Correlations between real stocks, real commodities, real house prices and treasury yields, together with inflation, interest rates, recessions, unemployment, demographics and sunspots. A more detailed, step by step study of the correlations, using correlation coefficients, whereby +1 means a perfect lockstep relationship between two things and -1 means a perfect inverse relationship, whilst zero would mean no relationship. A reading over +0.5 is considered a strong positive correlation. Note some of the data has been scaled to share the same chart (indicated by, for example, /10 or *3). Also note for US inflation I have used an average of Shadowstats and official CPI since the 1980s, and official CPI before that. You can click on any of the charts to view larger.

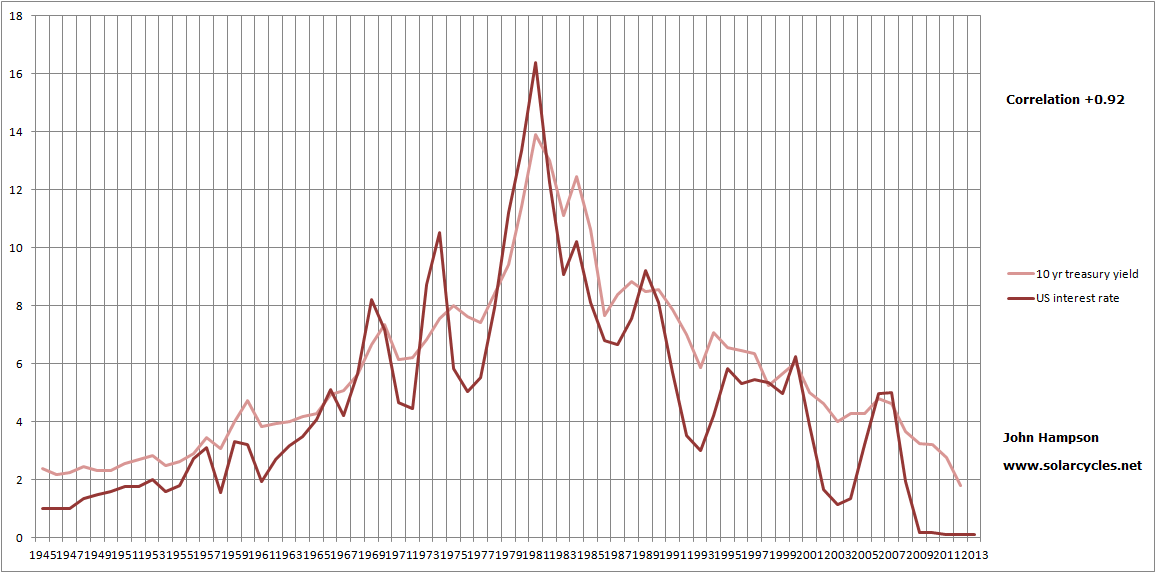

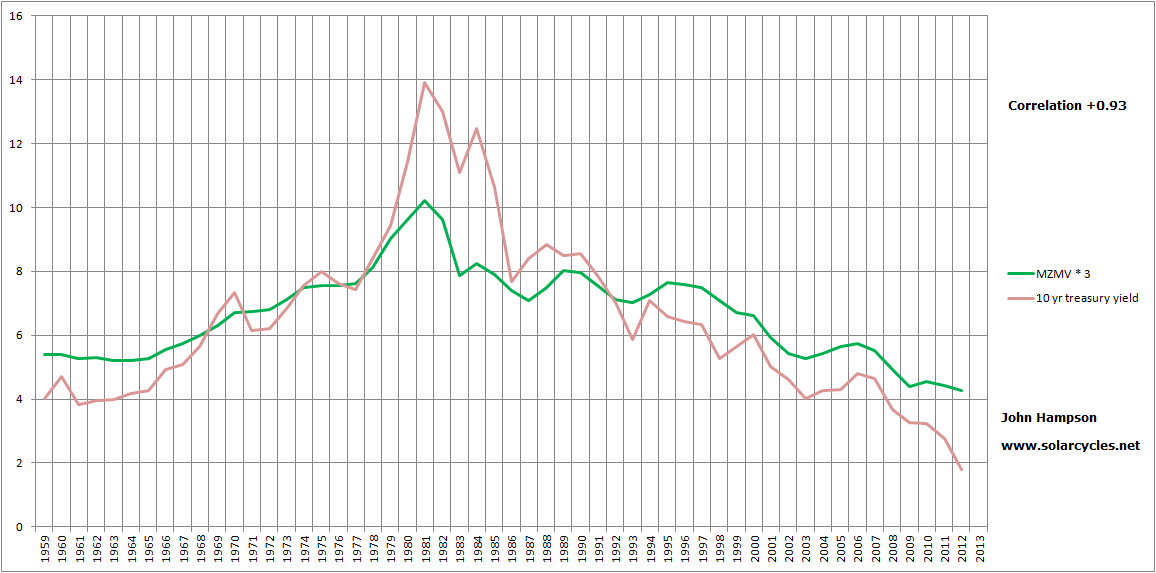

Let’s start with a couple of the highest correlations:

Combining the two, 10 year treasury yields, official US interest rates and MZM money velocity all move in almost perfect lockstep. They are currently all together at record lows. If one begins to rally, we should expect all to rally – with implications for the Fed.

Combining the two, 10 year treasury yields, official US interest rates and MZM money velocity all move in almost perfect lockstep. They are currently all together at record lows. If one begins to rally, we should expect all to rally – with implications for the Fed.

Now let’s look at another closely correlated pair:

Real commodity prices and inflation show a strong correlation. There is a feedback looping between the two as rising commodity prices cause price inflation but price inflation spurs money into commodities (hard assets) as an inflation hedge. There was a lot of debate around the 2008 and 2011 commodity spikes as to whether speculators were to blame. The trading of commodity futures has been around for 150 years in the US, and price spikes are more speculator-heavy because of the feedback looping. Regardless of which kicks off the process, the two occur together.

Real commodity prices and inflation show a strong correlation. There is a feedback looping between the two as rising commodity prices cause price inflation but price inflation spurs money into commodities (hard assets) as an inflation hedge. There was a lot of debate around the 2008 and 2011 commodity spikes as to whether speculators were to blame. The trading of commodity futures has been around for 150 years in the US, and price spikes are more speculator-heavy because of the feedback looping. Regardless of which kicks off the process, the two occur together.

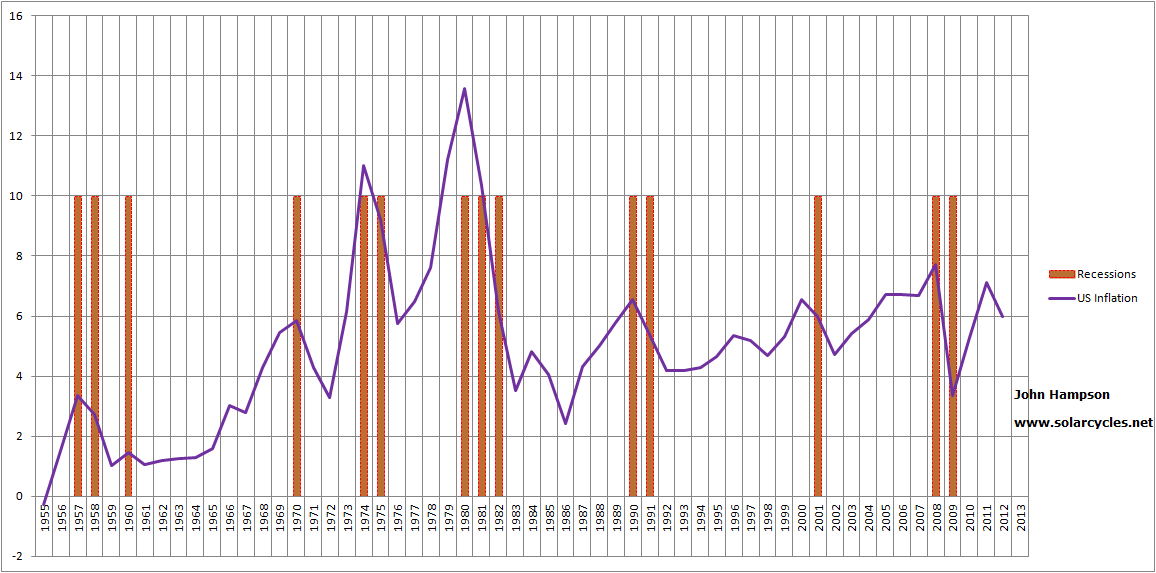

The next chart shows the relationship between US official interest rates and inflation. Most of the time there is a strong correlation, and as the Fed is the sole agent in rate-setting, we can say that the Fed move rates up and down either in response to or in anticipation of inflation, but largely in line with. However the late 1940s and the current period don’t match up as well as the rest.

