The less orthodox way, that is. Click to view larger, read the comments on the charts, then my comments below.

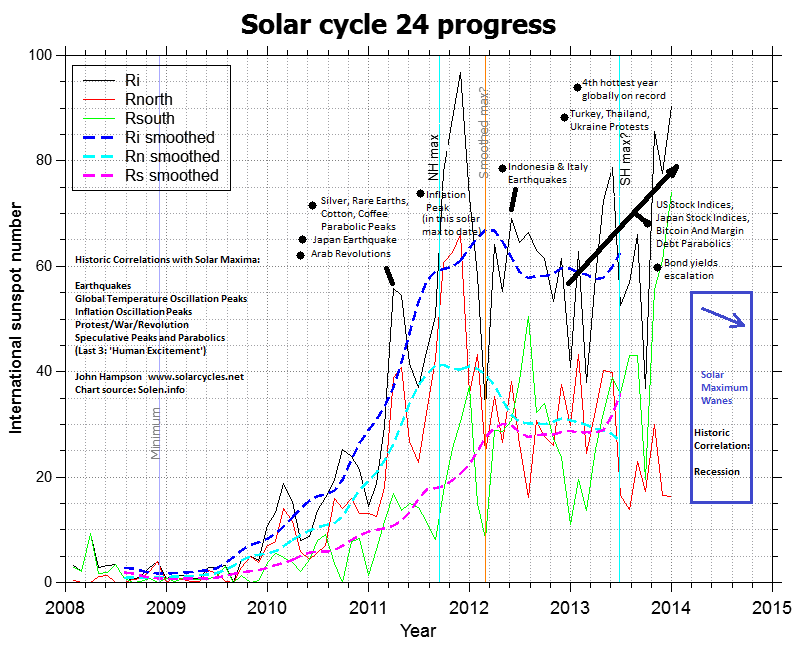

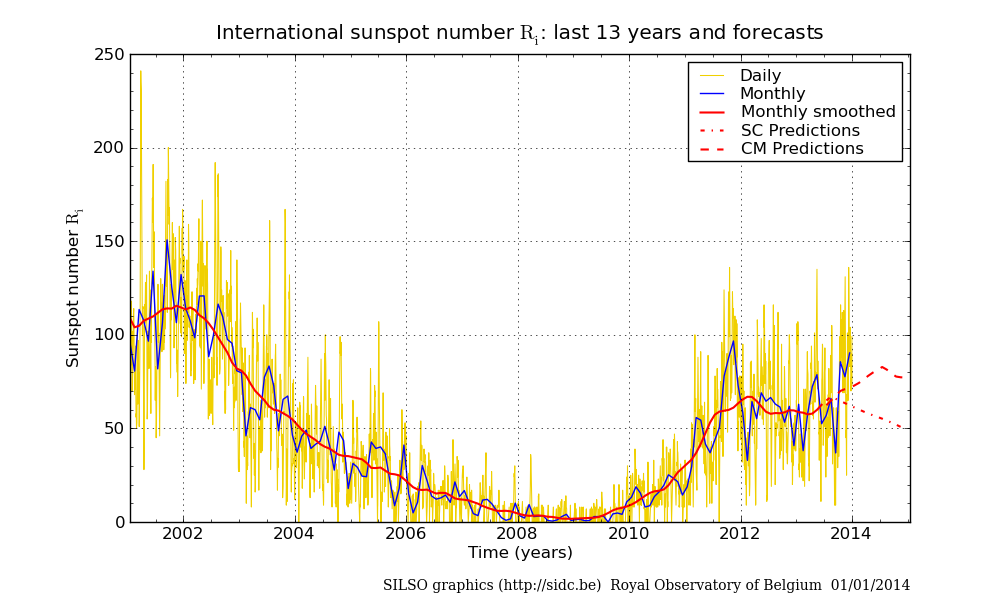

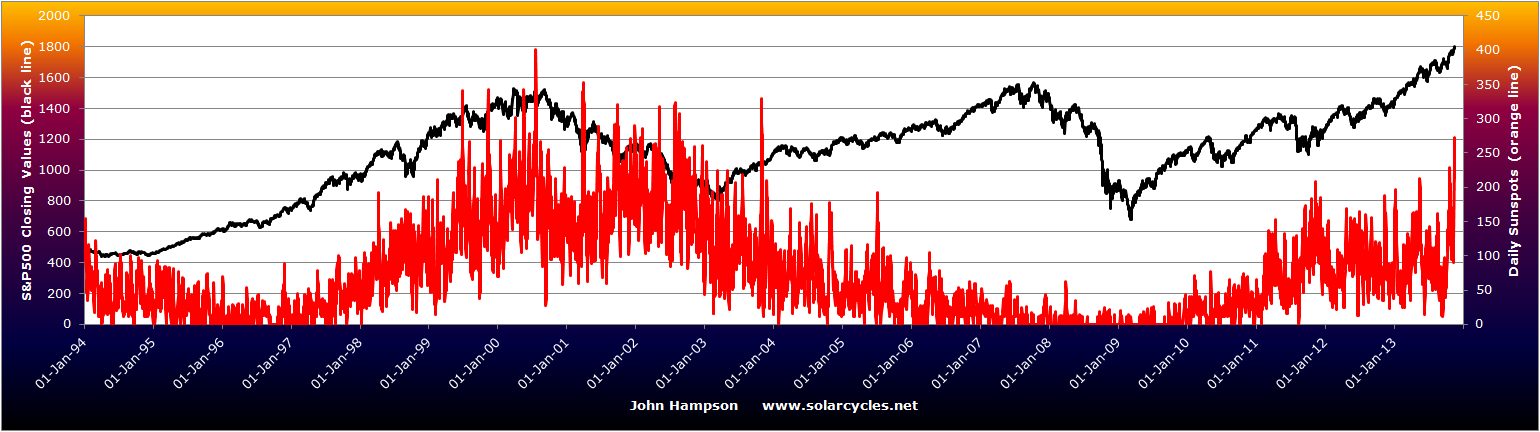

245 sunspots yesterday, third highest daily count of this solar cycle. The current cluster of solar activity, related to the recent southern pole flip, looks set to drag up the smoothed-max of SC24 and override the previous high of Feb 2012. No guarantees of course, until we see with hindsight. Also no guarantees that the sun does not yet become busier still. With SIDC’s CM prediction forecasting a mid-year smoothed solar maximum, there remains the potential for a peak any time up to then, which by association could mean a peak in US indices any time between now and then. However, SIDC’s SC foreast, NASA and NOAA models, confirmation of the pole flips, and our own Jan Benestad’s methods, support waning from now. So let’s see how this month progresses.

