Gold, silver and gold miners are at extremes of oversold and overbearish readings, with possible high volume capitulation candles on the last day of last week. Mean reversion should now follow in the form or either a relief rally to work off these conditions or the start of a new upleg, but first we need to see a turnaround and some buying interest.

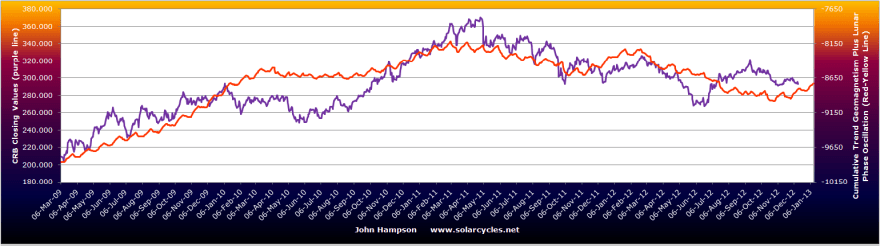

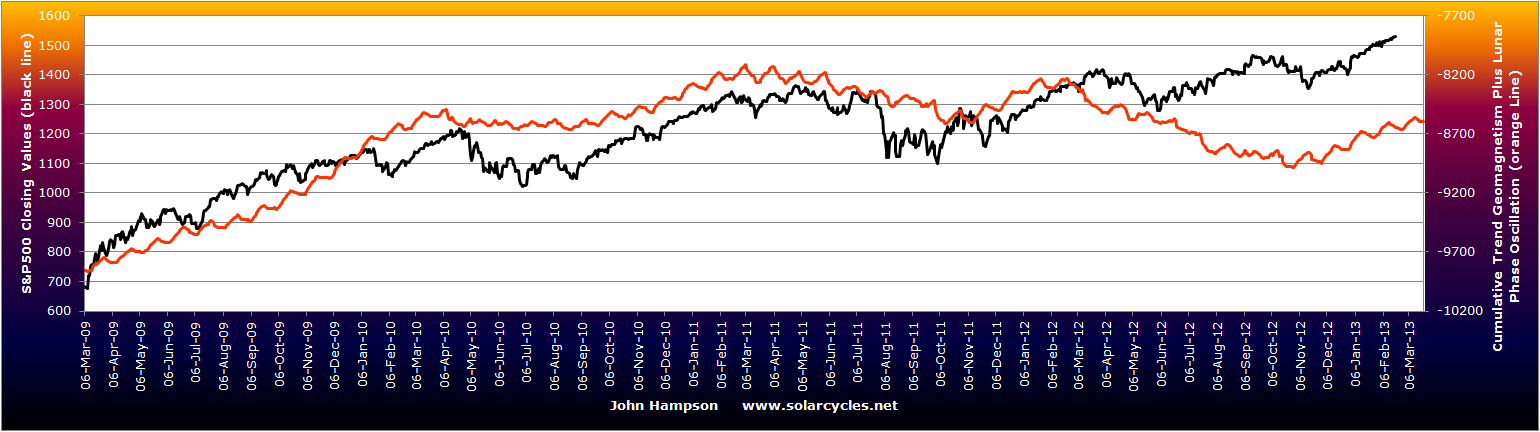

The majority of other stock sectors, aside gold miners, are overly bullish, and warning flags persist in equities, but without any technical break yet. Is the narrowing number of global stock indices making new highs a sign of a gradual top taking place since the end of January, or was that meagre correction only a blip in a continued advance into March? It’s not clear at this point, but here are two reasons why equities could potentially advance into March: cyclicals as a leading indicator and actual/forecast geomagnetism. So far this year actual geomagnetism has been tame and it is forecast to remain so into early March at this point – here is the latest model with the tail three weeks into the future:

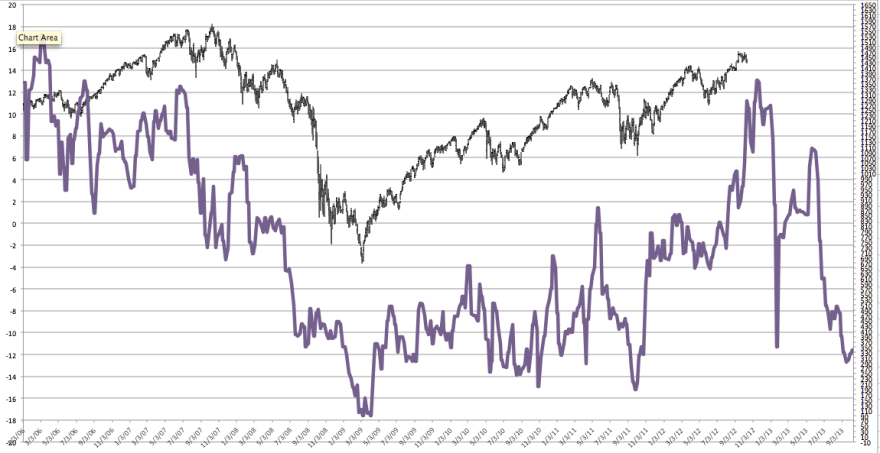

Only in June-September last year did US stocks diverge particularly from the cumulative geomagnetism model and whilst that divergence gap has not been repaired, the market direction has since been following the model direction again.

