I hope you all made money in 2012 and I wish you a very profitable 2013. I made a 17% return in 2012, versus a personal target of 40%, and compared to the world’s 300 most important hedge funds, my return is likely to rank in the top 30 (source HSBC – final week’s report not yet in). For comparison, I made a 40% return in 2009 but made only the top 50 in hedge fund ranking that year due to the bumper returns on offer from a trend year. I made my lowest return of 15% in 2011, but conversely that made the top 15, as it was a more difficult year in the markets. So for me, it’s important to measure both ways, and in doing so, I can declare 2012 a satisfactory year but not amazing.

40% is a stretch goal each year, but I shall be gunning for it again in 2013. If commodities accelerate towards their secular peak, as per my forecast, then it is very much achievable, based on my existing positioning. Yet, it was commodities that provided the drag on 2012’s returns, as they ended the year essentially flat:

I carried forward commodities long positions from 2011 (maintaining secular positioning), added to them on the sell-off into May, and have since held. The net result is little return from this asset class this last year. It is equities that have provided the larger part of my profits. I entered 2012 with long stock indices positions, and sold out of the remainder by late Jan / early Feb of 2012, before I switched from Amalgamator to Solarcycles. Here is one of the final charts from Amalgamator showing this:

I then bought back into equities in May 2012 on the oversold/overbearish selling exhaustion, and have largely sat on those positions since. I made additional purchases at the start of November with a longer term view (e.g. China at its cheapest p/e to date, Japan at ultra low p/b (since up 18%), Russia at ultra low p/e). I advised of all my trades on my site at the time of their action, and this can all be verified using the search functionality should you be new to the site.

I then bought back into equities in May 2012 on the oversold/overbearish selling exhaustion, and have largely sat on those positions since. I made additional purchases at the start of November with a longer term view (e.g. China at its cheapest p/e to date, Japan at ultra low p/b (since up 18%), Russia at ultra low p/e). I advised of all my trades on my site at the time of their action, and this can all be verified using the search functionality should you be new to the site.

I also added short treasuries in that May sell-off window. This is a smaller position compared to commodity and equity exposure, and has ended the year effectively flat like commodities. I have participated little in the currency markets this last year, and overall there have been no positions in any class that I have had to abandon and take a loss on. The bulk of my trades are open positions that are in profit.

My trading style is to attempt to call the global macro position for assets correctly, namely are we in secular bull or bear markets and are we in cyclical bull or bear markets, and be positioned accordingly. Within that I attempt to call turns, and buy on oversold/overbearish indicators, sell on overbought/overbullish indicators. Throughout 2012 I have deemed us to be in a secular commodities bull market and a cyclical equities bull market, as well as suggesting that we reached a secular treasury bond turn mid-year (from secular bull to secular bear). As we turn into 2013, we cannot definitively state that all those are true, but none of them have been proven false. I think they look good, and my profit snapshot is supportive of this. I have been looking for evidence of a cyclical equities top in H2 2012, but that evidence has been lacking, and so I enter 2013 with my stocks longs still in tact and will again be looking for that evidence coming to light in H1 2013. In short, I believe I have mainly called the strategic asset positioning correctly, but the biggest surprise of this last year, in my opinion, was the flat performance of commodities, as I was expecting their secular finale acceleration to begin and be a theme of the year.

One key factor in that commodities under-performance was economic weakness in China, which is the biggest consumer of commodities. As we move into 2013, China is strengthening, which – if this can be maintained – should provide a trigger for the commodities acceleration. Here is the latest China PMI reading:

Otherwise, global leading indicators and economic data are mixed, so the overall picture remains tentative and to be watched, one development at a time. Nonetheless, my forecasts for 2013 remain largely as predicted in my series of Forecast 2013 posts in September. If you are new to the site or wish to be reminded, go here and then click ‘Next Post’ five times to view the whole series in five parts:

https://solarcycles.net/2012/09/19/forecast-2013-part-1-inflationary-peak/

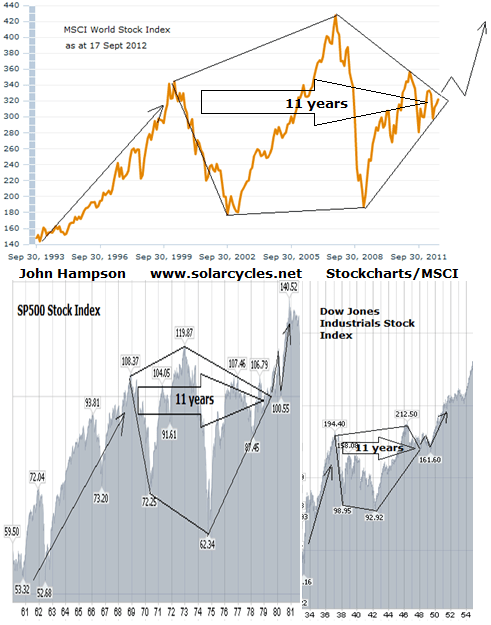

In a nutshell, I forecast an inflationary peak, a secular commodities peak (which could stretch into the beginning 2014), a new secular bonds bear market, and a winding out of a secular equities bear market. The shaping of this secular bear conclusion I suggested would look like this:

…And as we begin 2013 that MSCI World chart line is now peaking out of the top of the pentagon (we have seen such breakouts in the Hang Seng, FTSE, Nikkei and others). So I maintain that equities can rally further away from the secular bear pentagon before making a shallow and final cyclical bear in 2013/14 before new secular bull momentum erupts as of 2014/15. From the Forecast 2013 series, this was my combined forecast for stocks and commodities:

…And as we begin 2013 that MSCI World chart line is now peaking out of the top of the pentagon (we have seen such breakouts in the Hang Seng, FTSE, Nikkei and others). So I maintain that equities can rally further away from the secular bear pentagon before making a shallow and final cyclical bear in 2013/14 before new secular bull momentum erupts as of 2014/15. From the Forecast 2013 series, this was my combined forecast for stocks and commodities:

That is still the shaping that I expect, and therefore commodities ought to begin that out-performance soon. Equities should go on to make some kind of topping range whilst internals deteriorate and give clues to a cyclical top.

Returning for a moment to 2009, we stepped back from financial system meltdown and acknowledged ultra cheap assets, to deliver a very bullish year for pro-risk that a lot of participants ‘got’. In 2010, there was a mid-year retreat that had the hallmarks of a correction within an ongoing bull market, which most of those who I read ‘got’, for another year of bull returns. In 2011 however, action was more volatile and developments more confused, and I found the analysts that I read and respected at the time much more divided, with some getting it right and some getting it wrong. 2012 was similar to this. It was difficult to take the stance that ECRI were wrong in their recession call (but this now appears to be so), that H1 2012 concerns of a European sovereign default would not come true, and that, amongst others, Tiho’s detailed reasoning for a global recession and stocks bear since mid-year was not the accurate picture – at least not yet. It has been a year of fluctuating and short-lived developments and I maintain this more confusing action of the last 2 years is because we are in a gradual transition period from secular bear to secular bull in equities and from secular bull to secular bear in commodities and bonds. Wouldn’t we be glad of a trend year like 2008 (all down) or 2009 (all up), right? Well, I have some hope that this year will be a trend year for commodities: their final secular acceleration – so let’s see.

As I have previously detailed, my view is that March 2009 was the secular equities bear nominal low, and that since then we have been in a period of gradual repair. From financial system meltdown to sovereign default fears (that’s improvement), then from sovereign default fears to no natural growth (the European debt fear that was headline news in H1 2012 was very much wound down in H2 2012). I suggest that this year global growth will pick up and we will finally see the ‘growthflation’ that central banks have been keen to generate. Tightening (yields rising) and over- exuberance in commodity prices will then usher in the last equities cyclical bear before new secular bull market momentum. Of course problems and fears will still abound – the secular bull market will be built on a wall of worry – but they will gradually decrease with time.

