A recap of the big picture.

In 2014 around 40 stocks bull market top indicators gathered. The list includes valuations, leverage, allocations, sentiment, money losing IPOs, buybacks, breadth and risk divergences. Collectively, they depict what we just experienced as the second biggest mania of all time.

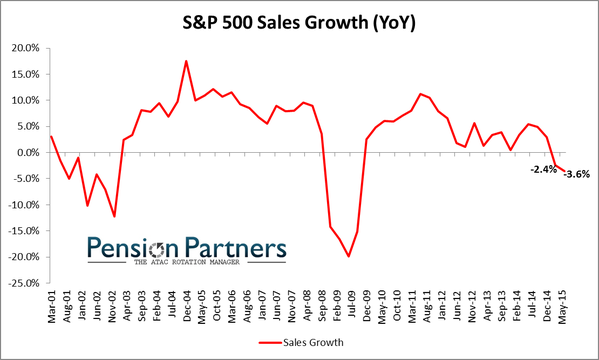

Here is the SP500 price to sales ratio reaching a record in 2015.

Now understand that the Nasdaq price to sales ratio escalated to 6 at the 2000 peak but the Biotech (poster boy for this mania) price to sales ratio reached 10 at the 2015 top.

The caveat to all the above is that conditions are historically anomalous: low inflation, falling commodity prices, ultra low interest rates and QE. Nonetheless, conditions were indeed similar to this in 30s US and 90s Japan and tellingly both bear markets and recessions occurred, i.e. stocks did not need ‘repricing’ or otherwise recalculating.

