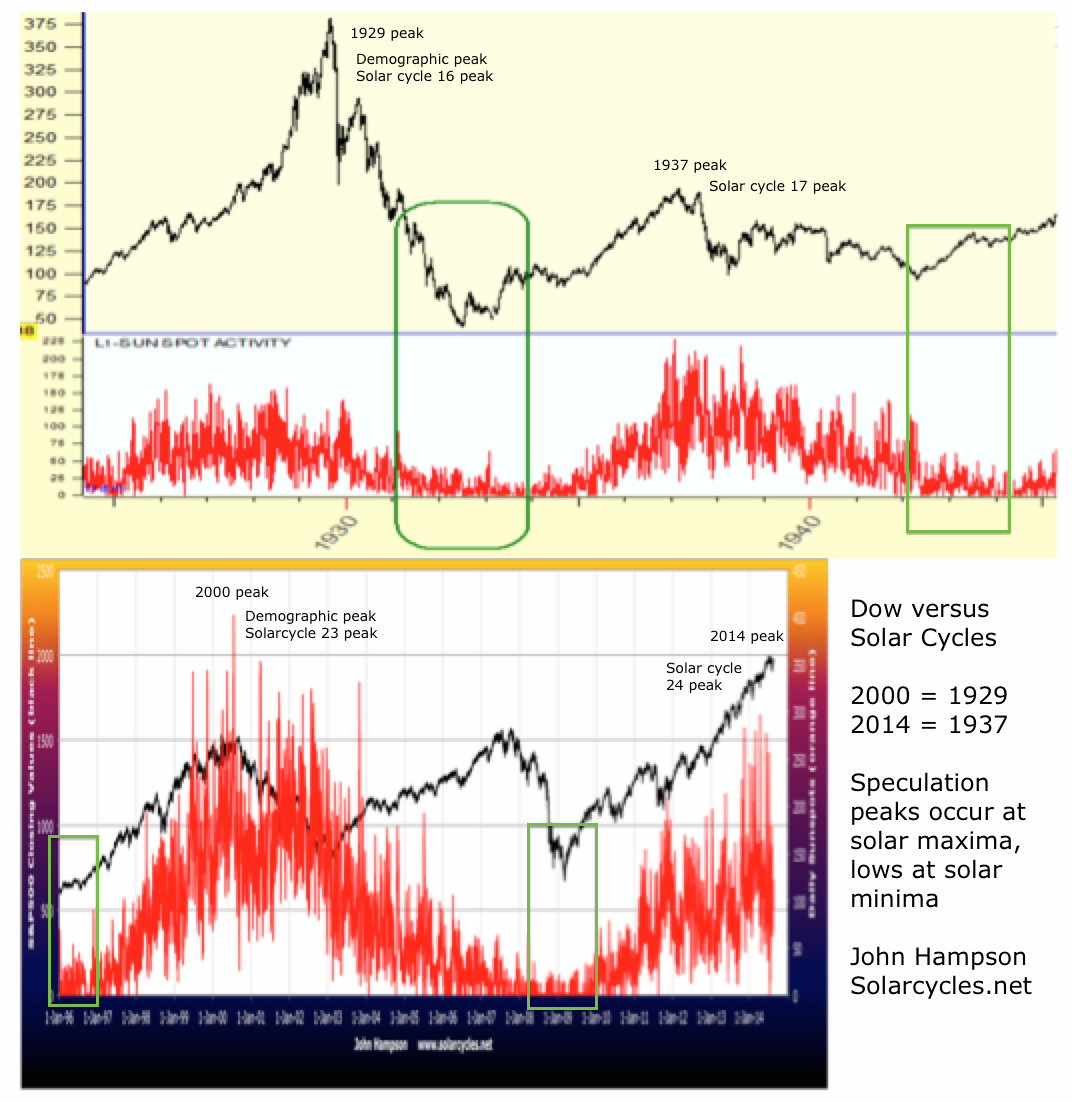

We have many historically reliable indicators of a major stock market peak in place: valuations, sentiment, allocations, leverage, negative divergences, risk-off money flows, all clustering around the smoothed solar maximum of April 2014. IMO, a compelling, cross-referenced real time test of the theory with too many angles all united as one, to question whether we are considering the wrong dominant cycle. If some other king cycle were at work with some peak in the future, then we would not have seen all those topping indicators and topping process characteristics coming to fruition in 2014. Rather, they would have only begun to form at at a later date. Therefore, there are only two possibilities in my eyes: either we are indeed seeing the last gasps of a topping process, or there is some other agent at work keeping price rising that is anomalous to historical peaks, namely the manipulation by a few big players fuelled by ZIRP-enabled leverage. With those two options in mind, here’s the latest picture:

