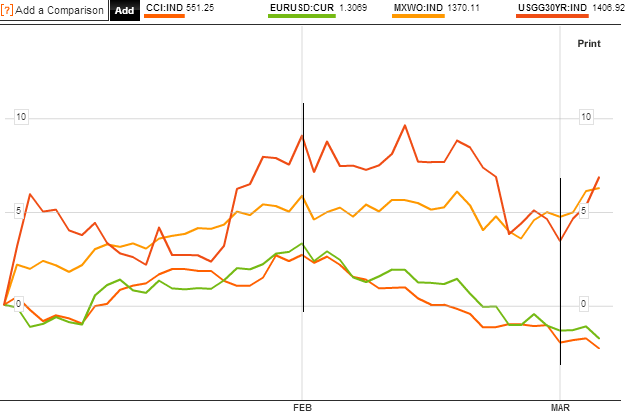

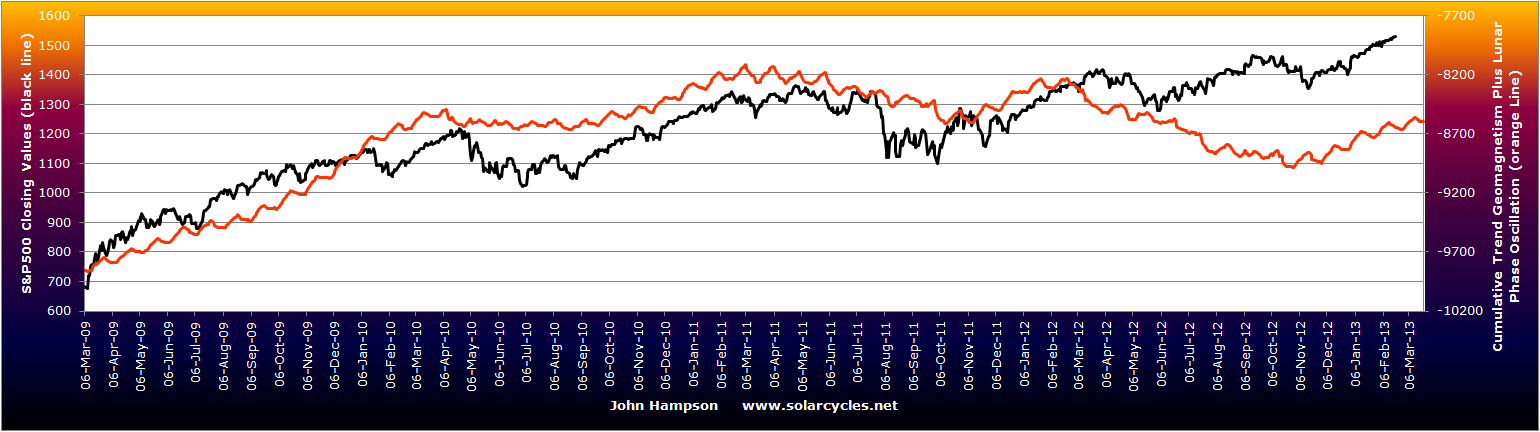

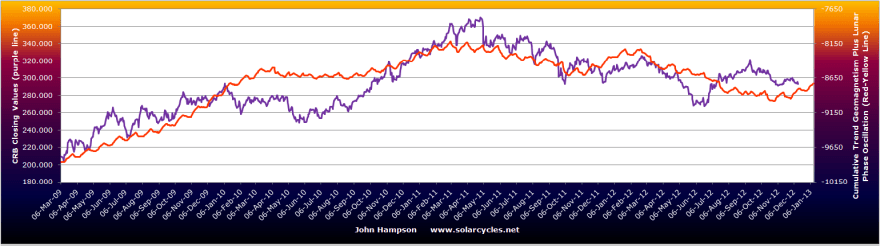

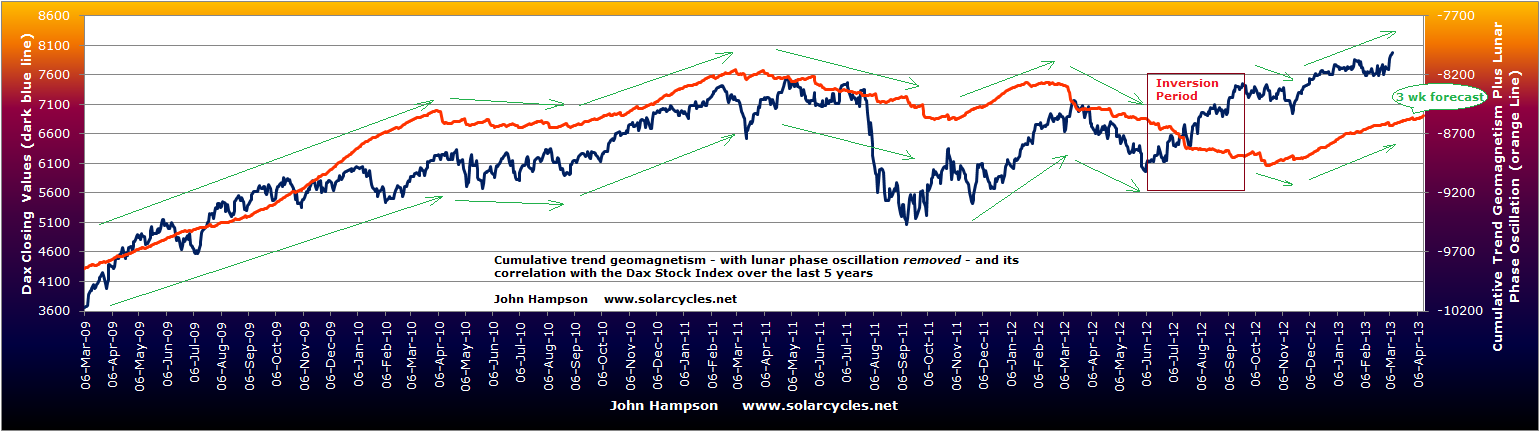

Four years of the cyclical stocks bull (in certain indices) gives me four years of the lunar geomagnetic model. If I remove the lunar phase oscillation (up and down alternate pressure between new and full moons) I can show you the chart showing purely geomagnetism. To be clear this is daily geomagnetism made into a cumulative trend line, with a 6 day lag as per Robotti/Krivelyova research, and nothing else added.

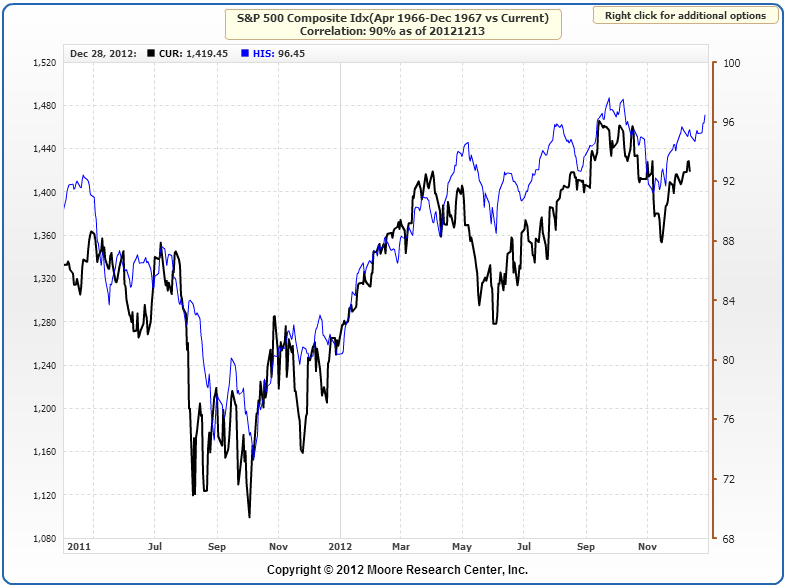

