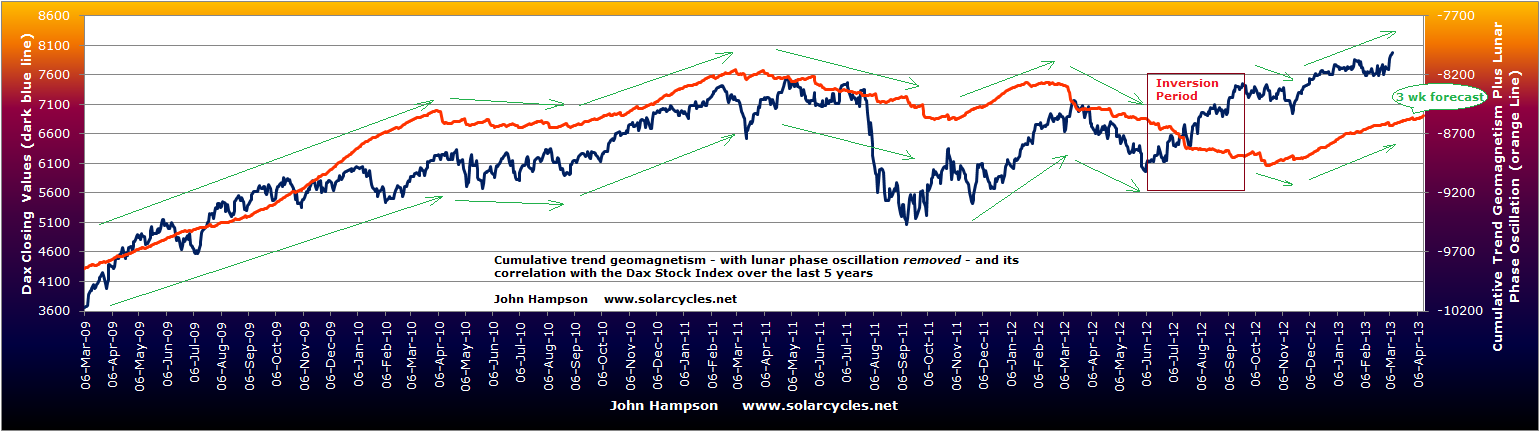

In my last post I suggested that using lunar phase oscillation would increase the probability of a trade. There are several papers that demonstrate this lunar edge in the markets, and underlying this is a body of research relating lunar phases to moods. The period into and around full moons can bring about pessimism in humans, and this endures despite the advent of artificial lighting. The period into and around new moons is conversely often one of optimism.

To verify the relationship in the markets for myself, I split the lunar month into the two opposing periods and studied data from the last 20 years (which covers multiple cyclical bulls and bears within secular bulls and bears) to assess any difference in returns between buying at the start of the positive lunar period and closing at the end of it, to buying at the start of the negative lunar period and closing at the end of it. Here is the summary of results for four indices:

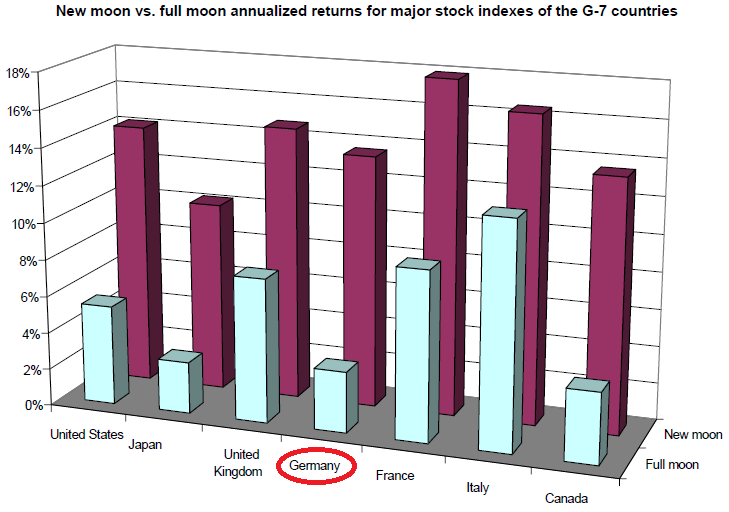

All three stock indices plus the commodities index displayed a lunar edge when totalling returns over 20 years, which means there was relatively more buying-up of pro-risk assets into and around new moons, compared to full moons. The commodities index displayed the weakest edge over the period, so I suggest lunar oscillation is best pursued through the stock indices, and of those, Singapore and Germany revealed the greatest differential. This is in line with the findings of Dichev and Janes, who also identified greater lunar differential in the Dax and Straits compared to some other indices.

