On a longer term view, these all fit together, and understanding their relationships can help us predict what’s coming.

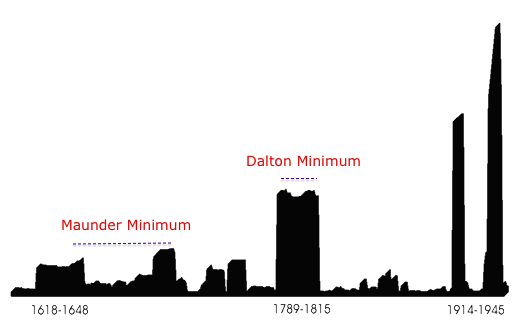

The grand solar minima correlate with clusters of war:

War clusters / cycles

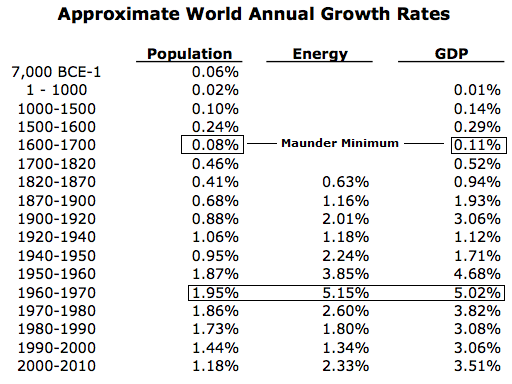

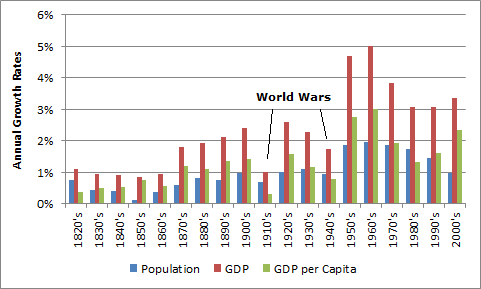

The grand minima were periods of lower population growth and lower GDP growth whilst conversely the grand solar maximum of the 1960s-70s was a period of peak population growth and GDP, shown here:

So, broadly speaking, the grand solar minima have equated to war, low GDP growth and low population growth, whilst the recent grand solar maximum was the opposite.

Benjamin Friedman established the correlation throughout history of declining economic growth giving rise to war. Extremists are brought to power under economic suffering. Revolutions occur when people are struggling (most recently, the Arab uprisings when food prices had risen to price people out of the basics).

World wars 1 and 2 were periods of low GDP growth, and WW2 occurred out of the Great Depression:

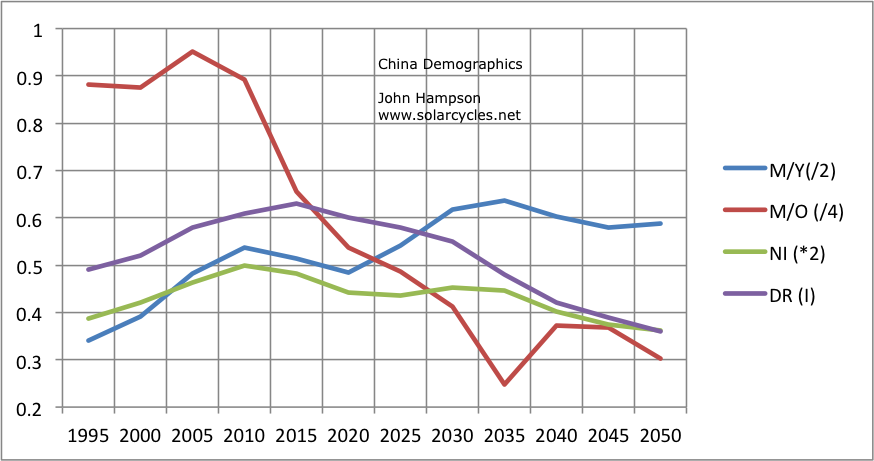

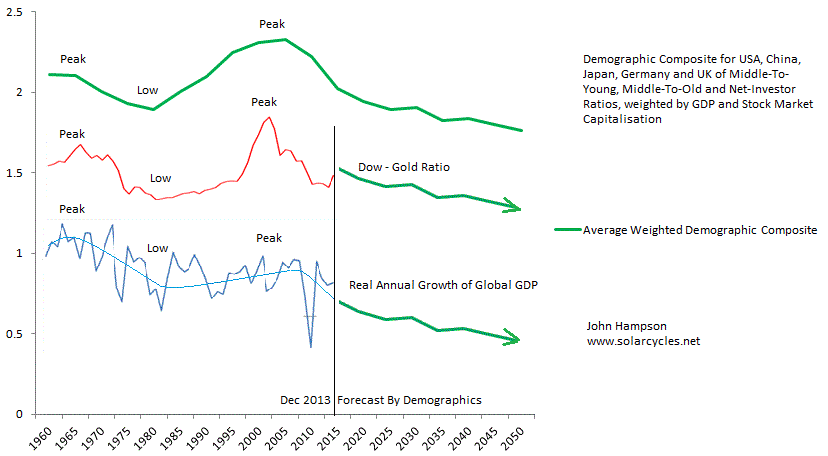

The end of that double great war period gave rise to a global baby boom that produced a young adult price-inflation swell in the 1970s then a middle-aged stock market boom swell between 1980 and 2010 (phased across individual countries).

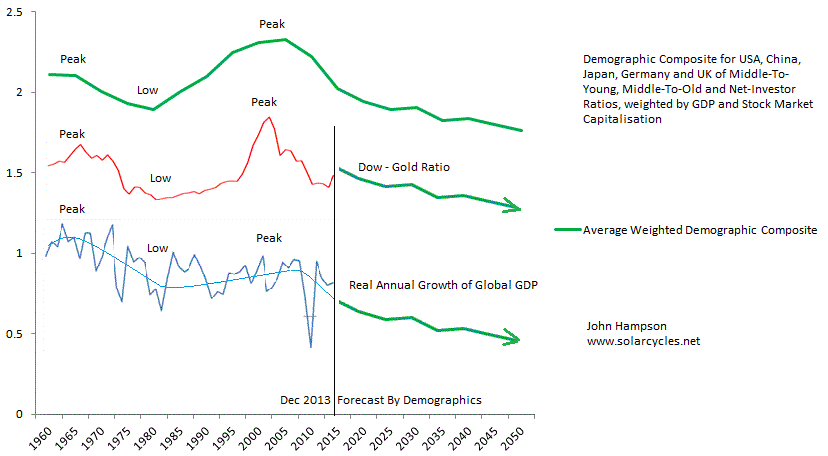

Since then demographics are united in downtrends in the major nations producing this sobering composite:

Global GDP growth is struggling and should do so for an extended period, and stock markets should suffer likewise.