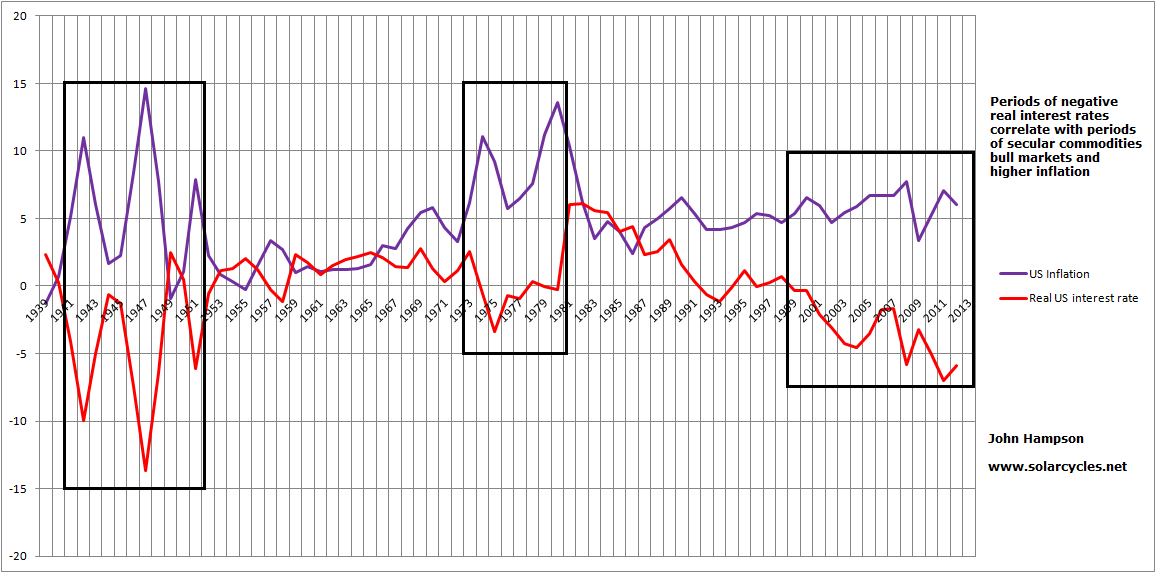

The picture becomes clearer when we look at real interest rates (net of inflation), and extend further back in time:

We see three clear periods of negative real interest rates – which notably coincided with secular commodities bull markets. Inflation was higher during these periods. If you subscribe to the Shadowstats calculation of inflation (that official inflation stats have been significantly doctored over the last 3 decades) then the purple and red lines would be somewhat higher and lower respectively than shown at the current time. If you take the official CPI data as true, then annual inflation would be currently running around 1.5% which would still maintain the real rates line in the negative. I suggest true inflation is likely somewhere between the two, and thus as shown. As things stand currently, therefore, the environment for the secular commodities bull is still in tact.

Here is another correlation with inflation. US unemployment brought forward two years has a correlation over +0.5 with US inflation:

This is because recessions occur following inflation spikes:

So we see inflation spikes bringing about recessions which bring about peaks in unemployment around 2 years after the inflation spike (due to unemployment being a lagging economic indicator).

So we see inflation spikes bringing about recessions which bring about peaks in unemployment around 2 years after the inflation spike (due to unemployment being a lagging economic indicator).

Now let’s draw together unemployment (brought forward 2 years) and inflation, and bring solar sunspot cycles into the picture:

Sunspot solar peaks correlate with inflation peaks, and unemployment brought forward 2 years. This is not a lockstep relationship – it is a correlation specifically related to the solar maxima – and the reasoning for that is the ‘excitement’ that Aleksandr Tchijevsky discovered around solar peaks in human history which is backed up by more recent research revealing bilogical changes in humans at sunspot peaks. If this ‘excitement’ translates into buying and speculation at solar peaks then we can justify spikes in inflation (with subsequent recessions and unemployment spikes).

Sunspot solar peaks correlate with inflation peaks, and unemployment brought forward 2 years. This is not a lockstep relationship – it is a correlation specifically related to the solar maxima – and the reasoning for that is the ‘excitement’ that Aleksandr Tchijevsky discovered around solar peaks in human history which is backed up by more recent research revealing bilogical changes in humans at sunspot peaks. If this ‘excitement’ translates into buying and speculation at solar peaks then we can justify spikes in inflation (with subsequent recessions and unemployment spikes).