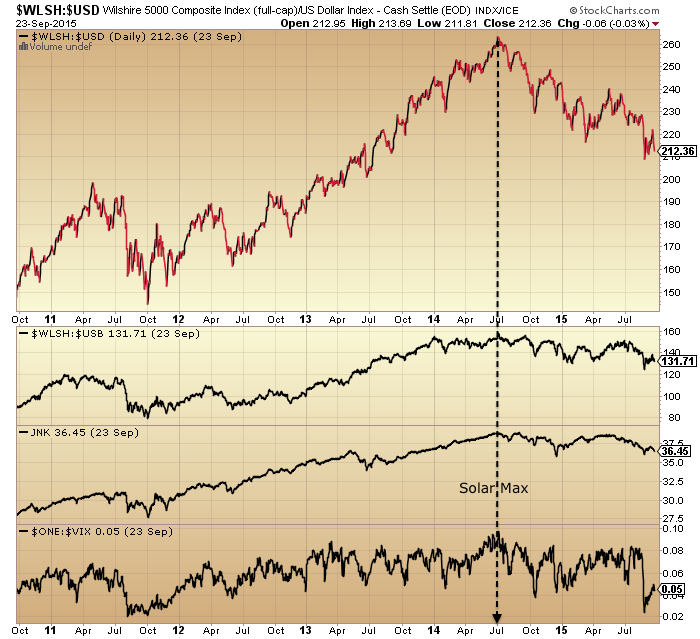

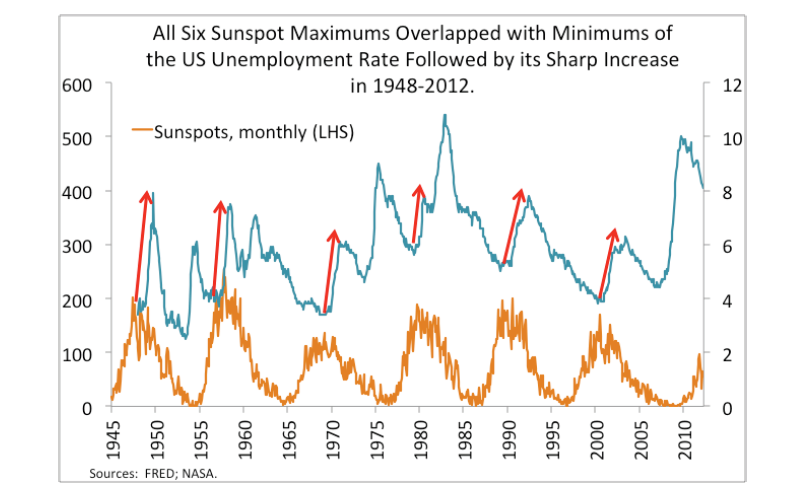

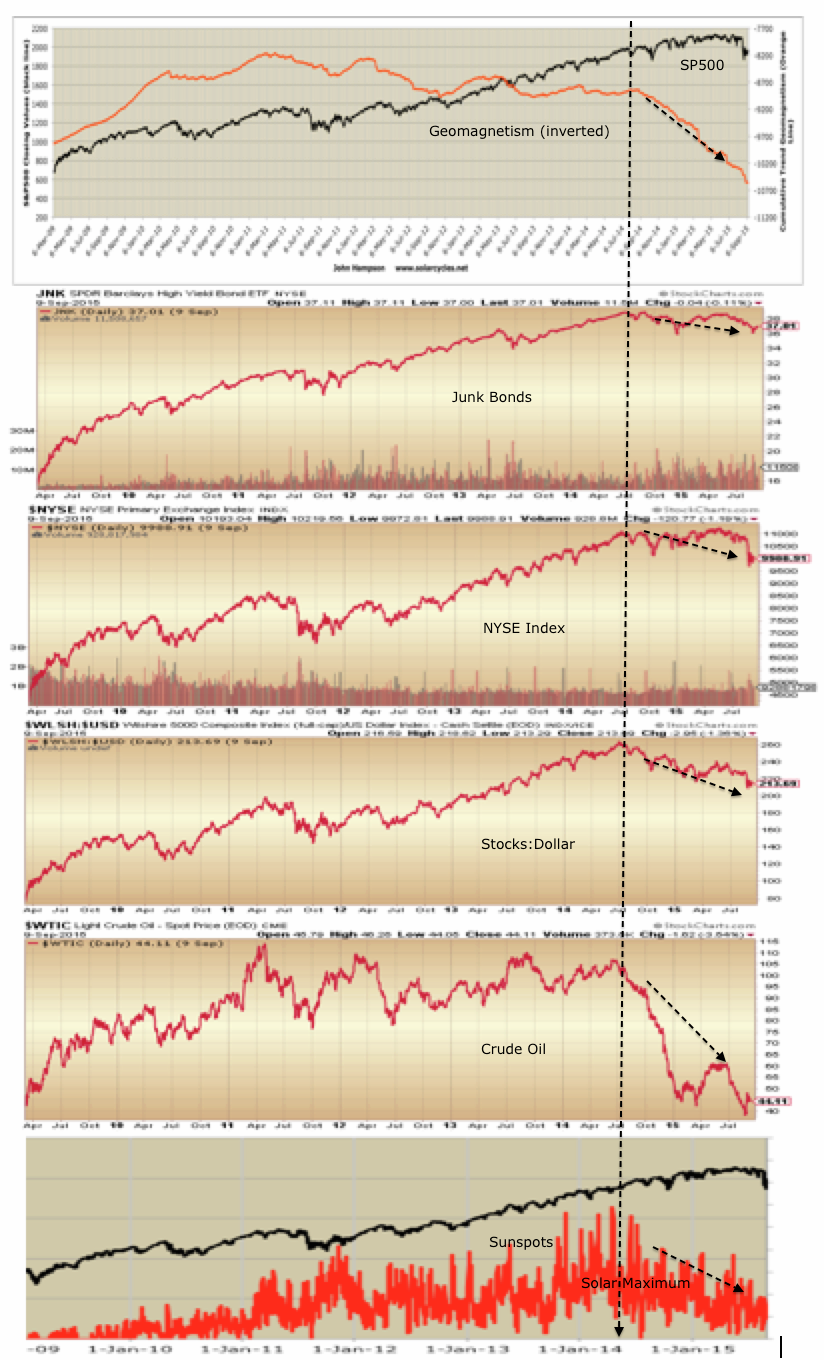

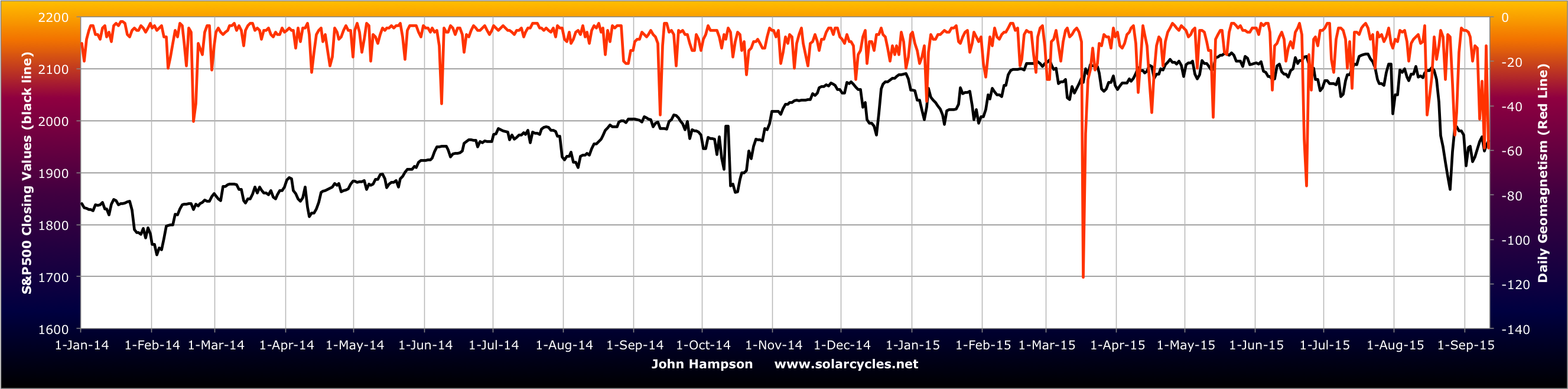

Add in the solar max for timing and we can see that under the hood multiple financial and economic indicators peaked out mid 2014 along with the solar reversal, adding to the likelihood that we are now in a bear market and heading into a recession.

