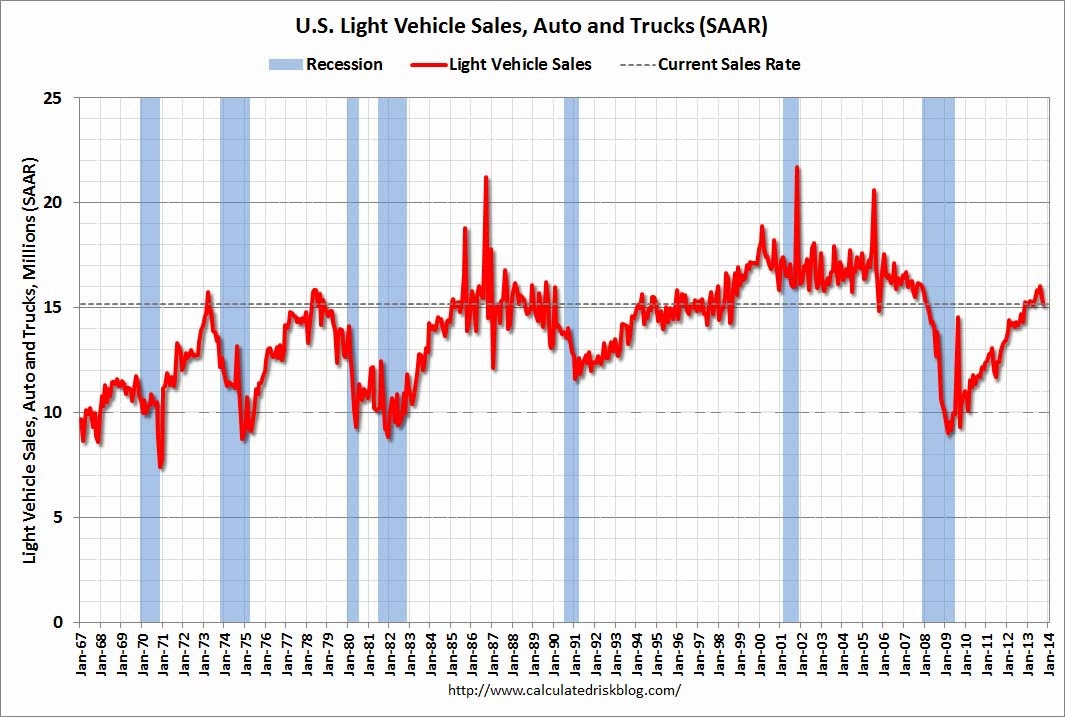

This year we have seen a sharp recovery in bond yields, in line with the second point, and if he is correct then we should now be seeing a reversal in automobile and housing sales, which the data from the last 3 months in the US does show:

Source: Calculated Risk

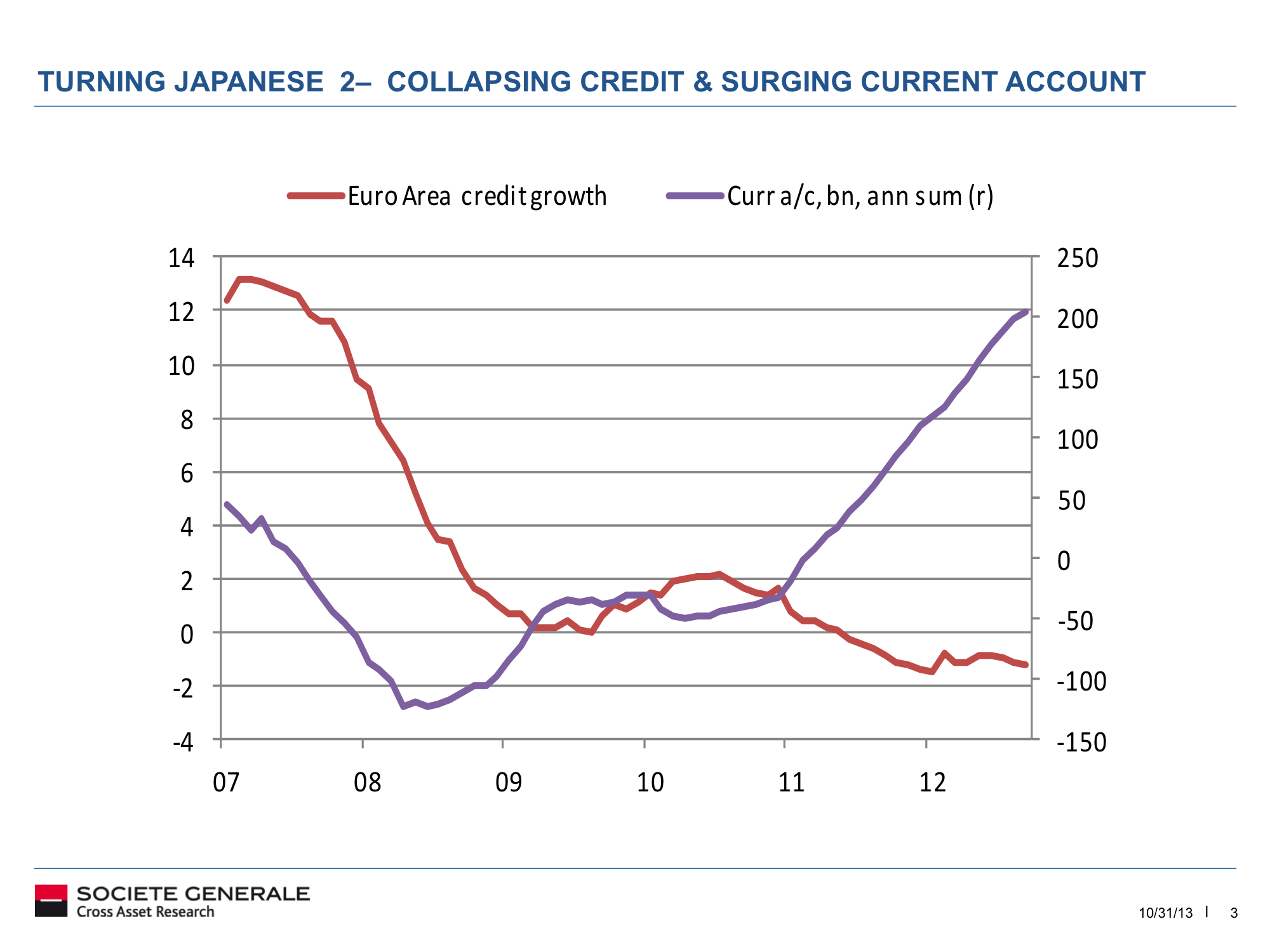

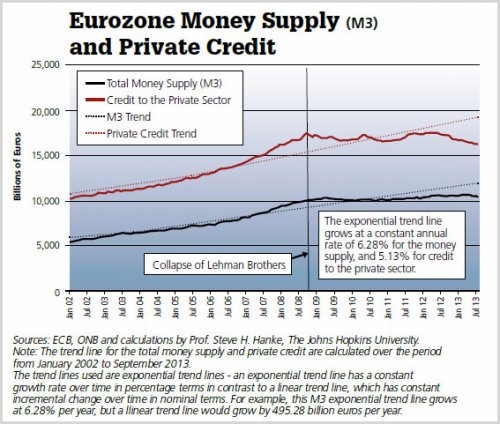

Meanwhile, the Eurozone is perhaps going to pay the price for its cautious central bank policy response since 2008 (compared to US and UK) by entering deflation first. Money supply has not grown in that period and narrow money as a leading indicator suggests the tentative recovery in Europe may be about to fizzle out again.

Source: MoneyMovesMarkets

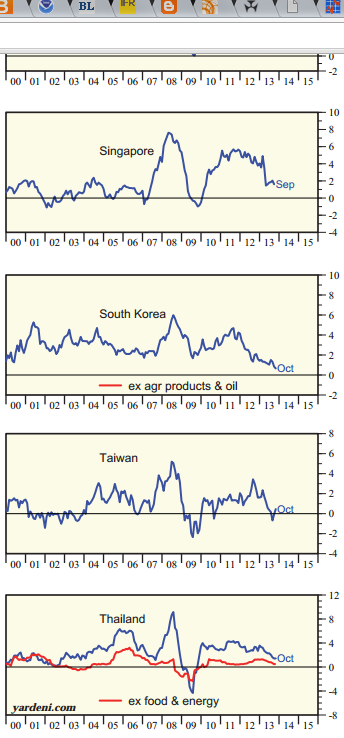

Source: Yardeni

Chinese monetary trends also show a slowdown into 2014, whilst producer prices have been in deflation over the last twelve months. Add China to the European Union and the USA, and that’s more than half the world’s economy in a collective demographic downtrend, before including other similarly demographically challenged major countries such as Canada and Russia. I just don’t see how this won’t escalate into a global deflationary recessionary feedback looping. If Japan couldn’t achieve it when collective major economy demographics aside itself were positive in the 1990s, and we see similar developments in data above as occurred in Japan, then it would seem the world economy is destined to slip into a deflationary recession. A QE taper and fiscal consolidation as part of debt ceiling renegociation as we turn into 2014 could provide the extra momentum on that path in the US, whilst for Europe any additional interventionary measures may well be too late at this point (and are of questionable effectiveness anyway).