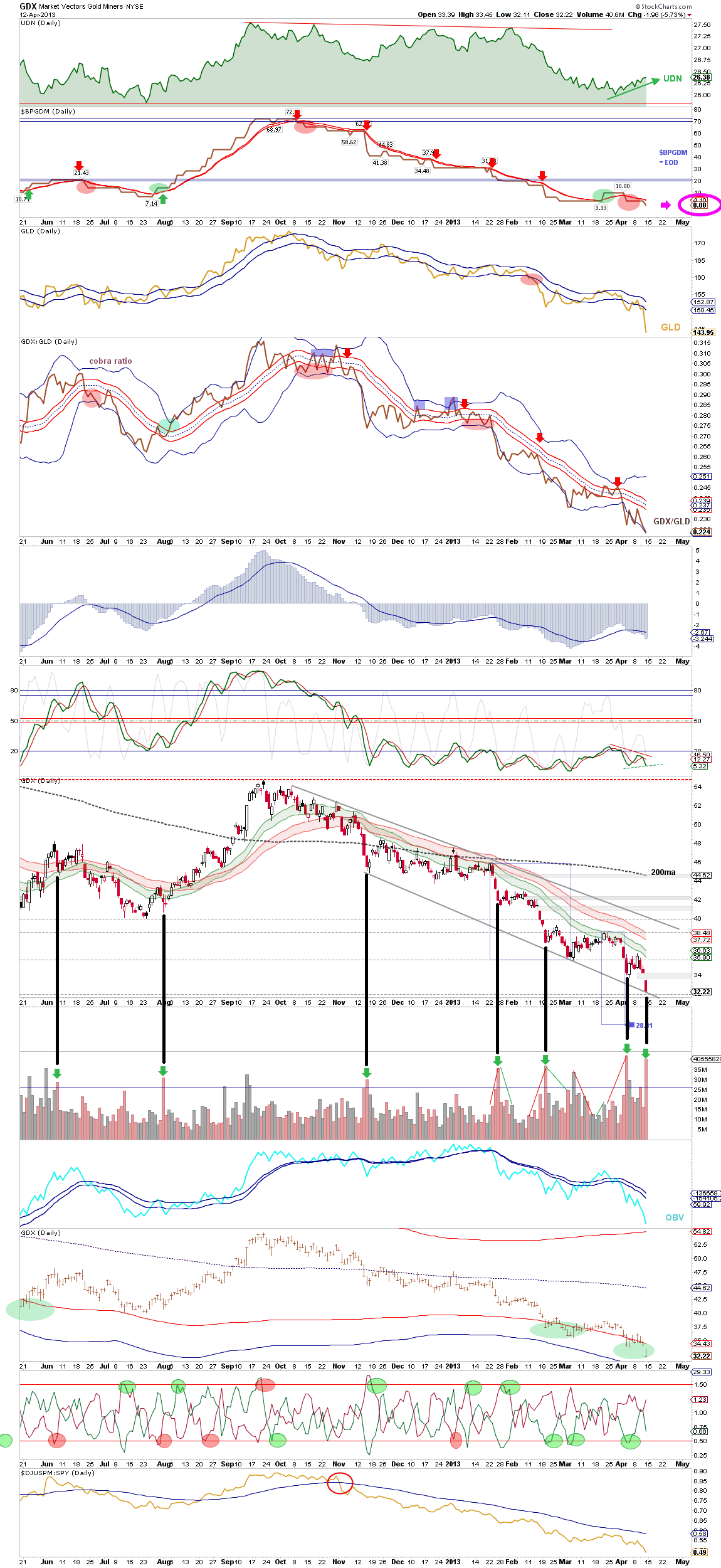

I wrote last year about secular equities bear market progression in this post (click to view). I suggested that a pentagon was a typical formation based on history, and that based on pattern repetition what should occur next was an upwards breakout, followed by a retrace to the nose level, then secular bull momentum after that.

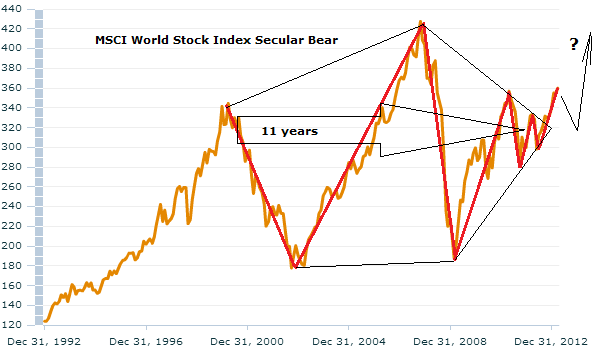

This is how the MSCI World Stock Index now looks:

Underlying Source: MSCI

Underlying Source: MSCI

A breakout has occurred. This pentagon shape and breakout can be found on the same timeframe for FTSE, Dax, SP500, Dow, Hang Seng and other indices. The action represented by the black arrow is what I suggested could happen next, with the momentum go point potentially coming in 2014/2015. This idea was based around my primary scenario of commodities making a secular top ahead in 2013/2014, helping to tip the world into a mild recession with stocks falling into a mild bear accordingly, before they charge – rather than the alternative that commodities peaked in 2011 and secular stocks bull momentum is already underway.