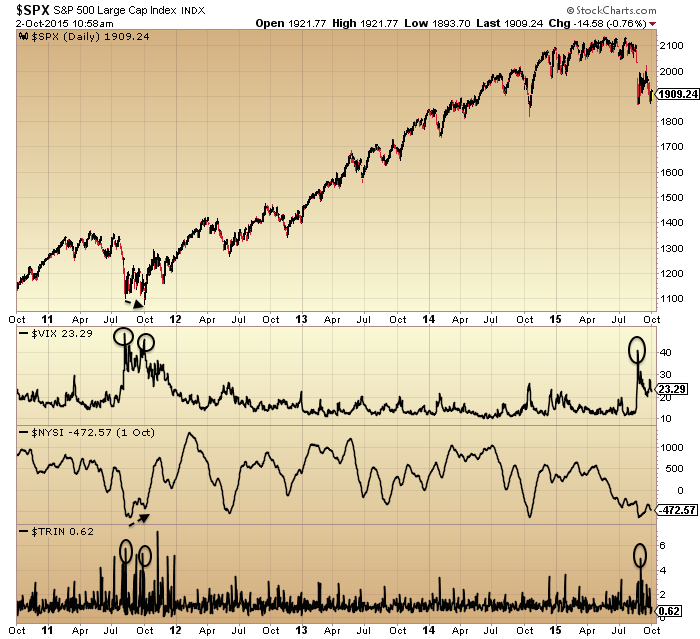

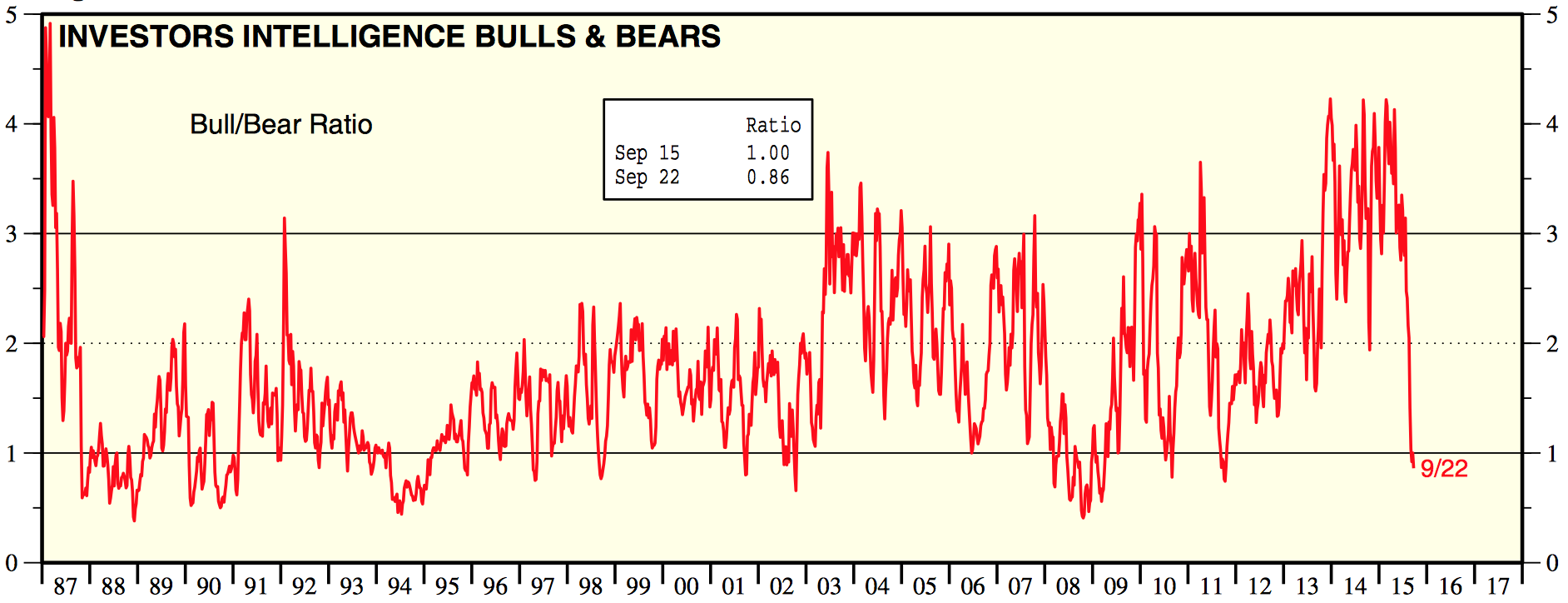

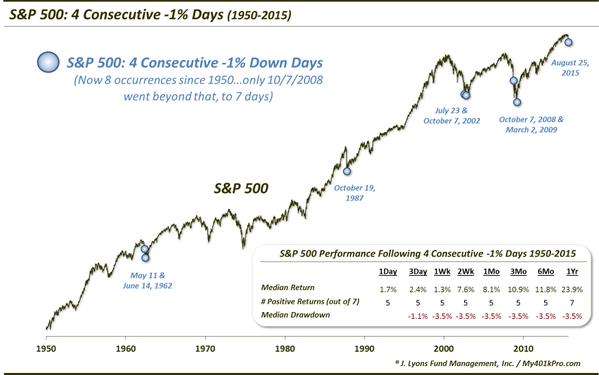

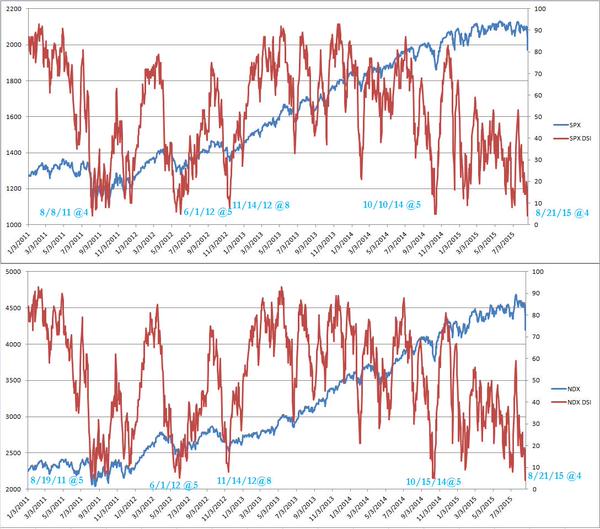

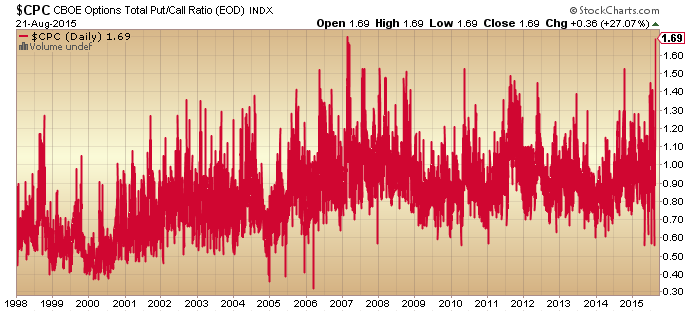

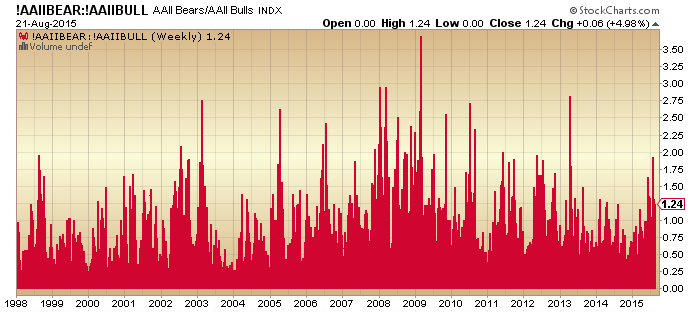

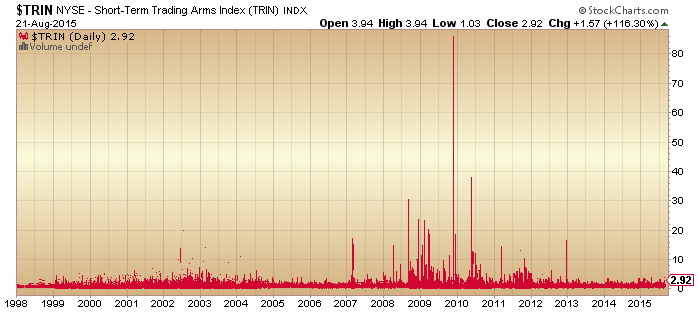

The mania burst in August, with a fairly vertical 10% price drop. Certain indicators that had been stuck at extreme bullish (contrarian bearish) fell sharply to low levels. These include sentiment surveys, put call ratios and inverted volatility. Based on the new readings in these indicators, some analysts are calling for a price bottom and bull market resumption. However, be aware that