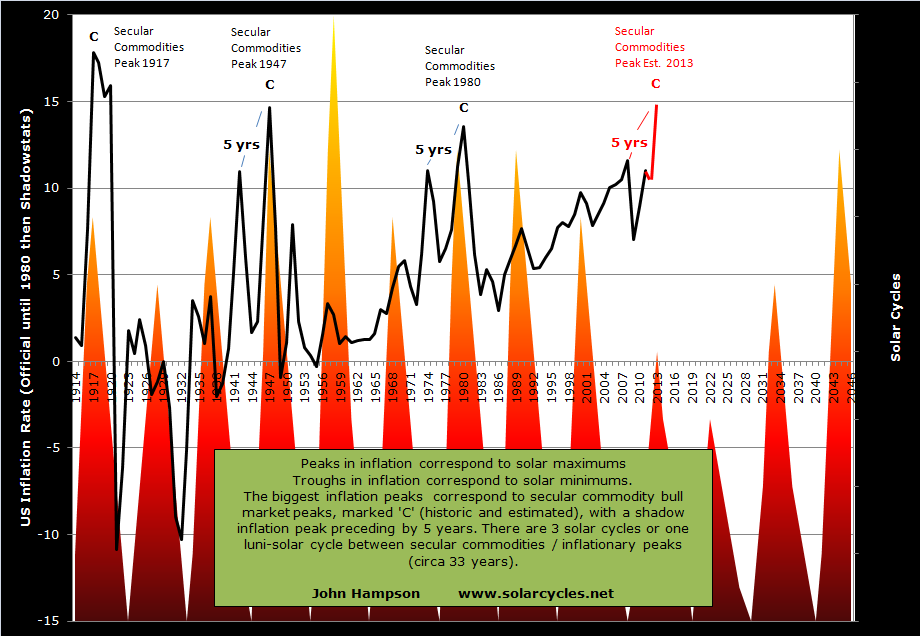

Forecasts for the smoothed solar peak still diverge as we await more a decisive sunspots trend, but the most common forecast remains for Fall/Autumn 2013 (NASA, SIBET, SIDC CM). If that proves accurate, then by history we should expect a peak in inflation and commodities within months of the solar peak. Here is the inflation guide:

I covered commodities in detail here, showing that we might expect commodities as a class (i.e. we should not need to be picky about which commodities – there should be broad participation) to rise into and around the solar peak, with a bias towards peaking after the solar peak, which could therefore be Q4 2013 or Q1 2014 even.

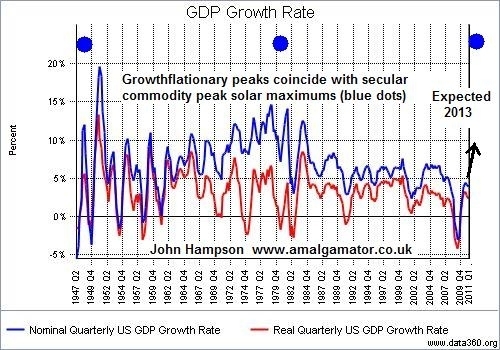

If commodities do fulfill the prediction, then inflation will fall into place, as those inflation peaks marked ‘C’ above were very much resultant from escalating commodities prices. The inflation ought to be ‘growthflation’, rather than a supply-side squeeze only, as this next chart shows:

We should see growth and inflation together, but with the emphasis on inflation, until commodity prices rise too far and help tip the world into recession.

If we draw together stock market history and exclude solar theory, using Russell Napier’s work, then the current cyclical stocks bull should end with rising treasury yields (6% the historic tipping point marker) and rising inflation (to 4% as a historical marker, using the official inflation rate). In other words, it is the same target: growthflation until excessive inflation and tightening. This is an important lesson, because many have prematurely called the end to this cyclical stocks bull when conditions have appeared to be worsening. We should be looking the other way: we need conditions to become growthflationary before the cyclical stocks bull can end, and since 2009 we have only seen short cycles of growth and/or inflation giving way to short cycles of weakness and deflation. The current strength in leading indicators and coincident data looks promising to stick long enough to get the required frothiness into markets and the economy.