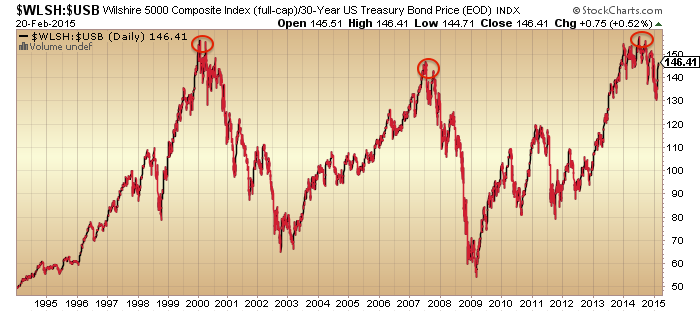

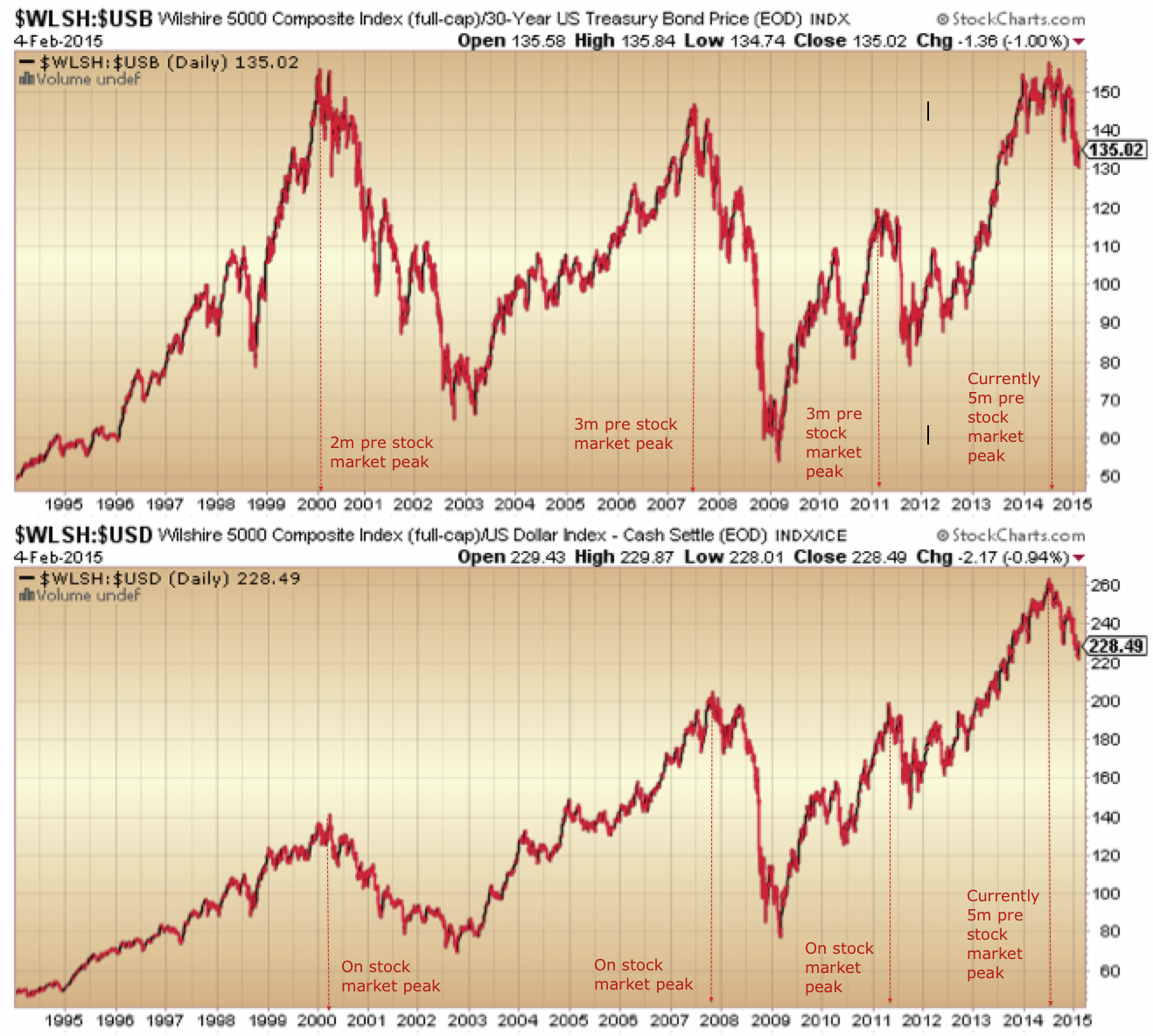

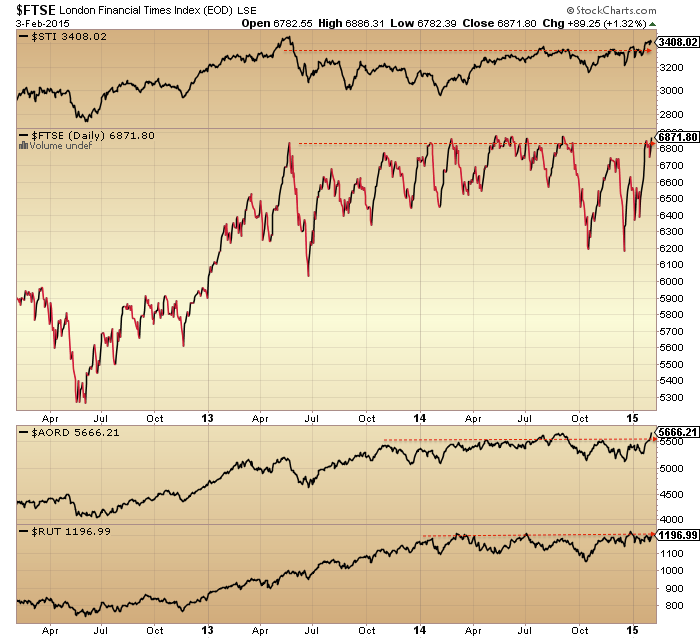

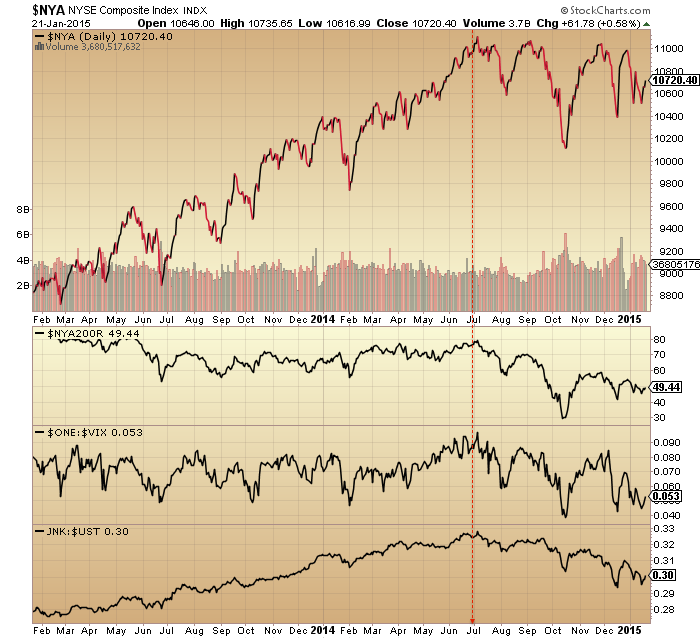

1. US stocks to bonds and stocks to dollar ratios have tentatively turned down again, maintaining the downtrend since, and real peak at, mid-2014:

Source: Stockcharts

Source: Stockcharts

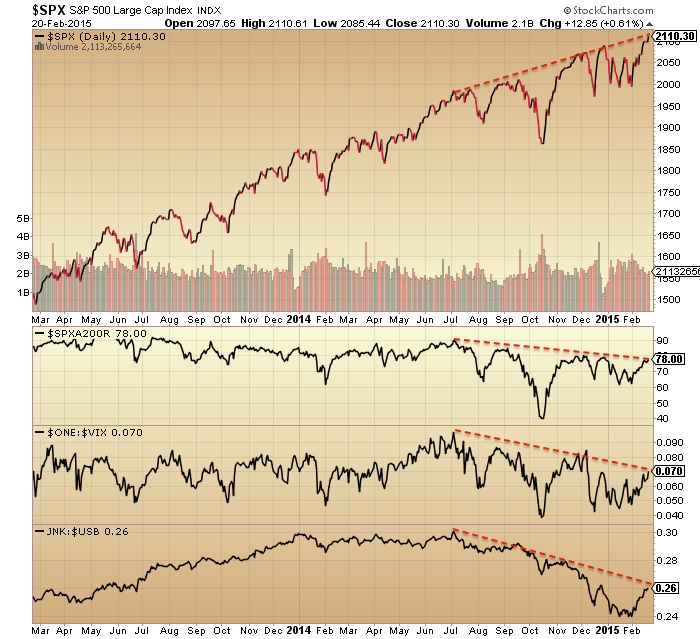

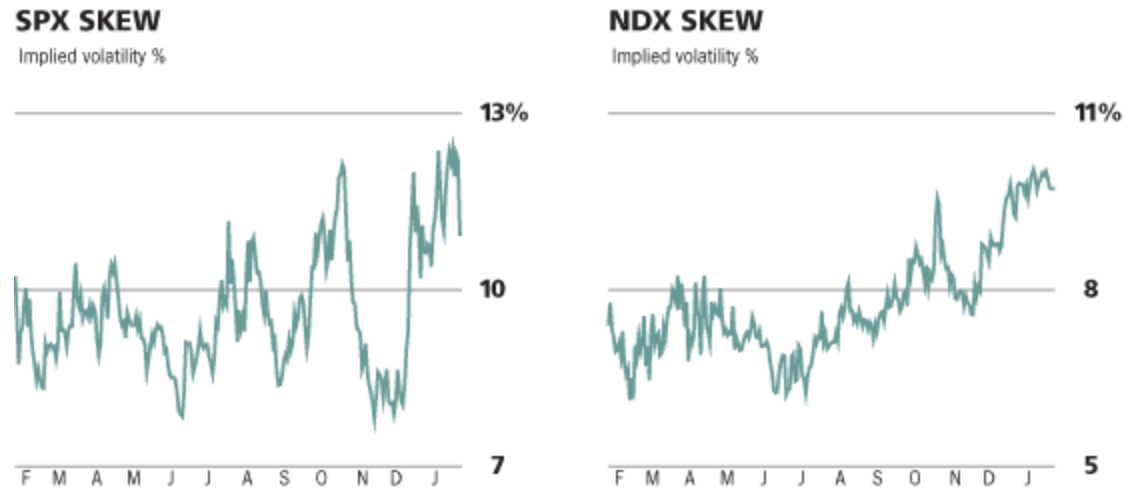

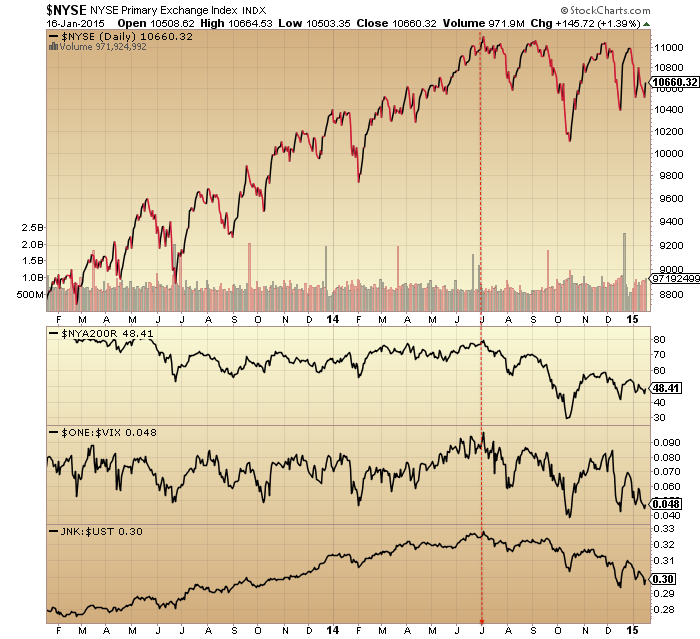

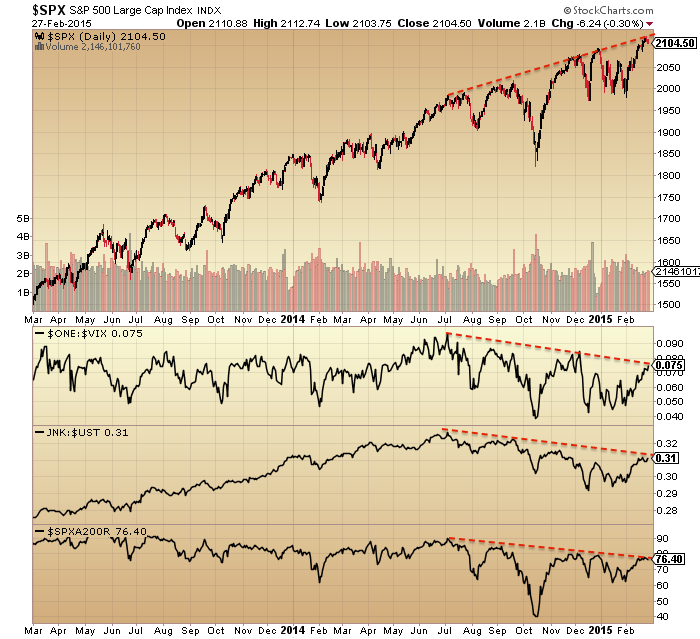

2. SP500 is at rising resistance, whilst volatility, breadth and risk-off divergent indicators are at downward resistance. An appropriate point for a turn if it is to occur.

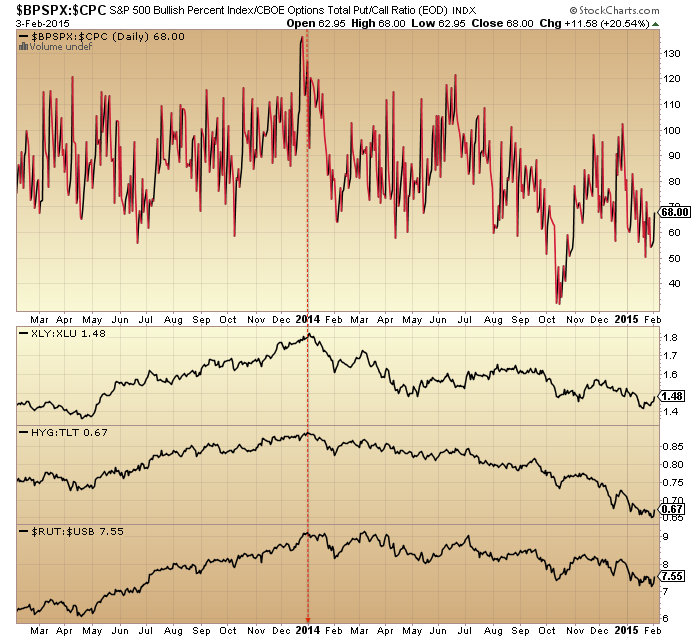