certain other indicators such as valuation, leverage and household allocations are still very high and a long way from mean reversion.

Many depict what we are going through as similar to 1998 or 2011. So here are the charts.

In both instances price made a lower low on a second capitulation reading before taking off again. Bringing us right up to date, the price reversal of this last week did not occur from a similar high volume high fear secondary low, which may mean a lower low is still ahead.

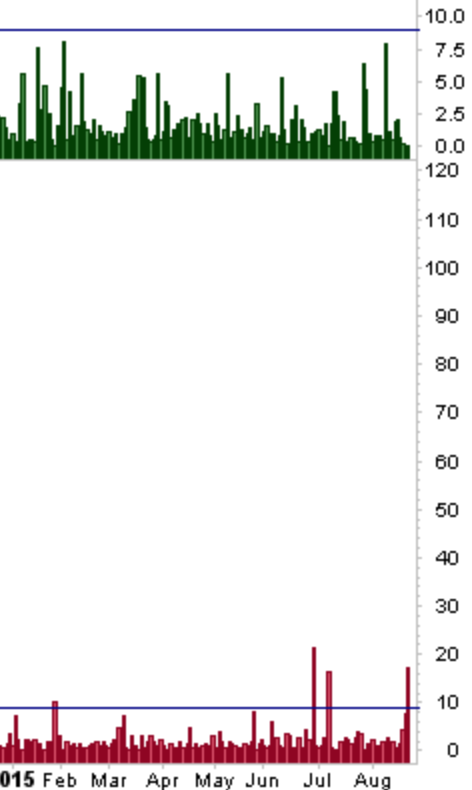

As an example of that partial case only, here is bullish percent to call out showing a suitable washout but volatility to stocks not there.

