Time to look at what has been invalidated from my Q1 analysis.

I am no permabear. I played equities long-only from 2009 through to 2013 but by the end of 2013 there was an impressive congregation of topping indicators, which aligned with a predicted peak in the solar cycle. Adding in my demographic research, the case was particularly compelling to short stocks and hunt for a major peak. So I decisively switched teams. That compelling bearish case still stands, as just a couple of weeks ago I produced a list of 30 indicators advocating short. See that list here.

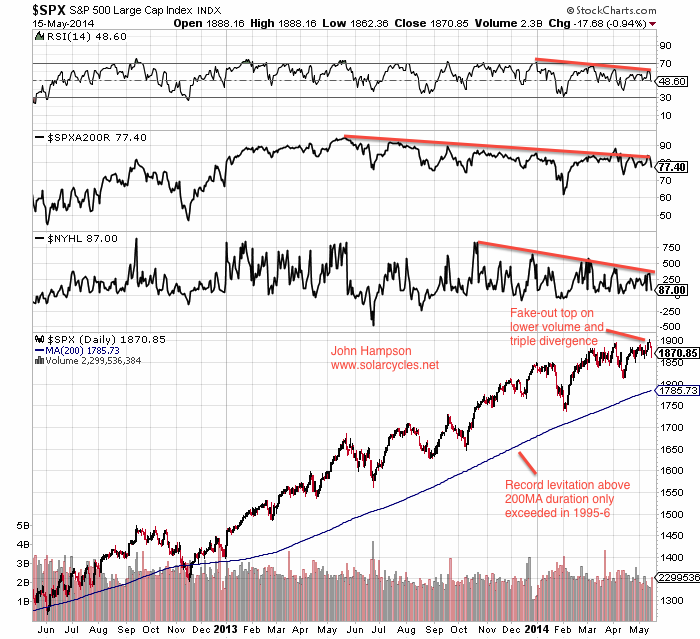

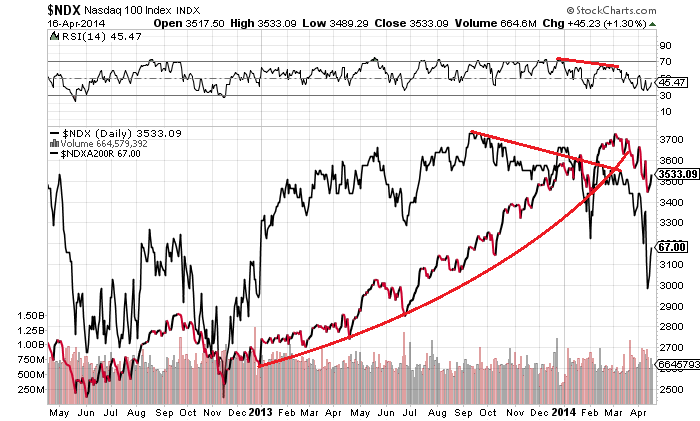

In short, focussing on US stock indices, whether we look at valuations, bull market characteristics, sentiment, euphoria, leverage, IPOs, equity allocations, smart money flows, breadth divergences and other indicators with reliable histories, we have a case for a top in US equities. Add them all together, and it’s just about the timing. Therefore I don’t understand shorters throwing in the towel at this point, and particularly because as things stand, US stock indices have traded sideways in 2014. There is no definitive bull or bear trend, and at the time of writing 3 of the 4 main US indices are below their Dec 31 close, whilst only marginally so. Price has only paid for short term trading over the last 4 months, and the rest of us are patiently – or impatiently – waiting. Pending that resolution, beware the price-cheerleading from both bull and bear camps, thinly disguised as analysis.