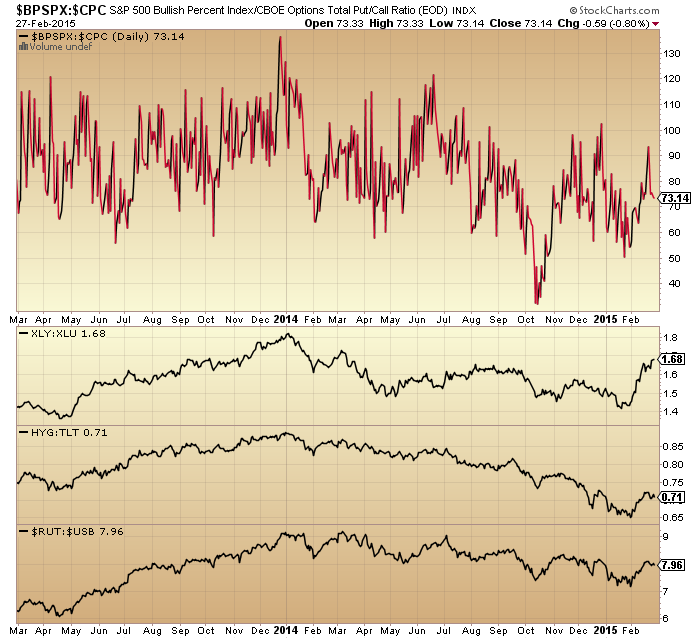

3. Four more risk-off measures below are in downtrends since the turn of 2014. Other than XLY:XLU they also give the appearance of turning down again at resistance now, keeping those downtrends in tact.

3. Four more risk-off measures below are in downtrends since the turn of 2014. Other than XLY:XLU they also give the appearance of turning down again at resistance now, keeping those downtrends in tact.