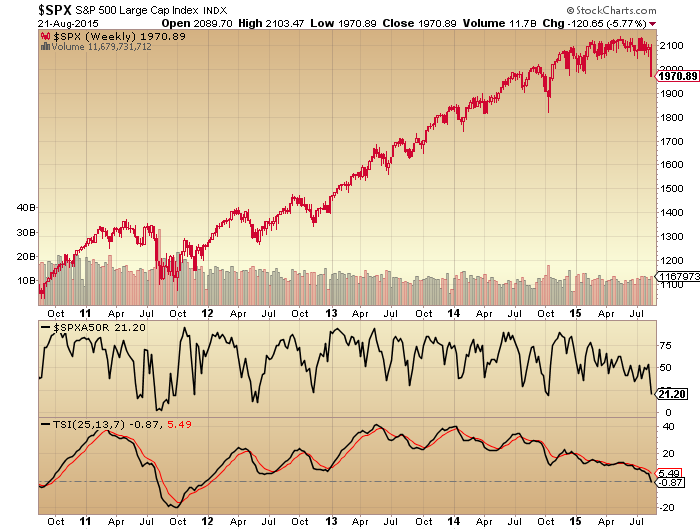

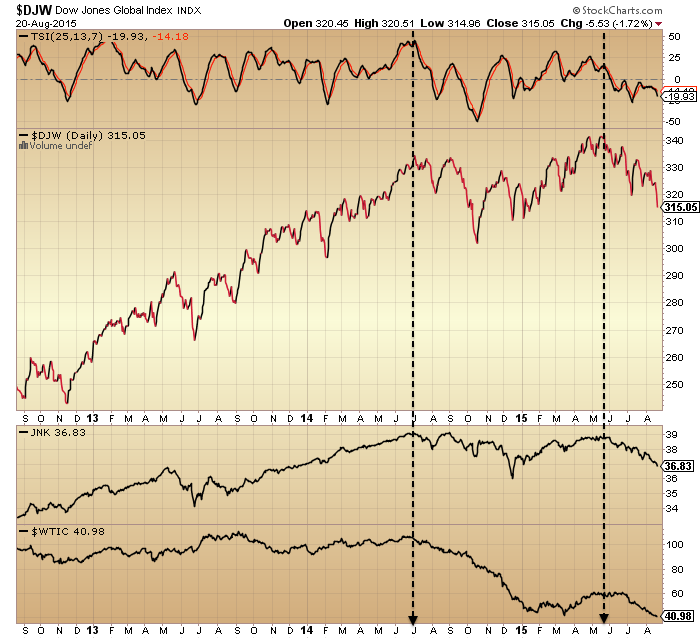

However, rather than 1998 or 2011 I think a more pertinent comparison is a bull market mania peak, such as this:

The arrow denotes a possible analog. The sharp declines and post sharp declines stabilisation are similar, followed by a couple of days rally into the arrow that then failed.

Should last week’s price recovery instead be built upon next week and through October, then we may be looking at a slower bear market initiation, whereby we perhaps head back up towards the 200MA like in early 2001 or 2008 before rolling over again.

