New highs in US equities despite…

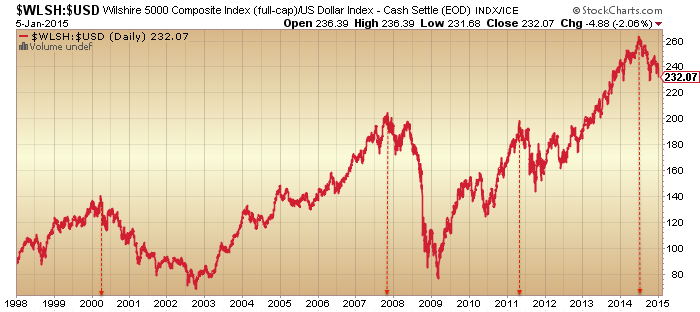

1. Valuations on a par with the 1929 peak

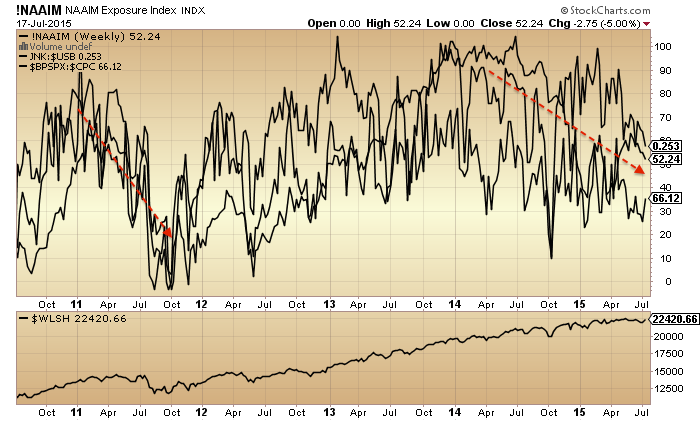

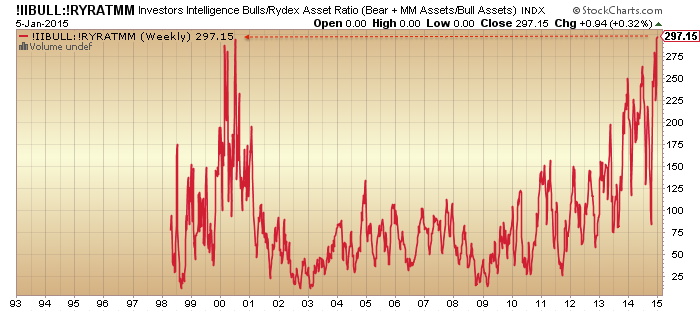

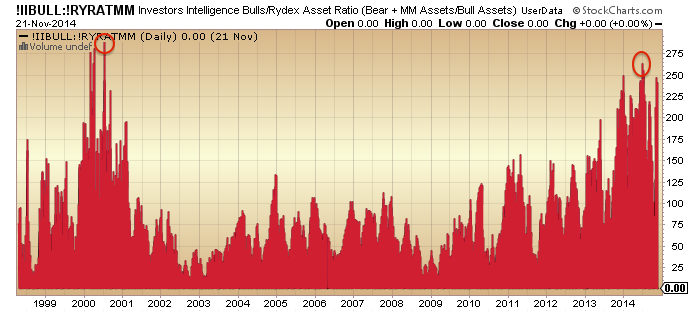

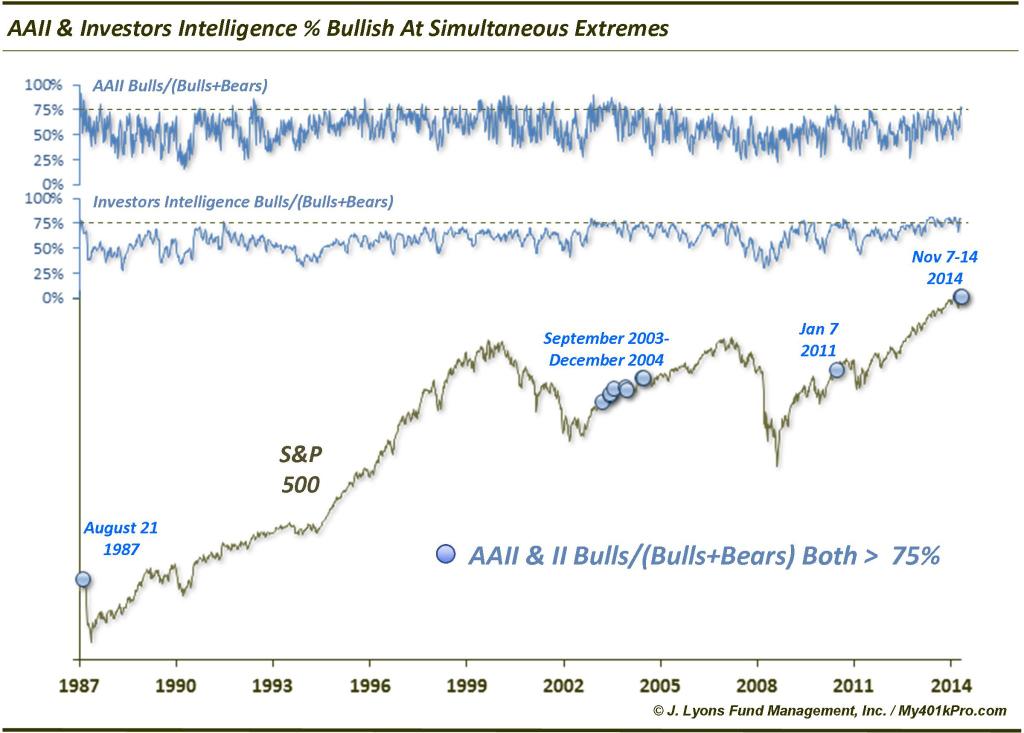

2. Sentiment extreme lopsided (II 3.5x bulls vs bears, NAAIM 84% bulls)

3. Allocations to equities on a par with 2000 peak (household, fund manager, Rydex)

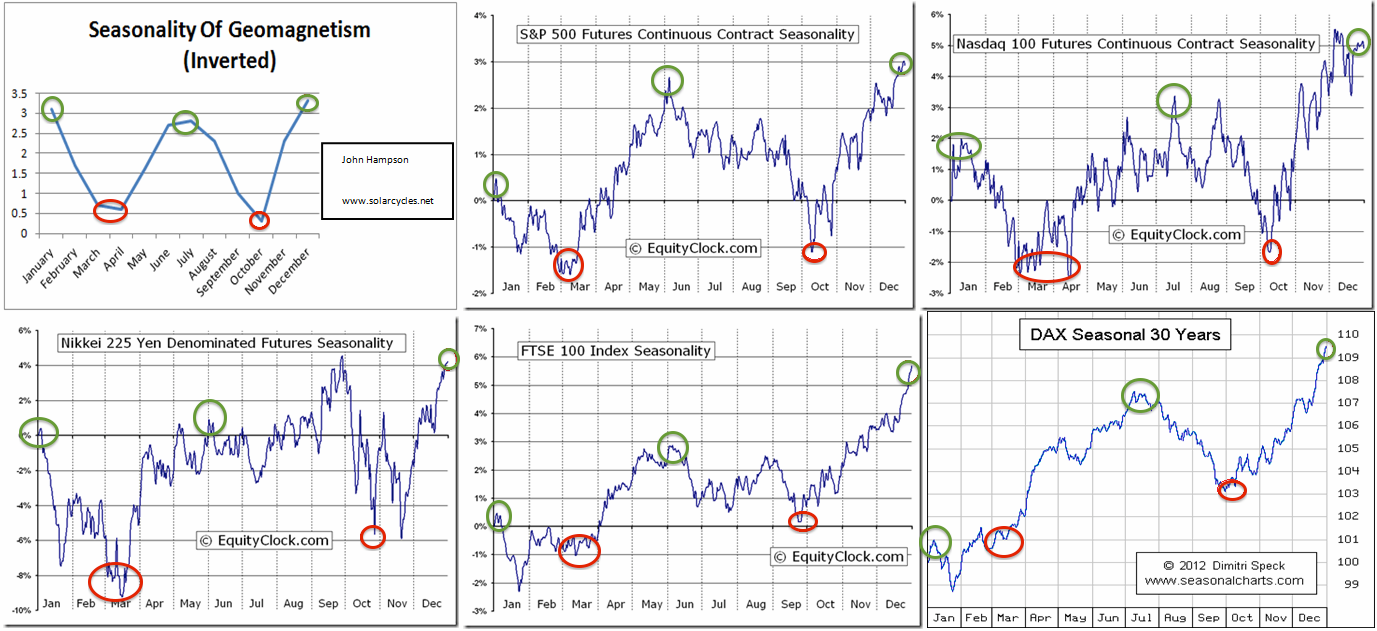

4. The solar maximum speculation peak being behind us in April 2014

5. Leverage having peaked out around then (margin debt Feb 2014, leveraged loans July 2014)

6. Multiple negative divergences in place 6-12 months (shift to defensives, breadth, financial conditions)

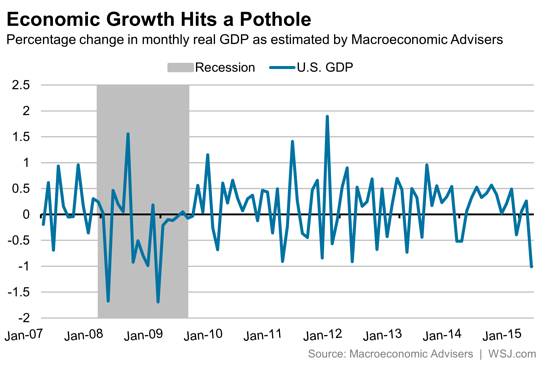

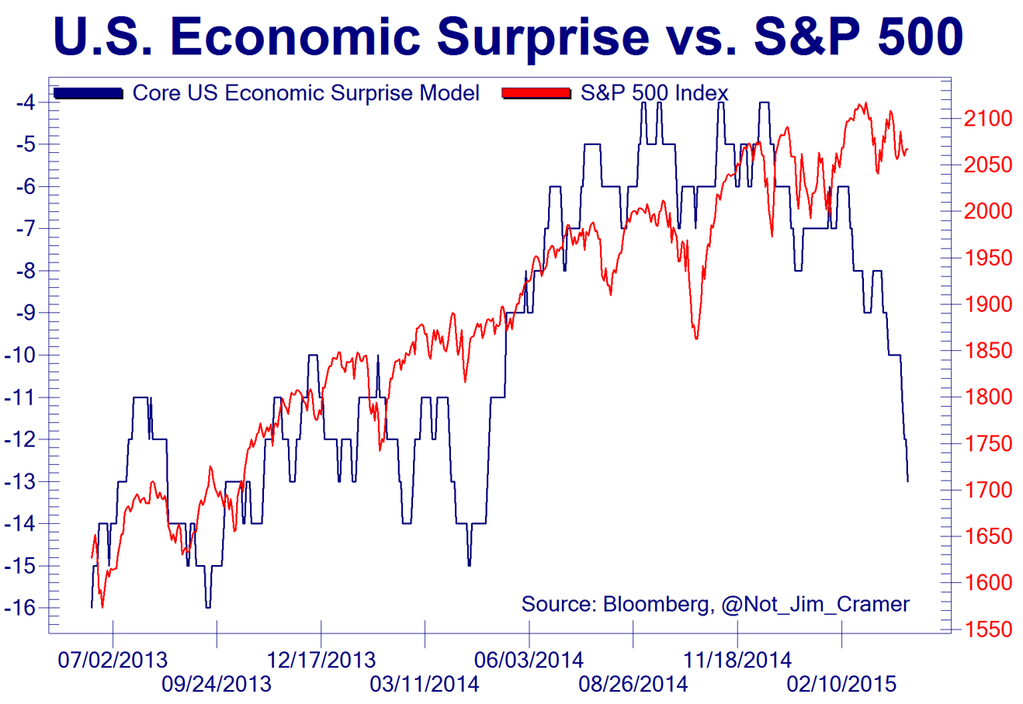

7. Economic surprises negative

8. Leading indicators negative

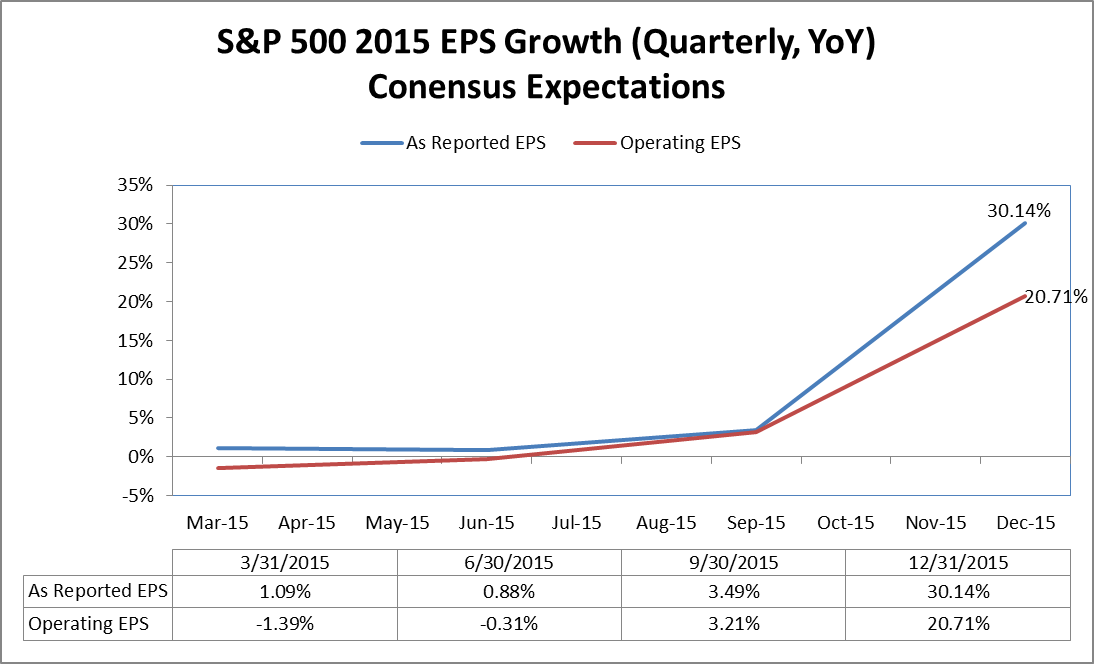

9. Earnings growth forecasts for H1 2015 negative

