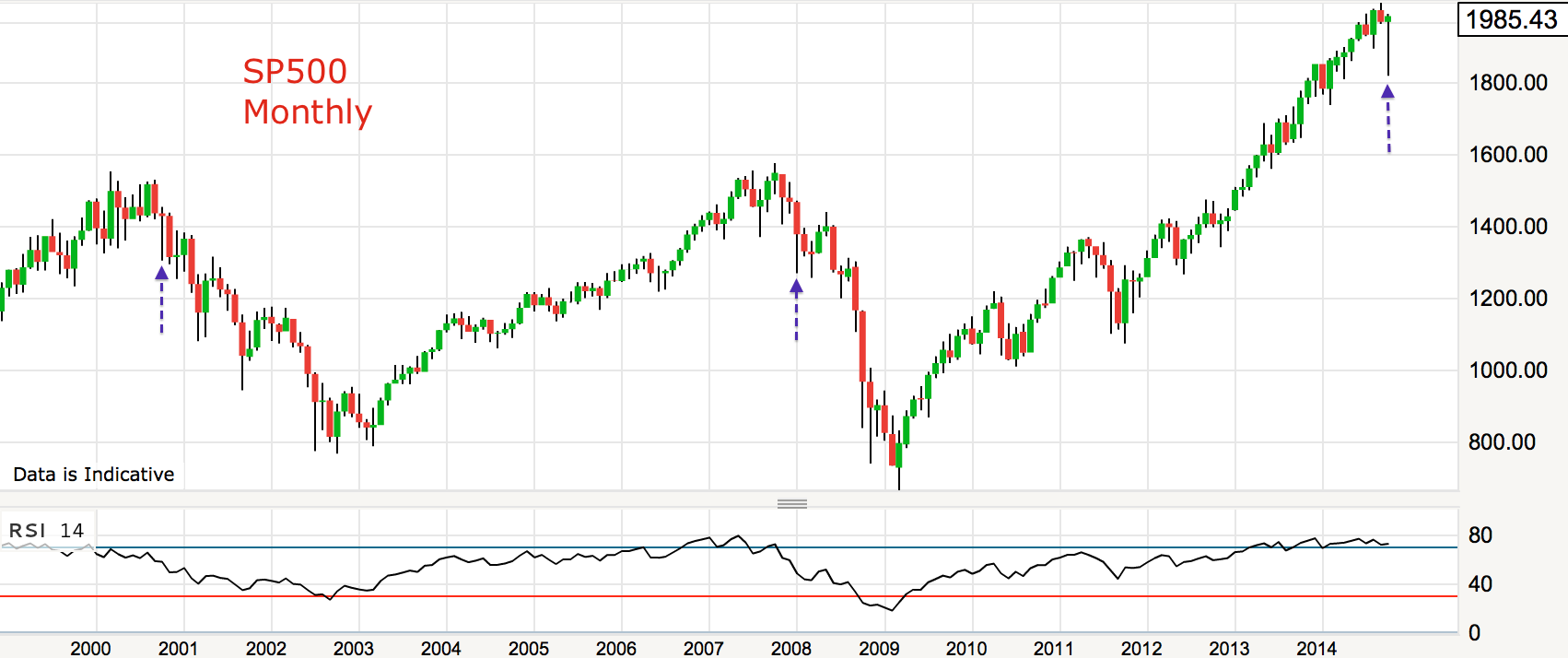

A doji on the SP500 on Friday, making for a week of sideways range. But there is one index still not slowing down, the Nasdaq 100. Apple and Microsoft are still in steepening uptrends, dragging this index higher. Note that these two stocks outperformed right into the end of 2007, later than most, so their rollover may be the last domino to fall. Unlike the other indices, the Nasdaq 100 is showing no major breadth issues, but does have divergences in bullish percent and volatility.

Source: Stockcharts

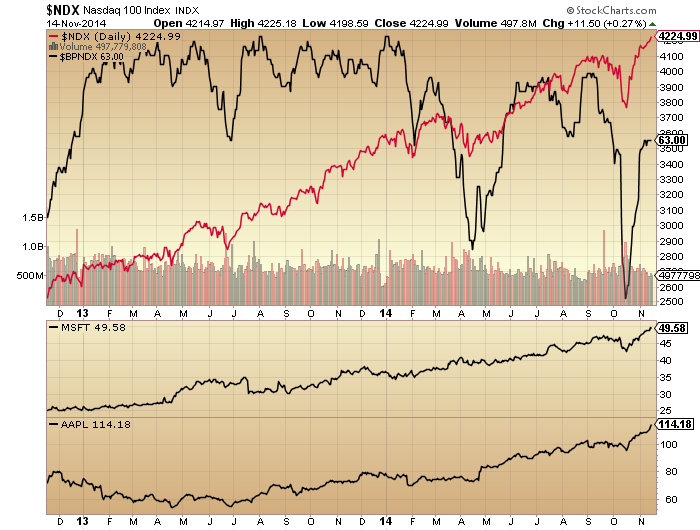

The longer term Nasdaq 100 chart does however show typical major topping divergences:

So, I’d like to see large intraday reversals / voluminous down candles on Apple and Microsoft and in turn the NDX as a sign of a peak.

