I’ve suffered poor internet access this week, but have it now, so let me catch up on developments since last Friday. I will respond to comments and emails in due course, but first, analysis.

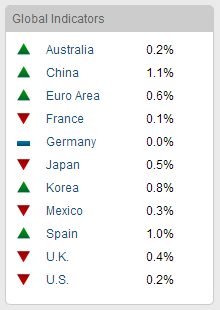

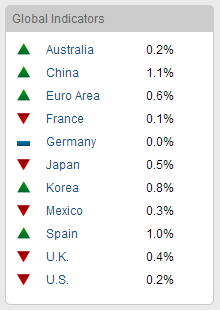

Conference Board leading indicator updates have been mixed. USA, France and Mexico slipped negative. Germany improved to flat and the general Euro area jumped into the positive. Australia also moved into the positive and China put in another good month. The summary table currently looks like this.

Source: Conference Board

Source: Conference Board

So a continued picture of mixed fortunes, but with a rotation in leaders, and overall a picture of weak growth ahead, rather than recession. ECRI leading indicators for the US advanced from 3.5 to 4.4 last week and US economic surprises have picked up again the last couple of weeks:

Source: Ed Yardeni

Source: Ed Yardeni

Euro debt, which bothered the markets from mid-2011 to mid-2012, has deflated as an issue, to much more benign levels.

Source: Acting Man

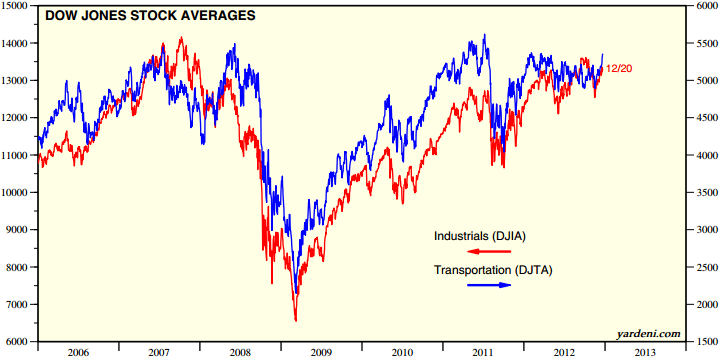

The Dow theory divergence of mid-year, which was a potentially bearish signal, has been resolved, with Transports since resuming strength:

Source: Ed Yardeni

And cyclical stocks in the US continue to perform strongly, with breadth also healthy.

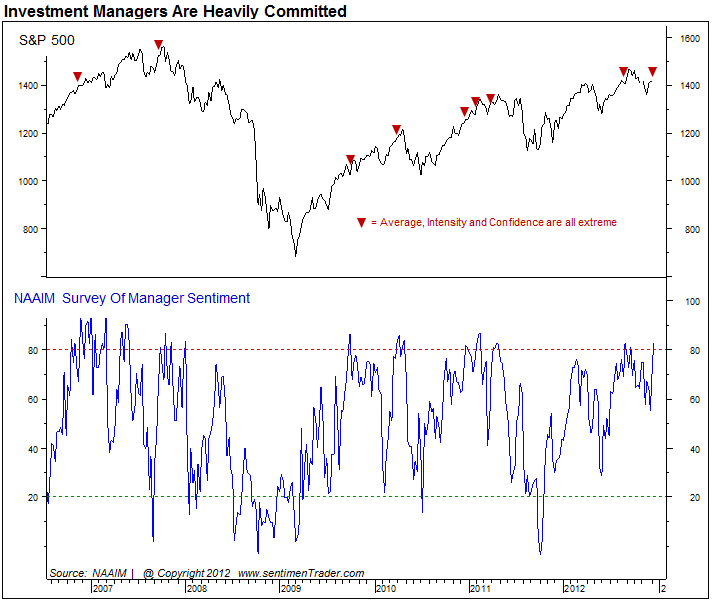

However, sentiment for US stocks has reached into frothy bullish territory in both NAIIM and AAII surveys:

Source: Sentimentrader

Source: Sentimentrader

Source: Bespoke

Source: Bespoke

Investors Intelligence and bullish percent over call put ratio both however remain in neutral territory, but overall risk aversion has reached very low levels:

Source: Big Picture

Source: Big Picture

Meanwhile, the Shanghai Composite has pulled up in a more compelling bottoming fashion, as the drop beneath shown support now looks like a fake out.

