There has been some consolidation in pro-risk over the last few sessions, which is normal into today’s full moon. The correction overall has been minor, and the next two week period into the new moon is one of low-forecast geomagnetism. I believe therefore that subject to some last minute resolution or postponement of the fiscal cliff issue, pro-risk can now rally again. But how near are we to a cyclical bull market top in equities? In the last few weeks we have seen technical breakouts in the FTSE, Dax and Nikkei, to add to the recent Hang Seng breakout. Plus we have seen a compelling bottoming formation in the Shanghai Composite. None of that looks like a top. If there is a cyclical bull topping process occurring anywhere then the most likely would be the US markets, as they have pulled back from their highs and remain someway beneath, with tech (usually a leader) underperforming. It is possible that US markets could top first, leading the rest, so let’s take a look under the hood of the US markets.

NAAIM sentiment is into the bullish extreme. That’s a caution, but note how we saw a congregation of such extremes in 2007 prior to the peak, i.e. we could be at the start of such a process rather than the sell point.

Source: Sentimentrader

Source: Sentimentrader

Investors Intelligence sentiment remains neutral – bullish, not into the extreme bullish zone. Bullish percent over call/put ratio remains very neutral:

Source: Stockcharts

Source: Stockcharts

There is as yet no negative divergence in breadth as measured by advance-declines, shown below compared to 2007:

Source: Cobra / Stockcharts

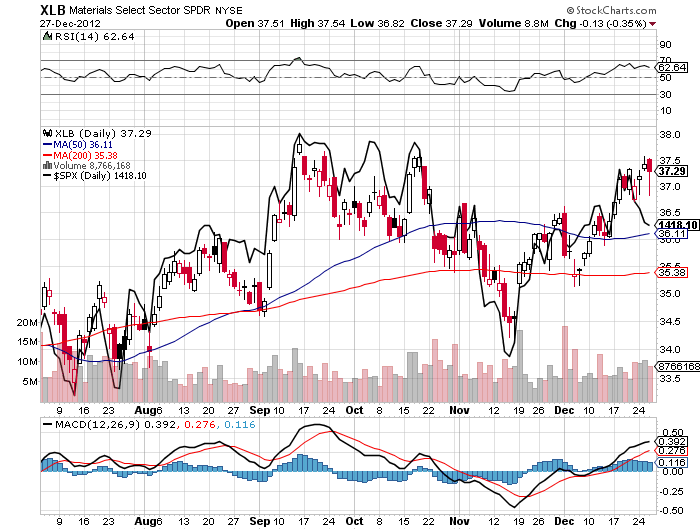

Cyclical sectors continue to perform well overall, with the exception of technology. Below are four cyclical sectors versus the SP500. Note that in 2007, around half a year before the final peak, cyclical sectors started to underperform the index and defensives outperform. This is not what we see, bar tech.

Source: Stockcharts

Economic surprises for the US remain in an uptrend, and ECRI leading indicators are positive and have been ticking up again the last 2 weeks. Global leading indicators remain mixed. Two PMI readings for Japan and Russia disappointed this week, with Russia falling to 5o (the dividing line between growth and contraction) and Japan languishing further negative.

Now take a look at this. Eurodollar COT 1 year in advance as a predictor of US equities, which I’ve referenced before. Whilst it has not been a perfect predictor, it is fairly compelling and points to a clear sharp downturn for equities as of the turn of the year.

Source: Tradetrekker

And to that I will add Norwegian Jan’s chart of the Kitchin cycle, which also shows a significant fall is due.

Source: Jan Benestad

Eurodollar COT and Kitchin cycles are not part of my usual toolkit, so I am unsure how much weighting to give. But it’s a signal for caution at the least. So what might I do? Well, if I draw in other historic signals of a stock market top and forthcoming recession, there’s a less compelling case for a top here. Treasury yields are rising but not significantly yet, inflation is not yet accelerating, leading indicators are mixed but showing weak growth ahead rather than rolling over, and we don’t yet see generally in equities the topping process of a rangebound market with reversals of reversals of reversals lasting several months whilst internals decay. If that process has begun, then I would argue that we don’t yet see anywhere where that process is mature.

