Certain key assets are finely poised as we enter December. The UK FTSE is once again attempting upside breakout from its long term triangle.

The German Dax is also back attacking key resistance. Yesterday it was repelled at this key level. I suggested yesterday it may need a couple of sessions’ consolidation before a breakout – and this is because it has already travelled a fair way since mid November on ‘one leg’.

The Nasdaq (and equally the Dow) is attempting to reclaim its 200MA (the SP500 is clear above). The Nasdaq remains in its neat cyclical bull channel, and stocks in general continue to display good breadth and cyclicals performance that are not suggestive of a top.

That said, a combined failure in the FTSE and Dax at upper resistance and the Nas and dow at their 200MAs would open up the possibility of a renewed leg down, and for the two US indices that would then look more like a major top had occurred.

I maintain a bullish outlook for equities into year end, due to positive seasonality (including Presidential), tame forecast geomagnetism, a lack of common cyclical bull topping indicators in the US indices, and renewed breakout attempts in the FTSE and Dax (typically resistance caves in under repeated attacks, the Hang Seng has already led the way, and by solar/secular history an upwards breakout at this point would be normal). We have a period now into and around the new moon of 13 December which should also be supportive. So let’s see if I am correct and all these indices break upwards.

Let me just list one or two other ‘important’ dates into year end. The Puetz crash window extends into the end of this week. The Mayan global transformation / apocalypse is 21 December, the last major Bradley turn is 22 December. The last full moon of the year is 28 December and the fiscal cliff deadline is the end of December. Out of those five, I am not convinced of the first three, but it does no harm to maintain awareness.

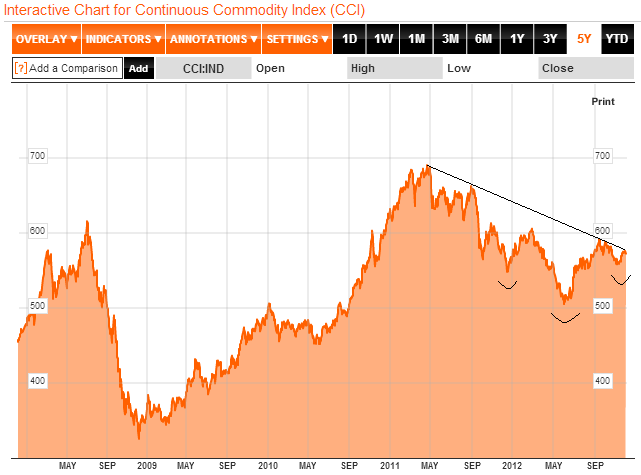

The finely poised position in key assets extends to commodities and Euro-USD. The broad CCI commodities index is at downsloping resistance in a potential bullish head and shoulders formation. Ditto the Euro-USD.

Source: Bloomberg

Combining stocks, commodities and Euro-USD, we have two clear paths forward: one, pro-risk breaks out (the correction in October / November was a correction in an ongoing cyclical bull), and two, pro-risk is repelled here and resumes downward (the rally in the second half of November was a relief rally in a new downtrend). As is usual when the markets are finely poised, some confusing and teasing action could occur this week, with both bulls and bears prematurely claiming victory before true resolution comes to pass.

Besides the reasons above, one other key reason why I favour a bullish year end for pro-risk, is the improvement in global leading indicators. Markit released many individual country PMI reports yesterday, including fresh growth in China (whether looking at official or HSBC data). Below is the combined global picture, and the theme is fairly clear: a distinct up-tick. This is echoed in Conference Board global leading indicators. The general improvement is not in doubt, the question is whether this is just a temporary relief rally in a continued downtrend, or whether leading indicators have bottomed out.