So, I’d like to see large intraday reversals / voluminous down candles on Apple and Microsoft and in turn the NDX as a sign of a peak.

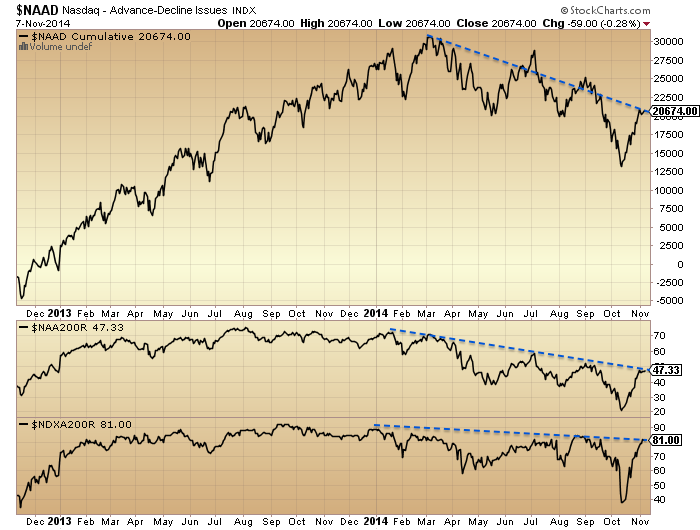

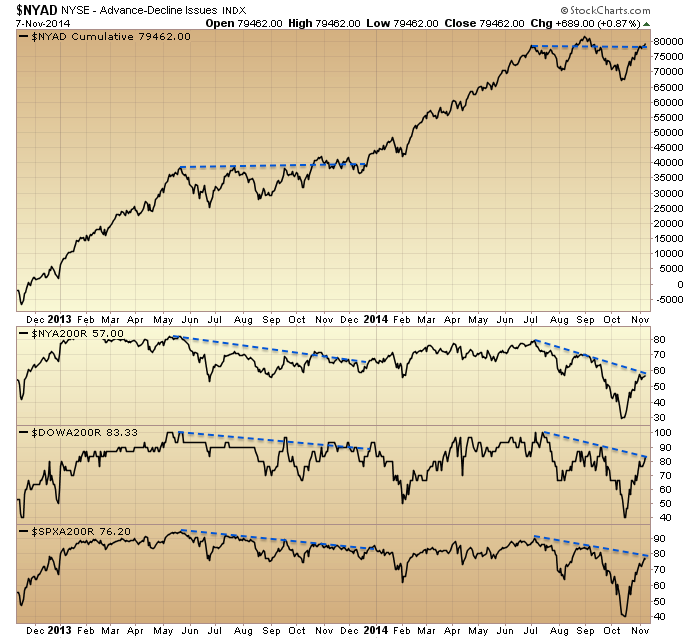

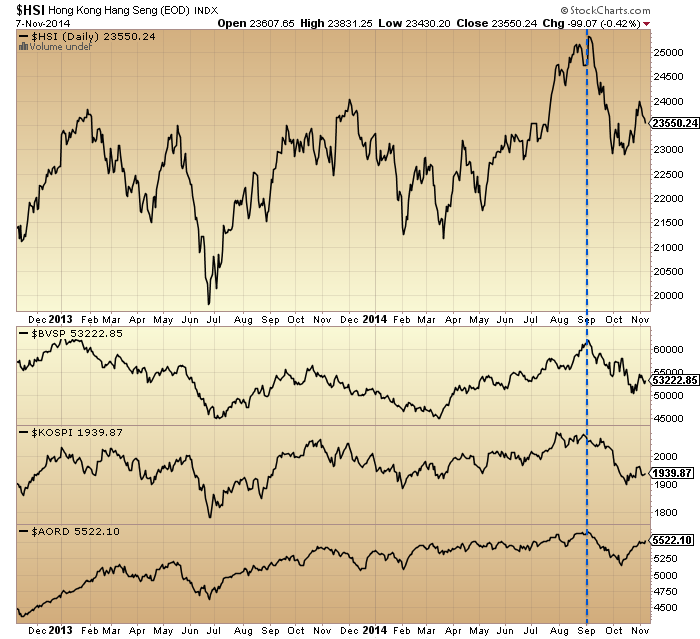

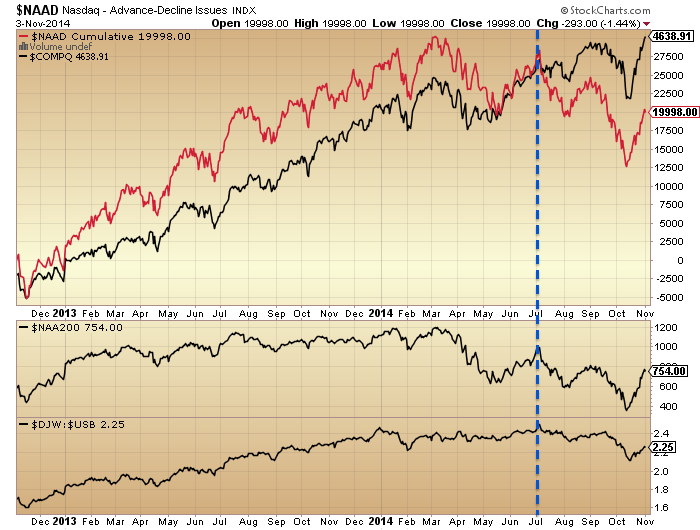

The last dominos to fall idea is supported by the bigger picture. Various risk measures peaked out in January, European stock indices and US small caps topped out around June, other global indices peaked out in September, and breadth has been diverging on the SP500, Dow and Nasdaq composite. Look at the Nasdaq composite breadth compared to the NDX, it now has 4 lower highs and lower lows over an 8 month period:

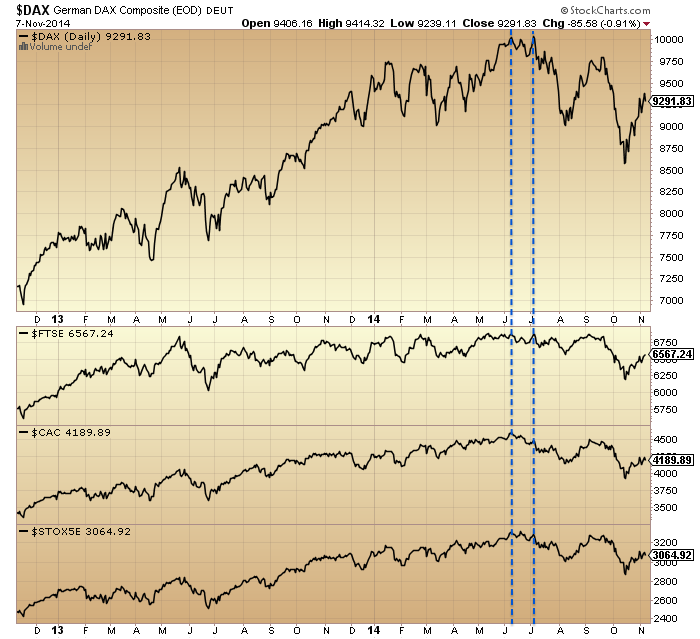

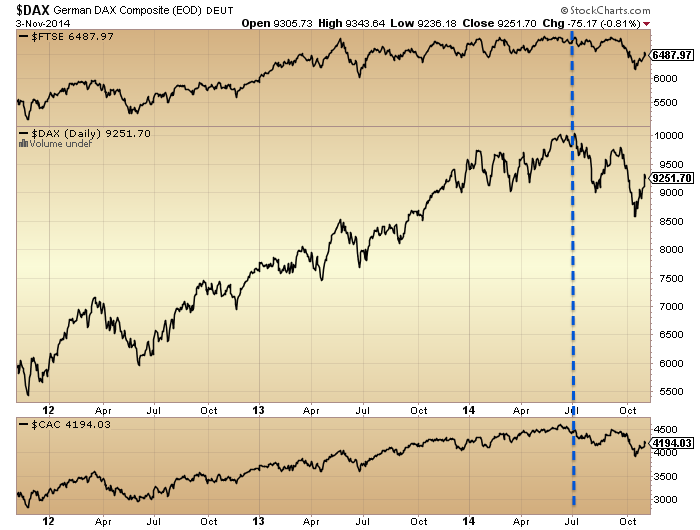

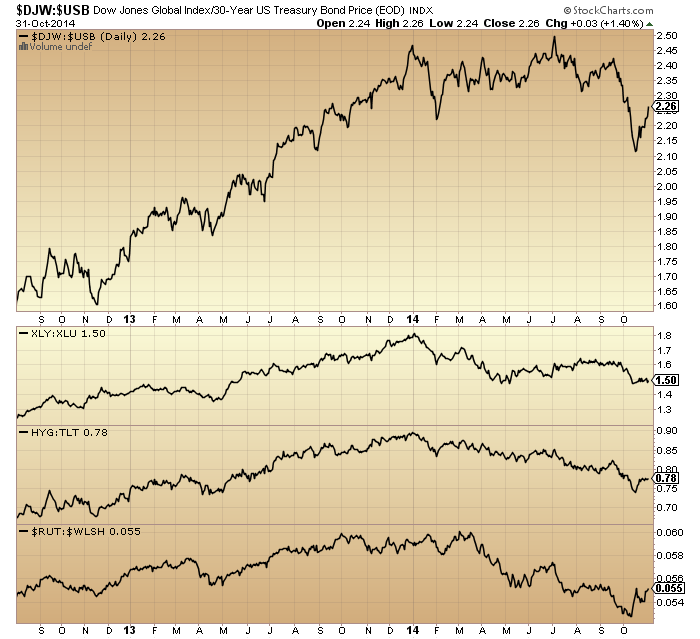

The Dow Jones World index is shown below. A clear double top and lower high/low, with divergences on this rally since the turn of November. John Li raised the possibility that US large caps may still need a ‘second chance’ peak given they have made new highs again, and I can’t rule that out, but on DJW this is a fairly typical second chance peak should stocks now roll over.

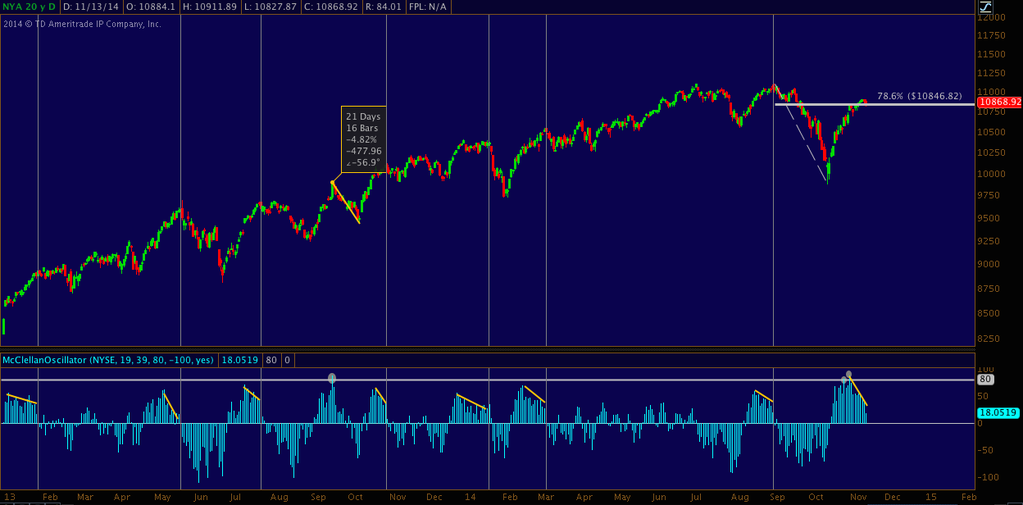

Here’s why stocks should be ready to now finally roll over. The McClellan Oscillator has diverged as it did at previous recent peaks:

Source: Andrew Kassen

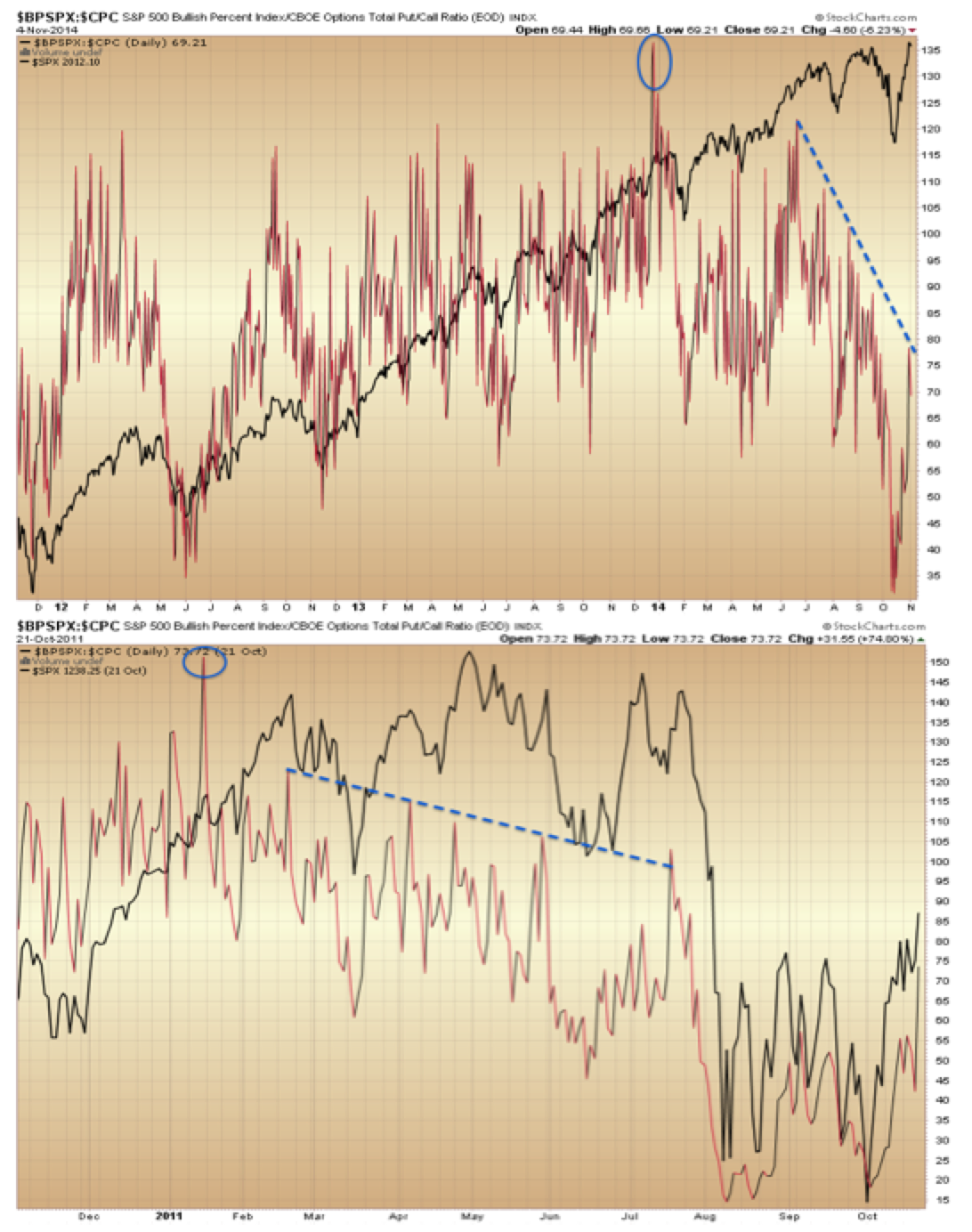

ISEE put/call ended over 200 again on Friday, making for 4 prints over 200 in the last 2 weeks. These extremes are signs of topping.