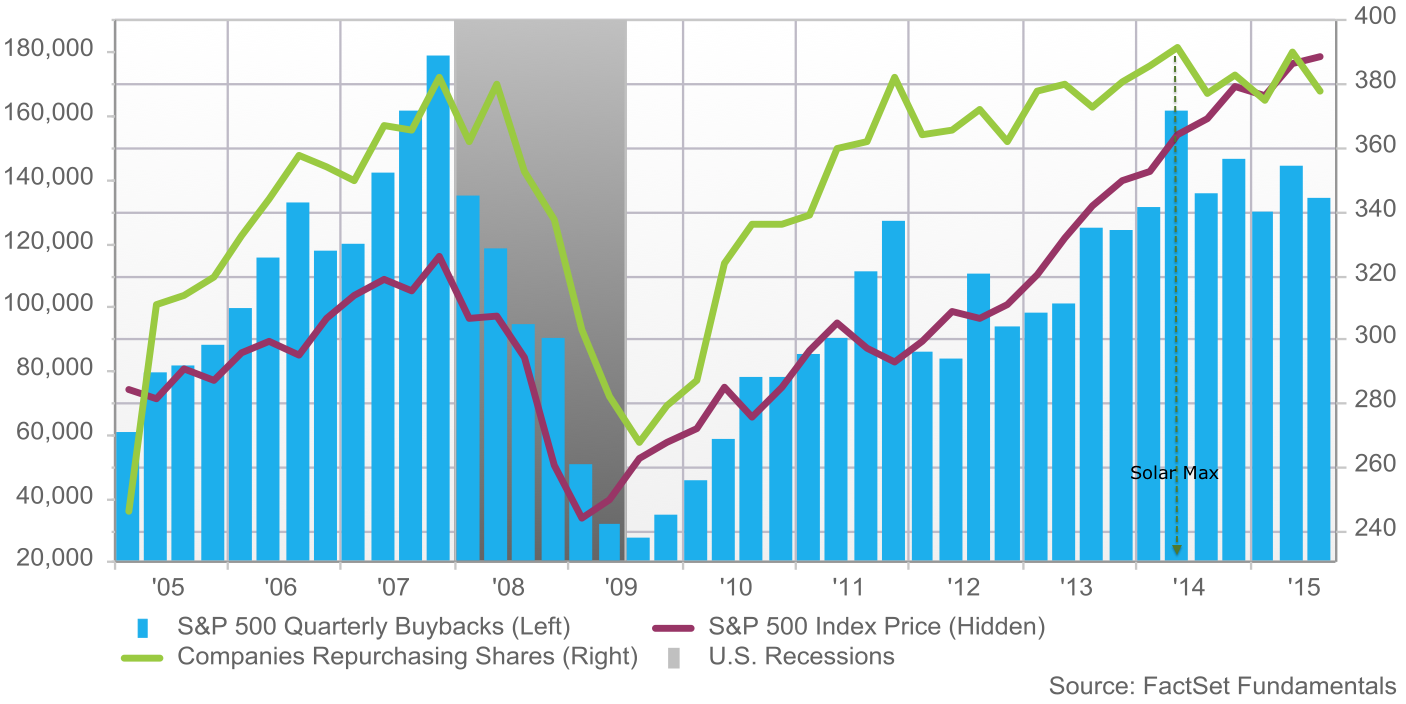

At this point I give negligible odds of the market resuming in a bull market and making new highs. Understand that we saw max saturation in terms of allocations, leverage and buybacks, whilst we have negative demographic trends in the major nations meaning a shrinking buyer pool. For prices to rally to new highs from here we would need to see allocations and leverage break to new collective records. The bursting of the mania that we just saw makes this very unlikely, plus buybacks peaked back with the solar max.

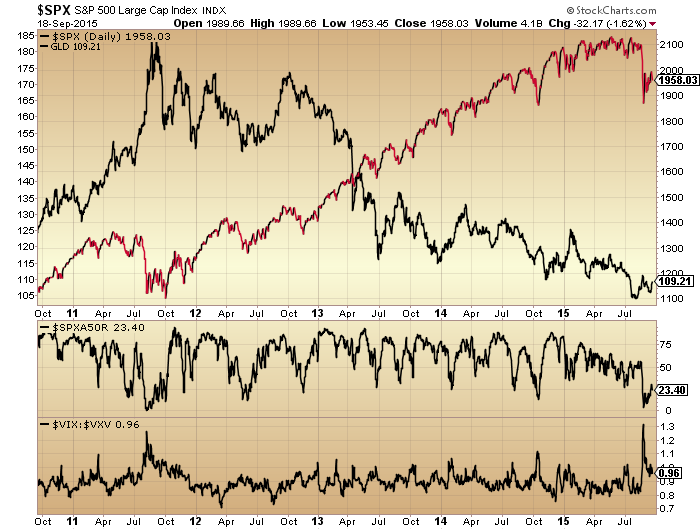

On the flip side of equities, gold and miners have been either basing or languishing: which one is yet unclear. Yesterday may have been a key day as they both rallied on the poor jobs number and did not then reverse, unlike equities. So, we see how they develop next week too.

Earnings season kicks off again this next week.

My positions:

Short Biotech – I see the mania as burst, the parabolic broken and the second chance done. Therefore, I expect hard and fast falls to resume here promptly.

Short R2K – the R2K reached its highest ever valuation at this peak and history suggests small caps should retrace their full gains under a bear.

Short Dow – more likely to hold up than the others but a lower high or sideways range trade are the most bullish outcomes that I can conceive.