Source: Markit

Source: Markit

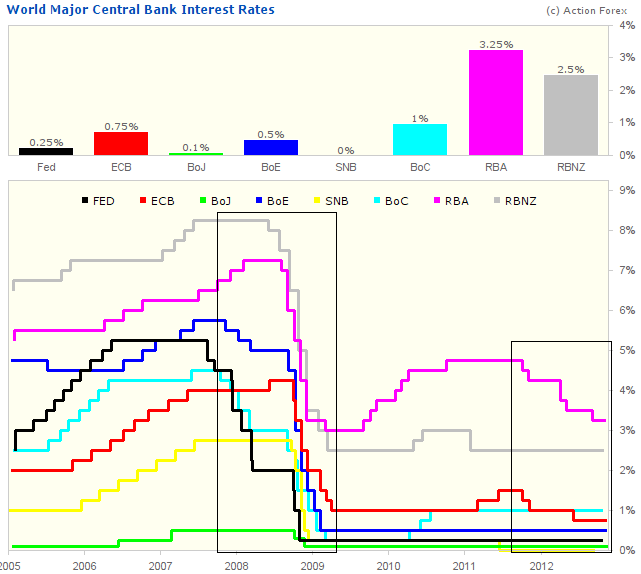

And here we get to the real key issue. By solar cycles, a growthflationary finale should occur into next year’s solar peak. By stock market history, cyclical stocks bulls end with excessive inflation and overtightening of rates. A cyclical stocks bear here and a tipping into global recession at this point into 2013 would mark an anomaly in both those historic indicators. It would be evidence that central bank actions in cutting rates and applying stimulus have been impotent in this cycle, and that too would also mark an anomaly in history, because historically interest rate cuts have had a positive impact on the economy between 9 and 24 months after cutting cycles, and Quantitative Easing has so far been shown to work its impact through in the two years following asset purchases. The two charts below show the renewed easing and stimulating efforts over the last 18 months – not as dramatic as in 2008-9 but nonetheless a fresh round of pro-action and intervention.

Source: Action Forex

Source: Action Forex

If the mechanism is not broken, and such action is not impotent, then we ought to see economic improvement occurring now and into next year. I believe this is the case, as currently global leading indicators are improving, PMIs are improving, and growth in narrow money suggests global industrial output will increase ahead. It is possible that we therefore do see that growthlationary finale next year and we do get normal cyclical stocks bull termination under conditions of excessive frothiness and an upswing in market rates. But one step at at time – first we need to see a couple of months of continued improvement in leading indicators to be confident that this is a new up trend and a normal positive impact lag to central bank actions together with normal buying/speculating/risk-taking behaviour into the solar maximum. If this does not occur and instead we topple over again in terms of leading indicators and key assets, then either (i) the triple historic anomaly would have indeed come to pass (‘it’s different this time’) or (ii) yet further central bank action and unorthodox policy tools are deployed soon ahead before we finally do get that growthflationary finale not too far from the solar peak.

Until evidence points otherwise, I side with it not being different this time and that we will see normal behaviour into the solar maximum, aided by lagged impacts from central bank actions, and normal conditions to come to pass for a cyclical stocks bull end. I believe the current technical action in risk assets is supportive of this, in that we see certain key stock indices pushing to break out, an absence of normal cyclical stocks bull topping indicators (such as breadth divergence and defensives outperforming) and gold in a renewed up trend back above its 200MA following an 11 month consolidation.

Great post as always. USD is a little oversold here. I believe a one or two day bounce in the USD as commodities and equities consolidate/correct here.

Dec 12 is the next FOMC announcement – could be a big day in terms of news.

Another one to keep in mind, thanks.

Great post. Bullish Month according to Financial Ching. Any ideas about the validity of that methodology? Also read a nice piece about beautiful de-leveragings and ugly ones in a letter from Bridgewater. Very interesting about hyperinflation in Weimar and beautiful de-leveragings which the US looks more and more according to their ideas.

Not familiar with Financial Ching – do you have a link?

http://www.fourpillars.net/finance/index.php

New to all this astrofinance stuff so really going on a crazy testing spree.

John,

This article is about the December seasonal stock market pattern for the last 13 years. Data indicates that the Santa Claus Rally is in the 1st and 3rd week of December, but the last three days of the month are the strongest.

http://seekingalpha.com/article/1025881-santa-claus-rally-a-quick-glance-at-gains-for-13-years

Thanks Jack

All models updated this morning.

John,

A somewhat confounding notion for me is how we come to anticipate a speculative move up (equities and commodities) that is well above the ‘route map’ over the coming months while we simultaneously anticipating a somewhat tame or mild Solar Cycle in terms of geomagnetism, relative to other years. Would a speculative blow off move be accompanied by irrationally thinking investors influenced by a spike in Solar Activity? And while this doesn’t negate the theory does it mute the expected move a bit given that predetermining amplitude under any method is quite difficult. I wonder if this market can break through the range bound channel it’s carved. Significant Outer Planets are in waning squares and so may not pack the punch they provide on their waxing approach. Uranian Planets are not as active as they were during the 30’s/60’s. This past crisis and subsequent rebound seem orderly by comparison. And yet there lurks on the horizon a massive debt bomb that will have to go off one day if it isn’t detonated. I’m not convinced that inflation can defuse the bomb by itself.