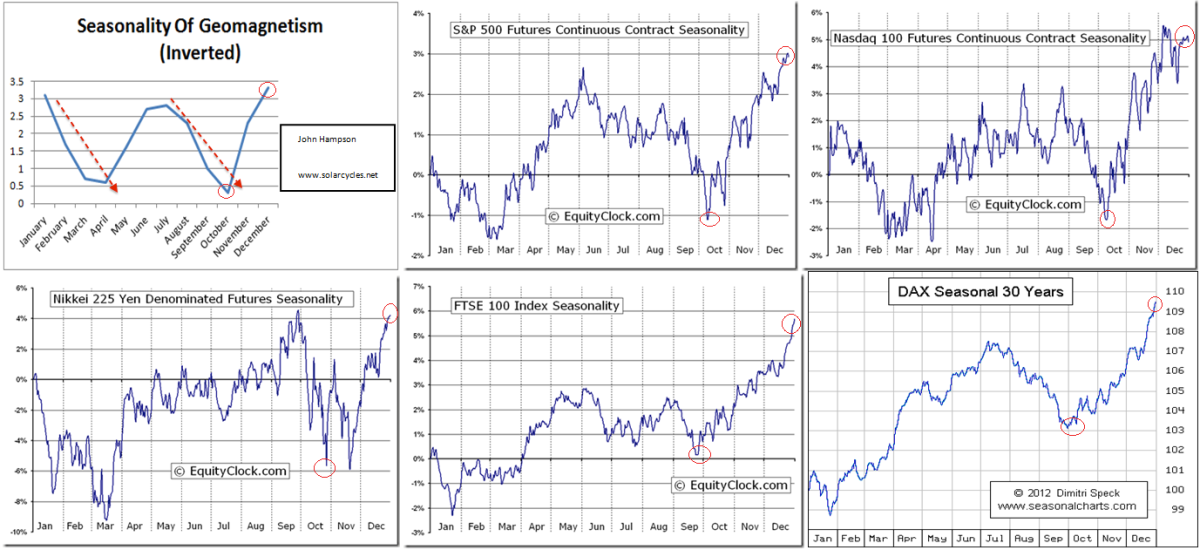

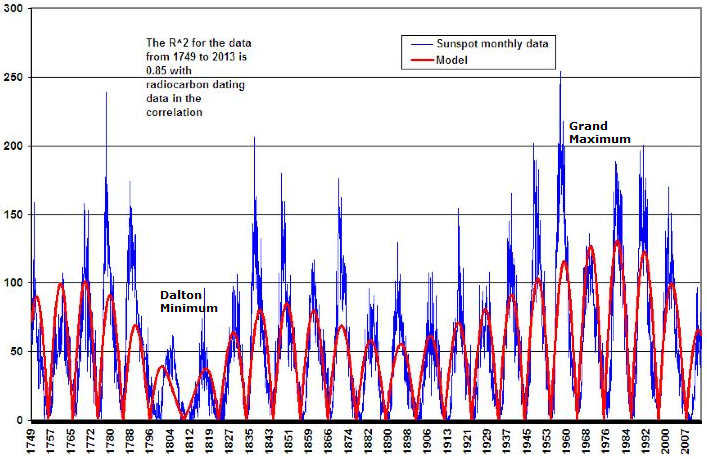

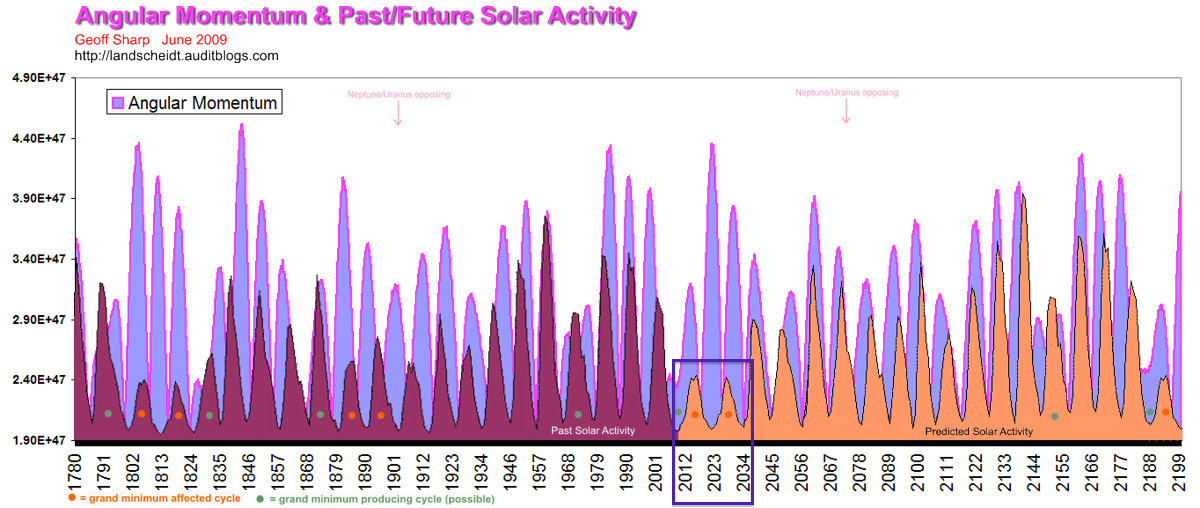

Meanwhile, solar scientists predict that we are tipping into a new grand solar minimum. The predicted low GDP growth above fits with the grand solar minimum predicted below, making for a compelling cross-reference.

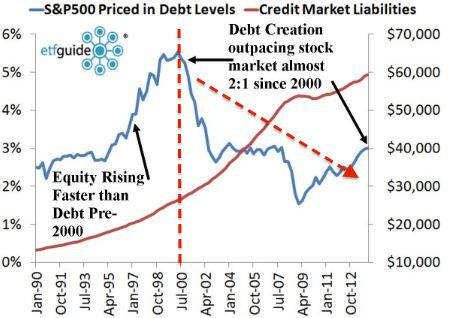

The last piece of the puzzle is debt. Debt is prosperity taken from the future and has been increased with each war and each major recessionary/depressionary period, to pay for or offset those events:

The last piece of the puzzle is debt. Debt is prosperity taken from the future and has been increased with each war and each major recessionary/depressionary period, to pay for or offset those events:

The resultant long rising debt trend means more productive receipts have to be spent on servicing the debt, which crimps the economy beyond that of demographics.

The end game for debt is QE. Printing money to buy your own debt is the policy of last resort. The only way out of this is if demographics point to much higher receipts ahead, but in fact they show the opposite.

Drawing all these relationships together, the outlook is grim. The next couple of decades will be characterised by low global GDP (as written in demographics), which puts the world at risk of war (at both national and international levels). The debt situation threatens to accelerate out of control in certain countries (Japan is at highest risk) as central banks offset even lower GDP and potentially have to pay for war additionally. Major war would cut both GDP and overall population further, making for even greater per capita debt burdens.

These are the major themes. The specifics by country and by timeline are more difficult to predict. But at the global level, the negative feedback looping between solar, population, GDP, debt and war, suggest the crunch is unstoppable for the world.

Eventually, these interconnected phenomena will turn into a positive feedback looping. Out of the ashes of a grand solar minimum with a purge of population, the devastation of war and bankruptcies should come a new solar normal with another baby boom and some anticipated revolutions in systems and organisation (financial, economic, social). True new ways of doing things only occur when circumstances force.

Set against the bleak outlook of the next couple of decades is the continued parabolic rise of technological evolution. Developments in nanotechnology, biotechnology, artificial intelligence, space exploration, geonengineering and renewable energy may produce paradigm shifts that assist with GDP and debt, and accordingly could ease the conditions for war. However, the negative feedback looping captured above extends its grip over this too, as corporate investment has been shrinking across the world in recent years, in accordance with lower economic demand and higher uncertainty.

Declining levels of investment and R&D worsen the outlook for the future and add to the downward spiral.