Source: Cobra / Stockcharts

Treasuries have declined and yields have added credibility to a W-bottom:

Source: Stockcharts

Source: Stockcharts

Copper remains in a triangle, unprepared to give a diagnosis on the global economy at this point:

Source: Stockcharts

Source: Stockcharts

And crude oil ditto:

Source: Trading Charts

Source: Trading Charts

November’s global climate stats from NOAA came in at the 6th hottest on record, making the year to date (minus December) the 5th hottest on land since records began. That’s a continued support for agri longs, as extreme conditions persist. Yet, soft commodities are, as measured by a broad agri commodities ETF, just range trading of late. Despite China’s improving fundamentals, and the Euro strengthening against the US dollar (USD technically weak formation shown below), commodities as a whole are failing to ignite currently.

Source: SeeitMarket

Source: SeeitMarket

The most surprising underperformer is gold, which currently looks like this:

It just dipped beneath the 200 MA, which has largely supported the secular bull since 2000. Is that a worrying development? It’s not great, but it is doing so on oversold RSI and a daily sentiment index reading of sub 10. Furthermore, gold miners have reached a bearish extreme in public sentiment. I still suggest that gold broke upwards out of its 11 month consolidation in August this year and has resumed its uptrend, albeit tentatively at this point. Gold seasonals, solar/secular history and negative real interest rates all support gold bouncing here and making that tentative renewed uptrend more concrete, but once again it is finely poised. I am happy with my exposure both to precious metals and to miners, but if i were underexposed I would choose now to buy both, based on the reasons I have aggregated here. In other words, I believe gold will bounce here and reclaim its 200MA (with the weak hands shaken out).

Today is the Mayan apocalypse, the Mayan hinge point, a miscalculation, or a falsehood. Tomorrow is a Bradley turn, which would mean today (due to market opening days). I do not buy in to the Mayan blogosphere phenomenon, and have found Bradley turns more miss than hit, but that said we do have some drama today, with fiscal cliff nerves helping bring about a big sell off this morning which at the time of writing has been semi-reversed. I place more weight on lunar cycles, and next week’s full moon typically spells downward pressure into it. However, this is balanced by positive seasonality which goes hand in hand with favourable geomagnetism at this time of year – the updated model shows an uptrend into early January:

It’s the morning session in Europe at the time of writing, and I don’t pretend to know how today is going to turn out, given the dramatic market action in the early hours. However, my stance is to stay put on my pro-risk portfolio currently. 1. Weakness in precious metals, 2. indecision in copper and oil, 3. frothy sentiment in US stocks, and 4. complacency in risk aversion, are all current flags. But I would contrast with: 1. oversold and overbearish readings in precious metals and miners, 2. improvement in China, leading indicators and renewed dollar breakdown, 3. good breadth and cyclicals performance, better technicals in European and Asian stock indices, and 4. money pulling out of treasuries which should seek out pro-risk assets (by solar/secular/cyclical history). Broken down into my 3 areas on involvement: I don’t want to exit stock indices longs yet because we do not yet see sufficient congregation of cyclical bull market top indicators; I do not want to exit commodity longs yet because I maintain by solar/secular history the parabolic peak is to come 2013/2014; and I do not want to exit treasury shorts yet because I believe a new secular bear market in treasuries is getting underway and a rise in yields (of some note) should be one feature of the end of the cyclical stocks bull.

It’s the morning session in Europe at the time of writing, and I don’t pretend to know how today is going to turn out, given the dramatic market action in the early hours. However, my stance is to stay put on my pro-risk portfolio currently. 1. Weakness in precious metals, 2. indecision in copper and oil, 3. frothy sentiment in US stocks, and 4. complacency in risk aversion, are all current flags. But I would contrast with: 1. oversold and overbearish readings in precious metals and miners, 2. improvement in China, leading indicators and renewed dollar breakdown, 3. good breadth and cyclicals performance, better technicals in European and Asian stock indices, and 4. money pulling out of treasuries which should seek out pro-risk assets (by solar/secular/cyclical history). Broken down into my 3 areas on involvement: I don’t want to exit stock indices longs yet because we do not yet see sufficient congregation of cyclical bull market top indicators; I do not want to exit commodity longs yet because I maintain by solar/secular history the parabolic peak is to come 2013/2014; and I do not want to exit treasury shorts yet because I believe a new secular bear market in treasuries is getting underway and a rise in yields (of some note) should be one feature of the end of the cyclical stocks bull.

Next week is usually a quiet week in the markets globally, due to Xmas, but there is the fiscal cliff deadline at the turn of the year, and so this period could be more volatile. My expectation is that agreement will be reached to prevent the fiscal cliff, and that markets will enjoy a relief rally when that occurs. However, there are no guarantees, so let’s see how things unfold. Next week I will be in Bangkok.