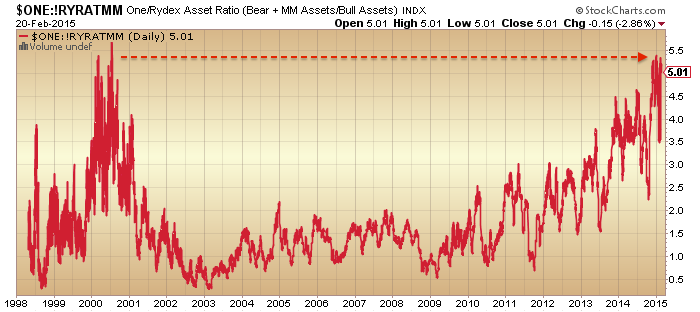

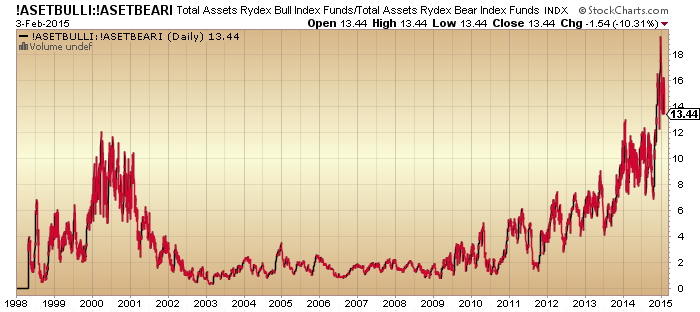

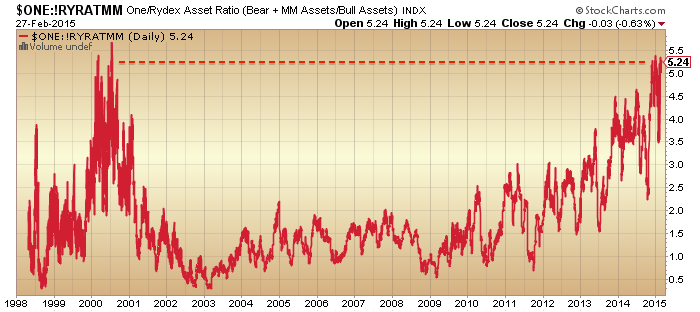

4. At the same time, Rydex allocations are back at their peak:

5. Plus, investors intelligence sentiment is also back at its peak:

5. Plus, investors intelligence sentiment is also back at its peak:

Source: Not_Jim_Cramer

Source: KingWorldNews

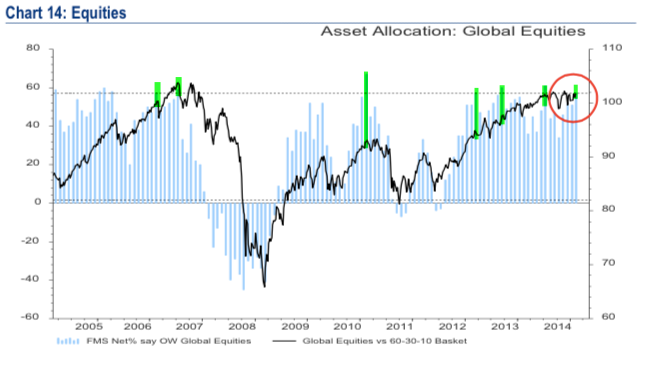

5. Fund manager allocations are back at their peak too:

Source: Fat-Pitch

Source: Fat-Pitch

6. And NAAIM exposure is also back testing all-time highs, with 99% long exposure currently.

All four of those sentiment/allocation angles suggest a correction should now come to pass, even if only short-lived or shallow. I’ve highlighted on the NAAIM chart that we previously saw NAAIM diverge before we saw a more significant correction – something to bear in mind.

All four of those sentiment/allocation angles suggest a correction should now come to pass, even if only short-lived or shallow. I’ve highlighted on the NAAIM chart that we previously saw NAAIM diverge before we saw a more significant correction – something to bear in mind.

