It’s the start of the lunar negative fortnight today. I think this lunar downward pressure can be realised in price action in US equities, for these reasons.

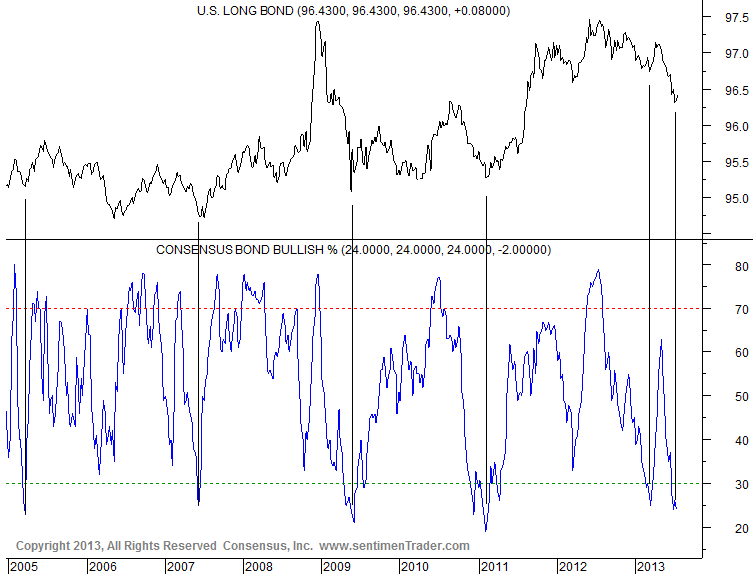

1. Bonds may put in a rally here. Yields look to be arching over.

Source: Sentimentrader

Source: Sentimentrader

2. Rydex equities involvement and sentiment at contrarian levels:

Source: Sentimentrader

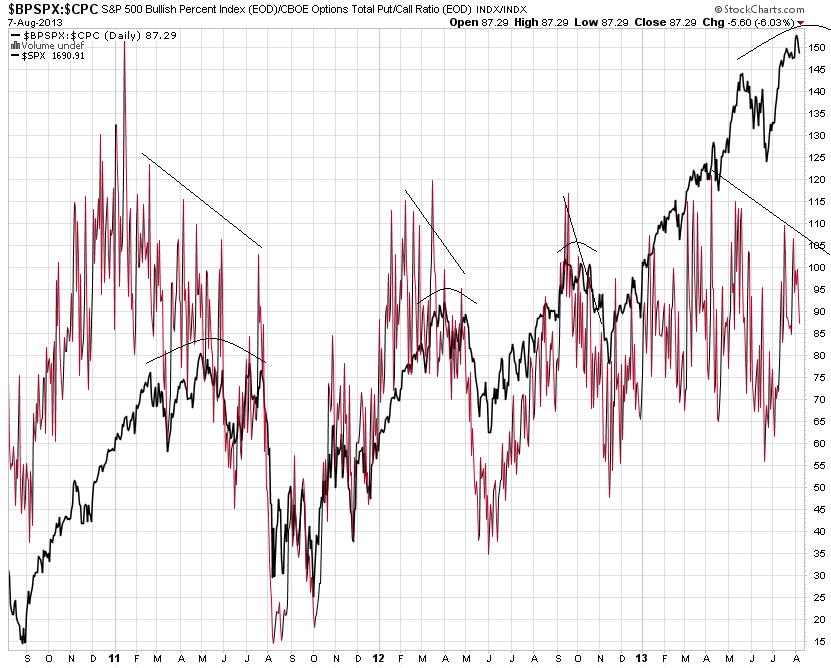

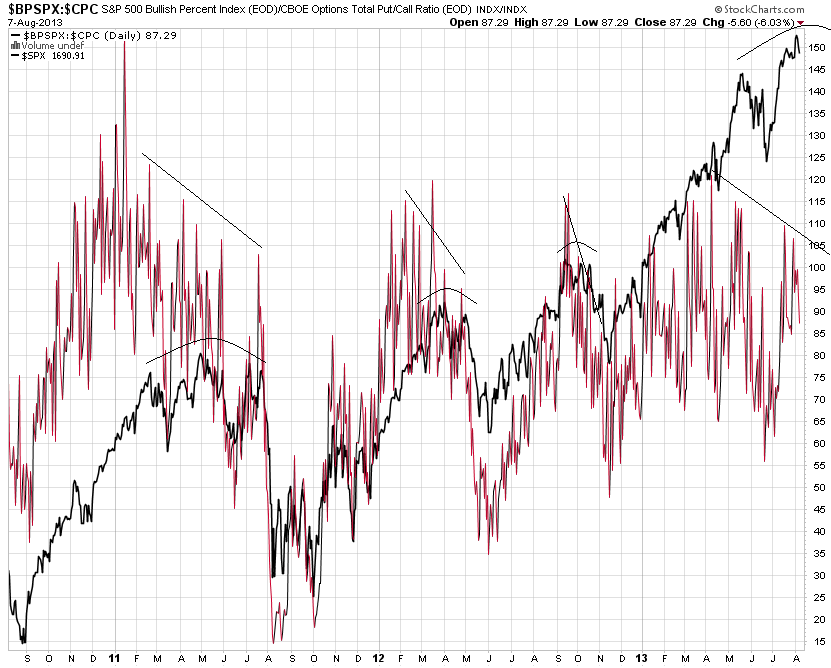

3. Diverging bullish percent over call put ratio – note the previous occurences here:

Source: Stockcharts

Source: Stockcharts

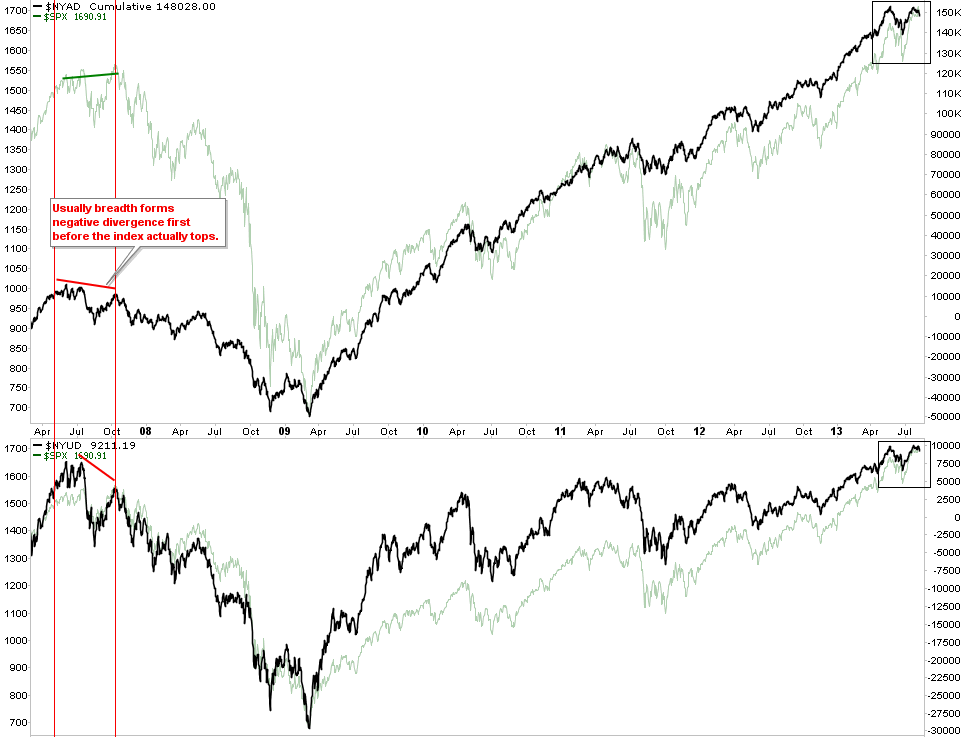

4. Breadth divergence. There are a few indicators showing this such as % stocks above 50MA, Mclellan Summation index, and, here, advance-declines (making a double top versus the higher high in equity prices):

Source: Cobra

Source: Cobra

No devastating decline in overall market internals. but enough to warrant a pullback. Countering this, the latest economic surprises, service PMI and manufacturing PMI, and overall earnings beat rate for the US have all been good. For a cyclical stock market top, we would need to start seeing some degradation in such data. However, if this is a topping process, then I expect we are only in the middle of it at this point, with a last push up to come ahead into September (assuming a decline can be realised over the next 2 weeks). By September I would then expect to see some macro reasons emerging to complete a topping process in equities.