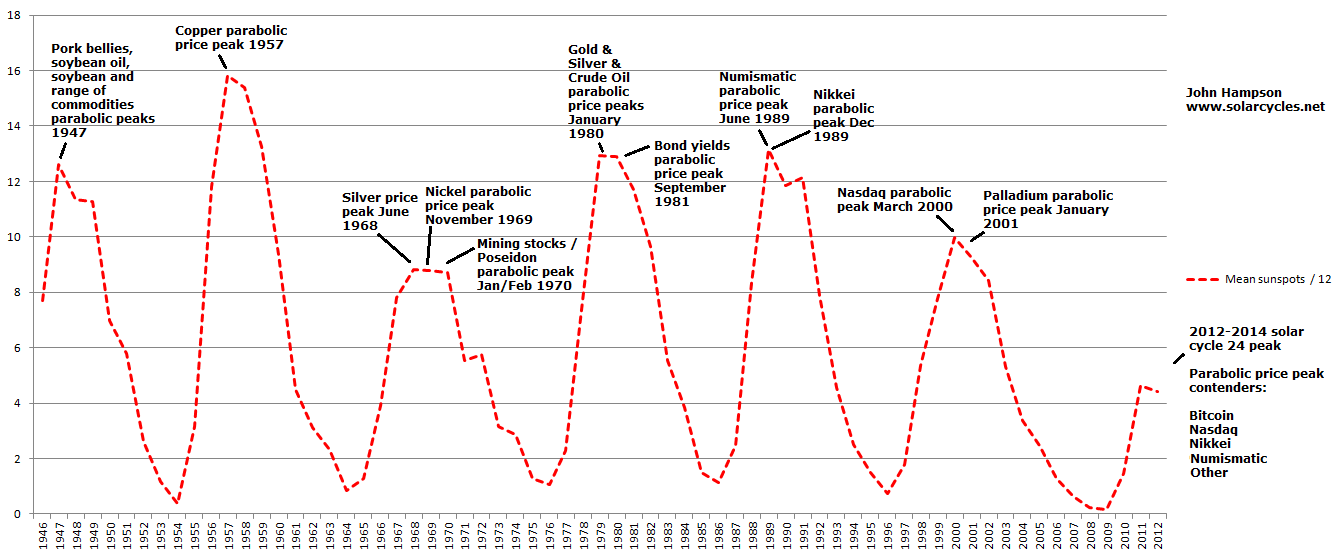

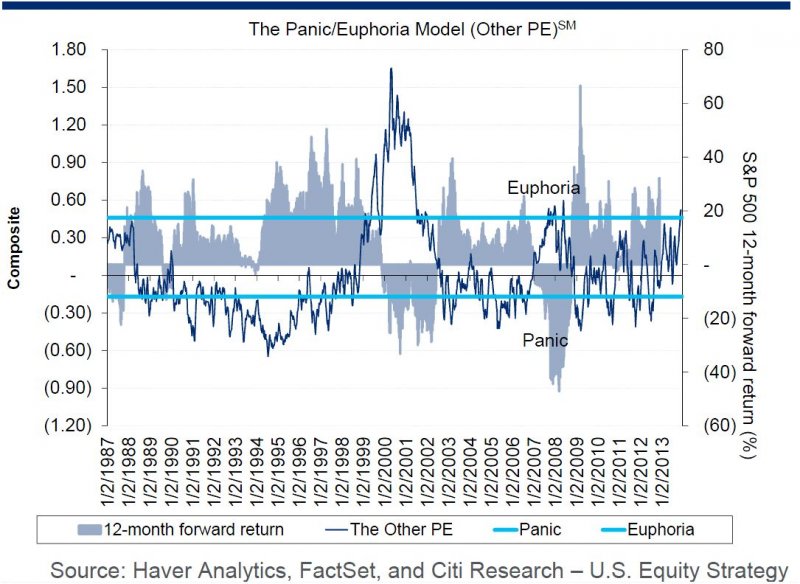

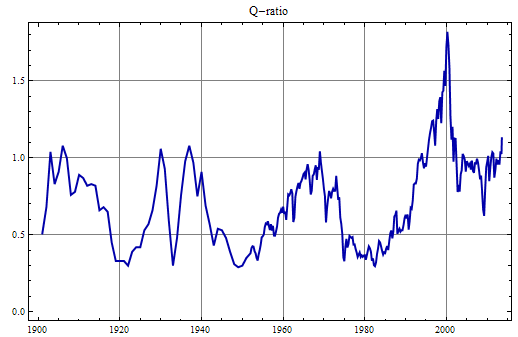

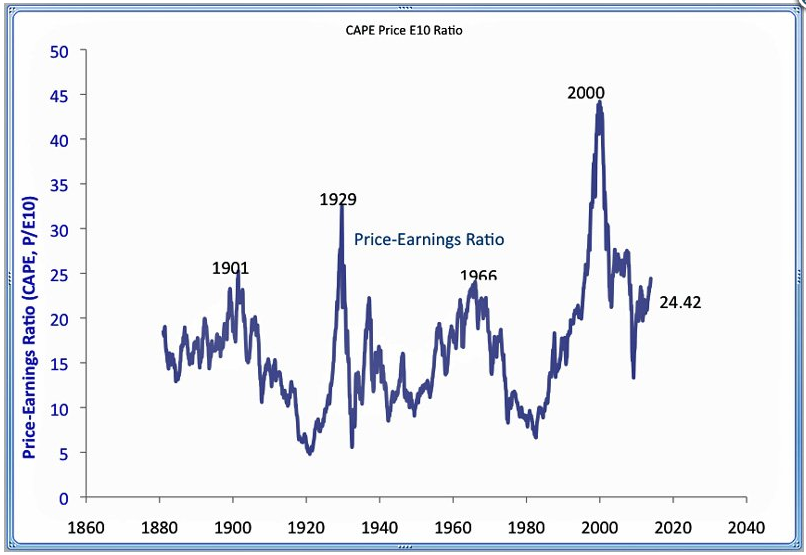

The gold and oil parabolic peaks of 1980 were unprecedented and historic. The Nikkei mania famous, and the numismatic bubble the only major one in its history. The dot.com boom the biggest mania of all time, by various measures, so does the current US stock indices rally measure up as a suitable solar-inspired excitement mania? If it is, then we will look back on it as the second largest and third longest equities bull of the last 80 years, where margin debt and investor credit spiked to dot.com peak levels (highest ever), where Market Cap to GDP valuation reached the second highest ever (first: the dot.com peak), where we printed some all-time record sentiment readings, including the highest ever II bull/bear spread, and stocks rose into their peak in a compressing parabolic, chasing price without earnings for 2 years into the peak. It definitely measures up.

However, caveat again. It does not preclude things going even crazier yet, before we roll over. But whether we look at what’s going on with the markets or what’s going on with the sun, they are both sounding the siren for a top.