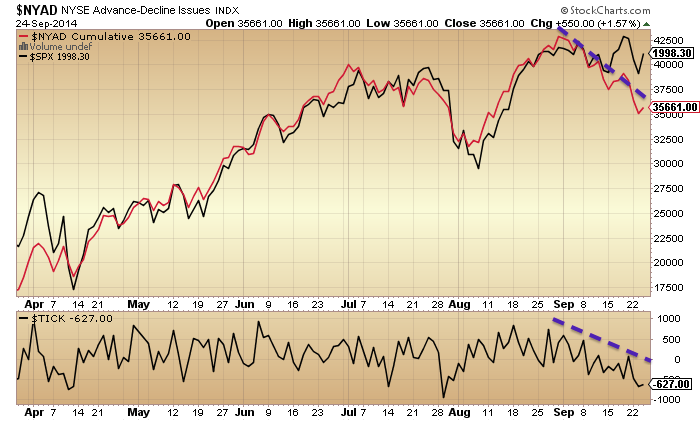

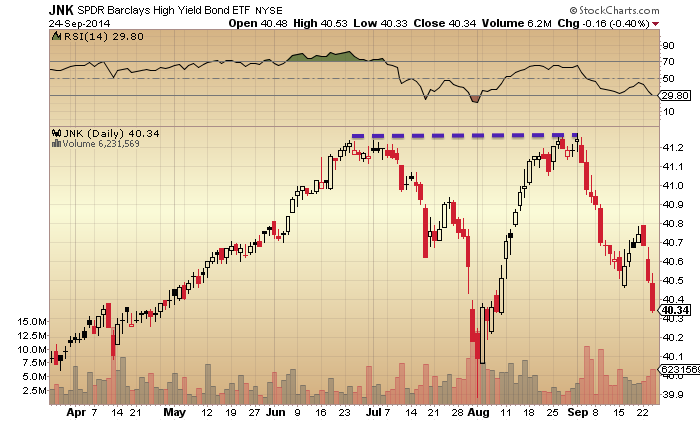

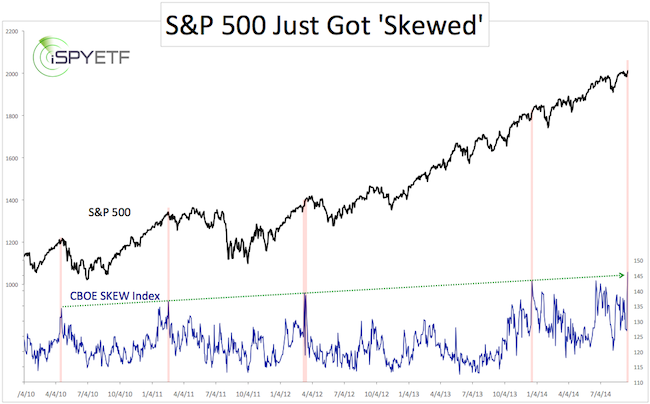

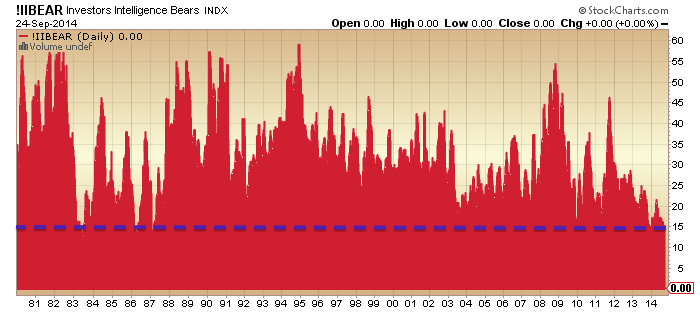

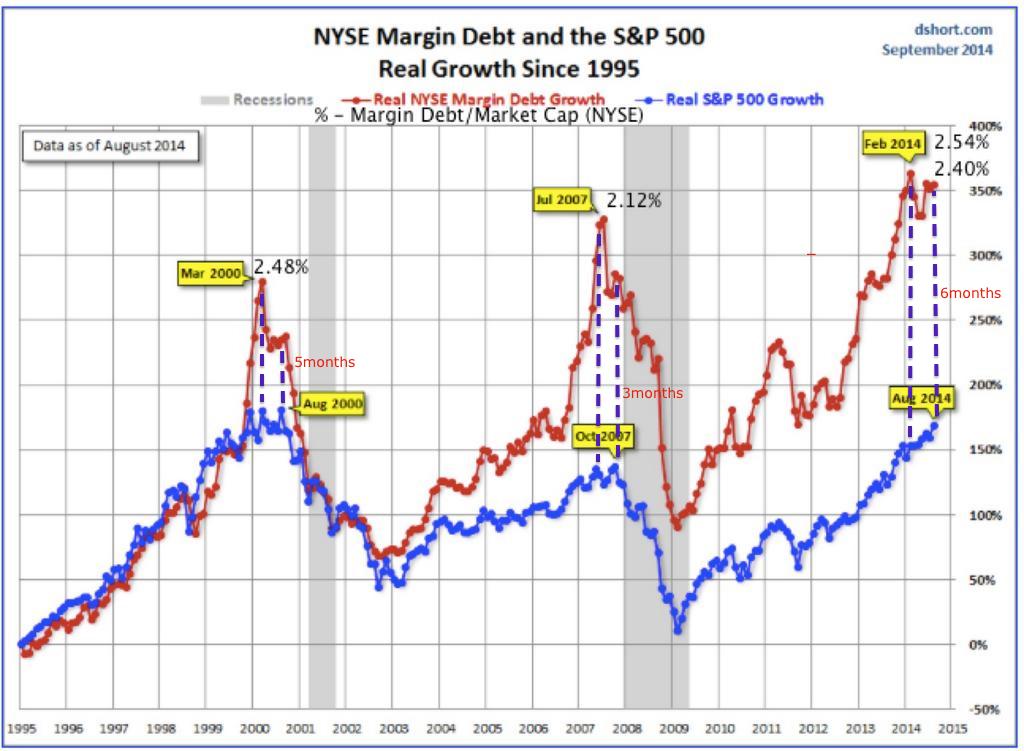

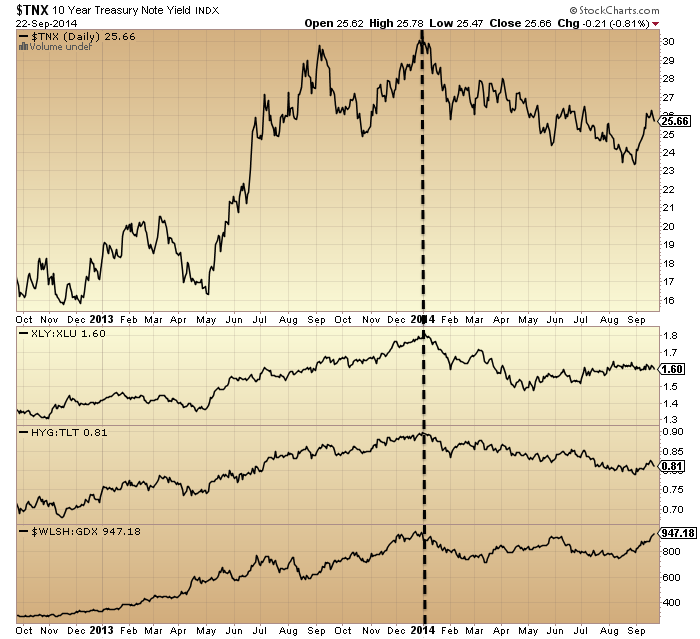

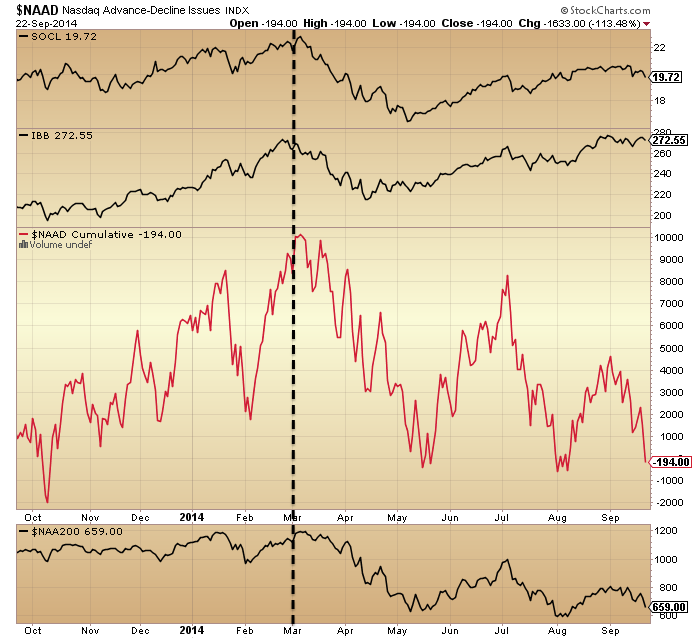

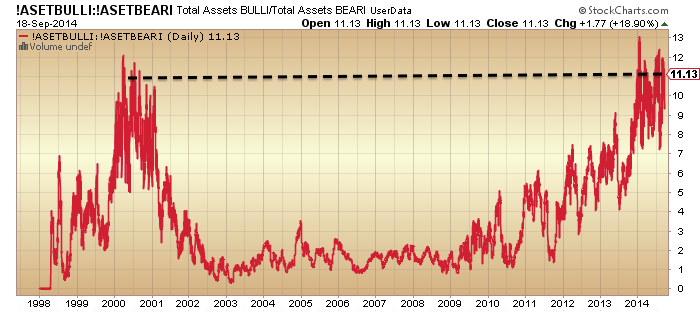

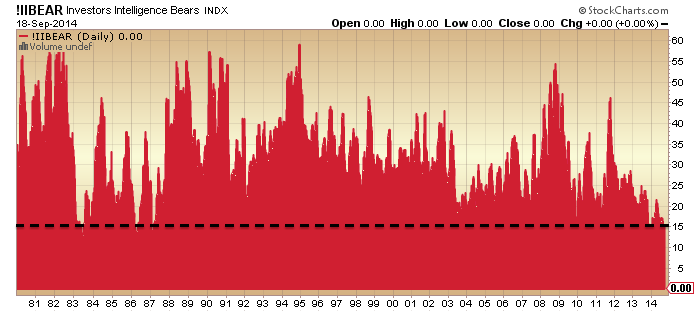

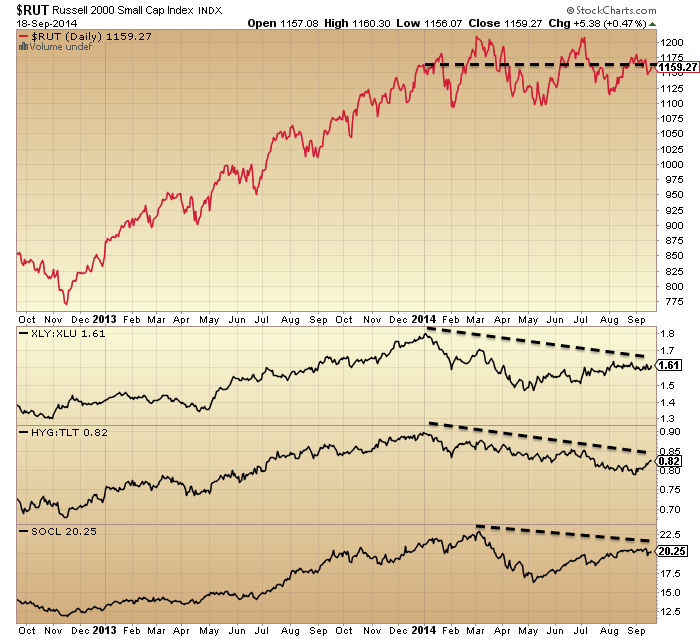

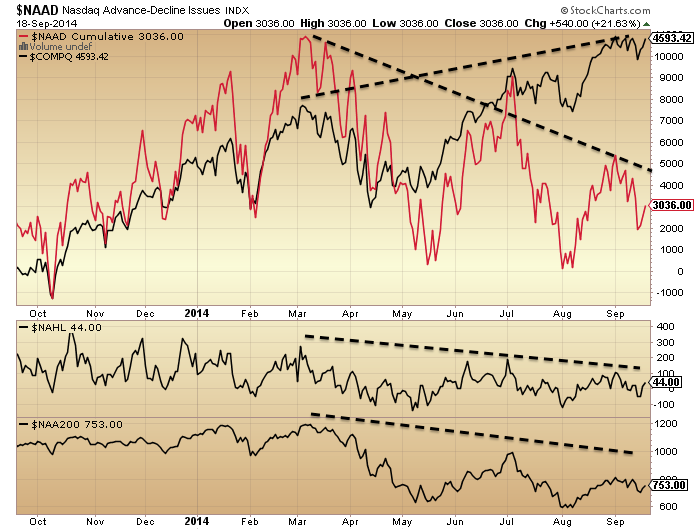

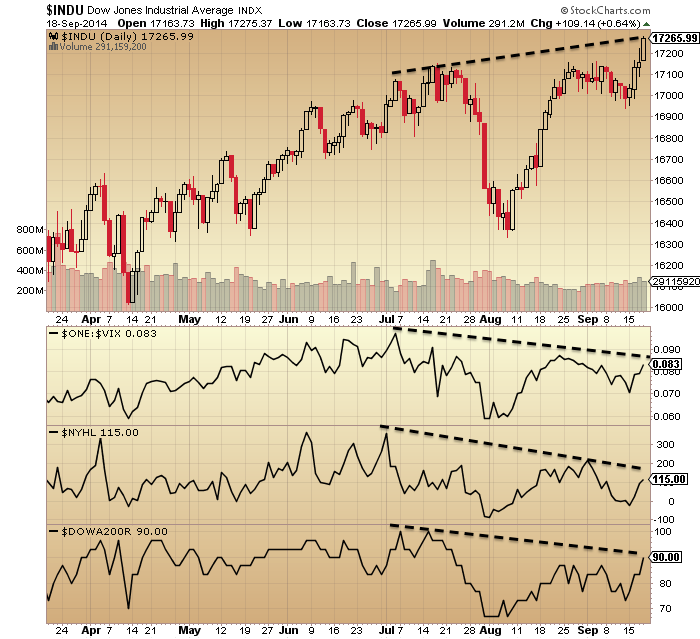

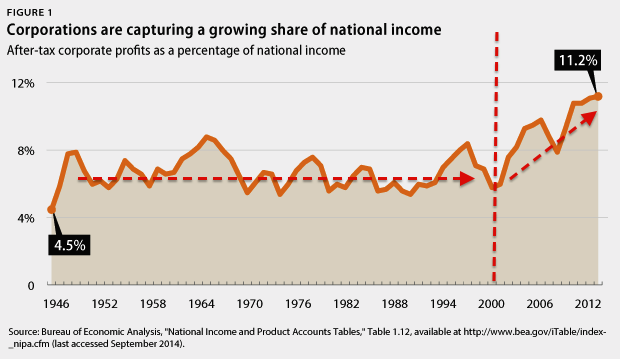

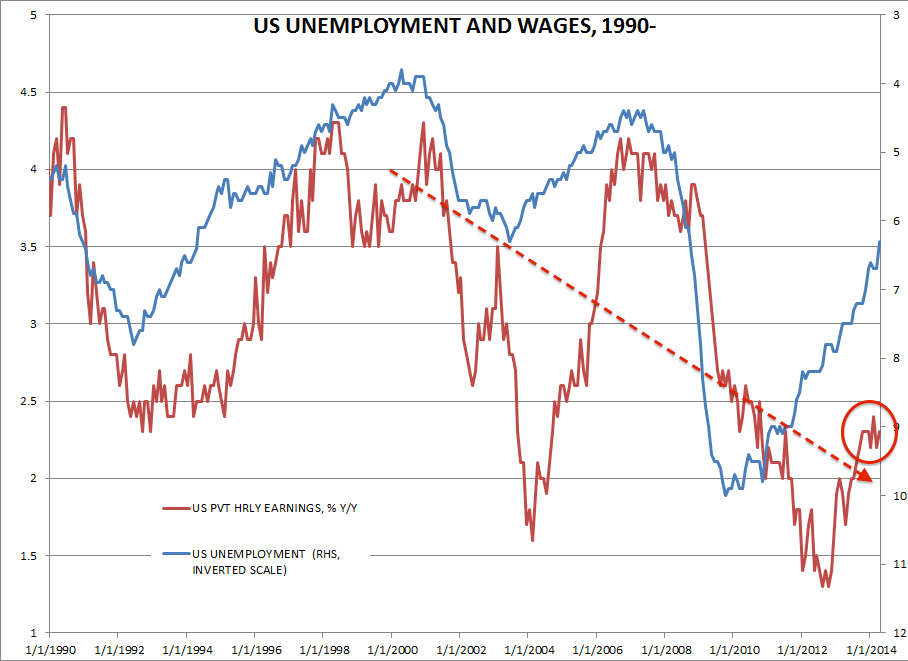

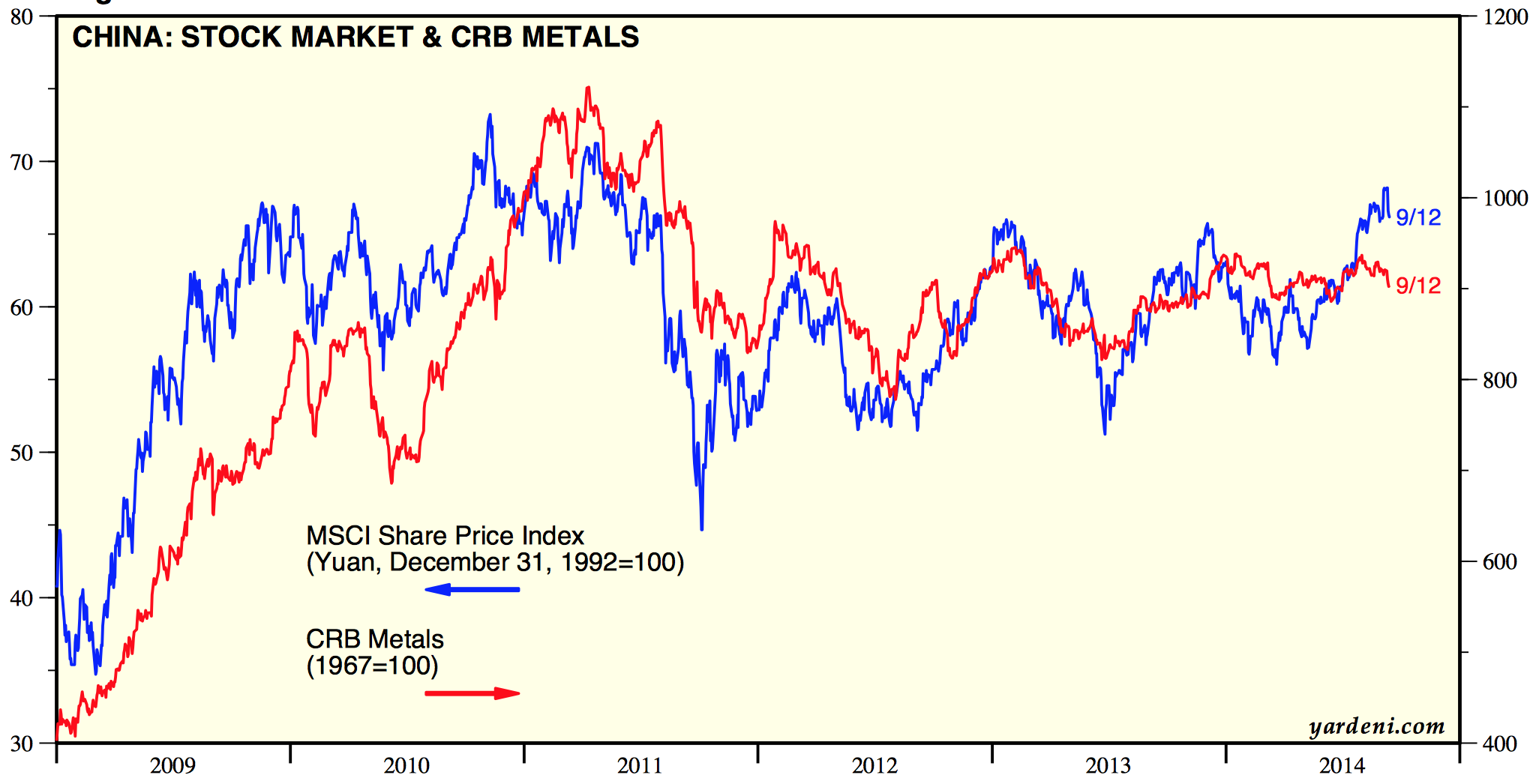