On the other hand, the Nikkei has rocketed to overbought levels, whilst the yen is at bearish sentiment extremes, plus the Aussie dollar is at the bullish extreme. Potentially a reversal in these assets could be ahead which could imply a wider move anti-risk, pro-safety. But as yet we do not see such significant sentiment extremes across wider pro-risk or safety that would make this more compelling.

I continue to watch treasuries, which may have topped out, and if so outflows should find a home pro-risk. Flows into equities remain negative, as opposed to frothy, as shown by the chart below which measures flows into US equity funds. It captures the secular bull / bear cycle well.

Source: Pragcap

Tom DeMark predicts a 50% increase in Chinese shares over the next 9 months. Solar/secular history predicts a blow off top in commodities ahead in 2013/2014 with acceleration beginning now, and this is echoed by Gann. Leading indicators of leading indicators predict improvement in Q1 2013, the lag of central bank actions this year. If equities made a cyclical bull market top here and now, I’d find it hard to square all that. I would rather expect growthflation (particularly with growth in China) brings about a surge into pro-risk and out of treasuries, with equities making an overthrow top first before commodities make their parabolic secular finale.

Back to the near term, I continue to expect some kind of satisfaction to the fiscal cliff, even if just postponement, will bring about a rally. But there are no guarantees. A failure could sink equities, as we saw in the steep cliff-nerve related put of hours falls of last week. The meeting is set for Sunday, which means one of the two scenarios on Monday.

I’m now in Central Thailand for a week near Phitsanulok. I shall mull all this over and assess whether I want to act today in any way. Any input or thoughts from you guys of course welcome.

BTW. Gold and silver and gold miners remain on extreme low sentiment readings. As previously stated, I would be a buyer here were I not satisfied with my exposure. So I believe the stage is set for this sector to propel higher in due course.

My point of view is that the Industrials is in the same place that in dec08, so my scenario is a drop about -15% until feb-march13. Regards.

Hi John et al

I believe that equities are most likely at the start of a rolling over process.

But because the FC has denied a rally which would normally have created a clean out of bears , even if there is some sort of wobble over the next week or so I wouldn’t be surprised if a rally then takes place which would be the continuation of the “normal” topping process.

Re PM’s I still don’t see any evidence that they are ready to trade significantly higher. As I wrote on my blog a while back this phase is a relative negative phase for PM’s which continues until week 28 of this year. The current phase started at the beginning of 2012 at 1612 in Gold so price will be drawn to that level or lower over the next few months.

Any fall in the Gold price will obviously mean that, valued in gold, equities become more expensive. So,even though there is room for a relief rally if FC negotiations are resolved in the short term, any substantial rally in equities should be sold.

I´m sorry, I meant dec07!!, not dec08

In the end of 2007, the word was perfect, no indicators said the collapse we were going ahead. This time everything is in calm, quiet, the 3rd QE and the plus recent one shows the perfect way to push the markets to the historical tops in the US.

A big amount of liquidity in the system to avoid another collapse and a ridiculous 2% for the GDP in US, or less? for 2012.

The Us index could push to the tops in the mid-end of the year if the FED and the politicians wants to, but the cycle of the Industrials as the historic -standard structure says is demanding a big drop, a retracement abot 0,618 from 2009 to 2012 in 3 yeras after a decline obot 50% in the 9th year and after a 2-3 yeras un more than 100% revaluation.

It´s time to.

Sorry, John to disagree with your meritorious study.

