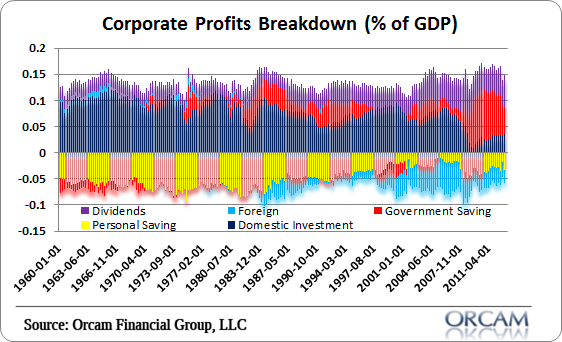

Here is a chart from Gary Tanashian through SlopeOfHope’s charting facility, which could be argued legitimises the current steep ascent in US stocks:

Parabolic money pump, steeply rising corporate profits, and therefore equities going vertical (on a long term view).

Parabolic money pump, steeply rising corporate profits, and therefore equities going vertical (on a long term view).

In fact the sharply rising monetary base is directly contributing to those rising corporate profits, as government spending (debt) has been the key driver of corporate profits since 2008:

Therefore, if the US Fed begins to withdraw stimulus, disappointment in corporate profits is likely, as the chart shows the traditional profits driver of private investment has collapsed and not recovered over the last few years. Once again, this fits with demographics, and we should therefore not expect private investment to ramp up significantly again any time soon. So it’s in the hands of the US government and Fed. Maintain or increase stimulus, corporate profits should keep rising; decrease or end stimulus, corporate profits should retreat.

Therefore, if the US Fed begins to withdraw stimulus, disappointment in corporate profits is likely, as the chart shows the traditional profits driver of private investment has collapsed and not recovered over the last few years. Once again, this fits with demographics, and we should therefore not expect private investment to ramp up significantly again any time soon. So it’s in the hands of the US government and Fed. Maintain or increase stimulus, corporate profits should keep rising; decrease or end stimulus, corporate profits should retreat.

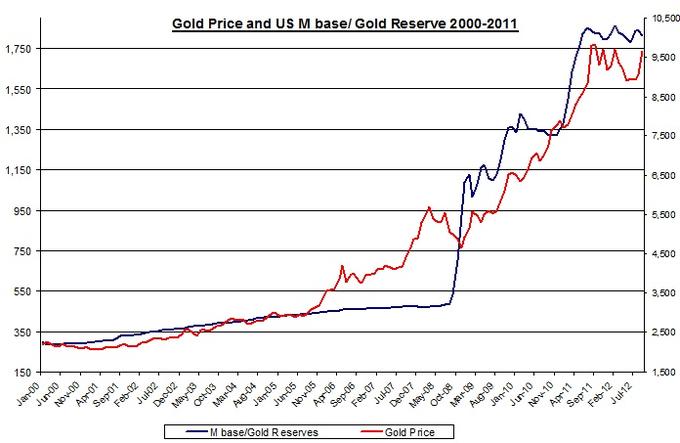

Turning to the monetary base, equities are not the only correlated class. In fact, gold has had a tighter correlation, until 2013. Here 2000-2012:

Source: Fool.com

Source: Fool.com

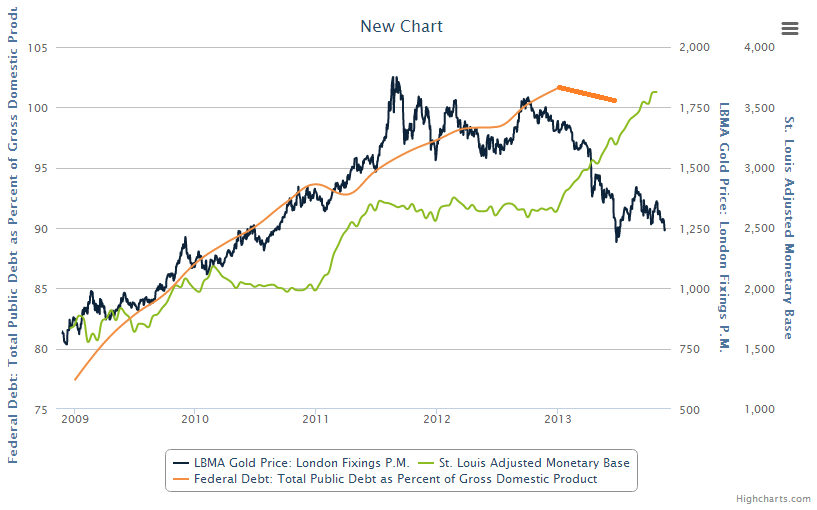

Gold displayed a similar correlation with government debt, also until 2013.

Source: RockSituationReport

Source: SlopeCharts

The first shows the debt limit, which will be back on the agenda soon, and surely must keep rising, whilst they retain the need to stimulate, which they will due to demographics. The second shows debt as a percentage of GDP, which actually fell back a little in H1 2013 (my extension on the chart). The reason for that was better than expected economic growth and a trimming in certain areas of government spending. Total debt continues to rise at a historically rapid rate.