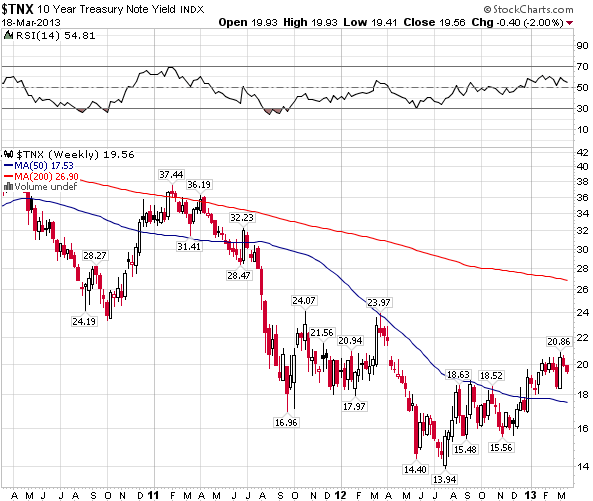

As the Fed has explicitly manipulated the treasury market, I suggest we ignore the 6% marker this time, but just look for evidence of persistent upward trending yields to demonstrate that money is exiting that class and pouring into commodities. We have seen yields rise 25% since 2012’s low (and I believe that move is the process beginning), but they could still potentially be in a downtrend, so I want to see them break out of the downward channel and above the 200MA.

Source: Stockcharts

The historic 4% official inflation marker may also need to be dropped in favour of a ‘persistent upward trending in inflation’. This is because official inflation statistics have been doctored over the years so we no longer are comparing like for like. To this end we should see the main commodities in sharply rising trends, then inflation will fall into place. Here is the equally weighted commodities index, the CCI:

What do you see? A secular commodities bull market that ended with a second peak in 2011? Or a secular bull market still in tact that has been consolidating since 2011? Well, we don’t have to wait long to find out the answer because of the triangle shown. Either commodities will break upwards and out, which should then inspire momentum buying, or commodities will break downwards and out, confirming a bear market in place since 2011. Based on solar-secular history, and based on the solar peak likely being ahead, I predict the former: for commodities to break out and become the outperforming class.

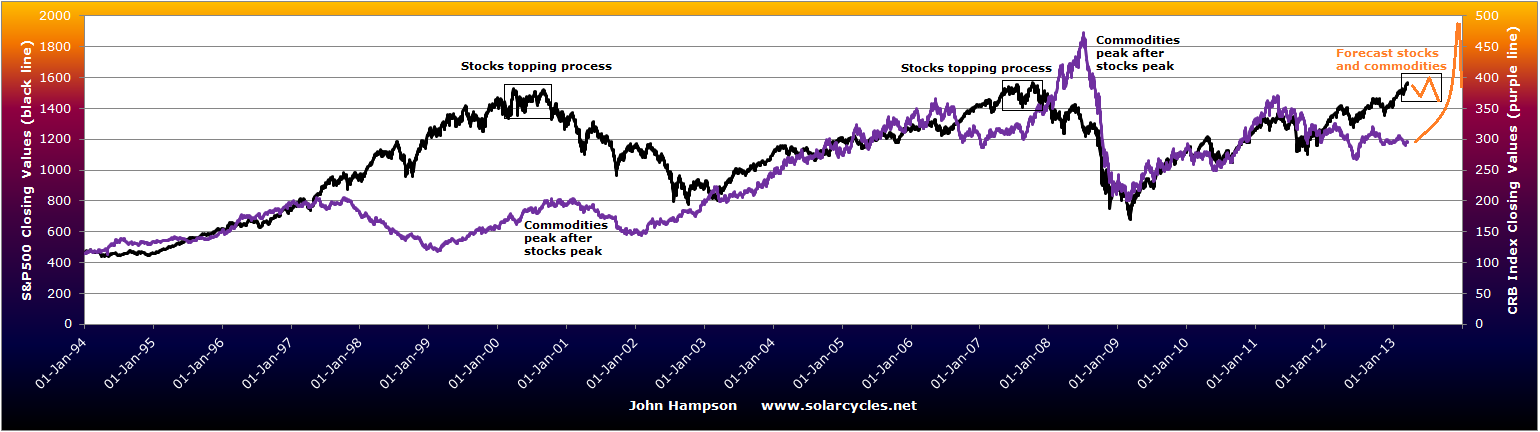

An acceleration in commodities should coincide with a loss of momentum in equities. It is normal for a peak in commodities to follow a peak in stocks (sequence per Hurst). Equities should begin a topping process which is an overall sideways range consisting of a swing top, a retreat, and then a marginal new high but on negative divergences (breadth, leading indicators). Whilst this process is taking place, commodities should be rising. See here:

I have highlighted the last two cyclical stock bulls topping processes and the associated lagged peaks in commodities. This should make it clearer why I exited my stock indices longs, because although I predict a marginally higher high ahead for equities, and we do not as yet see divergences in breadth or leading indicators, I suggest we are at the start of this pattern, and the upside remaining for equities is fairly limited.