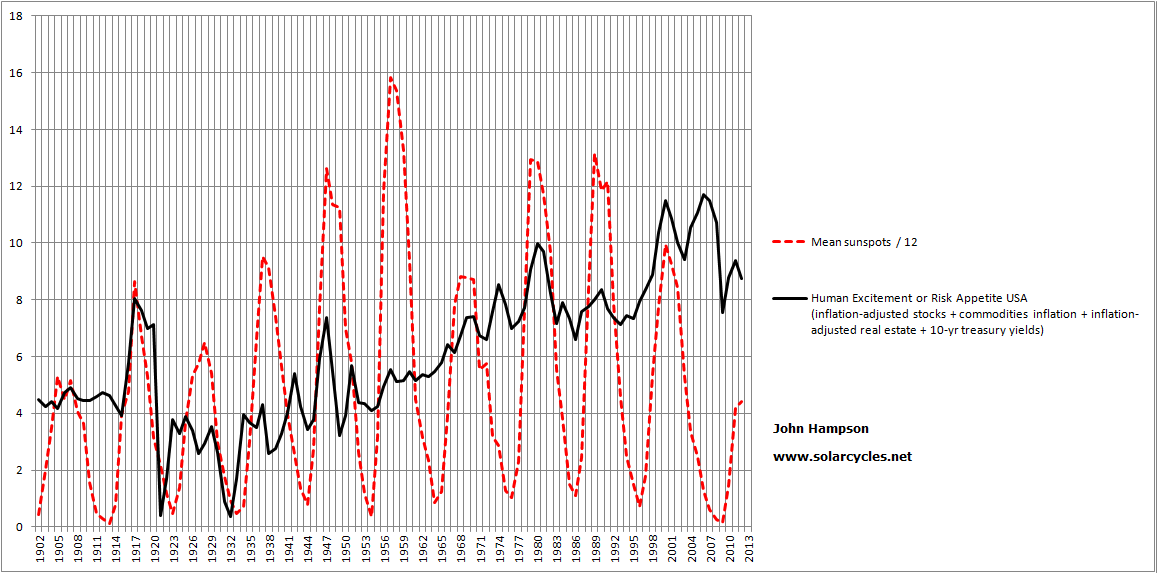

If it is true that humans are biologically disposed to buying and speculation at solar maxima then a composite of risk assets, namely real stocks, commodities, real estate and treasury yields, should spike up at each solar maximum. Here it is:

The composite uses Schiller real house price data and real SP500 index annual values. Each solar peak is accompanied by a spike in what can be termed risk appetite. There are other spikes inbetween the maxima, but what is key here is whether solar maxima reliably bring about spikes in risk assets, given that we are likely in the year of a solar maximum in 2013.

The composite uses Schiller real house price data and real SP500 index annual values. Each solar peak is accompanied by a spike in what can be termed risk appetite. There are other spikes inbetween the maxima, but what is key here is whether solar maxima reliably bring about spikes in risk assets, given that we are likely in the year of a solar maximum in 2013.