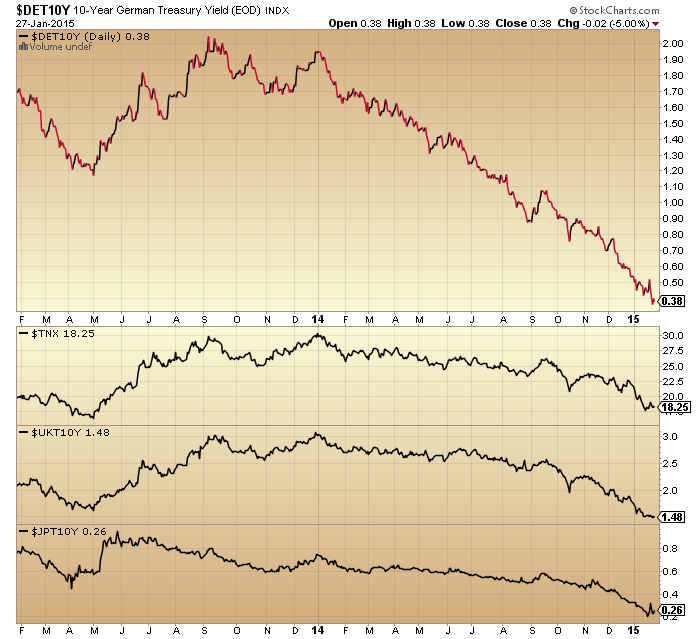

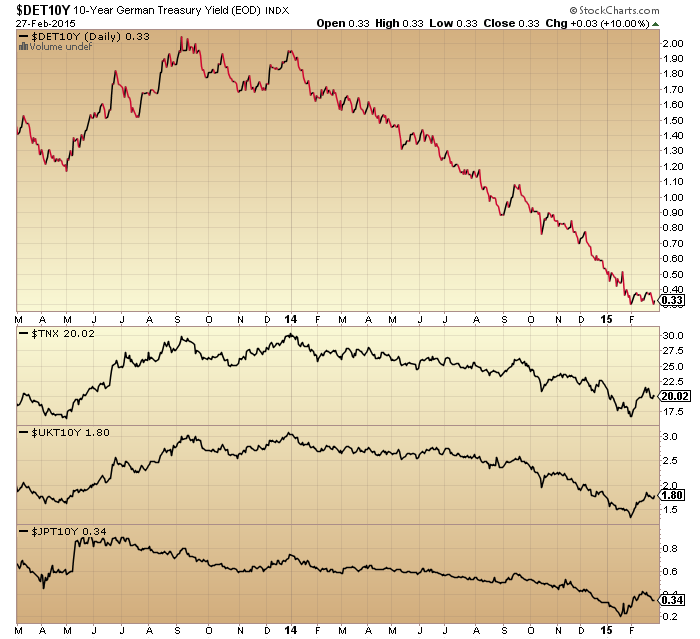

7. Bonds yields appear to be rolling over again, which would also fit with a stocks pullback.

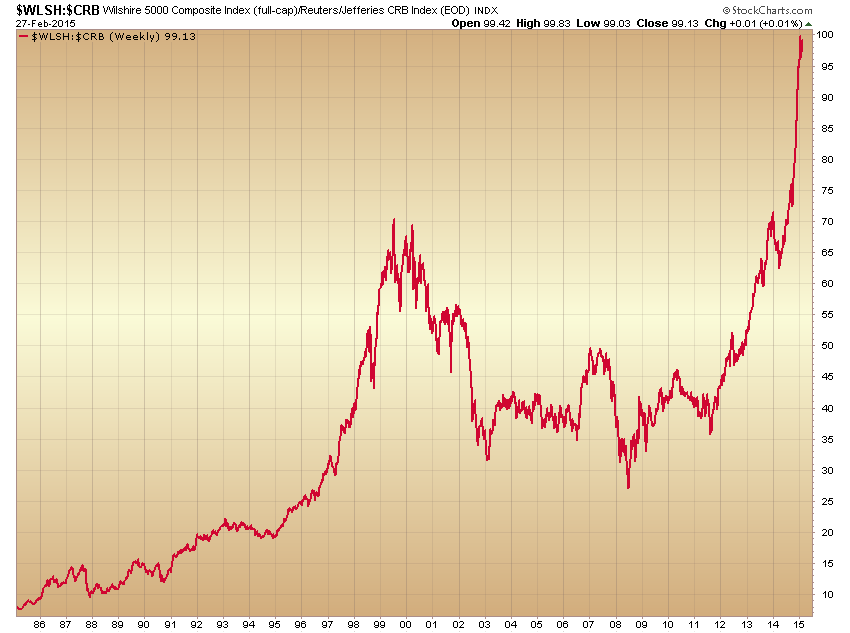

8. Stocks to commodities, suggested by Simo, looks exhaustive and ripe for reversal.

8. Stocks to commodities, suggested by Simo, looks exhaustive and ripe for reversal.

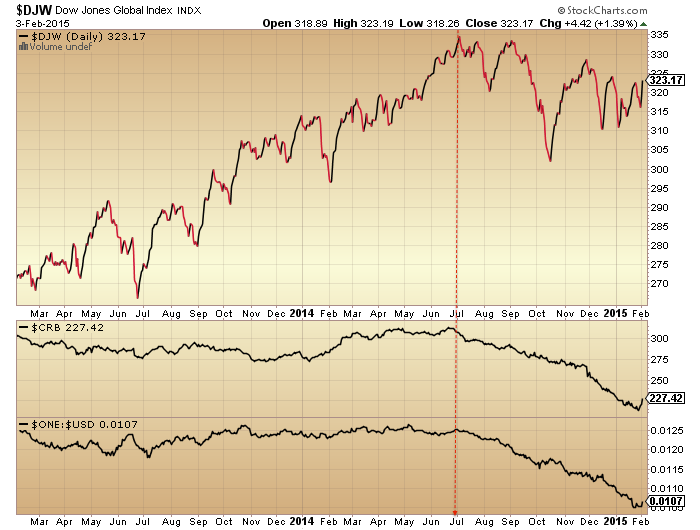

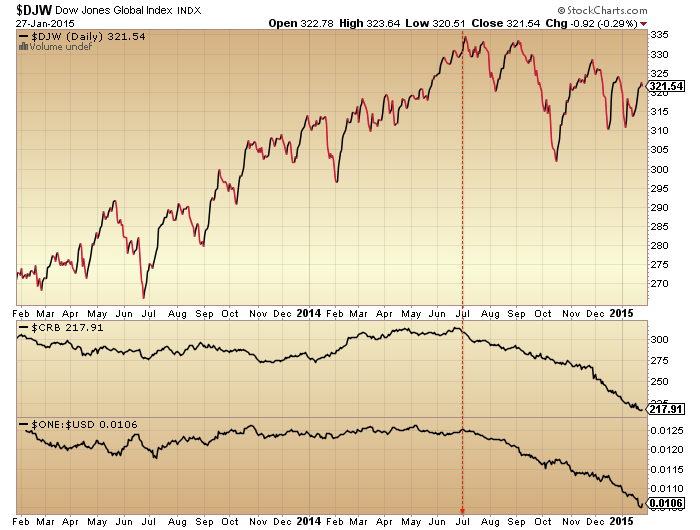

9. Margin debt declined in January, keeping the peak to date as February 2014. Meanwhile, leveraged loans have risen again and are well correlated to the Dow Jones World stock index, namely either at the end of a topping process or heading for new highs.

9. Margin debt declined in January, keeping the peak to date as February 2014. Meanwhile, leveraged loans have risen again and are well correlated to the Dow Jones World stock index, namely either at the end of a topping process or heading for new highs.