My forecasts for inflation, commodities and equities are all based on historic norms as I see it. That does not preclude an anomaly occurring. Therefore I continue to assess whether evidence supports my case. The current trends in coincident data, leading indicators and treasury yields are all supportive. However, the missing elements remain a decisive upward break in sunspots, momentum shifting to commodities, and ideally a run against the US dollar. Chris Puplava expects this latter development – that the fear and negativity that has been directed at Europe will shift to the US for a period. Here we see the US dollar index versus gold and the potential for that to occur: the USD retreats now from resistance whilst gold pushes upwards and out of its triangle.

Source: Stockcharts

Source: Stockcharts

The opposite scenario is also possible: that the USD breaks upwards and out and gold breaks down. So one relationship to watch. Personally, I am not sure whether a run against the USD will take place. However, as long as the USD range trades and does not find grounds for a bull run upwards, that should be sufficient as a backdrop for a commodities finale (as occurred for the 1980 commodities peak).

Lastly, there was a significant geomagnetic storm at the weekend. Geomagnetism has been unseasonally tame in the last few weeks so such a storm is in fact normal. The result is a shift in the geomagnetic model (all models have been updated this morning) and it is now displaying a potential top:

Based on this, equities may make a swing top here, or at best lose momentum looking out into April. Should this occur, then commodities should begin to outperform.

In summary, I see developments ahead likely mapped out by historic patterns. However, there are various indicators to watch to confirm or invalidate this, namely:

1. Sunspots should break upwards to add weight to a solar peak being ahead rather than behind

2. Commodities should break out – the CCI and gold from their triangles

3. Commodities should start to outperform equities, as equities make a range top

4. Inflation and treasury yields should make upward trends

5. The USD should either range trade or break down

Let’s see!

Hi John,

How do you see emerging markets fitting into your game plan? Presumably they will reverse their recent underperformance if there are signs of accelerating global growth…?

Regards, Peter

Hi Peter, there should be a group of emerging countries that outperform in line with commodities, such as South Africa, Russia, Brazil. China, as the biggest commodity consumer, needs to show some strength. The latest CB leading indicators for China came in at +1.3% for the second month on the trot, which, at least for now, suggests this will be the case.

Nice writing, but at the moment Stocks outperform Commodities.

http://stockcharts.com/h-sc/ui?s=%24SPX&p=M&b=5&g=0&id=p10885789118&a=251788917&r=1362775213137&cmd=print

Some of the BRIC countries are rolling over and need to pick up steam pretty soon.

Brazil:

http://stockcharts.com/h-sc/ui?s=$BVSP&p=D&b=5&g=0&id=p30820021758&a=295514677&r=1363680589696&cmd=print

India:

http://stockcharts.com/h-sc/ui?s=$BSE&p=D&b=5&g=0&id=p72515887449&a=286300623&r=1363680805696&cmd=print

BRIC index fund:

http://stockcharts.com/h-sc/ui?s=BKF&p=W&b=5&g=0&id=p69725379663&a=224684107&r=1363680848895&cmd=print

I have bought NY Sugar No11 (new position) and Coffee Arabica this morning.

Arabica is back to long term support following its 2011 spike. It is at a 4 year relative price low compared to Robusta. It is down to just 7% daily sentiment. It is sub 30 RSI and out of its bollinger bands. It is into a seasonally strong time of year.

Sugar is also back to long term technical support following its 2011 spike. It reached a sentiment low in early March then broke out of a declining wedge. it has now retraced a little of that breakout and maybe poised to advance following backtest.

Playing for a mean reversion in both away from oversold/overbearish. Sometimes these things happen swiftly, sometimes they take time.

Brief comments on weather re coffee and sugar.

http://seekingalpha.com/article/1283291-natural-gas-soars-on-cold-march-weather-and-a-look-at-other-markets

Fed settlements re MBS and RMBS end today marking this month’s high point in liquidity. Last month markets dropped sharply for the remainder of the moon period when the settlements ended.