First is the model versus the SP500. The waves in the two lines align well, with the exception of the period mid-year last year, which appears to be inverted, similar to the inversions phenomenon we see elsewhere, such as in lunar phasing. The tail on the geomagnetic line is the NOAA forecast covering up to 3 weeks into the future. Click to view in more detail:

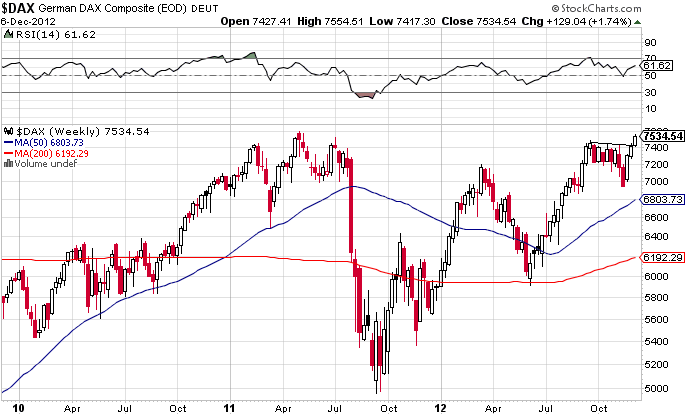

The second chart show the Dax versus geomagnetism, and whilst the Dax and SP500 have on occasions peformed differently, there is the same overall close alignment of the waves, with the same inversion exception last year.