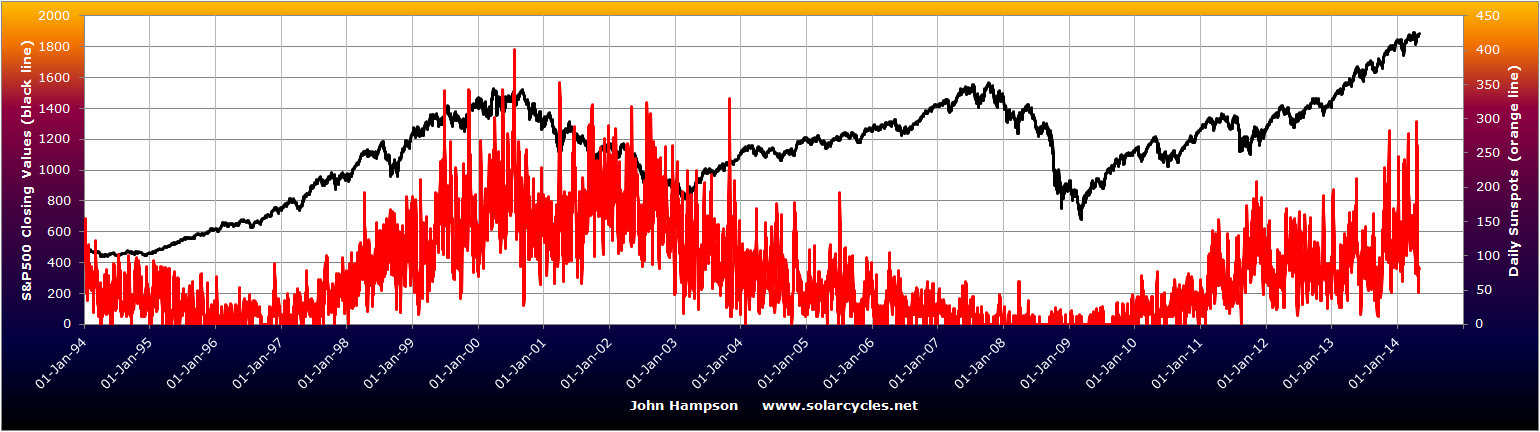

So, with that multi-angled case for a top, why have stocks not fallen decisively yet? I argue that the reason is the solar cycle maximum extending beyond the predictions of the major solar scientists, and its implication on speculation in the markets.

Therefore, my anticipated waterfall declines in March and April and analog aggregation did not happen:

However, by indicator extremes and similarities, the set up remains for a crash in the markets and the delivery of those waterfall declines as the peak leverage is unwound. But, for now, the stock indices have morphed into sideways ranges, as the solar maximum has extended. The solar maximum, through human excitement, influences speculation and also economic activity. Once the solar maximum begins to wane I expect both to ebb together, and I therefore consider this one of the most important items to track.