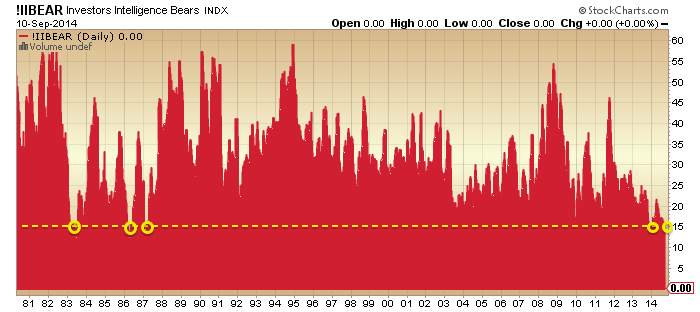

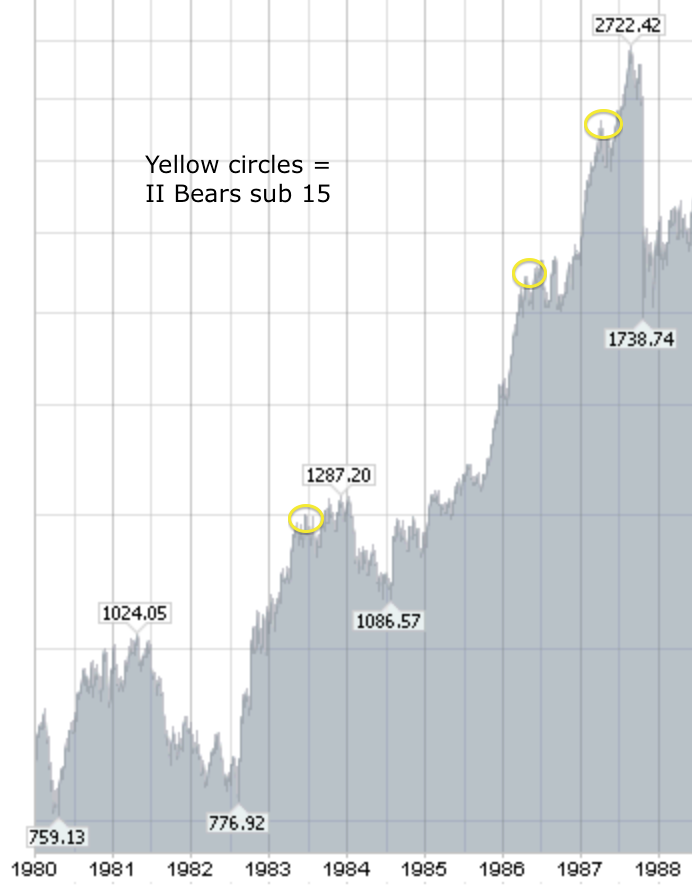

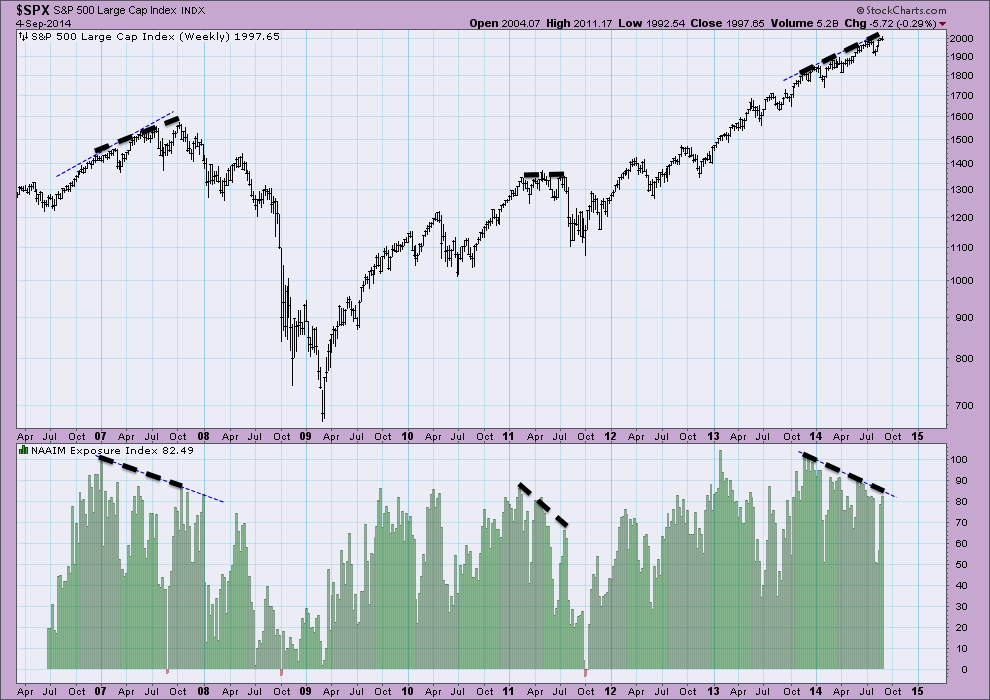

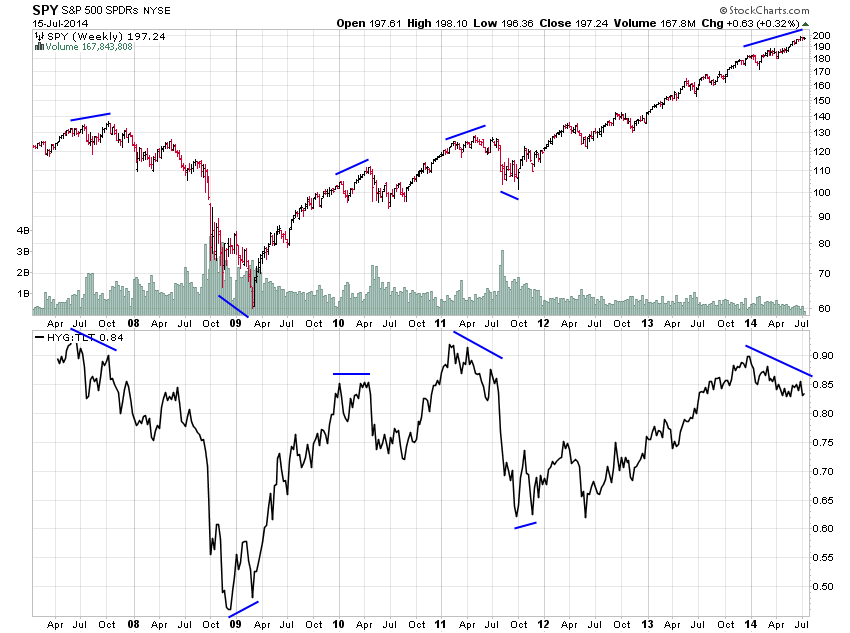

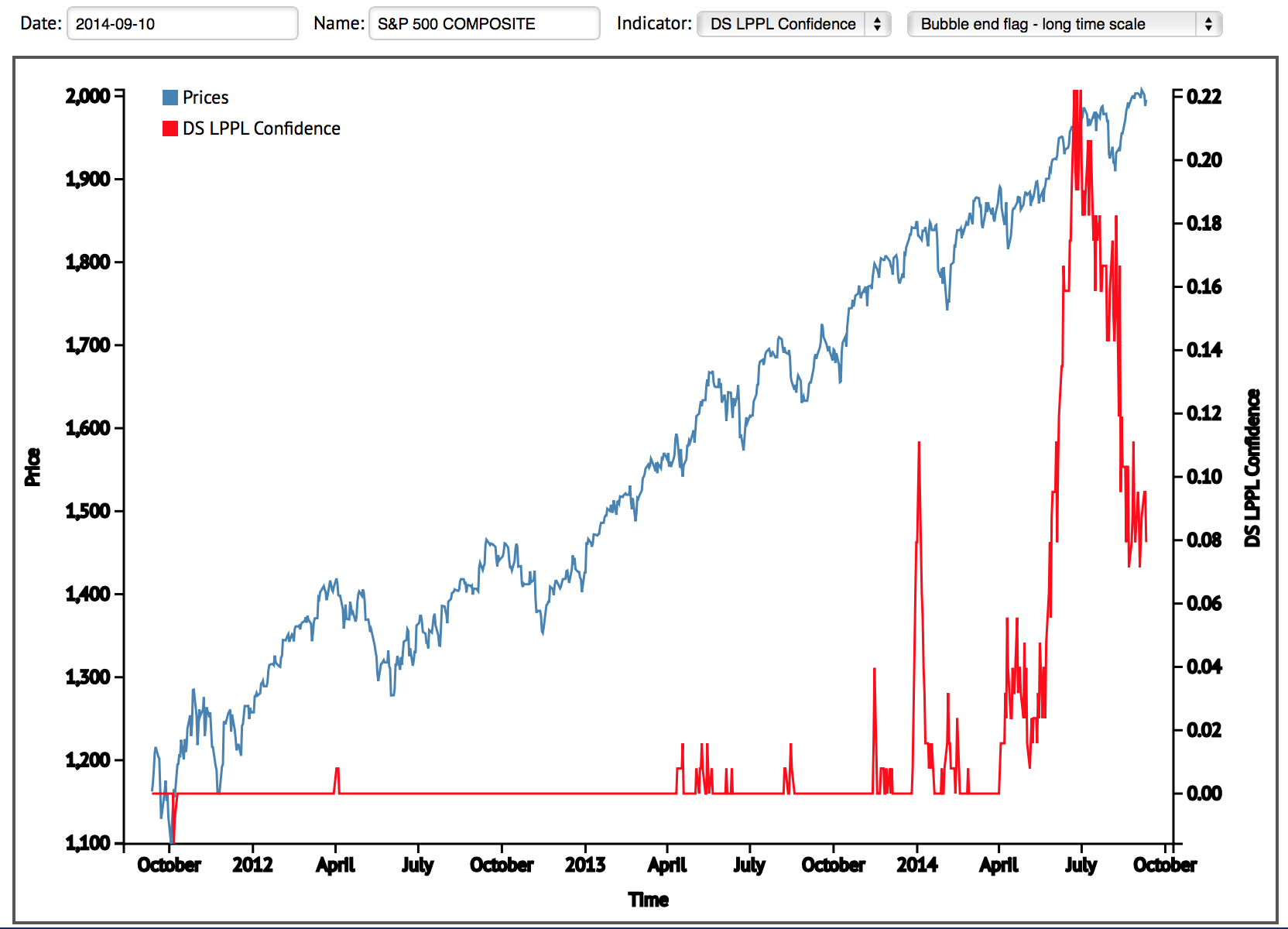

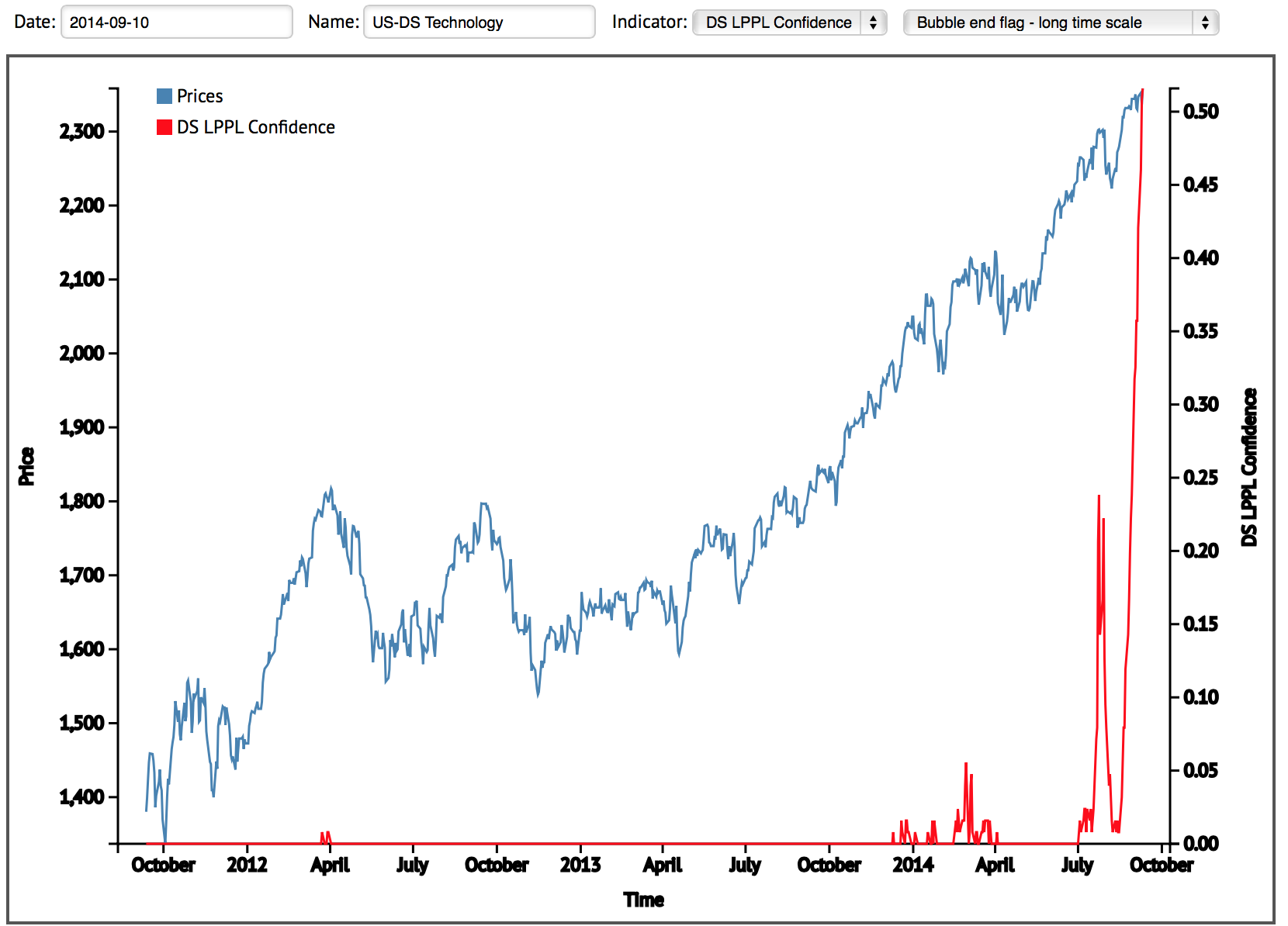

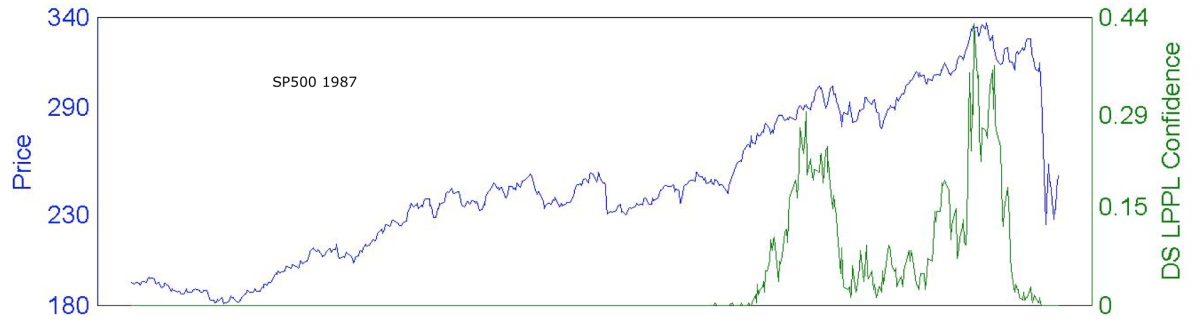

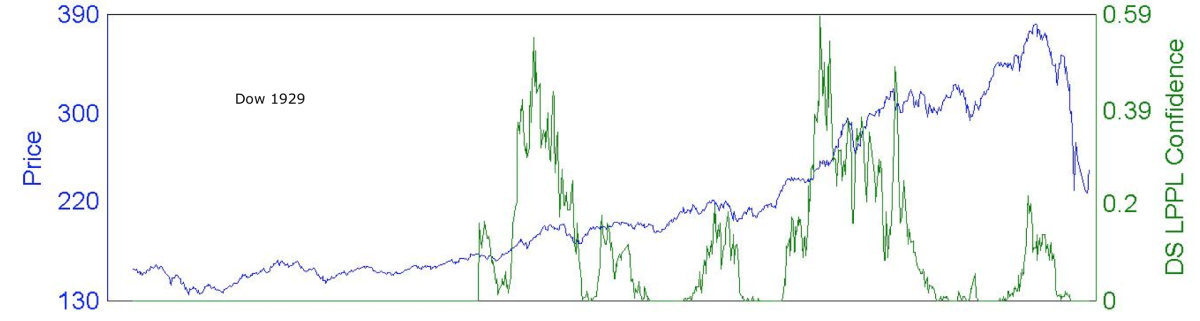

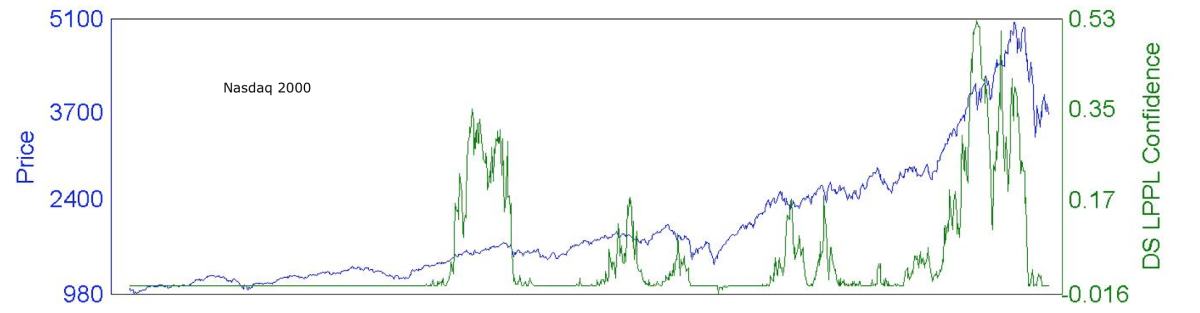

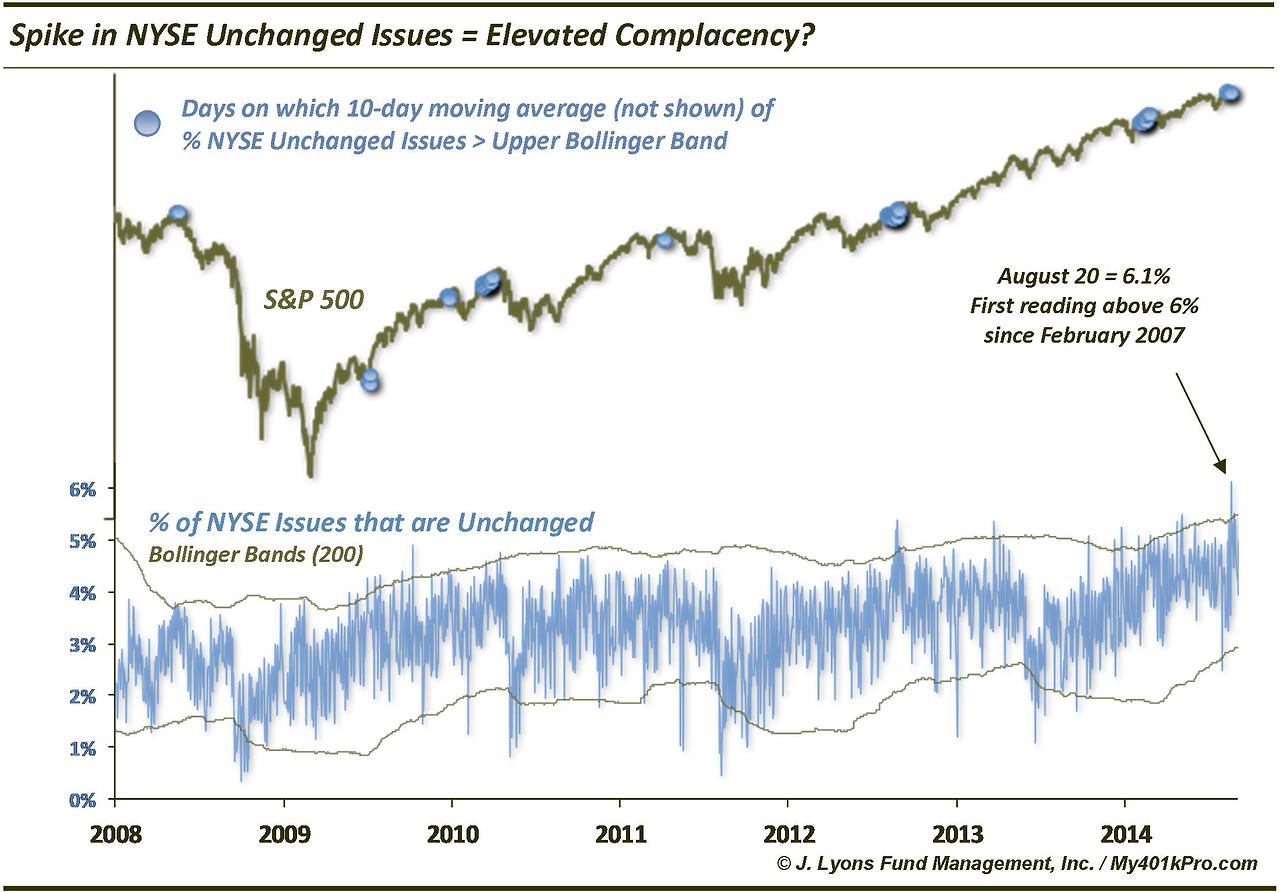

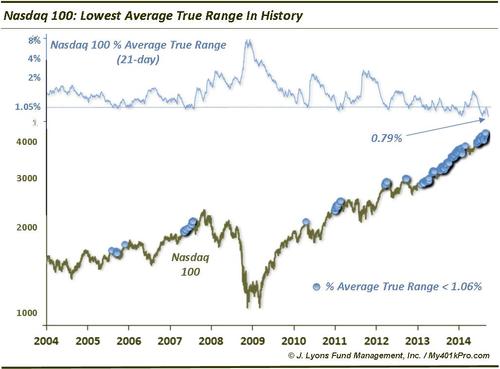

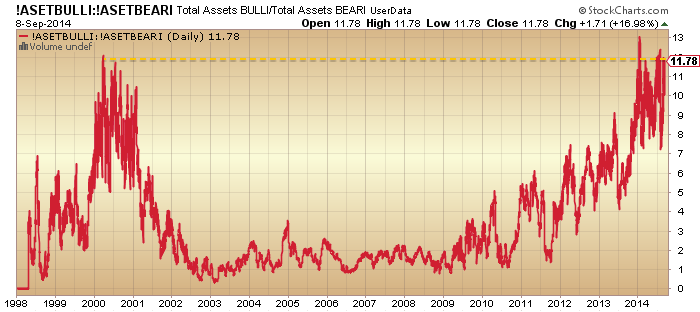

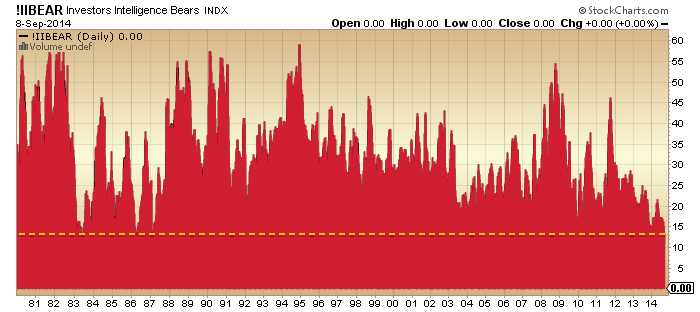

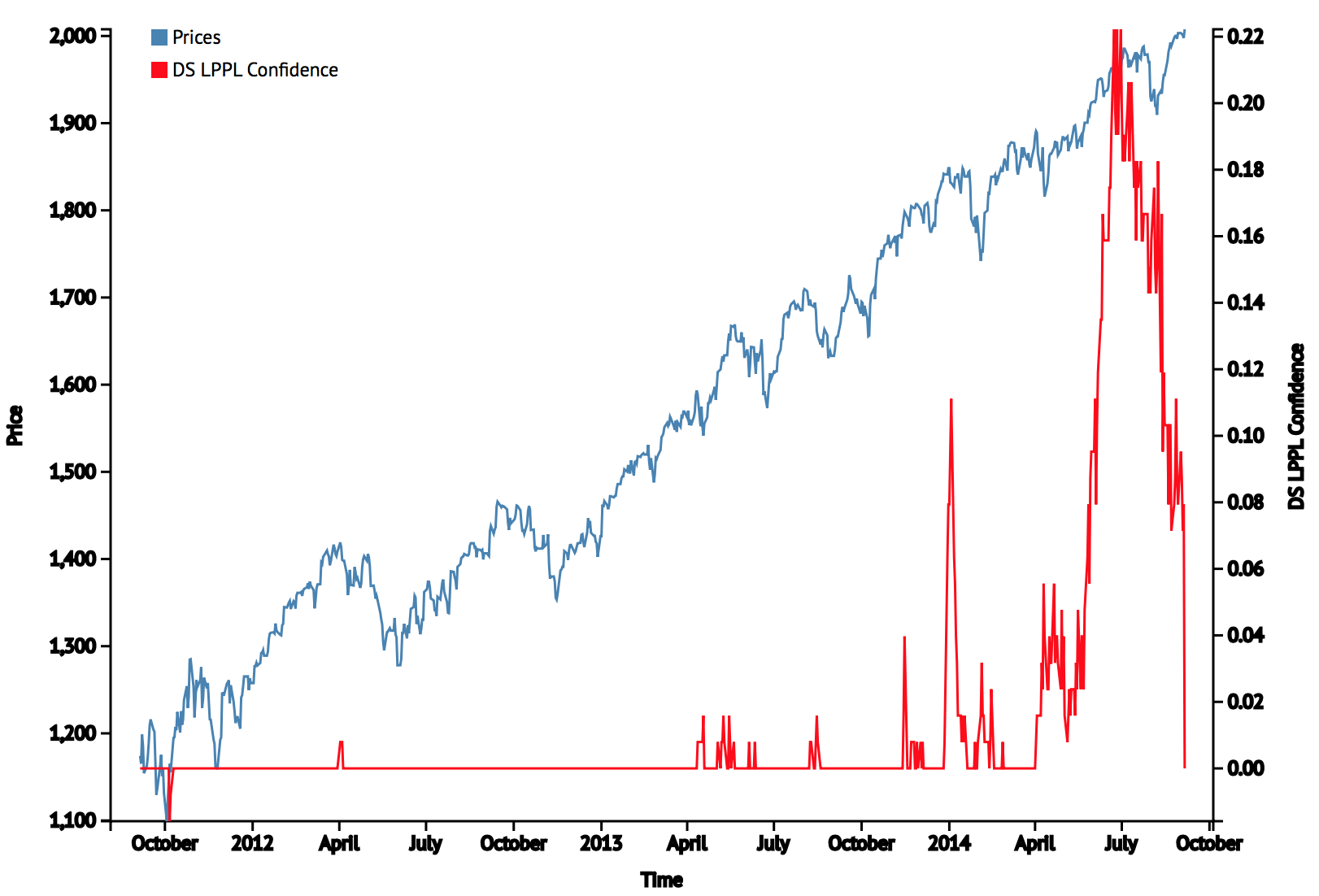

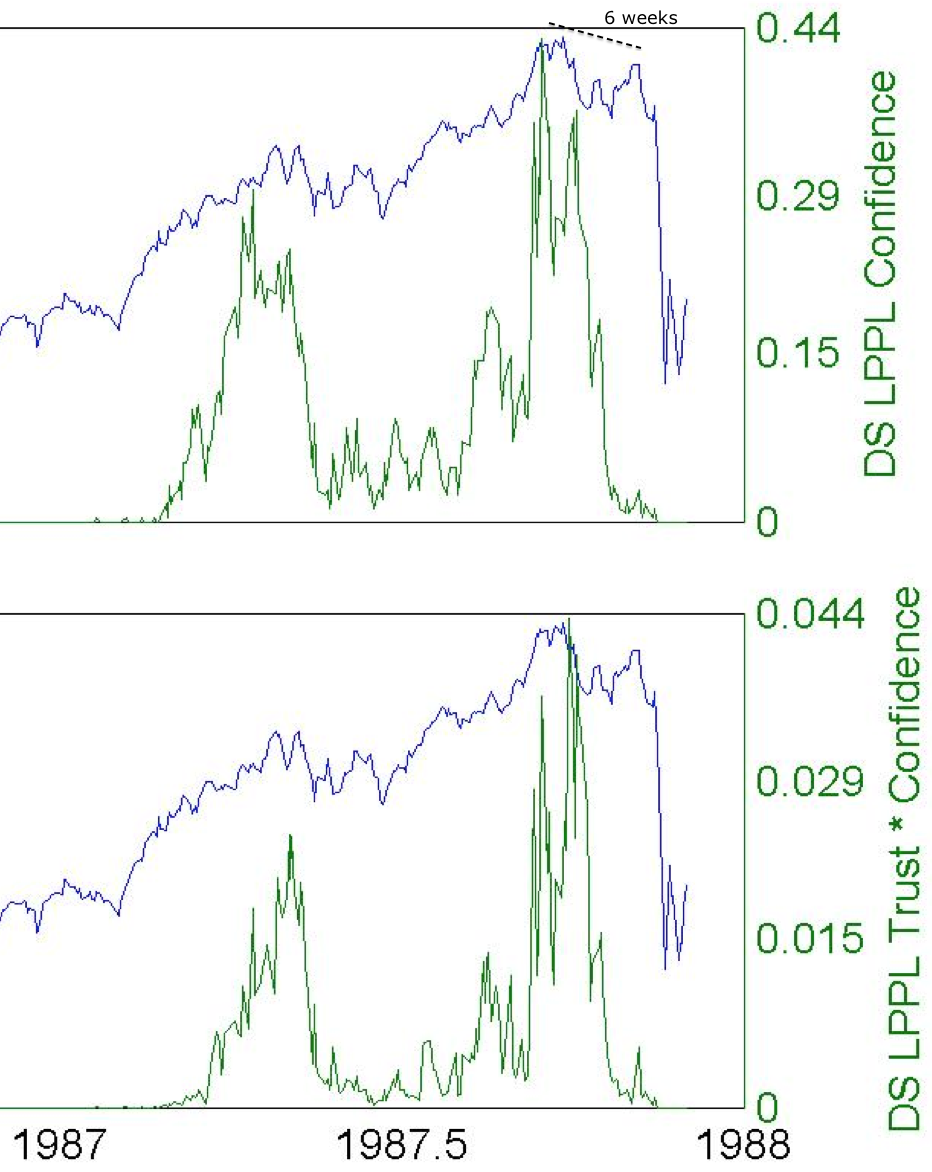