I bet this year is bearish for Commodities, including, Oil, Gold, Silver, Copper, bonds, assets and bullish in USD, and of course in the parity EURUSD we go to the 1.1-1.0 in 2014-2015.

hey john

love your work. i am not in your league but since you are a long way from home i am injecting my 2 cents worth… i mostly do cycle analysis including the sun which suggest that the dj30 average will peak around july 2013,,, some other averages peak starting in april… the sunspots will have a secondary peak mid year but the main peak occurred in the fall of 2011…. i only follow commodities as the affect stocks and this data suggest copper is done for at least a couple of years… i am not an elliott wave guy but i do follow 2 good analyst to make sure my cycle projections are not outlandish… pugsma and caldaro at wordpress.com do good work and are in harmony with my cycles for the time being…. from a fundamental pattern approach, i think caldaro’s bearish pattern looks better and it suggest we topped… i intend to stay with my cycles until caldaro confirms the bearish pattern… government actions do distort stock cycles for short times but not those from the sun… right now stock and sun cycles are in harmony and suggest weakness til mid janurary 2013..

Hi and thanks

I agree with John and Norwegian Jan i.e. rally until summer when sunspots are to be topping and we have some nice astro stuff happening but buying out of the money puts for protection for Monday as I always do. However I actually disagree that the fiscal cliff has any impact on stocks or financial assets whatsoever. The fiscal cliff has been discussed all over the world in media and in TV for about 6 months now. What has really changed or will change?

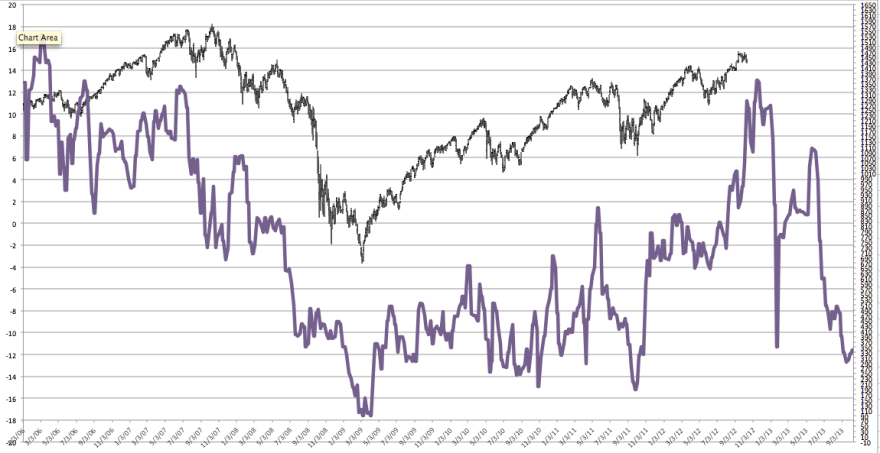

Thank you all for your thoughts. I took no action yesterday – the internet here died shortly after I’d made this post. Did you see Chris Puplava’s cyclicals v SP500 chart? Suggests equities rally into Feb/Mar then keel over:

ECRI leading indicators also ticked up again:

While the VIX has “gone through the roof”, we haven’t seen this occur in other volatility indices such as gold, silver, or EM. Higher beta, EM markets are doing very well relative to the SPX. ETFs like EWY, EWH, FXI continue to perform very well. My initial thoughts are: we get a deal and a massive volatility suck in SPX and equities are going to make new highs into Q1 with EM outperforming the SPY.

However, the flip side says:

1. The VXV – VIX ratio broke under 0 for the first time this year. Historically when this happens, accelerated downside in equities tends to occur (the rush for protection, bearish bets).

2. Volatility in some assets are unbelievably low relative to the SPX and in some cases on a historical basis, specifically currencies like USD/CAD and AUD/USD. Now, just cause vol rises doesn’t equate to lower prices however a breakout to some degree should be expected.

Most bears feel good about what we are seeing. Maybe we finally break the bears back with a big move higher in equities only to put in the top for a long time.

Just my two cents. Enjoy your travels John.

Thanks Ryknow

John, is possible that the sunspots already peaked? If you look at the radio flux progression for the solar cycle, it may have topped in Nov 2012. Predicted values predict an uptick but still lower than Nov 2012. If we don’t surpass Nov 2012 in radio flux solar cycle, does that suggest a top for US equity shortly after Nov 2012 according to your work?

Hi Peter

You are the second person in a day to suggest that sunspots have peaked.

I am starting to get worried.

