No collapse in the stock market, which makes the case stronger for a more regular multi-month topping process. It would be historically normal for equities to retest their May highs and even make a marginally new high, then complete a volatile trading range by around September time before falling in earnest.

Also historically normal would be if commodities outperform from here, with bonds having topped first, then stocks topping, and eventually commodities topping out, likely in 2014. The continued falls in bonds – and rise in yields – adds weight to bonds having topped – and yields bottomed – in 2012. Now are world equities in the process of making their top?:

Source: Bloomberg

Source: Bloomberg

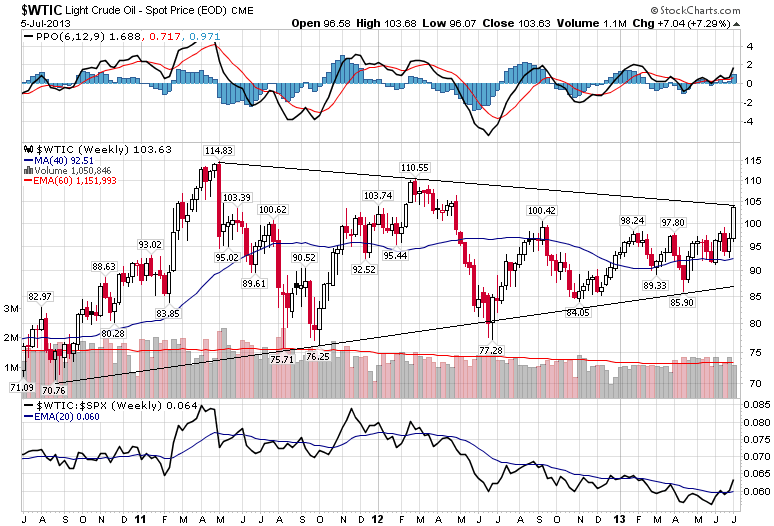

The strong advance in crude oil of late has added more weight to commodities going on to outperform here, rather than the historically abnormal but deflationary case of commodities sinking. The combination of protest and unrest in Egypt together with speculation in crude oil are both historically normal for a solar maximum, so I am encouraged. Nonetheless, crude oil has yet to truly break out and some geopolitical dampening could pull it back:

Source: Stockcharts

Source: Stockcharts

If crude does continue to rise, then commodities as a whole should catch a bid, due to high historic correlation, with oil a a key input in the agri process and a key inflationary force, which brings us to gold. Gold has dropped around 30% from its 2011 high, which is similar to the percentage drop made in 2008. It has the potential to be making a bottom here with a higher low than in late June, and the longstanding overdue bounce based on extreme bearishness, but only if it can rise this coming week, which brings back to oil’s performance, plus also the US dollar.

The recent strength in the USD has taken the currency to back up to a key level. Below is the long term view and the potential for an important breakout:

Source: Rambus / Stockcharts

Source: Rambus / Stockcharts

However, as per my demographic work, I believe leading indicators will weaken and gold will re-assert itself, and US stocks will top out here reducing demand for the dollar. Here is some evidence to support that view.

The latest global PMI combined services and manufacturing dropped to 51.4 from 52.9 and continues the overall weakening trend over the last few years. This is as I would expect under the combined deflationary demographics of USA, China and Europe since around 2010.

Source: Markit

Source: Markit

The performance in corporate bonds suggests US housing may be about to turn down again also:

Source: Martin Pring

Source: Martin Pring

And margin debt continues to look an important pointer for the stock market. See below how a sharp run up in margin debt, a final parabolic rise, precedes the 2000 and 2007 tops in the SP500 by several months. We have seen a similar parabolic rise since mid-2012 to now and there is the possibility that margin debt peaked out in April which would suggest stocks should indeed be in a topping process now and over the next couple of months:

Source: Dshort

Source: Dshort

If stocks are topping out then normal clues would be found in negative divergences in stock market internals and leading indicators. For the former, we should look for breadth divergence once we see a retest of the highs. For the latter, we have the potential in the global PMI above, but also in this leading indicator of leading indicators, by RecessionAlert:

Source: RecessionAlert

I have enquired with them what this MBS indicator is, but have no reply. If anyone knows, please share. But it would fit with my demographic-deflationary expectations.