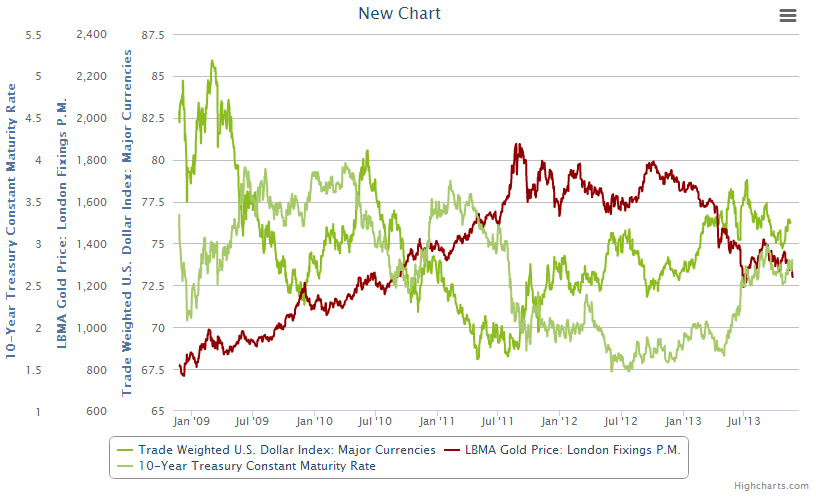

So are these correlations with gold broken, or is gold set to come back? One more chart shows that the US dollar and treasury yields have been largely inversely correlated with gold and the pair strengthening for much of 2013 has been a key factor in gold’s decline:

Source: SlopeCharts

Source: SlopeCharts

In my opinion, gold’s relations with money supply and debt levels are logically sound, and both money supply and debt should continue to rise into the future under the demographic trends. I therefore I expect gold can restore its bull market if the US dollar and treasury yields tip again into sideways or declining trends. If the US economy strengthens and a little inflation is restored, then this is unlikely to happen and gold will remain in the doldrums. However, demographics and debt suggest the Fed will have to keep fighting to maintain growth and keep deflation at bay (taper disappointment, yields suppression, new measures to attempt to inflate), which could bring about such a reversal in fortunes.

I still expect equities can go a little more parabolic first, under a typical solar maximum speculation push. However the warning flags already in place of dumb/smart money, trading volumes, margin debt and trading credit balances, and overvaluations (e.g. Q ratio) suggest it is most likely limited in duration and size. I would go with something like this from trader Moe:

Source: Trader Moe

Source: Trader Moe

A further 10% gain in a rapid time, with a catalyst being collective major breakouts in the major global indices, to get to some crazy extreme indicator readings, and a subsequent termination. My first checkpoint is the start of December, because the 3rd is the new moon and as of the 4th geomagnetism is forecast to ramp up again. If equities can rally hard and fast into that point, with a spread of indicators flashing, then I would suggest that could be the earliest point for declines to set in (barring any external shocks). If, however, equities can rally through the seasonally strong Xmas period, and solar intensity stays high into the beginning of 2014, then the next checkpoint would be early January.

Here’s a nice piece from Sy Harding with more data and interesting reflections to add to the debate: http://www.streetsmartpost.com/2013/11/23/the-market-is-not-in-a-bubble/

Thanks HighRev

lol on Sy though, the guy has been one of the biggest bears out there for a couple years and “now” he says no bubble? good contrarian indicator I’ll guess moving frwd.

“In by far the majority of cases the market had simply become overbought and over-valued in relation to economic conditions and earnings and needed those excesses to be corrected.

That is the current situation. ”

That is why I say I think a recession is looming in the USA for 2014 or has already started (or personally but numbers are manipulated) never ended from 2009.

By the surprised stock buy back wasn’t mentioned. Had the 2007-2009 great recession crisis not occurred and stock had remained where they were at in 2007. Given average annual gains, where would they be today? If the currency is devalued such that more fiat currency is required to purchase same stock, does that not alter volume? Shares remain same but the price psychology impacts volume. Any solar cycles charts that show volume vs. cycles? I guess really only impacts price weighted indexes.

John, almost 2 years since I’ve been following you now. Always great stuff. May I point out that we are seeing some unbelievably interesting periods in which stock indices aren’t looking all that much different from other periods in time or moreover, when “surgically adjusting” the markets, similar patterns tend to appear in price action.

Please have a look – http://positiveexpectedvalyou.blogspot.com/2013/11/surgical-abstractions.html

Thanks Ryknow. Your megaphone mirror particularly caught my attention.

I’d like to see the patterns you’re talking about, but the black ground combined with the very thin lines on the charts makes it impossible for me to read. Suggest either white or light gray background, or use thicker lines on the charts. 🙂

Ditto!

All models updated this morning

My point ow view is that the current structure is similar to upward wedge Dow Jones 1909-16-19, with the altered sit. 4-5 years,150%, instead 2-3 years 100% or the 1974-80 S&P referred Dow Jones.

@apanalis

Thanks Antonio

John, there seems to be a continued appetite for risk at the moment if the Carry Trade is anything to go by with regards to the Yen (and their CB’s current monetary policy stance). Many currencies vs the Yen are hitting multi-year highs and breaking out and some of those have plenty of above headroom to go before hitting any resistance of any note if these breakouts were to hold (GBP/JPY being one – if 160 holds, next at 200..?)

Looking at the charts, from the turn of the millenium there seems to be some correlation whereby the latter half of the DOW rally from 2002 (2005-2007/8) may have been aided with the Yen Carry Trade. Are we now in the latter half of this 2009 rally where the Carry Trade steps in again (2012 – maybe reaching 2015/16..?) The VIX remains at complacently low levels for the time being.

(Not ruling out a swift USD/JPY wind change at anytime but there are similarities and considerations).

Thanks Bootle. Maybe – but wasn’t the yen carry trade of old because of the big rate differential between Japan and the rest of the world? USA and Europe have since joined it at zirp.

Unless those investors are anticipating a rate rise in the US at some point.