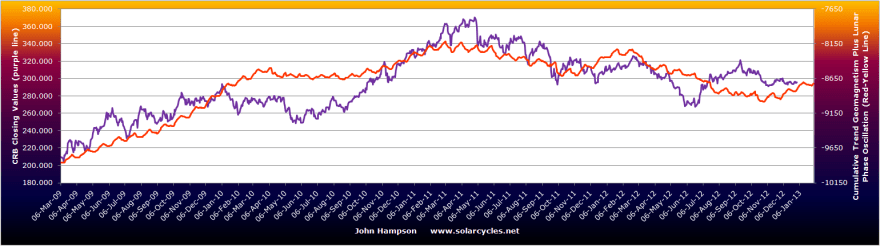

My geomagnetic models did not overall perform as well in 2012 as 2011, however commodities still follow the geomagnetic model very well:

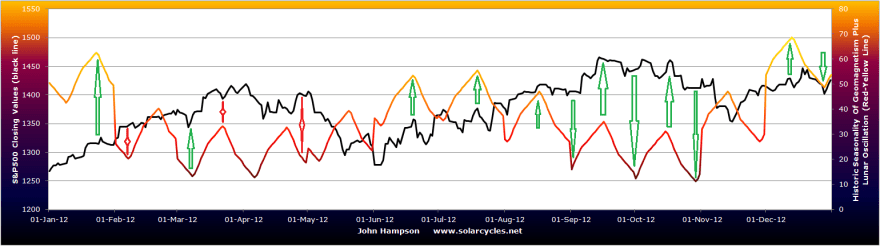

And using lunar phasing continued to provide an edge in 2012, with the SP500 ‘hits’ shown here in green, as well as some lunar inversions in red:

I believe the most important model in 2013 will be the sunspots model, which should see solar activity reach a peak in H2 2013, biologically inspiring speculative behaviour and excitement in humans (potentially also through war and protest behaviours).

So here’s to an exciting year. Thanks for all your comments and mails and links in 2012, I value your input. And to the silent majority: don’t be shy in coming forward with a question or a view or a great find. Keep spreading the word guys – it’s the year of the Solar. Happy New Year to you all.

John, Happy New Year! I am most bullish on “CAF”, a (profitable) position we both are holding. You know, when so many pundits continue to call for a China Hard landing when it had already crashed into pieces (……measured by $SSEC which dropped roughly 2/3 since 2007), my contrarian instinct says Buy It and hold!

I hope Tom DeMark is right that it will rise 50% in the next 9 months. Do you have a particular China strategy to share with us?

Your patience to sit tight, allowing your profit to grow is awesome..Just brilliant.

In addition to owning CAF, I have added LFC and HAO last week.

China’s 30 years of economic reform since Deng has brought significant progress to China. The recent (18th) People Congress targets the growth of the Middle Class in the next 30 years. I see the current set-back as a buy and hold opportunity while there are fear, lack of conviction and accusation of untrustworthy financial data.

I went to a Christmas function and a business man from Romania told me why the Chinese Government is giving next to zero interest rate loan to Chinese who want to start a business there. In my opinion, this sort of policy allows China to (deliberately) control the World economy in due time. I wonder what the next 30 60 or 90 years will bring.

China is to be bought and accumulated.

Thanks Edwin. I should list all my positions at the start of 2013 (there is ample China play with the commodities plus the CAF):

Long Dax

Long FTSE 100

Long SP500

Long Nasdaq

Long Austria 20

Long Hang Seng

Long Nikkei

Long Singapore Blue Chip

Long JPM Russia ETF

Long Morgan Stanley China ETF

Long Market Vectors Gold Miners ETF

Long Gold

Long Silver

Long Crude Oil

Long Nat Gas

Long Oats

Long Orange Juice

Long NY Cocoa

Long London Cocoa

Long Coffee Arabica

Long Coffee Robusta

Long Wheat

Long Wheat ETF

Long Agriculture ETF

Long Ultrashort treasury bond ETF (i.e short treasuries)

As always excellent post !! You are like a FX Jesus that comes with Salvation to small retailers :)) My dream in this year is also to see a new section in Your blog titled “My Signals” 🙂 It can be donated or paid in small amounts, 1000 ppl x 5,99 is nice cash 🙂 or paid only when You will publish a NEW signal with refference to historical trades / decisions 🙂

Pls think and keep working 🙂

Thanks Greg. Something like that maybe with time.