We also see a potential divergence in geomagnetism, if equities can now rally again to a retest of the highs:

The ideal combination by my work and research is for commodities to outperform again now into next year, and make a speculative peak near to the solar peak (the timing of the solar peak remains unknown, with the experts still diverging. Sunspots are currently back up over 100, which adds to the muddy trend), then deflationary demographics to mean the global economy fairly quickly tips into recession under that commodity price pressure, and then we should see the steep falls in nominal stocks. My alternative scenario is that the deflationary forces are too great and commodities in general sink with just gold, as the anti-demographic, eventually coming again alone.

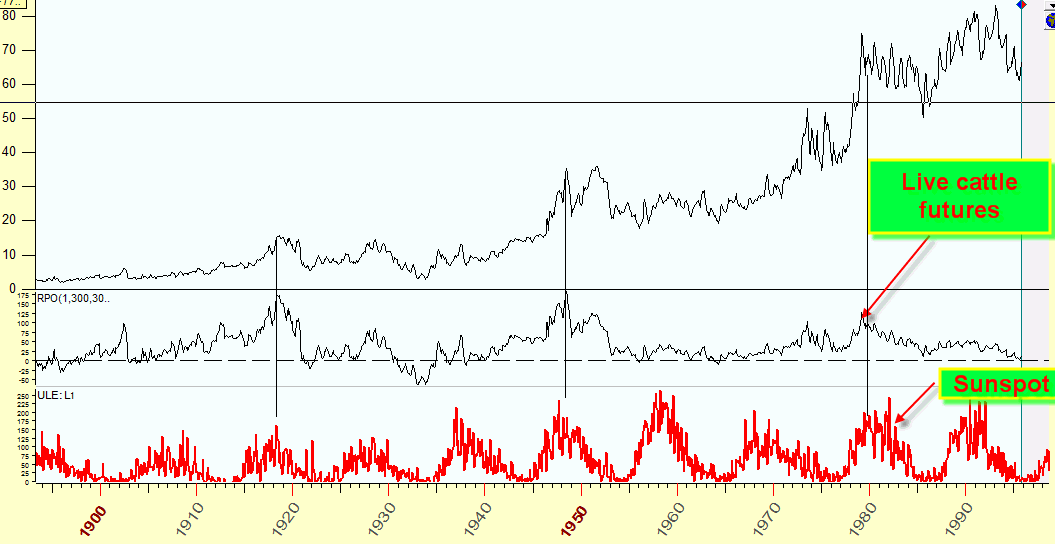

In support of my primary scenario, the action in live cattle has been very much aligned with solar history, with what looks like a peak earlier this year:

Source: Tarassov

Source: Tarassov

Source: TradingCharts

Source: TradingCharts

Now we need to see other commodities make a fresh rally to new highs, assuming a solar peak is still ahead.

This week we have the new moon on Monday and the end of the lunar positive period by Thursday. So I am ideally looking for equities to rise further in the next couple of days and make that retest of the highs or marginally higher high, then retracing again in the negative lunar period ahead, to further the technical look of a topping process. If we get that retest of the highs then I will be looking to sell equities longs and add short. But for further support I would like to see oil break out, commodities to rise en masse and the US dollar to be turned down with gold catching a bid at last. Let’s see how the action unfolds.

Oil often plays a different game. But please remember that silver has confirmed the bubble in 2011 (new lows and has more than halved). If my indicator shown here is right, we could see an important low in Gold at the end of the year / early next year. And that could be $ 1,000 or less.

I just want to make it carefully. Of course that would be a good buying opportunity.

Thanks Rolandu

THanks for more valuable information.

about gold I let this link, that is intersting

http://imarketsignals.com/2013/gold-how-much-lower-will-it-go/

and about recession this graph is very very interesting:

http://advisorperspectives.com/dshort/guest/Georg-Vrba-130503-Unemployment-Rate.php

Thanks Jose

I actually think a recession also started in 2012 in the US and that is without looking at ECRI. I just observe around me. I also do not think unemployment is a good guide to indicate when a recession begins and ends. There is always a lag. Consumer confidence is a better gauge for inflows and outflows ergo GDP.

Unemployment is like inflation, impacted by and a aggressor of and during recessions.

