Hi all, in a cafe with Wifi, due to storm-damaged internet access at our second hotel (neat Ubud, Bali), so will get down to it.

My trading boils down to this. I am long commodities, attempting to time the secular bull market top. I am long stocks, attempting to gauge the cyclical bull market top. And I am to a smaller extent short treasuries, believing us to have made a secular bull market top in treasuries this mid-year. Currently I believe all these still look good.

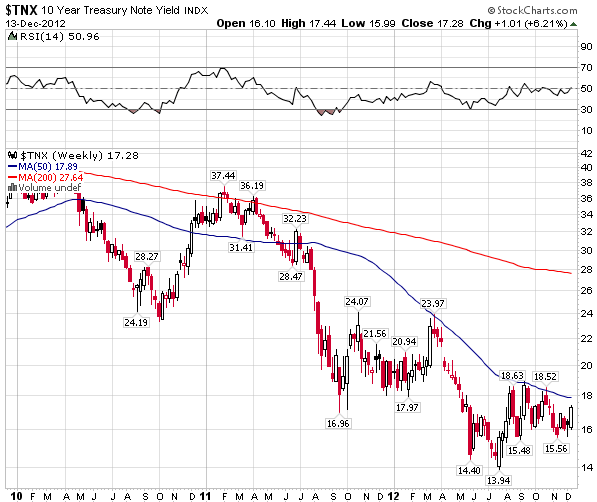

Treasuries are still ‘potentially’ making a W-bottom. By Gann they should have bottomed mid-year, and ditto by solar/secular history, which predicts yields should now rise into a stocks cyclical bull top. Still very tentative, more time is required to judge this one.

Source: Stockcharts

Source: Stockcharts

Regarding the cyclical bull market in stocks (within a secular bear market), there are several ways to assess its likelihood of continuation:

1. A topping process lasting months with reversals of reversals of reversals – as the Hang Seng, Dax and now the FTSE have broken out of their long term triangles I don’t think this is happening yet, though US stocks show the most potential.

2. Overbought and overbullish extremes – we see largely neutral sentiment readings and only short term overbought readings (which I believe has produced the pullback of the last two days).

3. Breadth divergence – NYSE breadth has just made an all-time high, which is bullish.

4. New lows confluence prior to top – we haven’t seen this leading into the US Q3 highs.

5. Defensives outperforming cyclicals – again not seen, cyclicals have been strong.

6. Major distribution days near the highs – we did see these near the US Q3 highs, but since we have seen major accumulation days, which are bullish.

7. Rising inflation, tightening yields, yield curve flat or negative – we don’t yet see these macro developments

8. Rolling over of leading indicators and recession model alerts – we see evidence for growth into Q1 2013 – more below.

The latest CB global leading indicators revealed positive strong for Spain and Korea, but slightly weak for UK and Japan. The latest OECD leading indicators show weak growth but overall above long term trend for the OECD nations:

Source: OECD

Note the horizontal lines are the long term growth trendlines, rather than expansion/contraction divide. Drawing out the narrow money supply leading indicator, the forecast is for global industrial output to increase into Jan/Feb 2013:

Source: Moneymovesmarkets

Source: Moneymovesmarkets

HSBC’s flash PMI for China today came in at 50.9 for December, a 14-month high, adding weight to an upturn in China, and Chinese stocks continue to attempt to make a bottom, with a further 3% jump today at the time of writing.

Economic Surprises have recently weakened for both the US and Asia, but both remain positive. One to watch, as a trend change in this indicator has previously led a trend change in equities.

Commodities have been weaker than equities this last couple of weeks, but I believe they will catch up, with support from an improving China, an improving Euro-USD, depressed sentiment in certain commodities and gold miners. We just passed through the new moon, but with very tame geomagnetism there is support for commodities to rise into year end, as shown by the new model uptrend here:

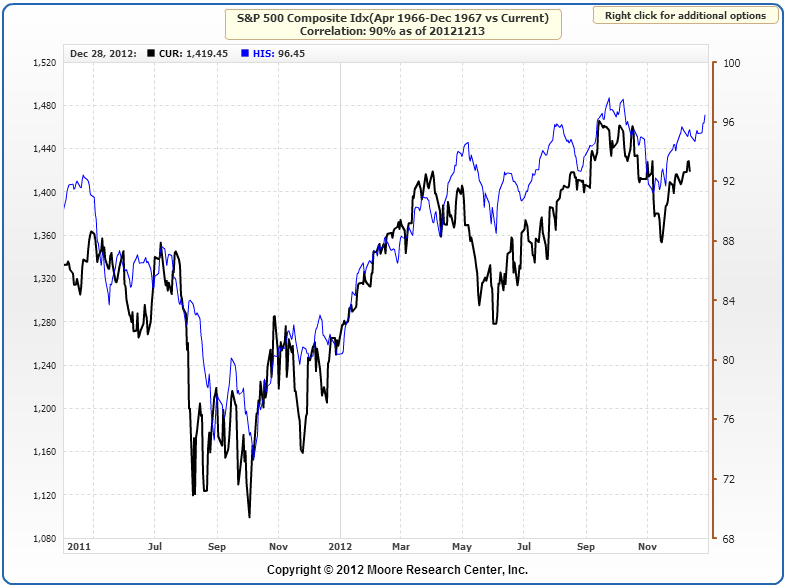

Finally, a look back at history reveals that the closest mirror for US equities from history is 1967, with a 90% correlation. I find this interesting, because 1968 was the secular equities top and the solar peak – around November/December 1968. In other words, equities are behaving very similarly, as we head into next year’s solar peak, which I anticipate to be a cyclical stocks peak and then secular commodities peak.

Source: MCRI

Source: MCRI

In short, I see no current reason to change my outlook that the secular commodities bull and cyclical stocks bull will continue into the start of 2013. I continue to watch all the measures and indicators outlined above, and believe my first move will be to close of out of the bulk of equities longs, but as yet we do not see typical topping indicators nor compelling divergence in leading indicators.

Currently we are planning to spend a further week and a half in Bali. The rest of our trip is looking like this (subject to change of course, as we are booking and ‘feeling it’ as we go): Thailand, Philippines, Hong Kong, New Zealand, Fiji, Australia, Sri Lanka and maybe Maldives. There are other countries and continents we would dearly like to visit, but we have to draw the line somewhere as time is limited.

Have a great weekend all.

All models updated this morning

Do not miss Philippines… Specially Palawan! Check Coron/Busuanga & El Nido …

http://www.marketwatch.com/story/leading-indicators-of-a-stock-market-top-2012-12-14?link=home_carousel

Hey John. What commodities are you long? I have been going for nat gas cos. i.e. XCO etc.

I am long a range of commodities – the commodities themselves rather than stock sectors. Biggest weightings in precious metals, energy and agri.

When talking about Gann what exact study are you referencing to?

Wikipedia article on Gann:

http://en.wikipedia.org/wiki/W._D._Gann

Gann Global

Thank you. PMs are certainly testing us here.

http://stockcharts.com/h-sc/ui?s=$SSEC&p=D&yr=0&mn=9&dy=0&id=p51489567867

Looks good for Aussie commodities next week

Hope the trip is going well John. Got a bit of stuff to share today, sorry if it bores everyone. The Gold Price has been reversing the gains of the QE3 rally. It’s now below the level it had been at when QE3 was announced by the Fed. Some are saying there’s a bit of late-year selling for profit-making, but there are several other reasons to consider.

Currencies are strengthening. The trade-weighted Dollar index has held in recent weeks, and the trade weighted Pound sterling index has seen strong gains in the past year. The trade-weighted Euro index has been recovering, having made a low in July. Meanwhile, bond prices have failed to surpass the July peak, whilst stocks are charging higher, and are even climbing a wall of worry, despite the fiscal cliff not being resolved fully.

If there has been a secular inversion already, it seems the commodities bull went out with a whimper and it will go down as one of the most unexpected shifts, as people are still saying Gold didn’t go parabolic like 1979-80. The 1970s gold bull was the first of its kind, and the latest one is only the second prolonged period of rising nominal Gold prices, so we shouldn’t assume it will repeat necessarily.

Parabolic prices by 1980 make sense, because there was genuine fear of hyperinflation thanks to double-digit inflation due to over-dependence on imported oil. However, with the current situation, QE rounds and LTROs have been initiated but the money is stuck on the balance sheets of central banks, not into the monetary base itself. We haven’t seen the wave of hyperinflation Gold bulls are constantly predicting; at best, inflation in Europe and the US averages 2-3%. Plus, oil prices have failed to soar past 2008’s high.

My advice would be to take the prediction of a new Gold standard with a pinch of salt. People who are predicting a new Gold standard have an agenda to push, as they have decent quantities of physical Gold, which would benefit them greatly, should the creation of a new Gold standard occur. The Keiser Report also has an agenda to push, so just because Max Keiser says “buy PMs on the dip”, it doesn’t mean he has any idea which way PMs are going to go. Always make your decisions, based on your own judgement, not someone else’s.

Thanks Pete