Source: Andrew Kassen

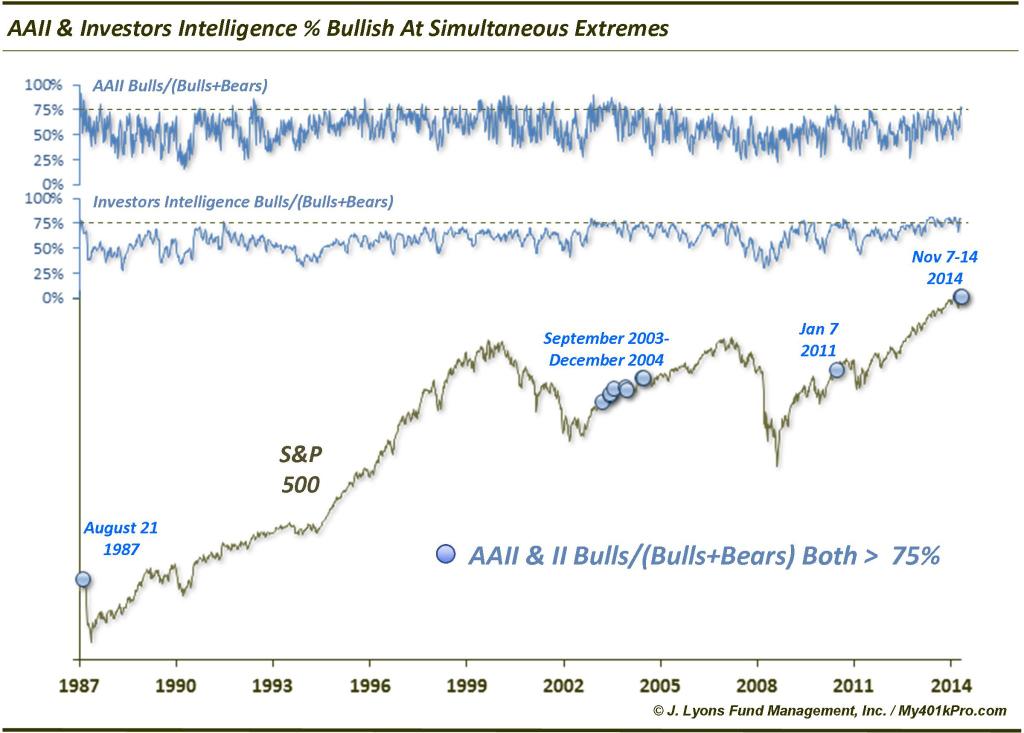

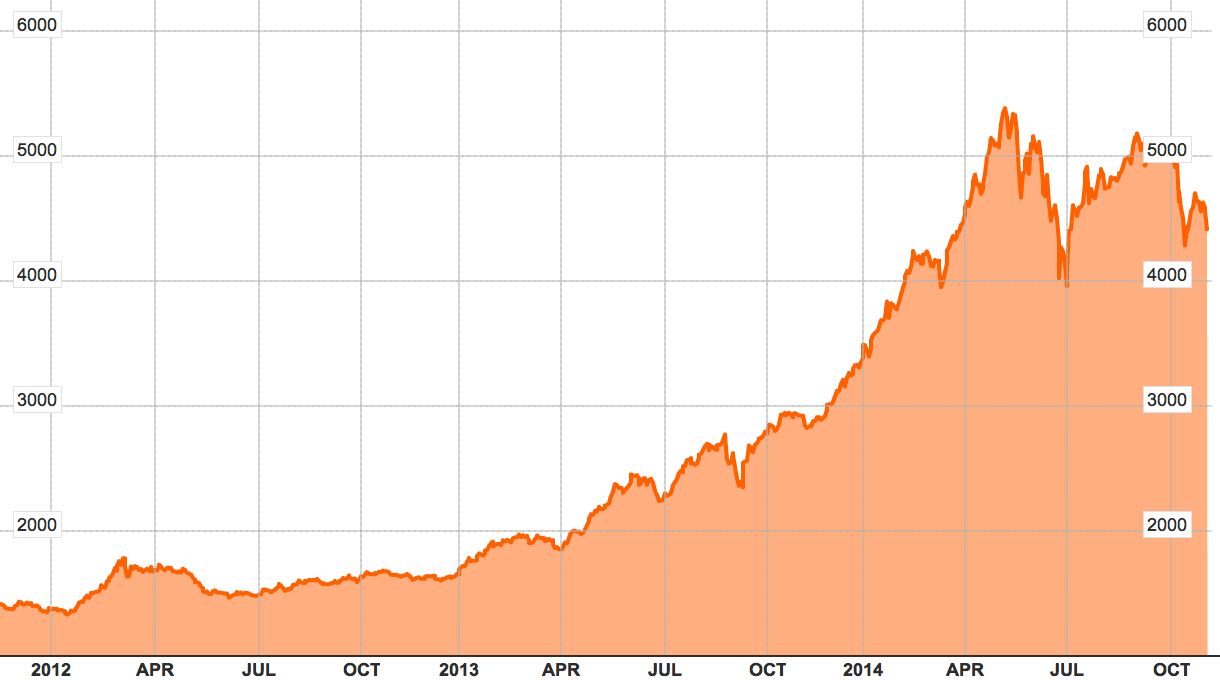

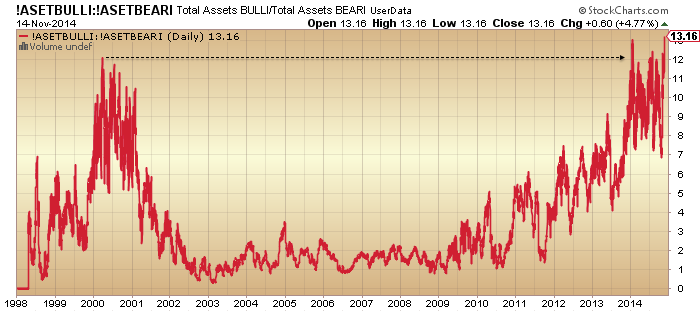

Rydex allocations made a new all-time record at the end of Friday. Take a look at the Rydex history in conjunction with AAII bears and II bears history versus current readings:

All at absolute extremes. If a bull market top occurs when there are no bears left to convert then these three proxies are screaming exactly that.