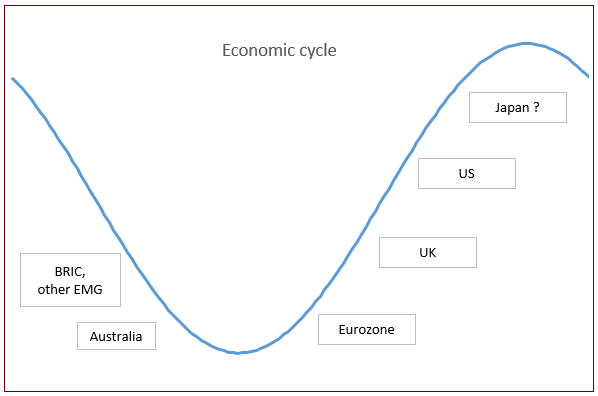

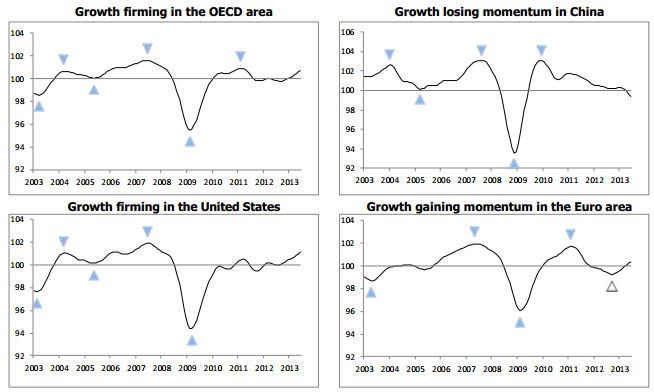

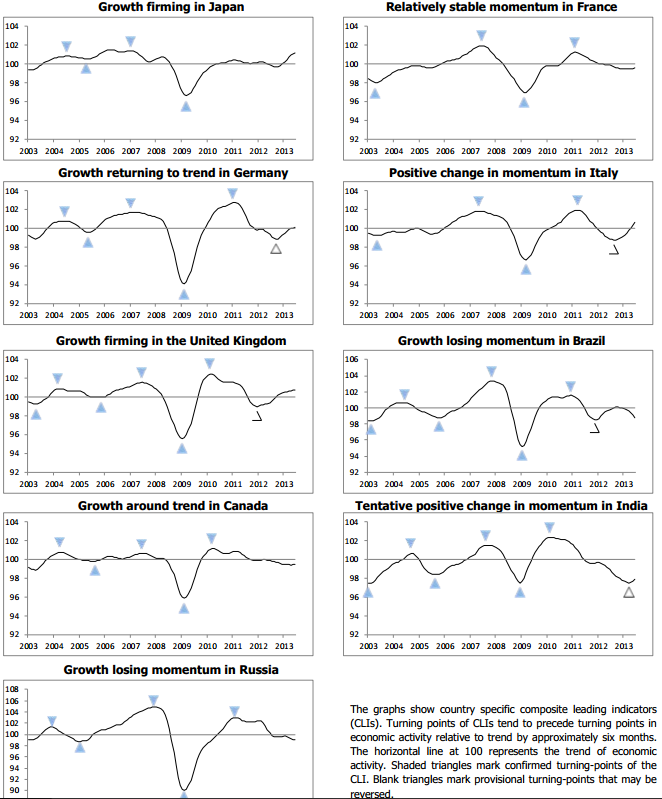

I have doubled my short position on the Dow today and have specifically tallked about and targeted US equities because of the current divergence around the globe. The latest Markit PMIs really showed a vast difference between emerging and developed economies. Sober Look suggests this spread in economic cycle positioning:

Source: SoberLook

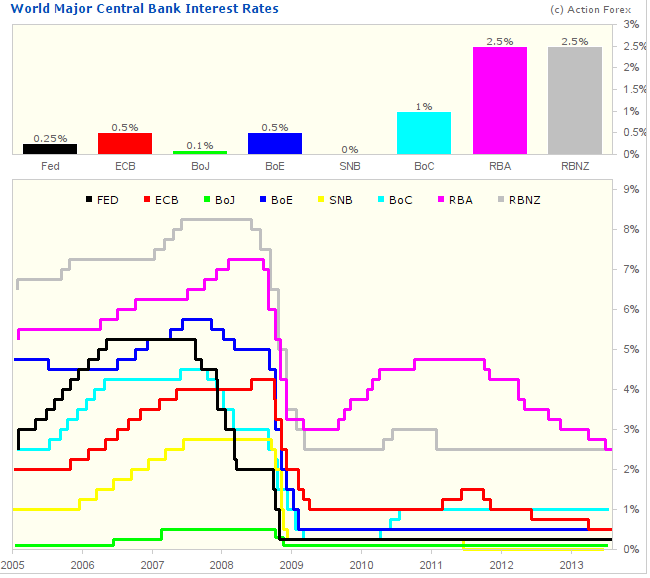

UK and Eurozone are looking particularly impressive and USA ticking along nicely. Australia has suffered since China lost momentum, and its central bank reduced rates again this week. This is the collective picture for the major central banks:

Source: Action Forex

Despite the QE tapering talk in the US, the graphic shows that we are still in an era of easing, with interest rate reduction still being pursued. As you know, I believe demographic trends are the source of the global economic weakness, ensuring we will be in an era of negligible rates for some time. Maybe the Fed will start to taper as early as next month, but I believe an end to QE and a renewed rate-increase policy will not be seen soon.

So, China has cracked, in my opinion, since its demographic trends reversed circa 2010. Those developing nations that boomed directly as China partners and those commodity-economies that benefitted from the long rising trends in commodity prices (through China demand) are currently suffering. This would include Brazil and Russia. India’s issues have been more internal and it needs reforms to help realise its demographic potential.

For most of the 2000s, this China plus emerging markets story was the fuel for the global economy, but now we are looking back towards the developed world to take the batton. Unfortunately, the US and Europe have significant demographic headwinds. I therefore don’t believe that we are now going to see sustained growth in the West. I continue to believe that either another rally in commodities will tip the world into a global recession, or the world is heading that way in a deflationary trend.

And that remains the key question for my account. Will my commodities longs prosper, or continue to sink? Right now, the commodities indices are potentially carving out a higher low than late June, which could spell an end to their downtrend. I believe this is the time for that to occur, because of my belief that equities are in a topping process. Historically they should now outperform and largely act as late cyclicals. I see this next month as critical for commodities. If they cannot make a higher low than June at this point, paricularly as the USD weakens, then it would look bearish for commodities.