Thanks for such provocative and insightful work.

HVA

Hi HVA, it’s something that remains on my mind as I look at the weak sunspots hill on the chart to date. However, when I looked back in time I found that there was no notable correlation between the size of the speculative mania and the size of the sunspots peak. My theorising on lunar cycles is that the influence of nocturnal illumination on humans is ‘hard coded’ into human biology now (and also a range of living things) – evidence for which is that artificial lighting has not made it redundant. In a similar manner, the ‘excitement’ in humans may ebb and flow with sunspot cycles in a partially internalised fashion, less sensitive to the size and intensity of the sunspot action (like the nearer ‘supermoons’ don’t appear to produce any greater effect on the markets than regular full moons). I believe that if the size of the solar cycle matters less, then we should see the regular range of associated phenomena: protest, war, earthquakes, speculative mania and inflation. So there are several measures.

I concur on the debt bomb, but again by my previous work, I maintain that, generally speaking, a collective crunch point for major developed countries is further out, 2030s onwards (I see us further down an unsustainable path). That is based on a renewed cycle of growth coming to pass, starting in a couple of years – a secular stocks bull. I expect debt growth to slow significantly in that period, but the next secular stocks bear following that has the potential for something more catalcysmic, due to the much higher public debt levels that have been reached in this secular bear.

Oh… It’s an inverse relationship… Hmmm… also just read that some investment houses are pricing in additional QEetc. into their models… Still, Getting to Euphoria from where we are seems quite a leap…

HVA

I believe we have the evironment for it to occur, in that cash and bonds are paying negative real returns, money supply has swollen but much is parked in reserves, central banks are still on the accelerator. If we were to see a natural upswing ahead in the business cycle together with the lagged impacts of renewed central bank actions this year, we could see the shift in confidence for money to pour out of reseves and bonds into pro-risk. After all, no-one wants to be in cash and bonds at current rates, it’s just the fear of capital depreciation in the other classes. If the solar theory is correct, then the rise into the solar maximum next year should inspire speculative confidence, which can become an upward spiral.

If conflict erupts in oil supply sensitve regions, if extreme climate continues to push on low-inventory agriculture, then we can add supply side pushes to the mix.

But yes, it takes a leap from how things are currently (and others might argue the central bank actions are impotent). Which I why I always say one step at a time, and see how things progress.

John,

Worth a look.

Also Tom Demark has predicted the Shanhai Comp. will rally 48% in the next ( monthsfrom below 1960 to around 2900.

Cheers.

.http://www.telegraph.co.uk/finance/comment/ambroseevans_pritchard/9717728/The-worlds-commodity-supercycle-is-far-from-dead.html

Good stuff, thanks

Sorry.

Thats 9 months and the Shanghai Comp. index.

Hey John, good stuff. What a frustrating year to be an investor. Even some of the bulls have got crushed picking the wrong stocks. If you were a macro investor like yourself, betting on a broader scale, you got it right and congrats to you.

I wanted to share with you and the rest of the board probably the best financial quarterly letter/ paper I read all year. It was written by Christopher Cole of Artemis Capital Management, a volatility investment fund. It is a bit of a read and lot’s of technical details, but by far the best paper produced this year that I think any and every trader and investor should read at least once. Very profound, very enlightening.

Guess it would help if I post the link:

Click to access ArtemisVegaQ32012_Volatility_of_an_Impossible-Object.pdf

Love these guys! Thanks for posting. Have been been long financials and started looking for long dated out of the money options to protect the inflation/hyperinflation tail end 😉 as per Artemis previous letters.

Call me crazy but I love Bank of Ireland and AIG.

Thanks Ryknow, and a good read.

Bravo. I appreciate your generous sharing. Thank you.

Buy the stock market when there is a bull market in fear as participants are hedged for a 2008 replay while Joe Sixpack has the cash to buy the dips. No wonder corrections have been relatively shallow so far…. So the corollary is that we may see a new high before a significant correction.

Here in Stockholm it is a total snow storm. I can’t see more than a meter from my window. It is really really cold here. From what I understand this winter is going to be abnormally cold and perhaps the same is true for the US which should be bullish for stocks.

Don,t forget about the COT data