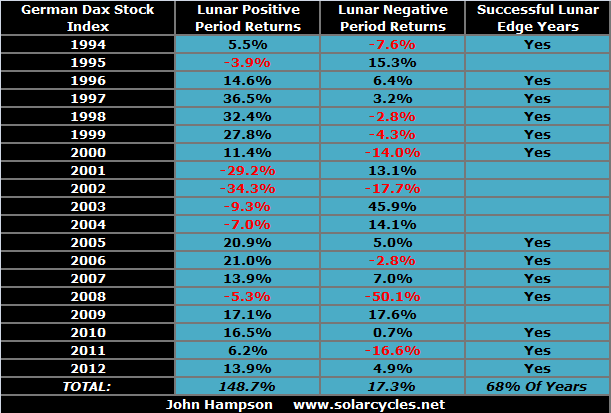

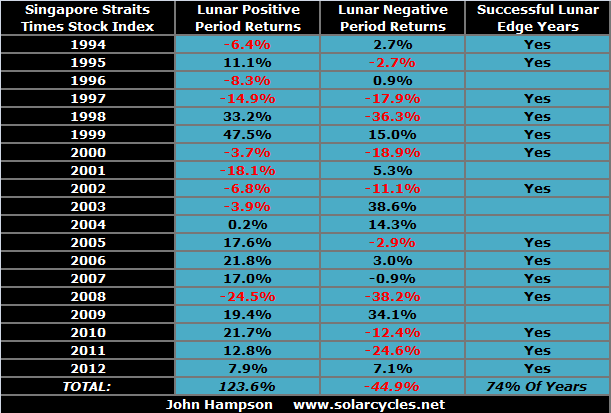

I don’t think it’s overstating it to say that the lunar edge in both the Dax and the Straits is pretty massive and compelling. Understand that a lunar month differs from a calendar month so that new and full moons move through the months over the years. That means we are not confusing calendar phenomena here, such as end of month or quarter window dressing. In the case of the Dax, almost all the 20-year return came from within the positive lunar periods. Nonetheless, it would still have been better to buy and hold for 20 years than only participate during the positive lunar periods, as there was an extra 17% on offer in the negative lunar periods. However, in the case of the Singapore stock index, not only would ‘long’ participation restricted to the positive lunar periods have returned more than buy-and-hold, but additionally shorting the lunar negative period would have added even more to overall returns.

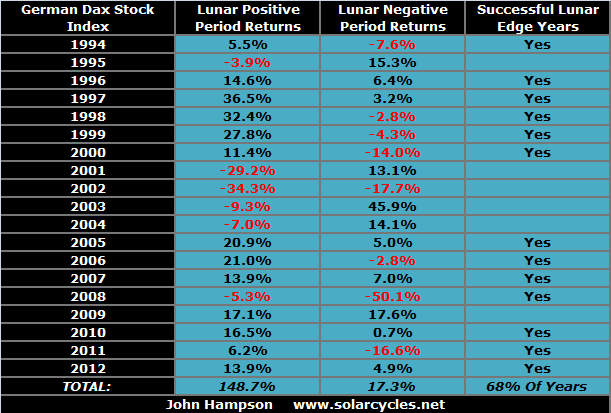

To return to my opening comments from the last post, nothing works all the time, but some things work most of the time. Lunar phase oscillation is such a phenomenon. It takes persistence through successes and failures to draw out the lunar edge, but the edge is real and profitable. The next table breaks down the Dax returns by year, revealing how the 132% differential built up. As can be seen, not all years demonstrated a positive lunar edge, and the gaps in returns varied year to year.

Drilling down one level further, if I show a sample year from Singapore’s history with an impressive differential, it can be seen that not all lunar months within the year demonstrated a positive lunar edge, but most did.

So some years fail, and some months fail, but most years and months successfully return a lunar edge. This fits with my expectations, because lunar phasing influences market sentiment but other phenomena are also influential in stock market performance. So we shouldn’t expect ‘without fail’ but ‘more often than not’.

I suggest there are two trades to consider. The first trade would be a pair on the Singapore Straits: long the positive lunar fortnight, then short the negative lunar fortnight (this aims to capture the negative return made over 20 years into and around full moons). The second trade would be just long the positive lunar fortnight on the Dax, staying out of the market during the negative period (this aims to capture the biggest nominal return of all the indices over 20 years, made on the positive lunar fortnights by the Dax). A ‘failure’ month or year then depends on which of these trades we are studying – i.e. the failure is in a negative differential between the two periods or the failure is in a negative nominal return in the positive lunar periods.