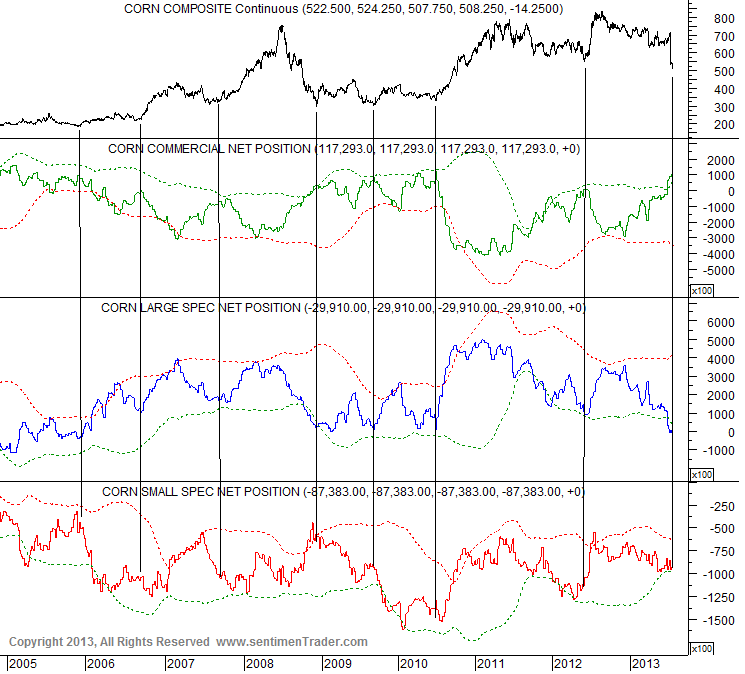

Here is corn, showing a potential rally set up.

Source: Sentimentrader

Source: Sentimentrader

And copper looks to be breaking out following a month-long basing pattern.

To draw the above themes together, can emerging markets strengthen into year-end, positively-infected by current developed economy performance? If so, the commodities rally would appear more likely. If on the other hand developed markets begin to join emerging economies in weakness, then a deflationary downdraft would be more likely. The wildcards remain the solar cycle (if the peak is ahead, then a speculative push in commodities could occur with increased geopolitical conflict an associated input) and climate (drought, flood and very high historical temperatures remain very much in play – it depends whether we see a devastating coming-together at the critical time and global location for agricultural crops).

OECD leading indicators just released today are more supportive to the first scenario of emerging markets strengthening and joining developed nations, with Russia stabilising and India improving:

Source: OECD

Source: OECD

Thanks, john,excellent stuff. Which level do you manage in the Dow. Me,at least 30% decline, as SP500 1980, to touch Monthly MM200.

At this point I am expecting just a small decline e.g. 5% to continue the topping range. The big drop to come later.

Hello John,

Why? ” lunar negative fortnight today”? why is it negative??

thanks

The influence of nocturnal illumination on human behaviour hardcoded over time. The period from 4 days after the new moon to 4 days after the full moon is typically one of lower stock market returns, relative to the opposite fortnight.

It’s important to remember that the lunar negative periods still have an overall positive expectation over the long term. So shorting them only works in specific circumstances.

These can be: seasonal weak period, market overbought, and so on. This is currently the case, so going short lunar red periods has good chances over the next couple of months. There is also a Hindenburg omen in place: http://albertarocks-ta-discussions.blogspot.com/2013/08/hindenburg-omen-fires-off-3rd-volley-in.html

And in my Chinese astrology cycles we are now in metal months, which have a history of producing declines in the stock market.

The lunar cycles have been working unusually well so far this year, http://lunatictrader.wordpress.com/performance/ , so I think we are also ready for what some people like to call “inversions”. They are more common near trend changes in the market. If this comes to pass, then I think we will be in a sideways market well into 2014. I think most commodities will also continue to be weak into 2014, just some occasional spikes and rallies.

Gabrielle, before we knew about gravity we only knew that the tides happened. The influence of moon phases on the stk mkt makes no scientific sense. However, as John says, there is a correlation. But it is like seasonality, it is weak and can be easily inverted. I’m skeptical of the nocturnal illumination theory.

Hello Kent, thanks for your answer. I run a financial astrology blog- and I know all about th eplanets’ influences. But I don’t know why did John define this fortnight negative…

Gabriella, what’s the address of your financial astrology blog? Would add you to my blog roll.

Interesting that China is talking of doing away with the one child

policy. They have caused such pain with it – for what.

They must understand the demographic consequences over the next 20 years.

I can only imagine they didn’t understand the demographic consequences.

Due to Mao, 20 + million people starved to death. All the missing population, may have stopped another round of that.

We remain in the decade (plus) bond and commodity bull market. Equities have a rude awakening, whether it come in nominal or real terms.

Stay true. Great information. Remember, it’s a long view, not a monthly view.

Thanks Sam

Excellent article once again, thank you John!