Happy New Year to one and all, and may the New Year bring us continued success at least equal to 2012. 😉

Same to you High Rev

Well done John

I’ve checked in since the first few weeks of Amalgamator so it’s been interesting to see how things have developed. Obviously, I don’t always agree with you: sometimes to my detriment(I should have gone for it more on June 6);sometimes in my favour (PM’s this year).

Either way I always enjoy your open minded, reasoned approach.

Good health and happiness to you and your family in 2013.

Will

Cheers Will, same to you, and well done on your PMs call.

I still cannot feel a big change in the commodities I trade. Coffee, cocoa, sugar, cotton in volatile sideways to lowering ranges, wheat has broken down from 6 month sideways pattern, nat gas broke today below 3.40 – level that could be a good support in weekly chart, gold in a range that may last another 12 months…nothing right now, nothing soon.

I still cannot feel a big change in the commodities I trade. Coffee, cocoa, sugar, cotton in volatile sideways to lowering ranges, wheat has broken down from 6 month sideways pattern, nat gas broke today below 3.40 – level that could be a good support in weekly chart, gold in a range that may last another 12 months…nothing right now, nothing soon.

I kind of agree. Takes a leap of faith to see commodities surging, so until then it’s just theory. But last year’s laggards have a better chance of being this year’s stars, and both gold and oil went nowhere in 2012, along with a few agri commodities. I would suggest the backdrop is changing in their favour, with China’s economy improving, the dollar declining, and some bearish extreme sentiment in the likes of gold, coffee.

John,

Congratulations! Despite all the naysayers you stuck to your outlook and stocks did indeed go up – at least for the time being as you make clear in your post. Great call.

For 2013 do you favor China/Japan over the USA/Europe as a place to invest?

Jack

Thanks Jack. Leading indicator strength has rotated over particularly to China and Korea, so Asia as a whole should see a pick up in Q1. By p/e Russia and China still stand out as the cheapest (US somewhere in the middle). Japan has risen almost 20% in 2 months and Yen sentiment is extreme bearish, so I wouldn’t be adding there at the moment.

Any ideas on natgas? It seems like the least bullish commodity but if the sunspot theories are correct then together with reversal to the mean could be a nice one. Perhaps a lot of bang for a small buck. I have been accumulating shares in XCO and CHK. Heads I win some. Tailes I win a lot.

I saw great value in natural gas in 2010 as it dipped to around 3.5, which was the long term rising lowest trend line together with historic extreme cheapness versus crude oil. I bought in, added more, and then waited for it to mean-revert, expecting the commodities secular bull finale to lift all commodities. I still expect that, but I am still waiting for my profits as it had a good – and overdue – year in 2012, but it still languishes sub 4. It was a good example of ‘the markets can stay irrational longer than…” – sometimes it can take a long time for a value play to come good. I still think it will do well – even if it gets nowhere near its dizzy heights of 2005 or 2008 – and I still hold patiently. So I agree – but dependent on the commodities finale coming good.

Even if we may suffer for being early, I think reward will come this year. “Many shall be restored that are now fallen and many shall fall that are now in honor.” Graham

A let the mighty reversal work his magic.

First question, Jonh: How long do you trade in open markets? Thanks

Rob, can You send me a link with this research ? or just give some name ?

grzegorz314: His research is here. http://armstrongeconomics.com/ I agree with John that it is hit and miss but he has done a lot of interesting research about financial history and I found it worthwhile reading.

I first tried my luck with a few shares in 2004. I gave it full time focus since 2008.

Is no the same context in a bullish market than in a bearish one; from 2004 to 2007 everything was calm and success, but from 2007 to 2009 is when you have to make hards decisitions.

It was the same from 1998 to 2002-3.

Prior that from 1966 to 1983.

Prior that from 1906-23.

And…the 90-100 years cycle tops like 1929-1835-1720.

I mean, John that a wide prespective is the clue for markets, i see you have it, but you can see that in 2010 you were in the point to miss all the profits of past years, as happens main people in 2007 or in 1998-2000.

I think we are border a Real Cliff. Look at this:

http://advisorperspectives.com/dshort/updates/ISM-Manufacturing.php

The FED is lagging this mini-cycle from march09.