Source: DShort

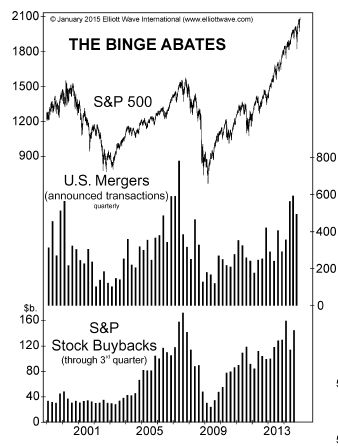

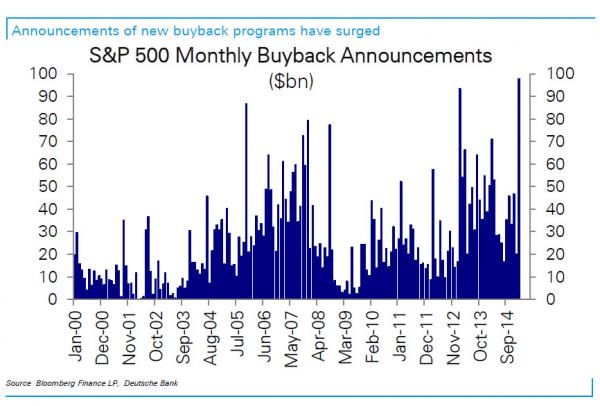

10. Buyback announcements, indicated by Allan, hit a new record. The previous spikes of start-2006 and mid-2013 corresponded to consolidation periods in the SP500, whilst the 2008 ones were contrarian.

Source: ZeroHedge

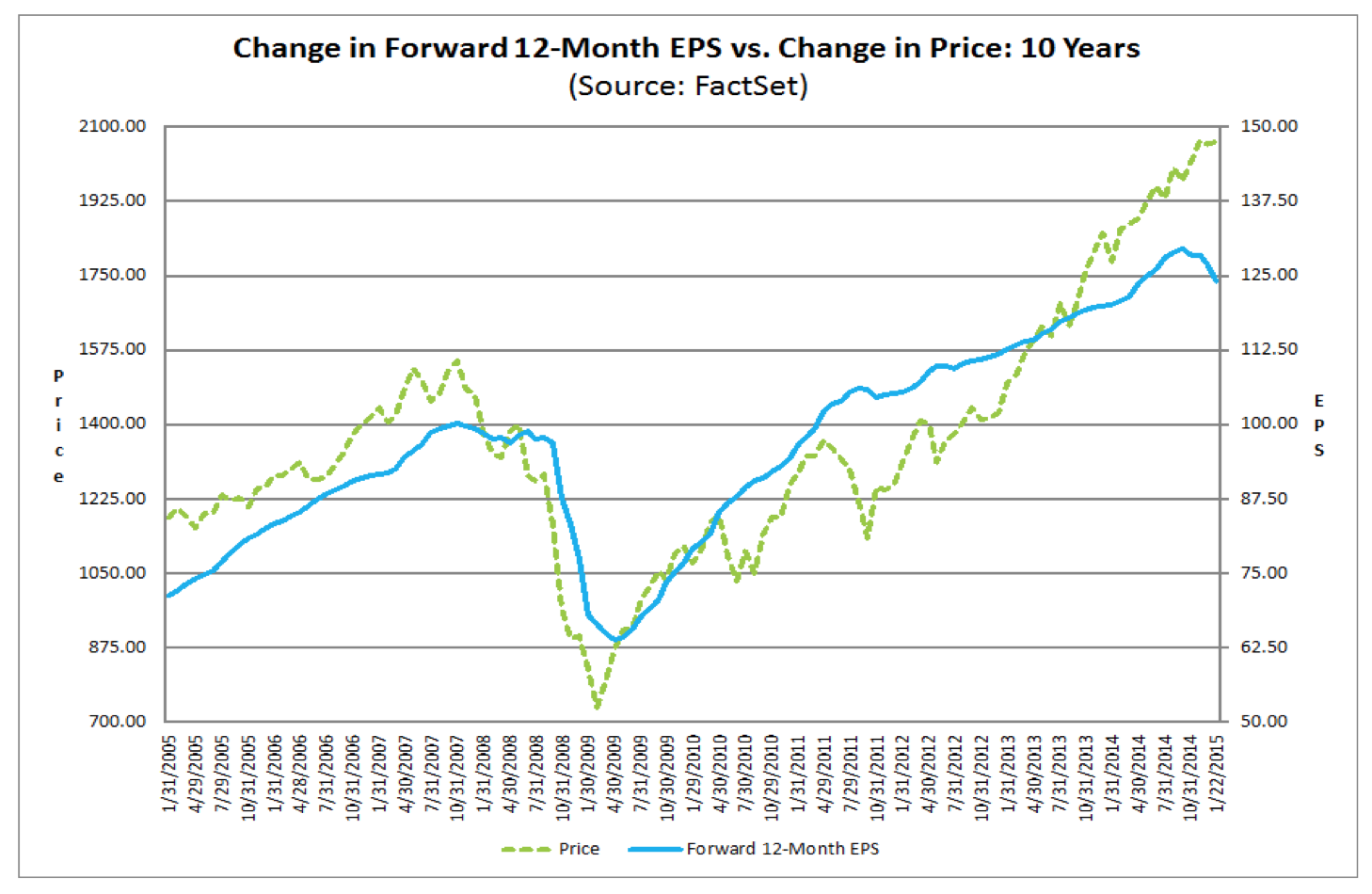

11. The negative divergence in earnings projections is shown in two ways here: arguing for a sharp correction in SP500 prices and the ushering in of a recession:

Source: Not_Jim_Cramer

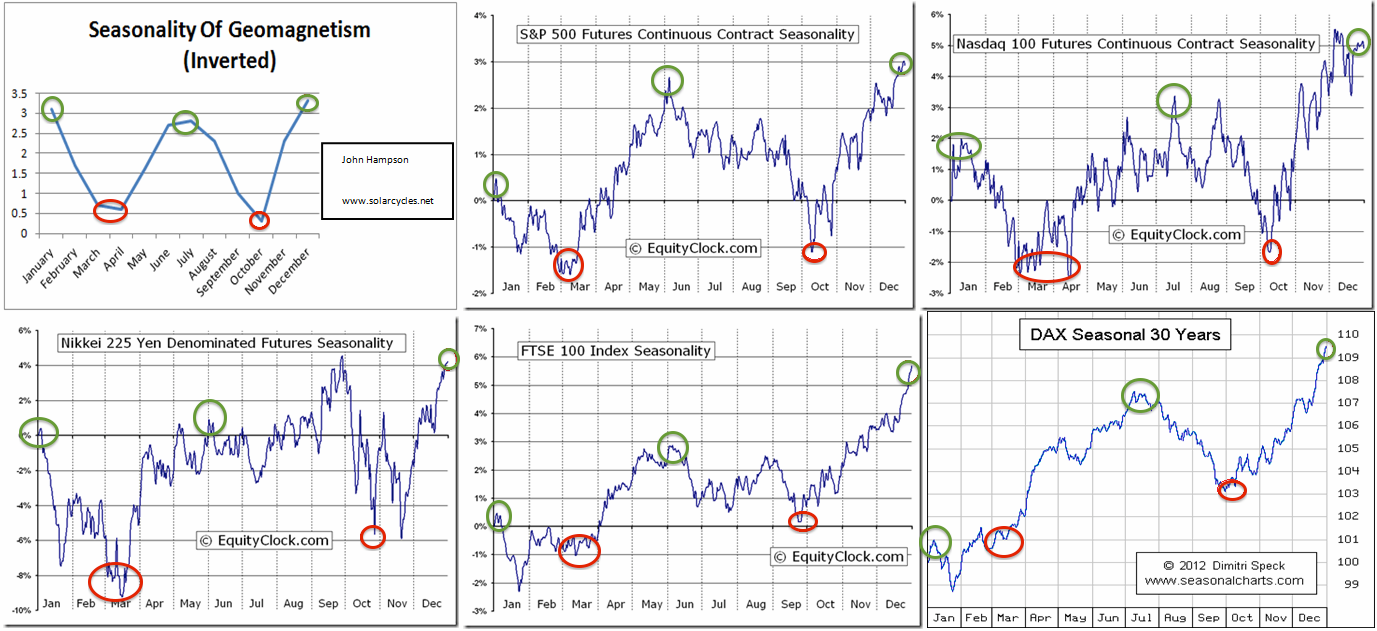

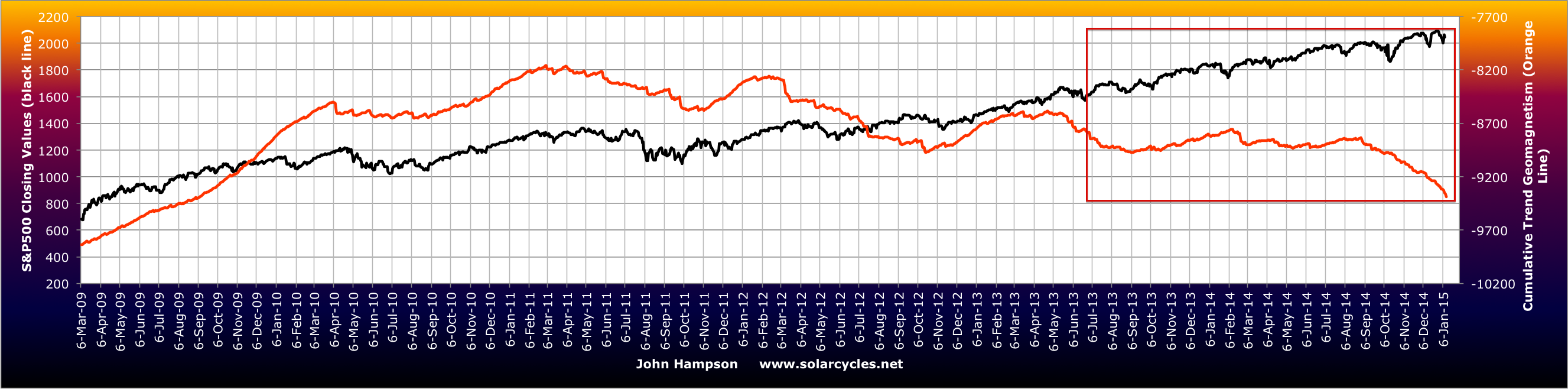

12. There is downward pressure into the full moon of March 5 and we have geomagnetic storming in progress:

Source: NOAA

In summary, the current saturation in sentiment, allocations and exposure, together with what appears to be a renewed roll-over in various risk-off, breadth and volatility measures, sets the scene for a price correction in stocks, assisted by the twin negative pressures of lunar phase and geomagnetism. The triple fundamental negatives of earnings, economic surprises and leading indicators provide the justification, and the potential short term basing in gold and exhaustion in the dollar both cross-reference.

A price correction in stocks may or may not be ‘significant’. Cumulative advance-declines and NAAIM trend would both argue that prices need yet to continue higher whilst both make renewed divergences. On the other hand, a host of other indicators continue to pin us at the very end of a topping process that is 12 months old.

I’m going to start a short position again tomorrow morning playing for this correction. I opened long gold again already. We’ll then see how it develops: short and/or shallow, or increasing in momentum and more significant. If there is no correction and stock prices march higher, then by a process of elimination we can increasingly point to the historically abnormal: the dark pools and primary dealers. However, even if we assume an abnormally large influence on their part, they are still logical and self-interested. The case is strong for a near term correction or consolidation.