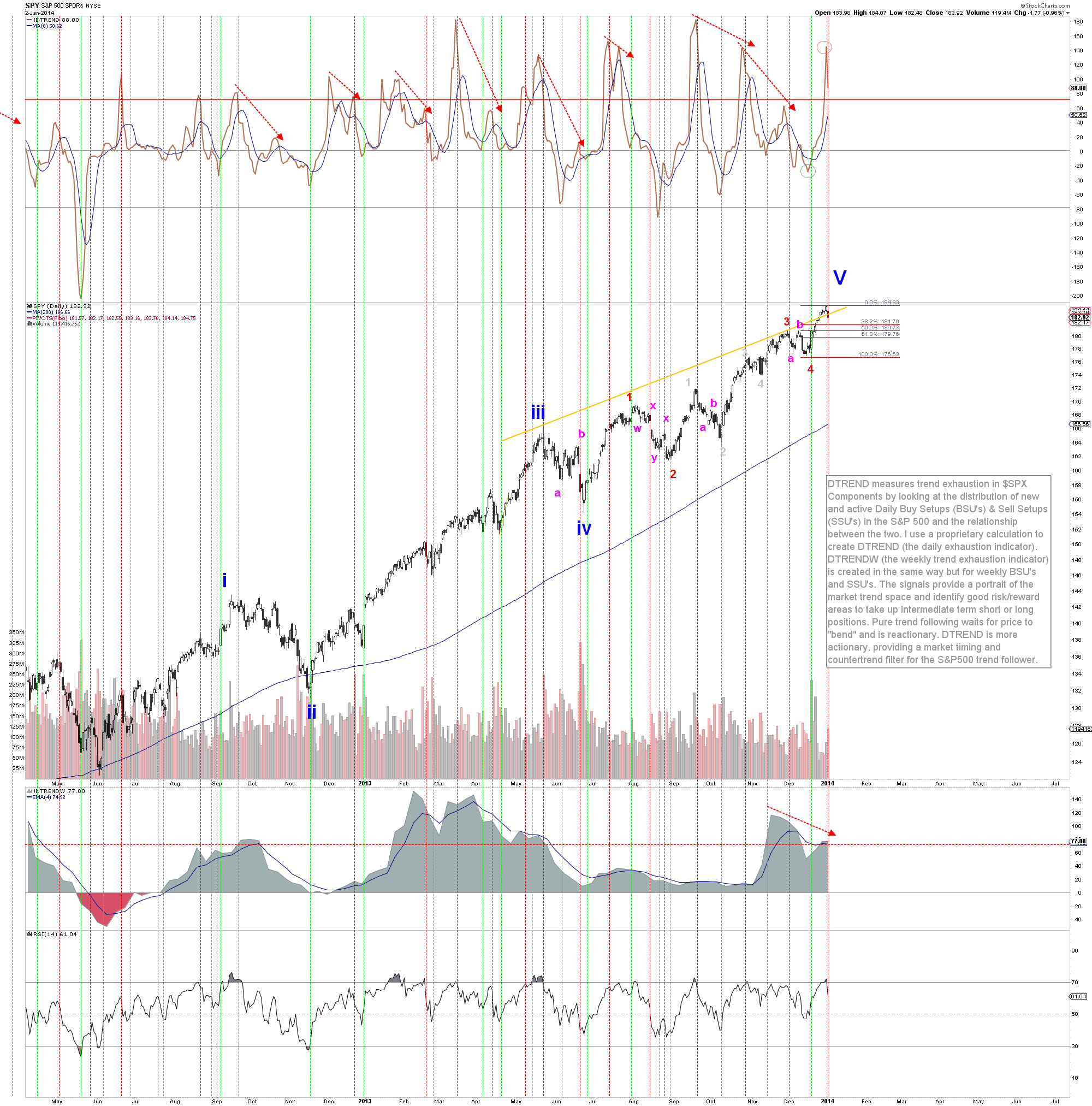

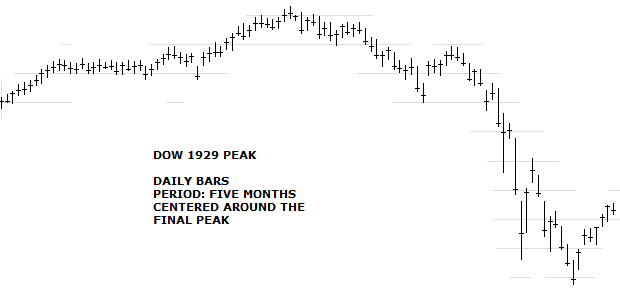

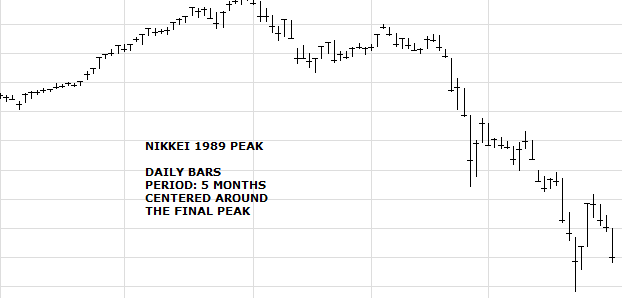

Below I’ve zoomed in on the daily action into the 1929 Dow and 1989 Nikkei tops (see post HERE for why these analogies carry weight). On a longer term view these were parabolic compressions, but we can see from the daily bars that at the peak there was no high volume climax and collapse (as might see in individual stocks), but rather a gradual transfer from bulls to bears, with some backing and filling until the bulls finally capitulated and a crash resulted.

So we can look out for something similar occurring now the markets are correcting from their 31 Dec high. If equities break upwards to new highs on strong momentum then chances are we are going more parabolic yet before termination. If equities stay beneath their 31 Dec highs or make a marginal higher high on divergences, then the case will build for a topping pattern similar to the above.

So we can look out for something similar occurring now the markets are correcting from their 31 Dec high. If equities break upwards to new highs on strong momentum then chances are we are going more parabolic yet before termination. If equities stay beneath their 31 Dec highs or make a marginal higher high on divergences, then the case will build for a topping pattern similar to the above.

If 31 Dec turns out to be the market top, it was the last trading day of the year. The last time a stock index topped out on the last day of the trading year was the Nikkei in 1989.