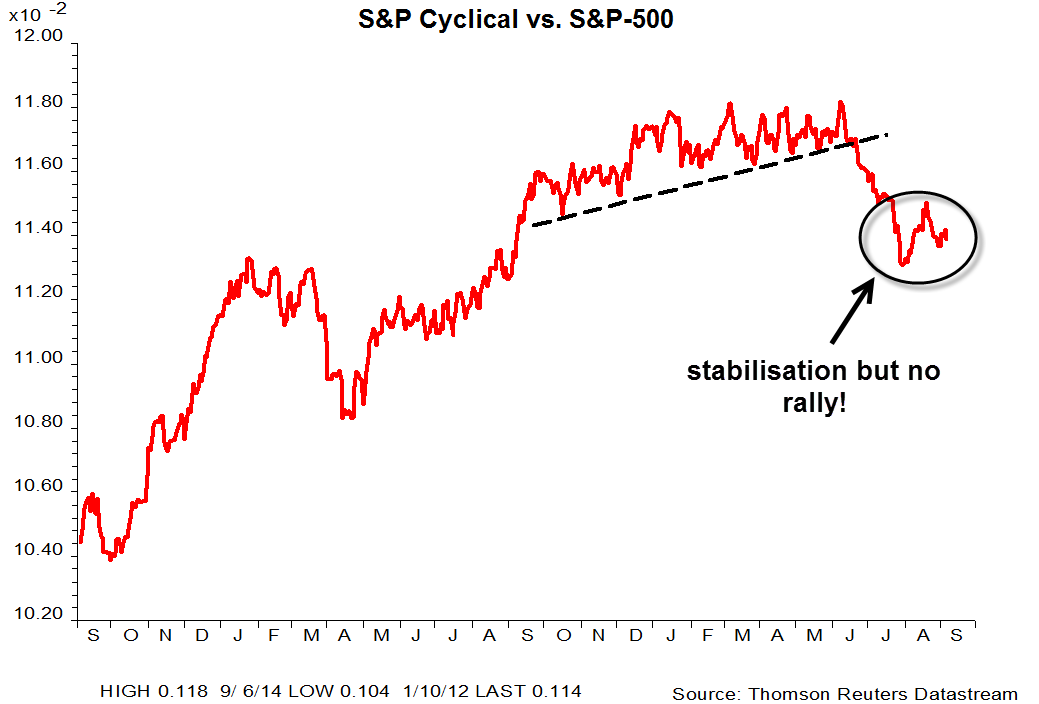

We could argue that the global secular bear in the economy and stock markets began in 2000 and that as yet we have avoided major war. However, collective demographics have worsened since then, as Europe and China tipped over to join the US and Japan. With a comprehensive case for stock market peak here in 2014, the next leg down both in equities and the global economy should be the worse yet. To add to this, a large percentage of the population has seen little improvement in personal finance for some years (as the cyclical recovery since 2009 has been very unevenly distributed), which creates bubbling trouble.