Marlowe:

I have been amping up my Natgas bet in XCO. Pays > 3% dividend too so can sit around and wait. Like the fact that we had storms last year. Historically, there is good stats for nat gas prices due to this as well as the coming months have good historical cyclicality. Like the fact that Wilbur Ross and Prem Watsa are there too.

Do you have a link to MBS and RMBS stats?

You know John, from a distant, very basic standpoint, there is a trend of lower highs in the previous secular commodity peaks on your US Inflation Rate – Solar Maximums chart, and the same with solar cycle peaks since 1980 (and projected into the 2022 peak). The GDP growth rates chart shows the same since the late 70’s, early 80’s.

Also, I question the expectations for an inflation pick-up during K-Winter (or even K-Spring for that matter).

Your thoughts on those issues?

Hi Highrev, 1947 was the last K-winter finale and you can see from the first chart that we did nonetheless have an inflationary peak.

John, this is interesting stuff from Dave:

http://lunatictrader.wordpress.com/2013/03/09/sunspots-high-sell-or-buy/

How do you reconcile this with your theories?

Hi Robert, I go into great detail on my site, both in my PDF and in my charts on this page: https://solarcycles.net/ultra-long-term-models/ (which can be tracked to individual related posts) about how sunspots peaks work with asset cycles. Only every third peak is a secular Dow peak – there is no ‘everytime’ relationship – it is the secular asset that is bid to a peak under the human exciteability of a sunspot max, and in the current cycle that is commodities.

Where human exciteability/optimism/pessimism is an important element in financial assets like stocks, I think that’s much less the case for commodities. Commodities are being bid to a peak (or sold to a low) based on actual supply and demand, shortages or glut.

If we look at the ’70s, the grains peaked in 1974-1975, while precious metals peaked in 1980, that’s 6 years apart.

Especially for agricultural commodities, shortages can come for all kinds of reason, and heat/drought (~ sunspot max) is only one of them. Food prices can also become expensive because of periods of cold (~ sunspot minimum). Sunspot minimum leads to colder winters and a shorter growing season, especially in more Northern regions (Canada, Europe, Russia). Russia had failed harvests in the mid 70s (solar minimum) and was forced to buy grain on the international market. That drove the prices to record highs.

Other examples of commodities that typically go up with cold (freezing damage) are coffee and orange juice.

It’s difficult to reconstruct historic food prices, because they have always differed locally. But we can look at the history of famines. Whenever there were big famines we can assume that food prices were very high: http://en.wikipedia.org/wiki/List_of_famines

I think your model fails to take into account that high food prices can come from cold as well as heat. Given the current weak solar cycle, there is an increased risk for a colder period around the next solar minimum. We would then look for potentially high food and grain prices in the 2019 – 2021 period.

Yes there was a peak in 1974-5 but there was also a peak on the solar max – see corn chart here:

And here are mutliple charts from the last 3 secular commodities peaks showing that commodities made secular peaks close to the solar peak. I disagree that human exciteability impacts commodities less.

https://solarcycles.net/2012/11/28/commodities-peaks-and-solar-peaks/

NECSI research shows that the key factor in commodities peaks (major peaks) is speculation. Agri commodities are indeed much more sensitive to weather and natural disasters and commodity supply lags are a fundamental part of the long term swings in commodities. But it is speculation that drives commodities to major peaks, just like equities.

A pertinent issue looking forward is whether fossil fuel exhaustion, natural resource depletion and permanent global wierding change the picture for commodities, or wether tech evolution can partially resolve or postpone these issues.

Thanks to you both John and Dave. You may want to check out Charlie Mungers discussion on BYD one of my long term holds. I think technology like this will dampen natural resources boom in the end. I think something holds through for all commodities which I do believe are affected by the cycle and that is when they get too expensive something new is invented to push the system in a new direction. When it gets pushed too low i.e. natural gas then even if we have a lot of supply the economics create imbalances such as rig count for nat gas and that creates a growing ground for speculation. Then throw some solar dust in to the equation and you have a thermodynamic system going off. It is very hard do gauge supply and demand for a commodity as it is also our ability to extract it that determines prices and many other complex variables (which I think are essentially pointless to study). Regardless I think the the cycle is there and people only trade their beliefs and not reality. Then their belifs create reality. “It is with your mind, that you create the world”, Buddha

Munger on BYD

Sorry I meant Danny. I am dyslexic. Better with numbers.