10. Buybacks peaked in Q1 2014

This is already so anomalous that I can’t offer much more by way of analysis. If there is a blow-off top about to unfold, then what is the fuel, given the extremes in allocations and sentiment and the stall in leverage and buybacks, plus the demographic headwind making for a shrinking investor pool? I believe it would have to come from leverage breaking its 12m ceiling and going to all-new extremes. But why would that occur, given the state of economic and earnings indicators versus valuations? And given we are approaching 12 months post solar maximum? It makes no sense.

I can still only side with logic, which says the real peak was mid-2014 and that this still represents last gasps of a topping process. That would mean nominal stock indices make marginal new highs here but then break down.

On the bullish side, there have been a couple of supportive developments. Cumulative advance-declines have broken upwards decisively, as they did in February 2014. Plus, cyclical sectors have taken over outperformance from defensive sectors now in 2015. These two developments alone certainly don’t overcome the list above, but, if stocks can now hold up whilst we go through the seasonal lows of March and April then we could perhaps again see economic surprises and earnings start to turn up again. In short, we could continue to see the market advancing in positive economic and earnings periods but not falling in negative periods despite the record lopsidedness, negative divergences and so on. Go figure.

That would in turn likely postpone the bear kick-off until the Autumn/Fall. I can’t compute that, but we have to consider the majorly anomalous here. Of course this can’t continue indefinitely. If stocks do somehow take off again here, then valuations, leverage, allocations and divergences will become yet more extreme, perhaps all-time extreme, making the subsequent crash even bigger and even more pressing.

But survival is key. So I have stepped aside and taken off my positions whilst we see how price action now unfolds. If we see a blow-off mania now somehow take hold, then I don’t want to hold short through that. If, instead, logic reigns, then stocks should only make marginal highs here on negative divergences and then be dragged down to new 2015 lows. We have the new moon on the 18th Feb into which I expect stocks to rise. Then we have the seasonally weak window into March and April. So either stocks make marginal new highs and then fall post 18 Feb into Mar/Apr to new 2015 lows, or they hold up and lift off through those seasonal lows heading for even higher highs in the summer. I will be looking to add back positions on evidence of the former unfolding.

Cross-market, gold’s behaviour will be another tell. If the bottom is in then gold should start to take off again here, making for a compelling higher low. Continued weakness and even a new low would postpone the whole process.