However, here is short interest, which appears to reflect the opposite:

Source: PFS

Either this is supremely bullish, like previous major lows, or something else is going on. It should be clear that we are not at a significant low like 2009 or 2011, and the October correction didn’t get close to a washout in sentiment or allocations like the other two lows shown, so how can we explain it? Look at the rising trend since the turn of 2013 which is when the mania began. I suggest this is hedging. Similar to the persistently high range in Skew that has been in place.

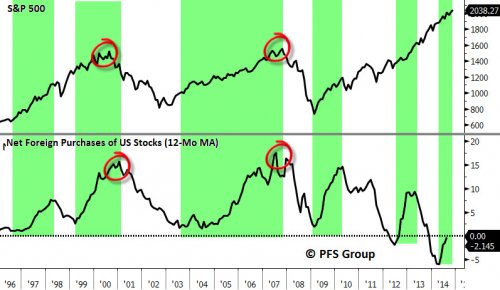

On a related note, look at foreign buying of US stocks, below. This also diverged from the turn of 2013 when the mania began. PFS see the current reading as bullish, but it should be clear again that something else is going on. Foreign purchases trended closely with the SP500 until the turn of 2013, after which they stopped tracking. Again the idea that this level is synonymous with a major low in stocks is clearly wrong. We know that buybacks and US retail clients have been the two main drivers of the mania phase and that leverage and allocations have been take to record extremes. We know that institutions have been net sellers in the mania phase and the below chart reveals there has been dwindling fuel from overseas too. Therefore, the combination of companies borrowing to buy their own shares back and retailers buying high and going all in on leverage is the worst possible foundation for current prices.

Treasuries rallied on Friday, precious metals burst upwards, and junk bonds had another down day. All these developments suggest stocks should be about to fall.

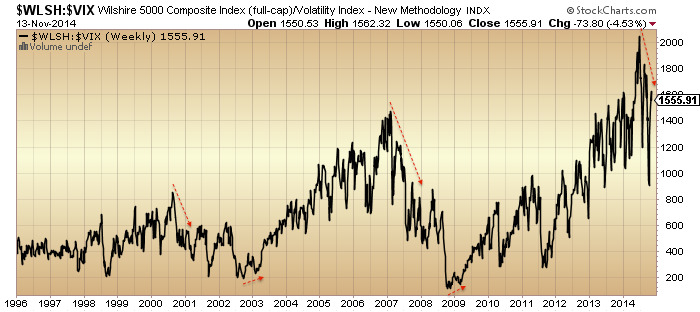

Vix rose last week and continues its overall divergence which again warns of a change in trend in stocks. Look at the similarities in stocks:volatility to the previous major peaks:

In short, I still think stocks will see a voluminous down day in the next few days and kick off the new and final leg down. There is no fuel for higher by various indicators above, so I believe the flattening out of the SP500 last week is the prelude to the next big move: down. I am not a fear-monger but given the incredible extreme state of multiple indicators, the ferocity and exhaustiveness of the rally since mid-Oct, and the large megaphone formation on US large caps, I believe an almighty crash is going to occur. In the last solar maximum mania of 2000, the Nasdaq’s mania from the start of 1999 to March 2000 was all retraced by the end of 2000. I equate us to November 2000 but here in 2014 we have postponed any true correction as the year has progressed, making for what may become a mega-correction right at the end of the year. How the mania reversed hard in 2000:

ECRI leading indicates for the US have dropped further. Their shaping level now mirrors 2011, 2010, 2007 or 2000: all significant market peaks.