Looking at the Real Estate we can see has already turned down.

http://stockcharts.com/h-sc/ui?s=VNQ&p=D&yr=2&mn=0&dy=0&id=p43145866091&a=251824803&r=1373226915206&cmd=print

Thanks Niels

Great charts Niels.

“It would be historically normal for equities to retest their May highs and even make a marginally new high, then complete a volatile trading range by around September time before falling in earnest.”

More or less what I’m also looking for, but with mid-August being my cut-off date, for now anyway.

Nice work as always. BTW, the difference between a negative and a positive lunar period?

Description here: https://solarcycles.net/the-lunar-edge/

Okay, I’ll let you in on what confused me: it looks like a buy recommendation on the 4th day after both new and full moons . . . but now I realize (after your insistance that I go back to that original page) that what you’re really communicating there are the *testing parameters* you used for comparative purposes: you analyzed theoretical returns buying on the 4th day after both new and full moons IN BOTH POSITIVE AND NEGATIVE PERIODS. I was scratching and wondering about the buy on the 4th day after regardless of negative or positive periods . . .

All that just to confirm that the positive period is the full moon to new moon period. 😉

You know what they say? Explain it to me as if I were 6 year old. 🙂

Lol. Think you’ve understood it now HR.

Well since HighRev openly admitted it, I was a bit confused too a month or so back when it came up in discussion.

hi,

if I am not wrong then it should be ” the end of the lunar positive period by Thursday”

p.

Thanks, corrected

john….this may help.

http://recessionalert.com/sample-report/

Thanks, but still can’t find MBS in it

Its time for MKT to decide deflation vs inflation scenario now. If 2010 scenario were to repeat, then DX should PB from here and PM and COMMODITIES should rally, which aligns well with John’s Primary scenario. Else, Stock market correction with deflation scenario for few months, atleast.

Thanks

Gold is not likely to create any noteworthy peak any time soon. Some rallies we will get, since nothing keeps going down in a straight line for years.

But when you have the kind of losses we have seen in gold and gold stocks recently, after a 10 year rally which started to pull in many small investors at the end, then it typically takes years to recover because there is too much pain in the market. There are too many small investors who bought late and still hope to get back to break even, as well as many who tried to pick the “bottom” when gold was at $1500, $1400,… A lot of them will start selling as soon as gold gets back anywhere near these levels. And some gold miners will start hedging their production again when gold gets back up to 1400.

The current gold decline is often compared to the 1976 bottom. But, then it also took 4 years to get to another peak. So, that’s the best case scenario. If gold is still in a bull market, then look for another peak 4 or more years from now.

Makes sense

Some claim there is an 8 or 9 year cycle in gold. The last 8 year cycle low was in 2008. The current 8 year cycle topped in 2011, so if that cycle exists, we’re not likely to see a final low in gold until 2016, which means new highs in gold may not occur till 2017 or later.

My main scenario is your alternative one, deflacionary enviroment, down-trend for Commodities, USD up, EURUSD to the parity in the end 2015-16 and falling process in Us indices

Cheers

Yes, Antonio it’s you and me against the world.

That´s is a good signal, Kent

John, for recession alert …I believe MBS is mortgage backed securities derivatives purchased by Fed and/or newly generated MBS purchased on open market (as reported), does FRED show this data to where you can produce a similar graph line? The drop depicted would make sense for rising rate and changed real estate market as well as its impact on recession indicators. Less refinancing, new starts, lower Fed bond buying…

I’ve looked at it on FRED but can’t see the correlation. Without an explanation that abbreviation was my initial guess but I just didn’t imagine it would be it.

Perhaps its YoY computed value plotted?

http://www.drought.gov/drought/

Pretty extreme

Updated all models this morning. Geomagnetic trend still down, sunspots on the rise again.

Russell 2000 hit new high yesterday. Ideally looking for others to follow suit in the next couple of days before lunar positive period ends.

US earnings season under way again as a market mover.

OECD leading indicators yesterday came in fairly healthy.

Dear John,

See this link in Google:

connection.ebscohost.com/c/articles/14980753/impact-of-affordability-product-mbs-growth

Unfortunately the article referred to can only be viewed as a whole at “your local library”, where this company offers a source service. “My nearest (such) library” is quite a distance. Maybe yours is nearer… and you could report?

Thanks!

Best regards,

locan.BBS