I still can’t regret my analysis, because it is as comprehensive and multi-angled as I could make it, and I still think the only logical outcome is that we do indeed look back on a topping process that kicked off at the start of 2014 but took a long time to play out. I can’t compute anything else, because I bring together such a wide range of angles and draw heavily on ‘fact’. However, it’s been a humbling 12 months and there is not yet sufficient clarity or hindsight to really diagnose it.

I host the website but you guys have created an excellent board, which is always a great read. Different opinions and approaches but there is a good balance and a lot of quality input. So thank you to all who comment.

So, let’s see now whether stocks break out decisively or fail at marginal new highs, whilst watching how gold performs.

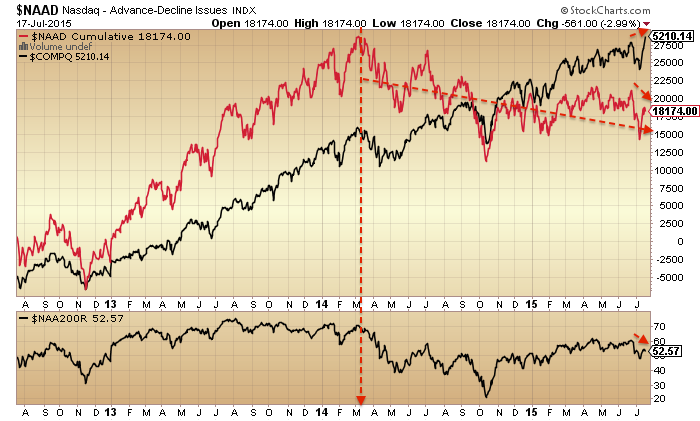

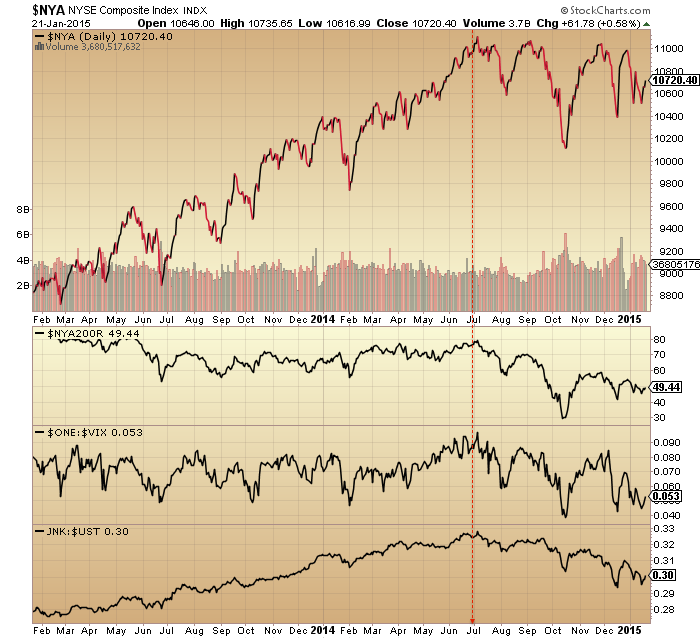

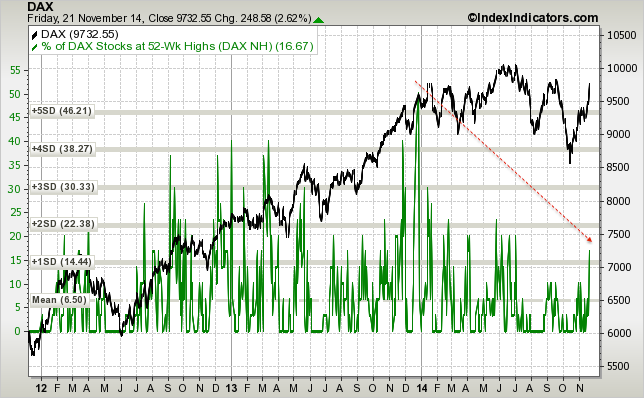

The Nasdaq has outperformed the other indices to make new highs with the rally back up, but breadth is flagging a clear warning.

The Nasdaq has outperformed the other indices to make new highs with the rally back up, but breadth is flagging a clear warning.