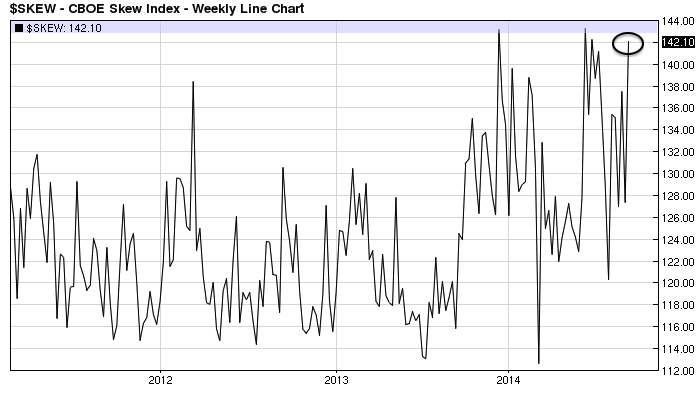

The situation in Ukraine and between Russia and the West may be a fruition of these themes. Economic troubles were a major factor in bringing about the revolutions in Ukraine. The sanctions against Russia are hurting both the Eurozone and Russian economies, which are already struggling, thus worsening the situation for both parties. Protectionism was a theme of the Great Depression, and is a self-defeating policy, but it will most likely increase here with the anticipated next leg down in the global economy and markets, as nations turn to helping themselves and trying to prevent domestic unrest. There is the risk that China and/or Russia sell chunks of their large US treasury holdings and destabilise global markets in a major way. Both countries have been increasing gold holdings in recent years. Indeed, ‘war’ could take a new form in this era of global, interconnected and instant: financial markets may be targeted, adding to the risks for traders.

Putting such speculation aside, the trends in debt, demographics and solar variation combine to make a compelling case for a period of serious economic trouble. That period kicked off in 2000 but is now strengthening in intensity, and stock market indicators assess us to be on the verge of the next leg down, which should be the worst yet. The conditions for war are in place, and it seems fairly sure that trouble around the world will intensify. The question is to what degree and how matters unfold. The recent deterioration of relations between the West and Russia is an ominous development if we are now heading into a major breakdown in the markets and global economy at the end of 2014. Major international conflict is by no means certain, but if we were looking for the appropriate conditions for it, then they are in place.