Let’s take the Dax trade first: long only during the positive lunar periods. 68% of years made a positive return. 62% of lunar months made a positive return. The total return over 20 years was 149%. The worst run was 4 years of negative returns: from 2001 to 2004. The worst run within any year was 5 consecutive lunar months of negative returns. What these ‘worst run’ stats reveal is that anyone mechanically trading this idea would have had to endure some significant drawdowns that we would ideally like to avoid. So are there any patterns in the failures? Yes, the failures are largely concentrated in the cyclical bear markets (as we might expect). If we were to only trade the Dax positive lunar periods during the cyclical bull markets of the last 20 years, avoiding the cyclical bears, the returns would rise from 149% to 240%. Whilst this is an impressive increase, it involves correctly calling cyclical tops and bottoms and patiently sitting aside the cyclical bears – both easier said than done. Nonetheless, this is supporting evidence for my suggested highest probability trading technique: trading long stock indices during the positive lunar periods during cyclical stocks bull markets.

Let’s turn to the Singapore ‘twin’ trade: long the positive lunar periods and short the negative lunar periods. 74% of years produced a positive differential. 60% of lunar months returned a net positive percentage, going long into and around the new moon and then short the full. The total return over 20 years was 169%. The worst runs were 2 years of negative consecutive returns, and 7 consecutive lunar months. Again, were there any patterns in the failures? Nothing significant that I could draw out. No seasonal patterns, no concentration of note during either cyclical bulls or bears (the Straits suffered an additional bear 1996-1998). Just sometimes the lunar edge differential didn’t work, but most of the time it did. If we were to change this trade to going long only during the positive lunar periods and only during cyclical bull markets – staying the rest of the time out – then the returns would be around 170%, so no notable improvement on a mechanical ‘twin’ trade regardless of bull or bear.

What about shorting the negative lunar periods during cyclical bears, and staying out otherwise? Again, this would involve being able to correctly call the start and end of the bears, but even with that assumption, I found that the returns are less than if we stayed short for the duration of the cyclical bears, rather than staying out during the positive lunar periods.

So returning to my ideas for highest probability trading, what if we look at returns during cyclical stocks bulls but additionally filter on those periods when the geomagnetic trend was up and when stocks were not overfrothy (suffering overbought and overbullish readings). This gets a bit more difficult to draw out retrospectively, but I can do this for the last 4 years. The result is we would have participated in 21 positive lunar periods (effectively just a quarter of the time active in the market, the rest of the time sitting out). 19 of those would have produced a positive return (i.e 90%), producing a 47.1% gain in the 19 winning periods and a 1.5% loss in the two failed periods. Clearly, this is a high winning rate and although patience would be required to sit out of the market three quarters of the time, the technique would be to apply large exposure when these trades arose. The difficulties in applying forward are correctly assessing whether we are in a cyclical bull or bear and identifying changes in the geomagnetism trend and assessing when overbought and overbullish apply. I believe that is all possible, but it is to some degree an art.

To be clear, I am not suggesting sitting out of the markets for entire cyclical bears, making no money. The idealised trade in my terms, the trade of highest probability, may only be available during cyclical bulls under specific circumstances and parameters detailed above and in the last post, however this does not preclude making trades of lower – but still good – probability, and going forward I will continue to look for opportunities at all times. However, this research has confirmed to me that there are specific trades out there that are worth pursuing with significant funding, and I intend to announce them when they arise and record their progress and success on my site.

Specifically, I am looking to capture and draw together lunar oscillation, geomagnetic trends, cyclical bear or bull trends, sentiment and buying/selling extremes, and I aim to take such trades on the German Dax and Singapore Straits for their sensitivity to lunar oscillation, and also on the SP500 for its sensitivity to geomagnetism. There are several permutations of trades within this: a repetitive twin trade on the Straits (alternating being long positive lunar fortnights and short negative lunar fortnights), a long trade on the Dax only during positive lunar periods within a cyclical bull, and a long trade on the SP500 for the duration of a geomagnetic uptrend. So watch this space.

Source: Conference Board

Source: Conference Board Source: Ed Yardeni

Source: Ed Yardeni Source: Beleggenopdegolven

Source: Beleggenopdegolven Source: Bloomberg

Source: Bloomberg

Crude has accelerated this last week with good momentum, but now encounters resistance. It does not have fundamental support from stockpiles, as they continue to be above seasonal average, but I suggest it is the global growth story that is the main reason for the advance.

Crude has accelerated this last week with good momentum, but now encounters resistance. It does not have fundamental support from stockpiles, as they continue to be above seasonal average, but I suggest it is the global growth story that is the main reason for the advance.