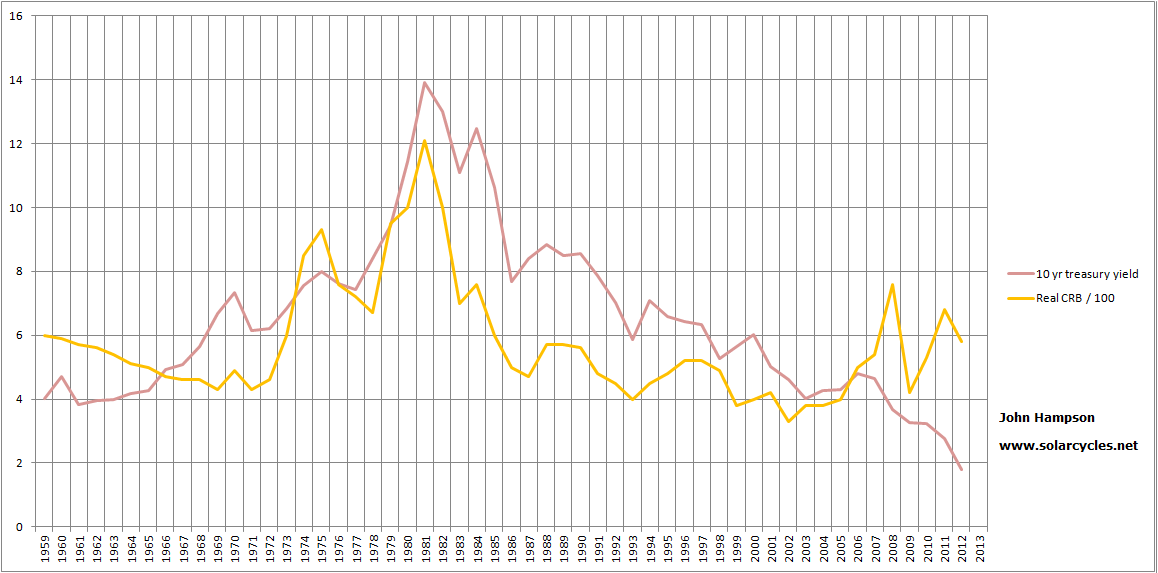

Within the risk asset composite, there are broadly speaking two pairs:

10 year treasury yields have a distinct relationship with real commodities, whilst real equities and real house prices correlate very positively together:

Yet commodities and stocks display an inverse relationship over time of around -0.5, with the result that the two above pairs are often going separate ways. Indeed, thus far in 2013 we have seen US equities and real estate rallying whilst commodities and treasury yields have been languishing. Is it time for a reversal?

If we bring in demographics at this point, and combine stocks and real estate into a composite, this is what we see:

All three demographic measures – middle to old ratio, middle to young ratio and percentage net investors – are all pointing down for the next couple of years. The stocks and real estate composite has historic correlations with the three measures ranging from +0.54 to +0.7, so all strong positive. It would therefore seem more likely that there is another leg down for real equities and real housing into circa 2015, rather than secular bull upwards action from here. Another leg down in real terms would also help satisfy secular p/e, Q ratio and regression to trend measures for equities, which all call for further washout.

Drawing all the above together, along with my previous analysis, I suggest it remains the most likely scenario that we see an inflationary peak to coincide with the solar maximum (allowing for a reasonable time window), within which commodities and treasury yields rise and stocks and real estate decline in real terms, but due to significant inflation hold up in nominal terms. A recession and peak in unemployment should then follow the inflationary peak. As of around mid-decade demographics improve sufficiently to remove the headwinds for equities and housing, which could enable a new stocks bull, with real interest rates turning positive again.

Once again, your observations and suggestions are welcome, as I believe there is more to be teased out.

Hi John, have you come across Strauss and Howe ( ‘The Fourth Turning’ http://store.lifecourse.com/products/15/The-Fourth-Turning.html + ‘The Graying of the Great Powers’ – http://csis.org/publication/graying-great-powers-0 )? If you have, did you find their findings useful? For generations research they are meant to be the go to source. Personally, I’ve found these two books to be goldmines. A more recent book that takes generations as the base for ‘history repeats itself’ is Pendulum: How Past Generations Shape Our Present and Predict Our Future by Roy H. Williams ( http://www.penduluminaction.com/ ). Have not read this one yet. Cheers.

Thanks for the tips Cesar. Not familiar with any of them.

Hi John

Here is the average Sunspotcycle, and the average for DOW

Notice that the DOW average shows weakness at the high platou in sunspotnumber, and strength in the rising and falling phase.

This is for normal/average sunspot cycles, and I should study those weak cycles in Gleissberg minima like now.

My hypothesis: Rising sunspotnumber produces optimism and euphoria. At the sunspot maximum there is a lot of violent solar activity, with spikes in flux and frequent solar storms. This produces volatility in markets, at an euphoric level, which “smells” like a market top. This again makes the market top out (sentiment get confused from all the mixed influences from the sun, and markets are typically overbought).

This again normally produces a 12-24 month bearmarket or so.

When markets are oversold, they start an oversold rally/bullmarked, and the oversold condition overrides the falling sunspot activity.

Now this would be a hypothesis for a normal sunspot cycle. At Gleissberg lows however there might be a somewhat different pattern… have to look 🙂

this would again imply that the sunspot cycle has one major effect: producing euphoria with rising sunspot level. And overbought condition that has to let air out.

So in todays market, we are at the high platou in sunspot activity, and the euphoric-phase should be over. And we are overbought and waiting for the volatility that tells us it is time for a bear…

I quickly made this one from SC number 12, 13, 14 and 20. Enough to see a pattern?

If so, the avrage DOW for these four SCs suggest we are right at the market top here and now, or perhaps in some 6months after a correction this summer

Very interesting – thanks Jan

Interestingly Jan your chart shows a low in 17/18 weeks! I like it 🙂

Good to have you back on your regular track, John. Felt like I lost you there for a bit.

Cheers Sam

Hi John. Correlations between inflation and interest rates are well known. It is the correlation with sunspots that is weak.