John, you may have already discussed the two “Great Comets” expected in 2013 but my search of the site reveals no results. Do you see any linkage between the comets and your solar cylces? The second comet, due in November, has been described as “epic” and “historical” and perhaps may coordinate with your solar and commodities peaks.

http://www.activistpost.com/2012/12/2013-year-of-comets.html

Look forward to more of your travelogue when you have time and connectivity.

Thanks Marlowe. I don’t know of any link between comets and solar cycles, and the impact of comets on human behaviour appears to be no more than some peoples historically were fearful of them. That could have some merit if the comets arrived in fairly fixed cycles (hard coding of the fear) but I don’t believe they do. Nor is there literature linking comets and behaviour. Interesting nonetheless.

Signs in the heavens presage happenings on earth -Star of Bethlehem. Everything is interconnected in the Jungian synchronisty sense

Well, the drama was deflated fairly swiftly in the end, with the markets clawing back the majority of the out of hours falls. ECRI leading indicators came in at +4.6.

The Dow Transport hit an all time high in mid 2011. The Dow failed to confirm. That is a warning. To get rid of the warning the Dow Industrials would need to go to a new high confirming the Transports high. Per Dow Theory, strength now in the Transports shouldn’t mean much. The important thing would be the Dow confirming the Tran’s new high.

One of my favorite Dow Theory stories is from way back in th 1970’s. A severe bear mkt had begun in 1966. The Dow had fallen from 1001 to 627 in 1970. The Trans had fallen from 282 to 116. From those lows they rallied to1067 and to 278 respectively. Another vicious bear ensued sending the Dow to a new low of 570 in Dec 1974. The trans refuse to confirm falling only to 124. That was a warning and the real low in the market. A confirmed buy signal did not come until 1983, but the worst was over. I have been wondering if the trans end a bear mkt and the Dow ends the bull?

It’s time to get long…. Vega….

Instead of looking into space for an answer – how about massive human market manipulation. Both USA and Europe banks (or govt.)want inflation badly – to write off debt, but need the masses to believe the opposite (or I am crazy). The ruling class are mostly invested in Asia and could care less what happens back home about jobs and fiscal cliffs etc. But as QE will continue,and € and $ will devalue together, commodity inflation will have to be politically suppressed as long as possible. Huge selloffs of gold and silver could also used to create an entry point for long term institutional buying into next year and beyond. I do hope this is the turning point for precious metals because that’s where I am.

The massive manipulation is a fact we must live with. The most notable chart I saw reviewing this week-end was long term treasuries. They are at the top of their long term bull mkt trend channel. But they are on the verge of breaking down. Long term rates could go up 2% or bonds could drop 20 points even within the context of a continuing bull mkt. That could be interpreted very negatively for stocks, commodities, real estate, and the economy, not to mention the Fed is losing control. It could of course be a positive due to strong growth. I think Reinhart and Rogoff have it right, The 2008 credit crisis broke the financial markets and strong growth will not be seen for years.

Agreed on the 2008 crisis meaning strong growth is still a while away. Output gaps still remain in most world economies after 2008. However, I am curious as to the fact that US unemployment has been falling, but the annual quarterly GDP figures have been no higher than 2-2.2%, which is below what most presume is the US economy’s trend growth rate, necessary to avoid unemployment rising.

I suspect the numbers on GDP for 2009 to 2012 will be revised up in the coming years, to account for the fairly decent fall in unemployment. I also belief UK GDP is underestimated, which makes sense as some say data compilation in the UK is apparently worse than China. However, for the UK, I’d say, based on the unemployment rate being fairly stagnant at about 7.7-8.4% in the past 3yrs, GDP has probably been growing at just about the required level of 2% or so, to ensure joblessness hasn’t risen substantially.

UK unemployment has been falling fairly decently since 2011 though, so I assume that growth has ticked up since the start of 2012, with the double dip recession being complete fiction. At worst, the UK economy stagnated for a few quarters and is now on an upward trend.

The massive manipulation is a fact we must live with. The most notable chart I saw reviewing this week-end was long term treasuries. They are at the top of their long term bull mkt trend channel. But they are on the verge of breaking down. Long term rates could go up 2% or bonds could drop 20 points even within the context of a continuing bull mkt. That could be interpreted very negatively for stocks, commodities, real estate, and the economy, not to mention the Fed is losing control. It could of course be a positive due to strong growth. I think Reinhart and Rogoff have it right, The 2008 credit crisis broke the financial markets and strong growth will not be seen for years.

Thanks for your thoughts guys