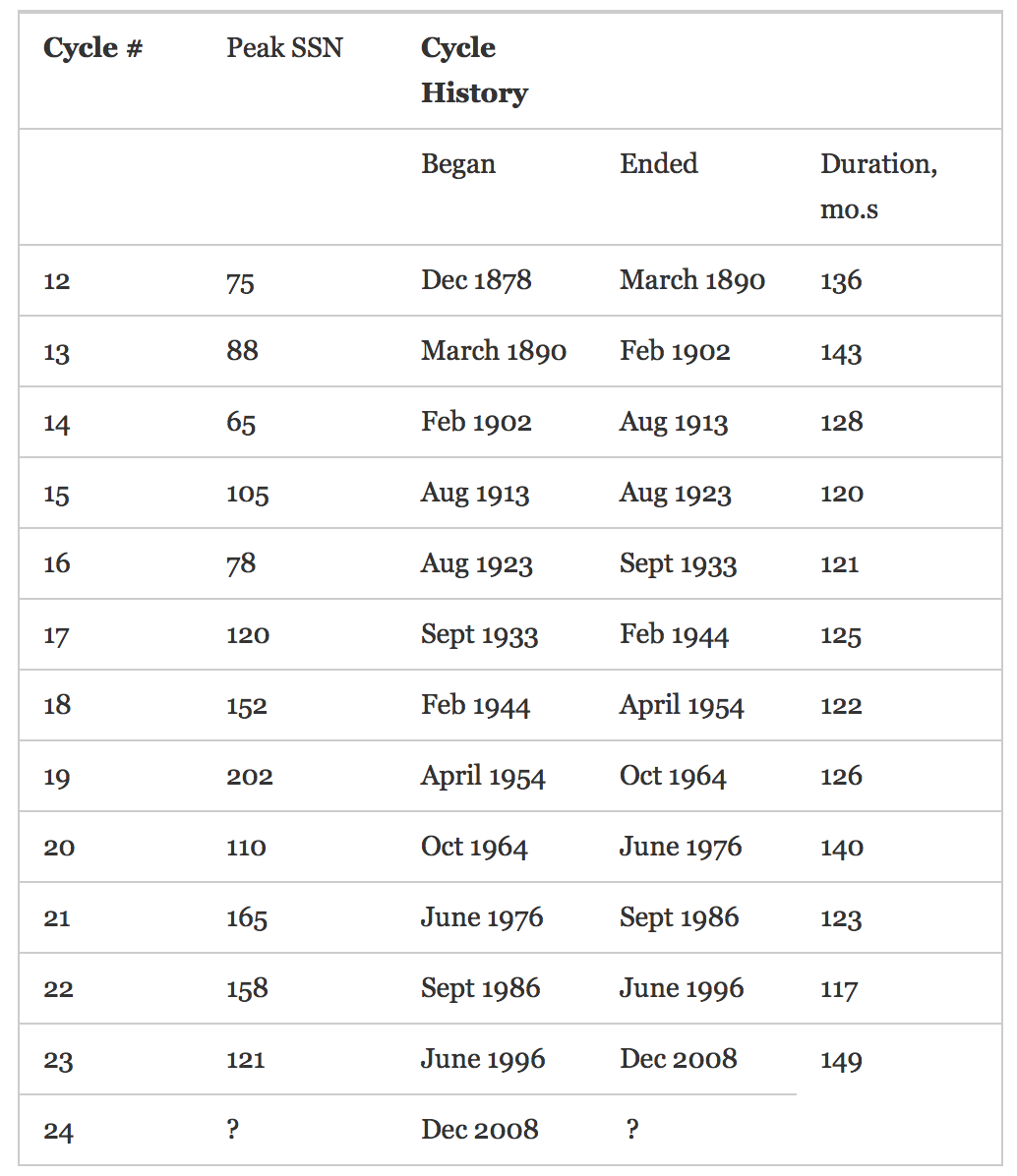

Should the solar maximum not peak out until mid-2014 then I would look to the possible analogs of 2011 and 1987 as price guides. Both these analogs shared similar indicator extreme readings and backdrops, and both saw waterfall declines in the Fall/Autumn. 2011 produced a long sideways range ahead of the falls, whilst 1987 eked out further price gains in the summer, before the falls. My approach is to stay short and attack short until we see the major declines, shearing off profits as I see fit based on the short term action, and should stocks eke out further new highs before the falls, as per 1987, then my current exposure can cope with that.

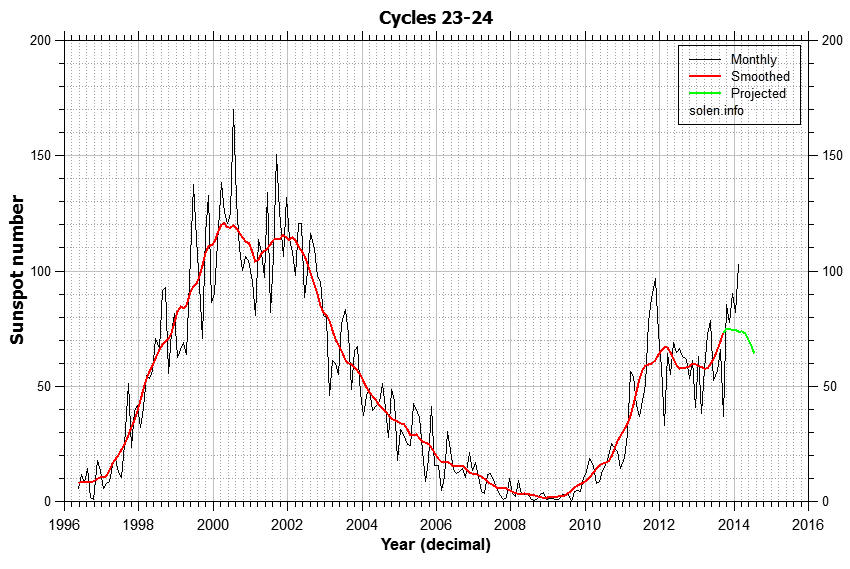

Should the smoothed solar maximum be behind us, and sunspots wane from here, then those Q1 2014 trading ranges in the indices may turn out retrospectively to be the beginning of a new downtrend, made clear by imminent sharp falls (declines from here would fit the Presidential cycle). In support of that possibility, my January call that the Dow and Nikkei peaked 31 Dec still stands at the time of writing, and my March 2 call that the Russell 2000 and Biotech sector peaked out around last day of Feb is so far accurate.