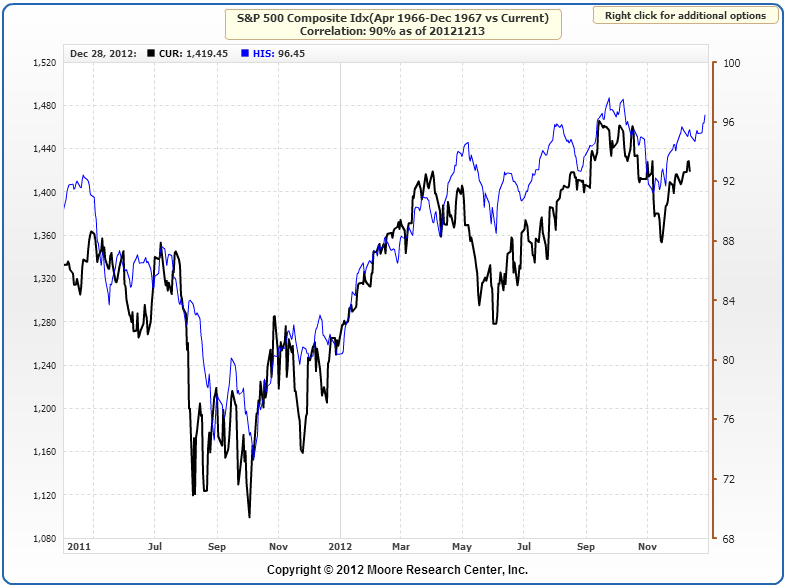

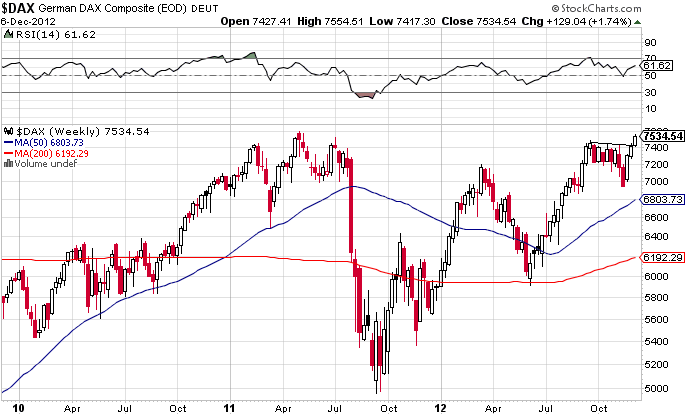

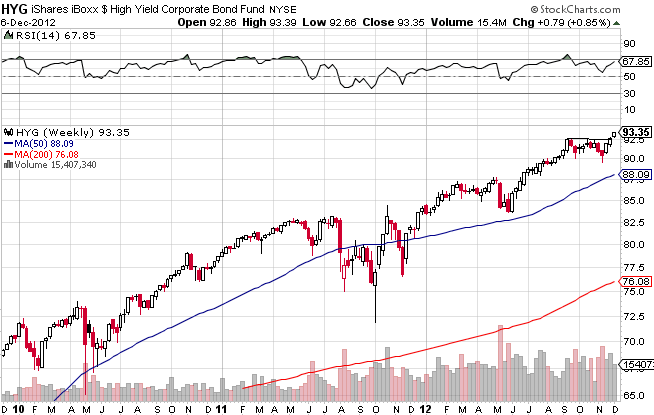

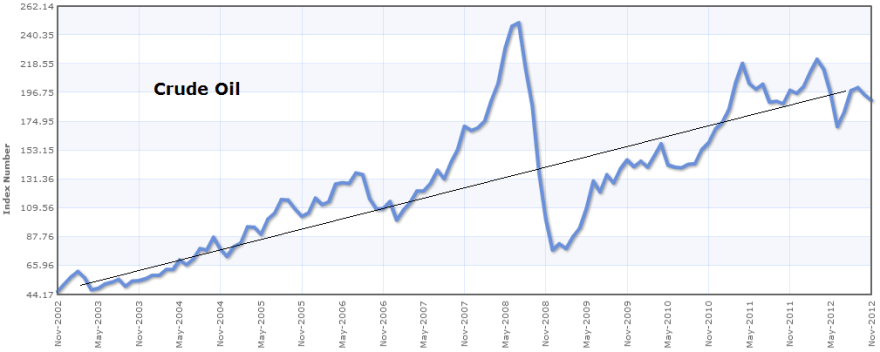

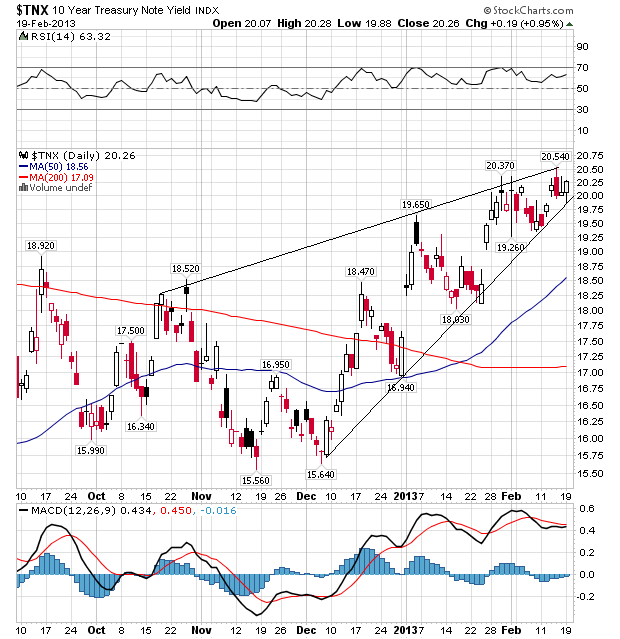

If equities are instead in a correction that began in late January, with a couple of laggards about to turn and join (e.g. US indices), then I can refer you back to five models in alignment, and would also point to the current narrowing wedge in treasury yields which could suggest a switch to safety and away from pro-risk is coming, if yields break down:

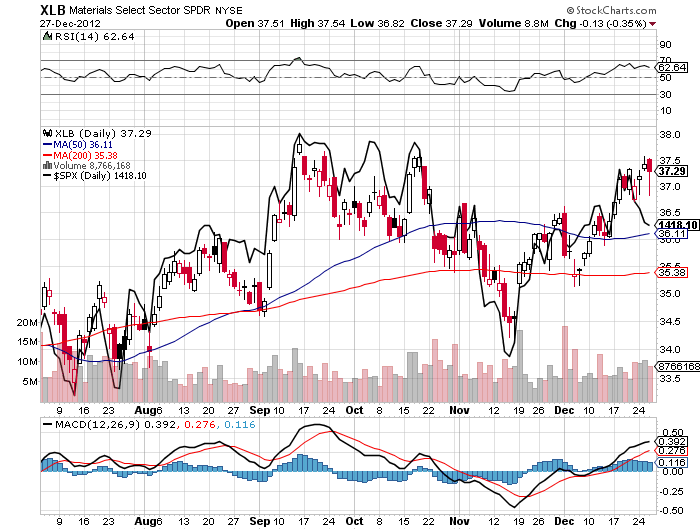

Source: Stockcharts

Source: Stockcharts

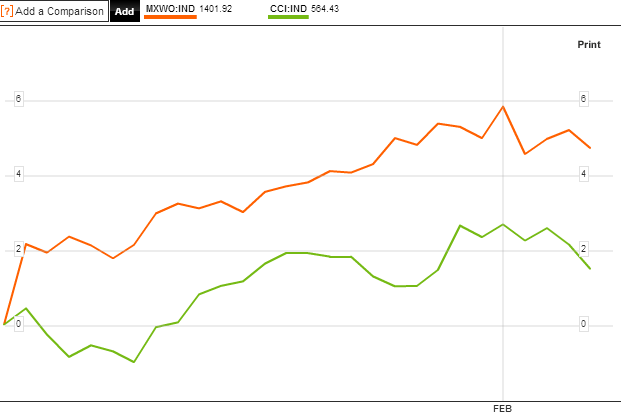

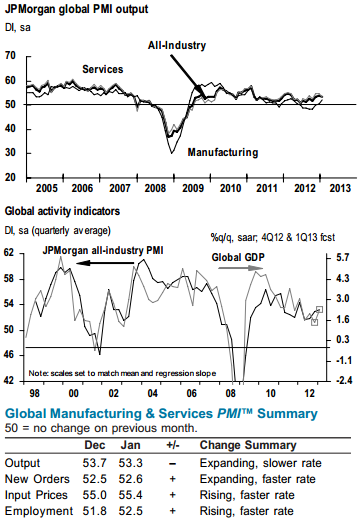

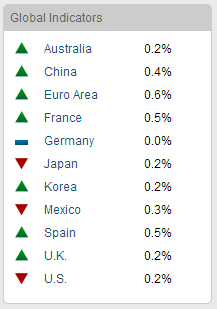

The latest leading indicator releases from CB came in flat for Korea, +1.0 for Spain (improvement on last month) and -0.1 for Australia (also). Commercial loan data for China showed quite a jump in January. US earnings beat rate for this quarter came in at an impressive 64% beat rate both in earnings and revenues. Citigroup economic surprises have turned up again in the US:

All in all, a continued positive environment persists for pro-risk assets and any pullback at this point should be as a result of excessive bullishness rather than a deterioration in the macro picture – at least until that changes.

I have no further evidence at this point to validate or invalidate the primary scenario (secular commodities peak and solar peak ahead) or the alternative scenario (secular commodities peak and solar peak in the past), but I expect we will see decisive evidence one way or the other within the next couple of months.

I am leaving Australia on Saturday and coming to Auckland NZ for 3 nights, before motorhoming around the rest of the North Island for 10 days.