Hi John,

Chalres Nenner appears to agree with your assessment that equities may make a top around this time. Nenner thinks the top will come around the April/May time frame, precious metals may put in a cycle low at end of April, and Gold may rise to $2,100 before it corrects then rises again. Nenner has been out of Gold since it last hit $1900. http://www.financialsense.com/financial-sense-newshour/2013/03/16/charles-nenner/bond-funds-get-out-while-you-can

However, other respected market gurus think that equities will correct at this time but will bounce to new highs till end of 2013 before making a deep correction. Do you think that if equities correct around April/May that they could bounce again to new highs before end of 2013?

Thanks Jack. I have previously shown the shape of historic secular bear pentagons and extrapolated for the current cycle. Largely, stock indices have completed their breakouts and are ripe for the pull back to the nose. I maintain therefore a mid-year cyclical bull top, not new highs towards the end of 2013. However, I continue to look at the evidence, and if leading indicators and breadth and technicals remain positive then I would adjust accordingly.

John, thank you for the great newsletter and for opening up my eyes to a whole new world of cycles. In today’s letter you mention “growthinflation” vs “supply-side squeeze”. I am guessing the growth version is better for all, but are there price implications between the two?

Thanks,

Larry M. Powell

LM Powell Development Co.

Larry@Lmpdevco.biz

P.O. Box 27878

Anaheim, CA 92809

714-299-7002 Cell

702-768-6090 Cell

714-970-2140 FAX

Logo

“Everyone thinks of changing the world, but no one thinks of changing himself.” – Leo Tolstoy

“Your thoughts control your life” – Prov 4.23

Thanks Larry. Previous secular or major cyclical commodities peaks became speculative spirals, making for the parabolic shaping. In other words, whether you begin from growthflationary or supply-side momentum, speculative interest should take over and drive it to a mania. At that point ‘how high’ becomes a game of cat and mouse, as we saw in 2008 with oil prices.

John,

Please consider these items as possibilities in your analysis:

1. Consider that 2011 was not a new peak in commodities (10% above the 2008 CCI is hardly a peak) but part of a longer consolidation from 2008 highs similar to the consolidation from 1974 to 1978. This consolidation is more apparent in the CRB index chart. And supported by the fact that oil, copper, platinum, corn, oats, rice, soybean, wheat and cocoa are all below their 2008 highs (with most never breaching their 2008 highs during the entire time). So the final run hasn’t happen yet and is ahead of us still.

2. Consider that all the final bull runs in commodities including 1920, 1950, and 1980 all took 2 to 3 years to complete from intermediate lows and if the final run started tomorrow it wouldn’t be until March 2015 to March 2016 for all time peak.

3. Consider that commodities are already in a 9 month bull run from mid 2012 bottom as show on CCI Chart and CRB chart and the above time frame could be shortened by 9 months to June 2014 to June 2015.

All my indicators show the finale is still ahead of us.

Thanks for your thoughts Justin. The lack of momentum at this point does make me wonder about how soon a peak can be reached. By my own analysis there was historically 12 months of momentum. If that were to start now (with a CCI breakout) that would put us at the end of Q1 2014. Mid-year 2014 would also be within normal parameters. 2015 or 2016 less so! But one step at a time: we need a breakout, then momentum and I am also looking for solar-related backdrop events to occur and support, such as protest, war, global wierding refocussing agri.

John. The crb bottomed in 77, silver in 76, ect. L 12 months has never been the case. After they reach new highs it takes 12 months, but they have to get back to new highs. Even agri takes 2 years.

Here’s something to mull over: Solar Cycle 24 closely mimics Solar Cycle 16, which ran from 1924 until 1934. In the link below, I matched peaks to peaks with SC 16 and 24, with the peak in 2011 correlated with a peak in December 1925, and in SC16, it took exactly 4yrs before the large spike above 100 sunspots took place.

Put the sunspot numbers into a spreadsheet, then into a picture, the link to which is this: http://twitpic.com/cd0ckh

What this could mean: if SC24 is a close repeat of SC16, it may have a flat profile from 2013 until mid 2015, when it makes a sudden spike up and then begins a downtrend, with SC 24 reaching its minimum by mid 2019. Hope this little thing interests you all.

Interesting Pete, thanks. The smoothed sunspot peak was April 1928, which would make us one year away from it. That would likely push back a secular commodities peak to the end of 2014.

But I’d need to see the solar peak forecasting organisations pushing out their forecasts to early 2014. We’ll see how it develops.

Hey John, how exactly do you derive the cumulative geomag. trend? Trying to run some tests of my own.