Thanks Yogi

combined 4/6 month cycles (planet/solar) have worked perfect for Norway since June

Going choppy sideways from here and into September

Range trading and decline in earnest as of late Sept would fit my expectations, thanks Jan

My Laundry T´s

The short one ended Aug 8. When drawing this way, SPX tend to top out a bit before, and so far it has.

If SPX still should make a higher high the coming days, I have a longer T that ends next week. However the same goes here – SPX should top out before the T-endingpoint, suggesting that the current high should be the one.

So could, but should not, make a marginally higher high the next days.

Then go near SPX 55ema ~1660, or break down lower, later in August.

But if we dont collapse, we get another T ending around mid-September… next FOMC ?

I have stated this many times. I think it is all random long term. Your strategy may work for a while and then it falls apart. =). Better just to focus on money management and how you scale in and scale out. Use a horizontal line =).

Good pt Robert. Most importantly money management. I have seen systems that worked even though the majority of trades were losses, but small ones. There have been a very few gurus with excellent long term records. Edson Gould, W. D. Gann, George Lindsay, Major LLB Angas, Hamilton Bolton, and Paul Dysart are the exceptions that prove the rule. Amazingly short list.

John, Good post. I like your charts, I’ve been looking at $CRB:$INDU compared to 2006-2008 Although no 2 markets are the same the cycle may need more bottom bouncing. At the same time I am wondering if the US market could be forming #2 of a 3 peaks & dome house. Which would mean range bound, drop and a final push up 2014 allowing more time for commodities to catch up. Another ratio I’ve been viewing $BPNYA:$TRIN weekly SMA and MACD divergence showing.

Paul. Ed Carlson who wrote the book on George Lindsay 3peaksdomed house says we already have a completed irregular 3P&DH. You can lookup his comments on http://www.themarketoracle.co.UK.

Good stuff John and commentators.

http://www.amateur-investor.net/AII_Weekend_AnalysisAug_10_13.htm

Thank you all.

I have updated all models this morning. The cumulative geomag model extends now to mid-Sept.

“… the young generation are anxious and eager to try their hands at SPECULATION. When they get into a RUN AWAY BULL MARKET, they have no more sense than to keep on BUYING. They throw caution to the wind. This increased BUYING power causes commodities to go to HEIGHTS UNWARRANTED BY SUPPLY AND DEMAND. The result is that when this BOOM is over, the young generation suffers severe LOSSESS, gets some valuable experience and is not so anxious to try it again.” Page 15-16 How to Make Profits Trading in Commodities by W.D. Gann 1942

Confidence “has been hard-wired into their DNA,” said Sharalyn Hartwell, executive director of Magid Generational Strategies, a unit of the Frank N. Magid Associates consulting firm. “It’s not that they’re young and dumb. They were taught, ‘Believe in yourselves.”’

And

Millennial optimism is not without its skeptics, however. Some experts say the generation’s hope could be an illusion, veiling the erosion of job security or fueling risky overconfidence. (skirted from Millenial Generation is Persistently Optimistic)

Thanks John

Watching and waiting. Bulls and bears doing battle in US stocks. Commodities look to have a higher low materialising but gold repelled again, for now, at 1350. Treasuries declined again and USD got some upward traction on ‘good enough’ retail sales to add weight to QE tapering as of Sept. That FOMC is 17/18 Sept so plenty of data to come out before then.

Break down in US stocks, adding to multi-month topping process look, as the marginal high on poorer breadth has been more cemented. Break out for gold, following silver, and higher low in commodities index looks firmer, plus USD weak. So things looking more promising for late cyclical commodities outperformance as equities make a top, but still tentative. Geomag storm in progress currently. Full moon and end of lunar neg period both next week – I will be looking then at possible trade changes.

:You have the solar energy cycle factor plus the negative demographic effect. Have you considered adding the energy aspect (oil peaking historically and the high cost of fracking). Combining all these looks a bit more “doomish”.

Peak resources – versus – exponential technological evolution. Difficult to call. Extrapolating resource usage trends features on my Timetables page, but technological paradigm shifts will change this, e.g. more efficient alternative energy, factory grown food, nanotech.