When I was working on my long term commodity chart I found some very long term inflation data for Norway (see: http://www.norges-bank.no/en/price-stability/historical-monetary-statistics/). I checked the correlation between yearly change in CPI and yearly sunspots. From 1700-2012 that correlation was -0.02, so almost zero.

I then split it up by century. From 1700-1799 the correlation is -0.03. Between 1800-1899 the correlation is -0.15. Between 1900-2012 the correlation was +0.15

That’s too weak to be significant, given the rather low number of solar cycles we are looking at.

I also looked at the most famous historic cases of hyperinflation. In France they had hyperinflation during the French revolution. The inflation peaked in 1796. Germany Weimar republic, hyperinflation peaked in 1923. And the most recent famous example was Zimbabwe, peaking in 2008.

None of these inflation spikes came anywhere near a solar cycle peak, in fact they were close to solar cycle lows.

Hi Danny, once again, the correlation applies only at the maxima. If you look for a continual correlation through all years then you are going to pick up non-sunspot-driven risk/inflation rallies. The inflation – solarmax chart shows a spike at every peak. The risk asset – solarmax chart shows a spike at every peak.

That’s what you get when there is no or weak correlation. Then you find correlation only in certain parts of the chart. There is no such thing as correlation that happens only at the peaks.

The reason why you find a peak “near” every solar max is very simple. There are 12 inflation peaks in the chart showing 6 solar peaks. So for every solar peak there were two chances for one of them to fall near a solar peak. In an 11 year cycle, the furthest an inflation peak can be away from a solar peak is 5.5 years, the average distance will be 2.75 years if there is no correlation. So, if you take two random shots at a solar peak, then chances are high that one of them will be less than two years away from a solar peak. This means there is little significance to finding these peaks “near” the solar max. And that’s why calculation shows little or no correlation. If there was a real tendency for inflation peaks to come near solar peaks, then it would translate into a significant correlation coefficient.

Also, you can make a spectral plot for inflation rates since 1700. I did so and no significant peak is seen anywhere near 11 or 22 years, which tells us that the sunspot cycle is not showing up as a factor in inflation rates.

It is what it is.

There’s no such thing as correlations that happen only at the peaks? Tchijevsky’s study of 2500 years of human history versus sunspot maximums would argue otherwise. You can find charts on my site showing corn and cattle peaks lining up with solar peaks and spectrograms for wheat and the Dow showing the dominant cycles to be the solar cycles. But I understand I am wasting my time, as you have made it clear you think it’s all false, and in which case I can’t help you Danny. I can only repeat that time will tell, as we are in the window of a solar maximum.

Hi John. I am talking about the weak correlation between sunspots and inflation, not with the Dow or wheat.

If you consider it a waste of time to look into what other researchers have found, then that’s OK with me. At the end of the day it is your blog.

People who are interested are welcome to check out this article: http://www.timingsolution.com/TS/Articles/Inflation/

He found just the same like I did for the Norway cpi data. The dominant cycle is 28 years, and the signal at 11 and 22 years is particularly weak, as you can see in the spectral plot. This suggests there is no connection between inflation and the sunspot cycle. This is for UK inflation between 1666 and now.

By the way, Tchijevsky did not find correlation at the peaks only, he studied the entire cycle and found more conflicts near solar max vs the number of conflicts near solar min. The peaks only exist in relation to the rest of the curve, which then supposedly contain the bottoms. So any correlation, if it exists, always encompasses the peaks and the bottoms. There is no other way.

Found a recent article that’s very bullish on Hong Kong. The article suggests the Hang Seng could go from 23,000 today to 50,000 by 2015.

http://www.scmp.com/business/article/1237075/morgan-stanleys-bull-tail-sees-hang-seng-50000

Cheers. Hong Kong real estate is very overvalued, and China’s demographics are turning bad, so I’m staying away.

In my opinion, deflation is underway, but I could be mistaken, look at PPI, commodities in a down-trend since 2011, look at Oil, nice divergence with S&P500.

US PPI> http://advisorperspectives.com/dshort/updates/PPI-Headline-and-Core.php

Thanks. Disinflation, rather than deflation, I’d say.

US Industrial Production>http://advisorperspectives.com/dshort/charts/indicators/Industrial-Production.html?INDPRO-YoY.gif

Hello! Some recessions have occurred in the years of minimum of solar activity. Later in this article I will explain why on the basis of medical experiments Academician Y. Gurfinkel http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2702909