Any ideas on the research Armstrong has done? With a peak in 2015?

I personally have found his dates a bit hit and miss. It doesn’t help that a ‘turn’ date can relate to any particular major market or indeed any major economic event. But I can relate the key dates ahead, provided by email by Jigs:

Top 7 Aug 2013

Bottom 3 Sep 2014

Second: Why do you always show the 60´s 70´s chart of the Sp500 and not the DOW Jones one? The Industrials is te historical chart that support the Historical charting, even before its creation, with UK economy recreations.

Thanks

I have shown both, but I figure the leading US index in 2000 was the Nasdaq, 30 years prior the SP500 and 30 years prior the Dow Industrials.

I´m not agree with you, John, always the boss in the markets is the Dow Jones, the Industrials one, is the World Bell Tower of the Economy from more than 100 past years. The Industrials point the Cycle, until now.

You can see the differences in 1966-83 betw Sp500 and Industrials, and the 1906-23 and so in the past, but always the best reference is the Dow Jones.

If not, you can not evaluate the structure of the markets from the past.

Great post, John. Happy New Year to you and your family. Here’s to 2013 being your most profitable year yet!

Thanks PimaCanyon! Same to you.

Hi John,

It’s been a while since I last posted on here due to taking on a busy, new role in the Middle East. First and foremost, I would like to wish you and your lucky a family a wonderful 2013 and hope it brings you continuing health and prosperity.

My main point is that I think your work and contribution has been outstanding and this site of yours is always at the top of my favourites’ list. The great thing about the web is that there are many different points of view being put across, beliefs being challenged continuously in, both friendly and aggressive approaches, and so the web can be a prickly place at times.

I have followed the sparring between Tiho and yourself (which has been educational, respectful and positive) and admired the both of you for sticking to your action plans and remaining with your trains of thought. There are many other sites out there including Anthony Tuleda’s Change in Trend, yet SolarCycles is the one I come back to time and time again. Your opinions are simple and succinct, your writing even more so and you’re never swayed by popular opinion and media hype.

To that Sir, I salute you. Congratulations to you on your 17% return in 2012 and fingers crossed that you surpass this return in the year that has presented itself. I think I speak for all when I say thank you for providing this site for all of us to continue learning, being entertained and hopefully, increasing our general prosperity.

Best Regards,

Jon

P.S. Long Physical Silver and Gold :-).

Hi Jonathan, i´m glad to see you again here. We are very grateful to John´s work, is meritory.

the differents point of views are positive for all, open minds!

In my case only try to alert that is a danger ahead for long positions this year as the standar cycle of the Dow Jones goes as in the past.

No commnets about Anthony Tudela tricks, very embarassing place, take care.

Regards

Hi Antonio,

I hope you’re well. Like you, I’m nervous about the year ahead and I feel equities will remain strong for the first month or two before leveling off. Corporate earnings, in my opinion, will be under a lot of stress this year and the early signs are there fore all to see. This is evident all over the world. Corporations have no more streamlining to do so growth is now essential. I just don’t know where it’s going to come from though.

The bond markets are a problem but I’m expecting a switch into commodities rather than a switch in to equities as investors look for safe havens and capital growth. Governments are increasing their exposure to Gold all over the world and I so precious metals could offset a turbulent year ahead. I actually tend to think silver will have a very good year after one of relative stagnant performance. Time will tell of course but I continue to purchase physical silver every month as it looks decent value to me.

Time will tell!

Pues hombre, espero que estes bien y mucho suerte este ano! Disculpame porque me teclado es britanico.. no es espanol entonces mi gramatica, obviamente, no es tan bueno! 🙂

Thanks so much Jonathan

Hi John,

Please accept my New Years wishes of Health for You and those you love.

Take care,

Pawel

Thanks Pawel, same to you

John, look at this, US economic suprsie:http://www.cotizalia.com/publicador_analisis_tecnico/fotos/2013010429cesiusd.gif

According to Korey Bauer, December 31st 2012 ans January 2, 2013 were consecutive 90% Up Volume Days..Only happened 6 times in history and 6 month after return = 18.90%.

Buy the dips or this time is different?

https://twitter.com/stockpickexpert