Here are the SP500 and Dow technical shapes during the last two secular bears:

In addition to the pentagon formation, I have highlighted on these charts and the top MSCI world chart above what is in effect a large W formation followed by a small W formation (in red). OK, we are operating on a fairly meagre sampling from history here, due to many country stock indices only having recent history, so perhaps don’t read too much into either of the formations that I am picking out. However, the message from both the pentagon and the WW formation would be that secular bears typically end with a coiling, a narrowing of volatility, and based on that we might not expect another major cyclical bear market ahead.

In addition to the pentagon formation, I have highlighted on these charts and the top MSCI world chart above what is in effect a large W formation followed by a small W formation (in red). OK, we are operating on a fairly meagre sampling from history here, due to many country stock indices only having recent history, so perhaps don’t read too much into either of the formations that I am picking out. However, the message from both the pentagon and the WW formation would be that secular bears typically end with a coiling, a narrowing of volatility, and based on that we might not expect another major cyclical bear market ahead.

However, these charts are nominal. The inflation adjusted picture is very much a down-sloping pentagon, rather than the relatively benign-looking sideways range that the above charts show. The true secular bear progression can also be revealed through a gradual wash out in the stocks to gold ratio, and a similar gradual demolition in the price/earnings ratio in equities. In the last secular bear, US stocks began with a p/e of 24.1 and ended on a p/e of 6.6, shown here:

Source: Zealllc

Source: Zealllc

Also note the bottoming p/e of the 1940s secular bear reached around 9. What I have tried to highlight with boxes on the above chart is that both the last secular bears ended with overall sideways action whilst p/es fell significantly to reach their secular low. This was because they both ended with an inflationary peak (circa 1947, 1980). High inflation will pull down the p/e ratio as stocks trade sideways, because they are cheapening in real terms.