The third chart shows the Reuters Jefferies commodities index, which again has gone its own way at times compared to the stock indices, but nevertheless the waves align well again, and the single exception period is the same.

Levels of geomagnetic disturbance in the atmosphere has been shown to impact human mood. If changes in mood subtly affect the collective behaviour of market participants then we might expect to see some correlation between risk assets and geomagnetism. I believe the above charts are good evidence that this is the case. Yet, I know of no-one else who runs a geomagnetism model and I can count on one hand the number of analysts/sites out there that track geomagnetism to use in their trading toolkit. Maybe this is more widely followed than I imagine, but it is not promoted as it would not sell to clients – I don’t know.

If the model fails badly going forward, then I will not be defending it. But looking back at the chart from the Peak v Peak page, showing geomagnetism versus the SP500 around the last secular peak, there appears to be more historical evidence that it is influential. I again have removed the lunar oscillation and show you the alignment of the waves. Once again there is a single period where the model inverts with the market, and in this case lasted around a year.

So how might we use this as traders and investors? I don’t see a way to parcel this up into a repetitive trade. I suggested in my Trading The Sun pdf that trades would present themselves when the market moved away from the model. But there are times when they don’t come back together for some time. I therefore suggest that it is better to follow the general path of geomagnetism, and use it as a guide. Occasionally there may be a period of inversion – for reasons unknown – but largely it should be a useful guide. To this end we can use the 3 week forecast to look ahead, and the seasonal model of geomagnetism that shows us how historically geomagnetism tends to flare at certain times of the year more than others (whilst understanding that occasionally we may see unseasonal behaviour). I therefore rate geomagnetism as an important tool to use along side other market disciplines.

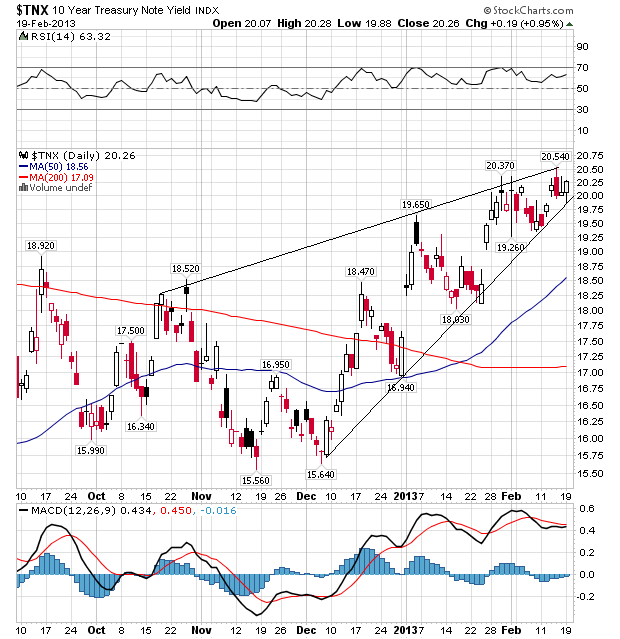

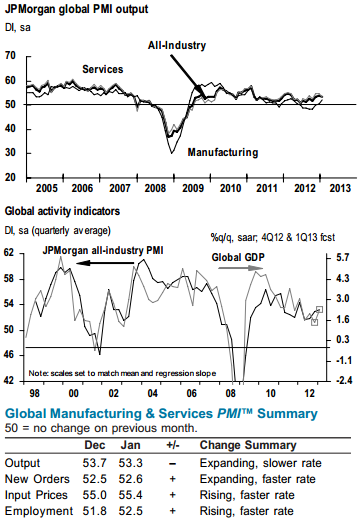

To the markets. I am staying put at the moment, still expecting commodities to start to outperform stocks, and weighted accordingly. CB leading indicators for Japan and Spain came in strong. OECD leading indicators for OECD countries came in strong bar China and India. Leading indicators as a whole do not show degredation, which I would expect for a cyclical bull top. Breadth remains supportive in equities. The SP500 is within a few points of the 2007 high and I expect a touch. This is roughly where Tom De Mark expects a swing top. If we can push up to there this week I may take off some equities profits. I have hope at this point that we are headed for yields rising, inflation rising and commodities making a belated push to help tip the world into a mild recession into 2014. These are all features of how previous cyclical bulls have ended, and until now (since 2009) we have not had enough sustained growth to get us to that point. If global growth can persist a little longer, then more money should pour out of treasuries and into pro-risk. We need froth and excess and growthflation to end the cyclical bull if we are to align with history. Before reaching the cyclical bull top, a pullback in equities would be normal, followed by a higher high with divergences. Should such a pullback occur, we should see commodities becoming the target of the money flow and advancing despite equities. This is all as per history – anomalies can occur – but that is my primary scenario.