Hi guys. Nasa, Sidc, and Jan’s work too, all still predict the solar top in 2013, so I’d be surprised if they were all wrong. I see the spike you refer to, but that’s part of the up-down oscillations. The solar peak is a smoothed sunspot peak. See here for the last peak:

Note how the solar peak is not the highest spike – it is the aggregated smoothed top.

Thanks for your comment John. I appreciate your work and timing wise agree with the March date per Chris Puplava’s chart you mentioned earlier for a possible peak as multiple dates align in March or September of 2013. Such is the nature of tops. Solar sunspot projections say the solar maximum should arrive in autumn of 2013 per NASA and be the smallest sunspot cycle since 1906. The current predicted and observed size makes this the smallest sunspot cycle since Cycle 14 which had a maximum of 64.2 in February of 1906. If we use Gann logic and go back and look at what happened in the stock market in 1906 because it is the closest year with the most similar small amplitude sunspot cycle, we get:

3rd Worst Stock Market Crash (1906 – 1907):

This crash was called the “Panic of 1907.” The U.S. Treasury department bought 36 million dollars worth of government bonds to offset the decline

Date Started: 1/19/1906

Date Ended: 11/15/1907

Total Days: 665

Starting DJIA: 75.45

Ending DJIA: 38.83

Total Loss: -48.5%

Article Source: http://EzineArticles.com/127590

Now to add to this, 4.5 years earlier we had:

6th Worst Stock Market Crash (1901 – 1903):

This is the oldest crash to make the list (DJIA records are not available before 1900).

Date Started: 6/17/1901

Date Ended: 11/9/1903

Total Days: 875

Starting DJIA: 57.33

Ending DJIA: 30.88

Total Loss: -46.1%

If 1901-1903 is an analog for 2007 to 2009, then similar timing for the next peak leading to a great crash would be Sept 7, 2013 if it were to follow the market reaction pattern in price and time of the previous sunspot amplitude in 1906.

Thanks for that peterslane

I would like to give my two cents by saying that when the Treasuries bull market comes to the end (if it hasn’t finished already), I think people will prefer to put their money into equities. If there is a lack of QE in 2013, combined with market panics, Gold will probably suffer the most. Gold has had a good run, since its 1999 low, but let’s be honest, all bull markets conclude at some point. Maybe now is the time to re

The Fed is targeting 6.5% unemployment, which, when reached, will market the green light for a tightening of monetary policy, assuming GDP is growing rapidly. If US unemployment does improve throughout the whole year, it’ll become more unlikely for the Fed to launch new QE. US equities may rise to new highs in 2013, before forming some kind of peak, as the economy slows down due to taxes rises as the US starts to enact its own austerity plans. Austerity is deflationary in the long term, so Gold and Oil will probably end the year lower, Oil’s price lowered due to a rise in fracking and shale gas extraction.

In the UK, GDP growth is likely to return in 2013 and be sustained. UK equities may end 2013 after having made healthy gains, and inflation will probably be 3-3.5%

In 2013 Mark Carney is set to become the new head of the BoE and he advocates a nominal GDP growth target as opposed to an inflation target, so my guess is that the BoE will support the austerity plan by allowing higher inflation to erode debts away from 2013 onwards. In other words, expect inflation to rise substantially before expecting the BoE to raise interest rates in the future. A bit of inflating debt is very helpful, but too much of it would lead to a new recession.

China is almost certainly going to accelerate in 2013, India will also accelerate in 2013, whilst Brazil and Russia might grow at a slower rate, given they have various problems related to poor infrastructure and trade links to slow-growing European countries. European economies will probably stagnate in 2013 and the recession in some countries may come to an end, whilst European equities may stay stable or shift slightly lower. I’d like to think no countries leave the Euro, and that Greece’s economy stops shrinking. I can’t wait to see if any of my two cents I’ve given come true by this time next year. I hope you all make the right calls in investing for the year to come, have a prosperous 2013 everybody!

Thanks for your projections Pete, and same to you

RE sunspots see

http://www.cxoadvisory.com/3942/calendar-effects/sunspot-cycle-and-stock-returns/