Source: DShort / ECRI

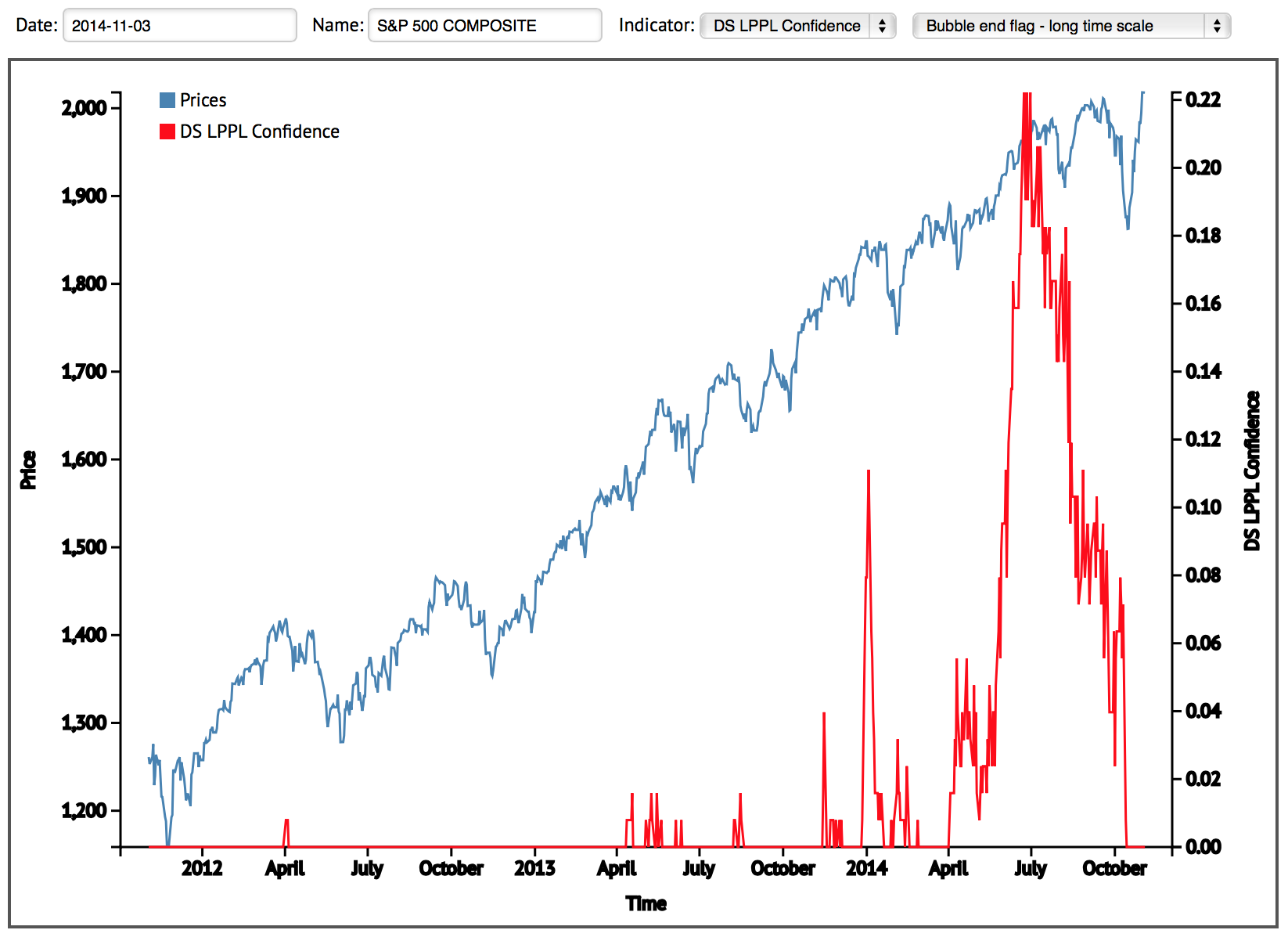

Lastly, the Sornette bubble end flag remains at July for the SP500 and September for US Tech. There has been no rebubbling since.

Source: Financial Crisis Observatory

Source: Financial Crisis Observatory

Looking for an analog where the Sornette bubble ended before stocks made marginally higher highs and then fell, there are only a couple of examples from history. In 2007, the bubble-end flagged in June/July and then stocks made their marginal higher high on multiple divergences in October 2007. In Russia 1998, something similar:

It was the same phenomenon: marginally higher highs but on multiple negative divergences. Same as now: a lot of divergences have developed since the start of July whilst we have gone on to make marginally higher highs.

So, it’s more support for the case that stocks should turn down here at their marginal higher highs in a final manner, rather than breaking upwards.

We have a week left until the new moon. Can equities hold up or even rally into then? Hold up with a few more dojis whilst we see further deterioration? Maybe. Rally? I just can’t see it when allocations and sentiment are so super-stretched. Rather, I still expect we will end November down and follow through on the large monthly October hanging man candle. That would imply stocks should fall before we get to the new moon. I am looking for a large red daily candle early next week, with the behaviour in gold, junk bonds, European indices and small caps last week as the lead in.