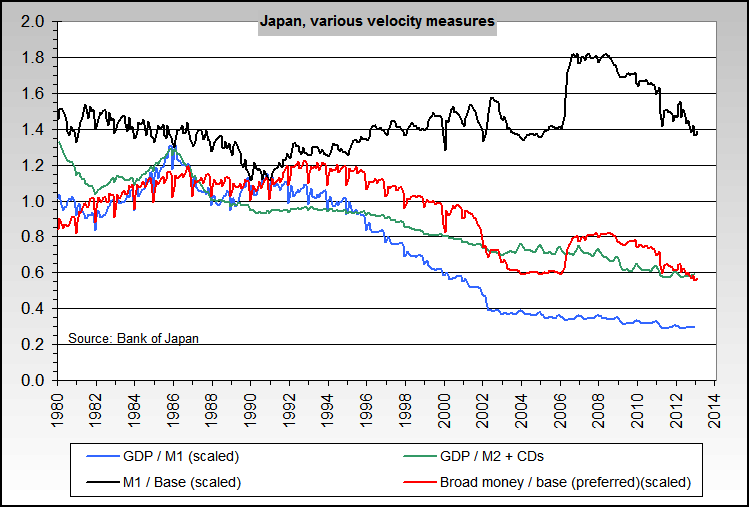

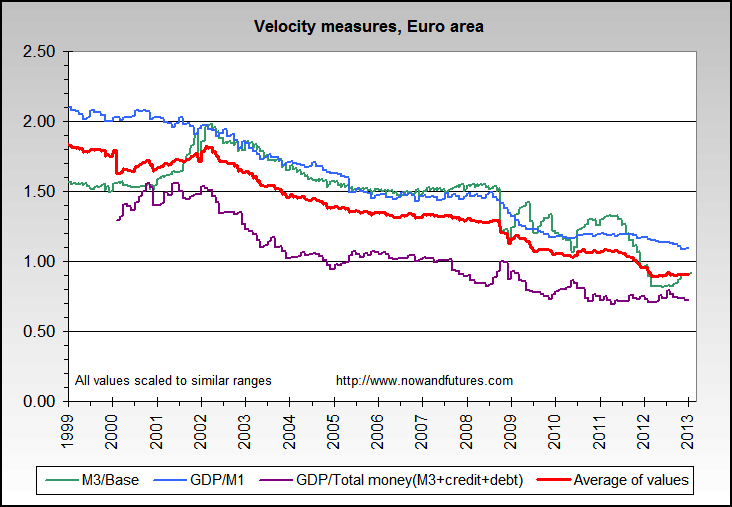

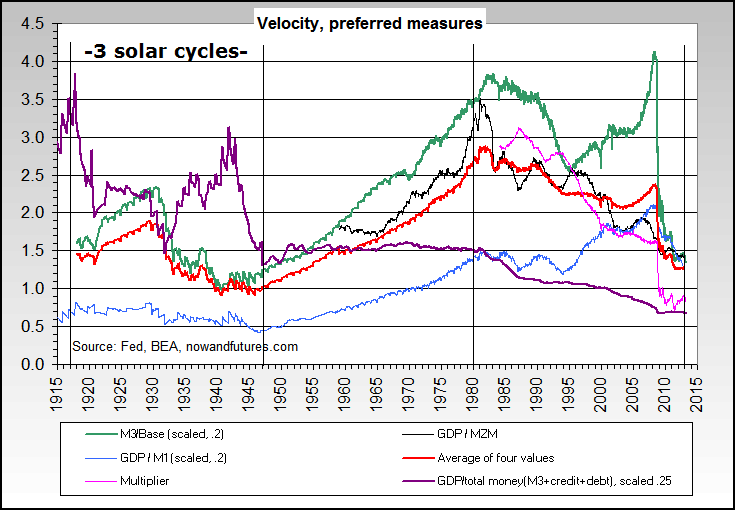

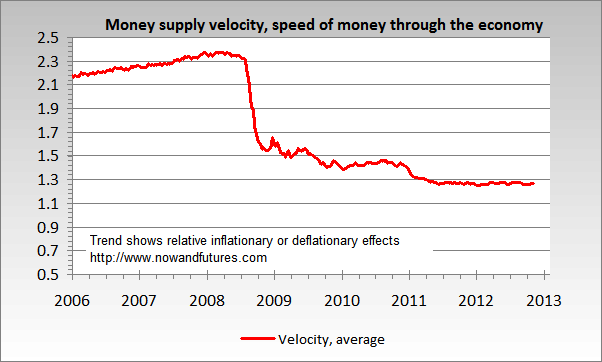

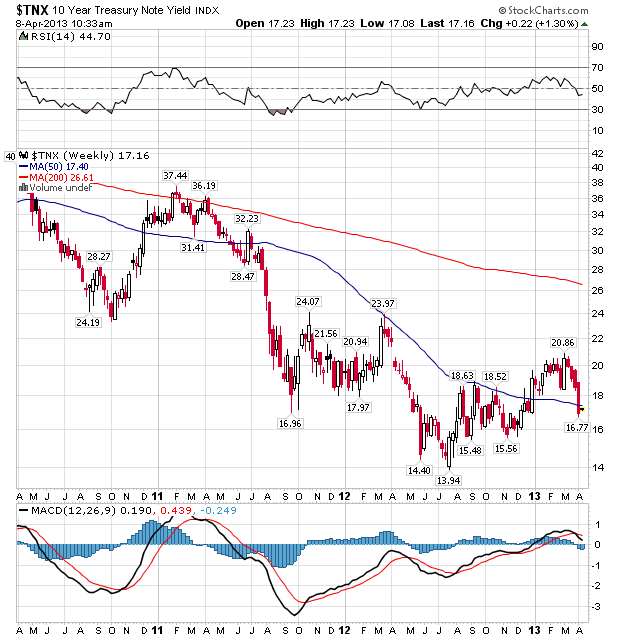

So, in our current times, if stocks are to end with a similar final washout in p/es before new secular bull momentum, then there are two ways to achieve it. The first would be in line with history and this would be a period of peak inflation, where p/es shrink as stocks trade overall sideways. The second would be an absence of inflation (commodity slack and low money velocity continue), whereby stocks fall hard in nominal terms to achieve the p/e washout. This second scenario perhaps has a rhyme with Japan’s secular bear from 1989, which made a series of lower lows as it progressed, in the clutches of deflation. So, like I posed yesterday, is the US the new Japan, or is inflation still dominating and peak inflation a likely possibility? I suggest the shaping of the secular bear to date (we are currently at all time highs despite being in a secular bear) and the undoctored picture of inflation reveal that inflation is in play in the US, rather than deflation.