Long Gold – has been unnervingly weak but I continue to believe it must be the beneficiary once stocks are more clearly cemented in a bear.

Long gold miners – new position as indicators depict washed out and positive divergence. A position on which I will rigidly use stops, however, due to uncertainty as to how this asset performs if stocks break lower.

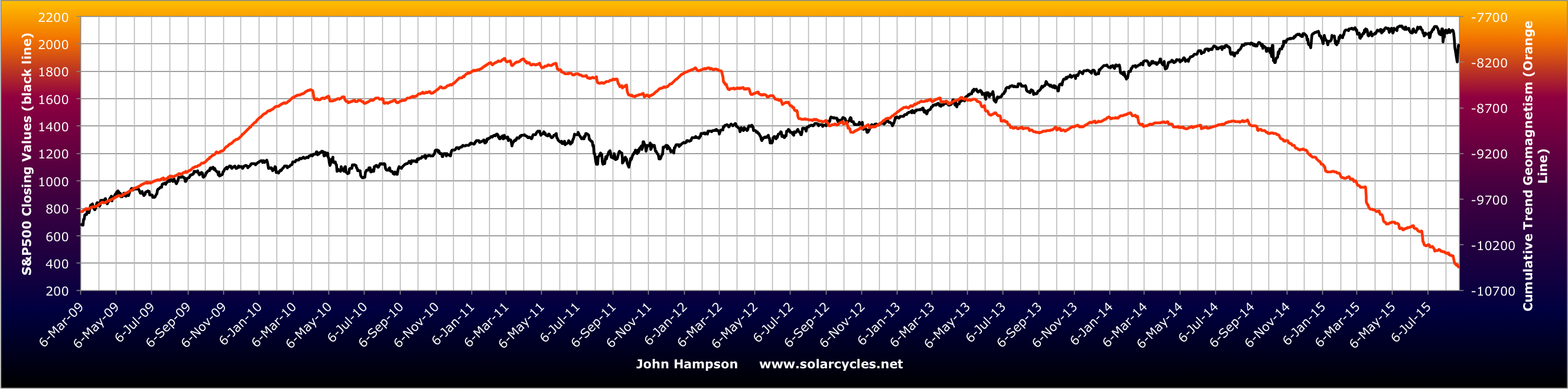

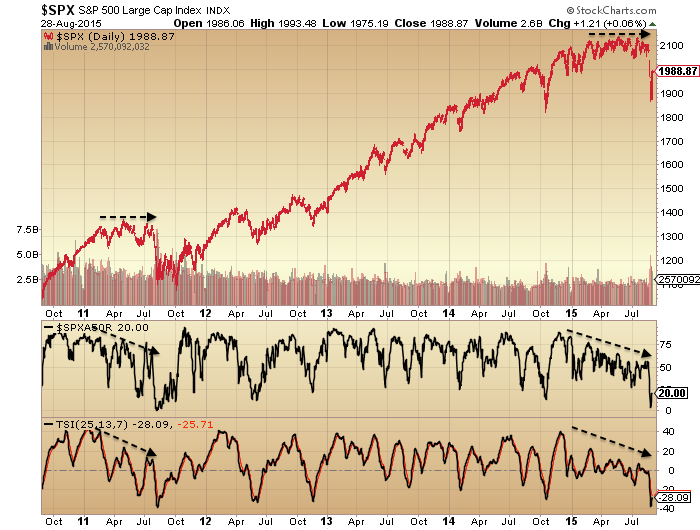

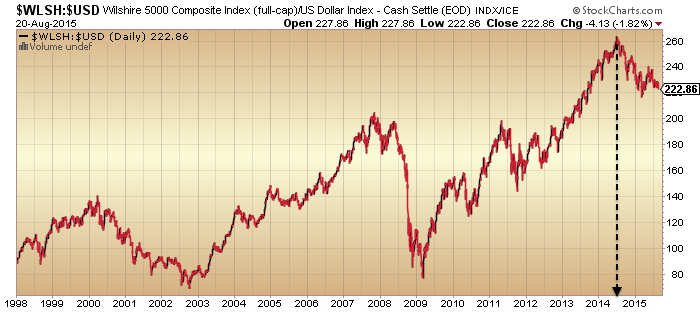

To finish here is US equities on a longer term view:

{kind=link}