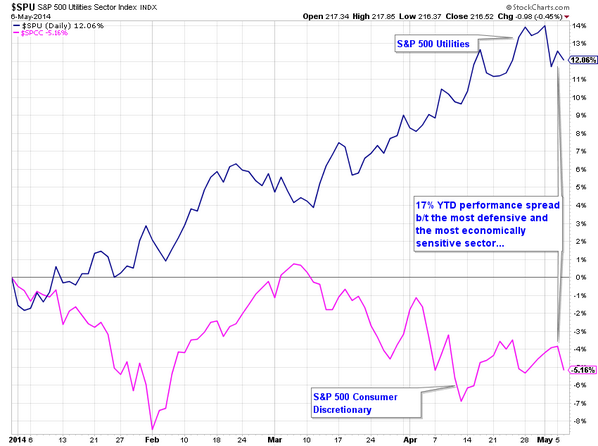

From a bullish perspective, cumulative advance-declines continue to support, and cyclical sectors recovered after their January sell-off. Gold and miners have fallen back since mid-March. Leading indicators suggest a pick up in global industrial production as of mid-May, so that could become a tailwind if stocks do not significantly sell off over the next couple of weeks. Q1 earnings are projected to produce an overall decrease in earnings, for the first quarter in some time, but thus far we do not see overall bearish price reaction to those that have reported. Economically, we do not yet see the tip into outright deflation or negative growth, but I expect that to come hand in hand with the stock market declines post-solar-maximum, i.e. sharp stock market declines will affect the economy and vice versa, all guided by the sun’s influence on people.

My Q1 2014 ‘misses’ in terms of analysis can be summed up as impatience over the sharp falls into a definitive bear trend, but I believe the reason for that is the extension of the solar maximum, which was unknown at the time. The bulk of my analysis still stands, and will continue to do so until that definitive selling erupts.

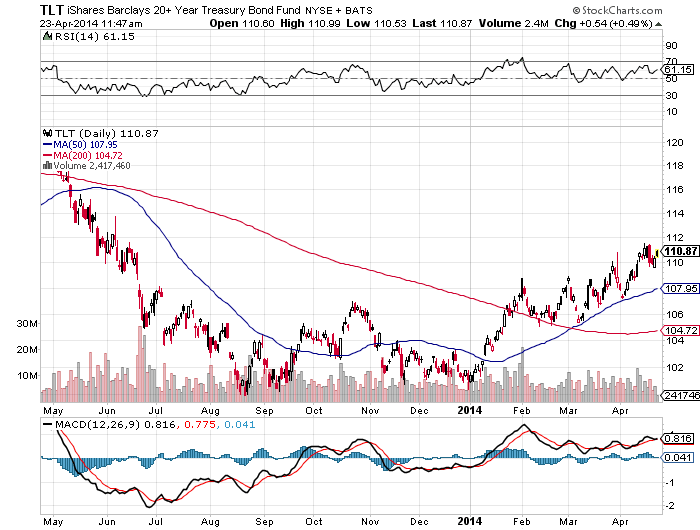

In the near term I am looking at market reaction to earnings, how price behaves into the new moon at the end of April, and the indicator reports at the turn of April-May for sunspots, margin debt, and more. I am adding short into the stock market rallies, such as this 6-day rally into today, looking to short term indicators for overbought/exhaustion. I am also watching commodities to see if they can continue to rally as a late cyclical class (considering gold separate) which typifies a top, but I have been taking profits on commodities positions as I have my doubts about the longevity of their rally due to deflationary/recessionary pressures. Potentially reflecting such pressures, treasuries have continued to perform since their turn-up as of the start of January and are another clue into what lies ahead.