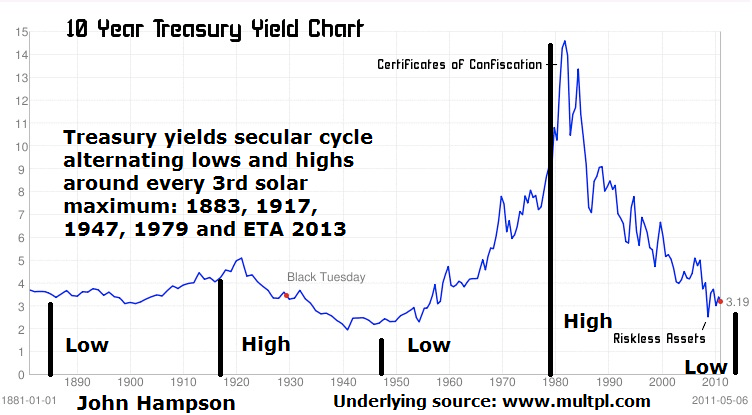

I don’t subcribe to a hyperinflationary outcome, but I think a pick up in yields and in money velocity and an inflationary feedback looping with stocks moving overall sideways is more likely than a deflationary end to the secular bear, whereby stocks fall hard to reach a washout in p/es. But have stocks already washed out enough by p/e?

I believe there is a reason why US stocks bottomed at a p/e of 9 in the 1940s bear, compared to 6.6 at the bottom of the 1970s bear, and that’s the difference in yields and rates, which were at opposite extremes in the two periods. In the current enviroment, and back in the 1940s, bonds and cash are earning little or even negative returns. Dividends are higher on many stocks than the yields on bonds. The p/e alone then doesn’t tell the whole story, because stocks are relatively more ‘valuable’ if bonds and cash are paying you a guaranteed loss. I suggest therefore that, generally speaking, a bottoming p/e of 9, rather than 6, may be more appropriate for this secular bear.

The Dow, SP500, Dax, FTSE, Singapore Straits and Hang Seng all already reached either p/e of 9 or below in this secular bear, not to mention much lower p/es for the PIIGS. Plus equities in general began this secular bear in 2000 from a much higher p/e (44) than the previous bears began. This begs the question as to whether we are going to see higher secular p/e bottoms and tops now and in the future as stocks capture exponential technological evolution or human progress. This question aside, perhaps we could doubt that US equities have washed out enough when we look at CAPE (at its lowest 12 so far) or the Q ratio (0.6 so far versus 0.3 historically). However, not all stock indices necessarily have to washout to single CAPEs (Japan ended the last secular bear at CAPE 20), and the Q ratio perhaps has a long term trend towards higher values, as shown by the narrowing of its two components over time here:

Source: Dshort

In short, I don’t see a compelling case that equities need to wash out more than they have by valuation in this secular bear so far. Meanwhile, the Dow-gold or SP500-gold ratio has also washed out ‘sufficiently’ in this secular bear, if not to record extremes.

So could secular stock bull momentum already be underway and commodities flipped into a secular bear in 2011? Much of what I wrote in The Alternative Scenario (here) to support this alternative possibility is still valid, with the added developments that gold has since broken down and NASA say perhaps the solar maximum already occurred in February 2012. It will become clearer as developments unfold with time, but until then, perhaps my best case against this having happened would be a lack of pick up in yields or velocity by now.

So these are my current conclusions. I don’t see a massive case to wash out valuations further, but will assume that some last drag-down is ahead because of historical secular bear ending patterns and perhaps CAPE and Q ratio. I don’t see a deflationary case for equities to tumble in nominal terms to achieve this, as the secular bear has proceeded against an inflationary backdrop with stocks currently at all time highs, so any such washout, if it is to occur, I’d expect to be overall sideways against an inflationary backdrop. The environment of low yields and rates is pertinent: it perhaps means stocks do not need to wash out ultra low by valuation, and that bid support would be higher. And there is also the potential that we have a permanent shift higher in Q ratio and p/e bottoms. In summary, I don’t expect a major drawdown in equity prices. but something milder.

So, I want to buy into a significant pullback in stocks with a secular bull view. Ideally something that looks like the pullback to the pentagon nose level. Ideally with a few more countries dropping under p/e 10, and ideally on the back of an escalation in commodities and inflation. Until I can rule out that a secular bull in stocks began already, I will likely adopt the strategy of layering in to any pullbacks that I consider deep ‘enough’, perhaps 10% off or more. However, if stocks were to mount such a pullback, then the action in commodities would likely be telling as to whether they have a peak left ahead, and in turn shed more light on the secular equities position, which which to further navigate.

{kind=link}