Time for a more in-depth post.

1. SOLAR CYCLES

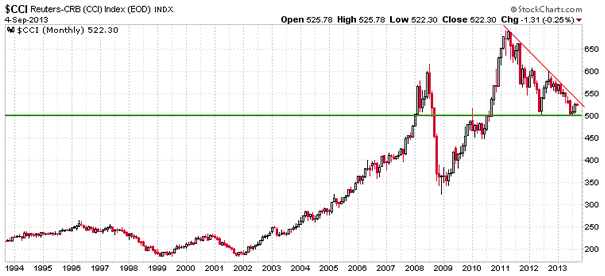

By my work the secular (more accurately demographic or anti-demographic) asset class should be bid to a peak in a solar-inspired speculation blow-off close to the solar maximum, which for this solar peak should be commodities to round off a decade long (plus) bull market. If the smoothed solar max has passed and was Feb 2012 and the CCI commodities index made its ultimate peak April/May 2011 then neither should now be exceeded. If this turns out to be the case in hindsight, once the solar max has been agreed, then the commodities peak would have occurred 9 months prior to the solar peak and would within normal parameters to continue to validate the theory.

Source: Gary Tanashian / Stockcharts

If, alternatively, the solar peak is ahead late 2013 into early 2014 (which is SIDC’s second option, and also Leif Svalgaard’s prediction – shown below), then that 2011 CCI peak is too far away and if the theory is correct we should get another commodities peak closer to the solar peak, which would mean a higher peak in the CCI ahead. We have the possible seed for this in a fledgling CCI uptrend following a base established in July/Aug 2013 together with their historic performance as late cyclicals in what is possibly a cyclical topping process in equities occurring. However, this CCI uptrend is currently tentative, devoid of momentum and without broad participation thus far. The dips in oil and precious metals at the end of this week cast further doubt for now, but their drops coincided with money flowing back into equities. If equities are in a topping process then money should flow back to commodities in due course as they go outperform as late cyclicals. I would suggest the higher peak in CCI to be possible as speculative money pours in, under these easy money conditions globally. ZIRP and QE may not be able to generate growth but they can generate bubbles.

Source: Leif Svalgaard / WattsUpWithThat

Source: Leif Svalgaard / WattsUpWithThat

If the first alternative turns out correct, and both the solar peak and commodities peak are behind us, then historically we have seen a new long term bull market in equities underway at this point, and the current easy money conditions could spell big momentum into equities (which would be the polar opposite to the second alternative of equities in a new bear and commoditites sharply rising, thus vital to call correctly). However, my demographic research shows that this is unlikely to be the case, at least not yet, as the positive demographic support for a new global secular stocks bull is absent. Indeed, the collective demographic trends of the major economies, bar Japan, are in an unprecedented collective downtrend.

2. DEMOGRAPHICS

This brings me to the question of whether central bank policy actions have been aggressive and potent enough to compensate for demographic headwinds. If that were to be the case then perhaps an enduring stocks bull and sticking economic growth could be achieved, albeit only whilst ZIRP and QE are maintained. I can very much recommend a read of the next link, which nicely summarises what QE can and can’t do and what Japan’s most-aggressive-to-date QE is likely to achieve:

http://www.scribd.com/doc/137092515/Richard-Koo-Quantitative-and-Qualitative-Easing-2013-04-16

In a nutshell, QE and ZIRP aren’t that potent as they cannot force people and companies to borrow or spend or invest. In the 1990s Japan tried to offset demographic downtrends with QE and ultra low rates and other stimulus tools. Even though most of the major economies were in demographic uptrends in that period (with booming asset markets and economies), this positive global environment AND these central bank actions were not enough to get people and companies to borrow, spend or invest.

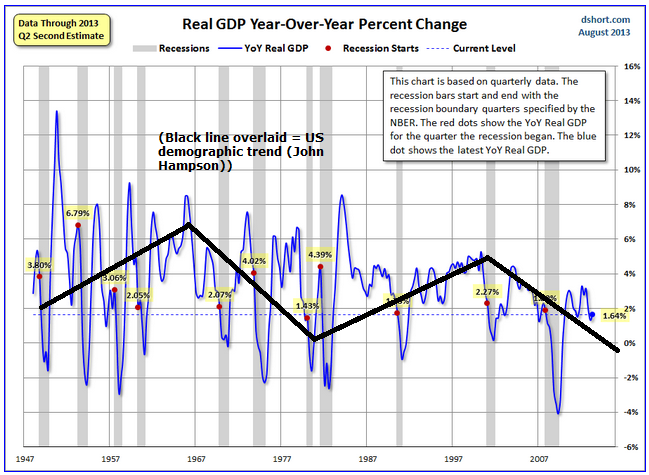

I have overlaid the overall US demographic trend against Doug Short’s real US GDP growth chart here:

Underlying Source: Dshort

The yellow dots reveal that real US GDP is currently lower than any previous recession start point. I suggest this shows the relative impotence of QE and ZIRP, and would argue that the demographic downtrend which should be in place for the bulk of this decade, suggests that real GDP growth level should fall negative again in the near future and another recession kick in. The question is whether this occurs with or without the tipping help of a speculative rally in commodities.

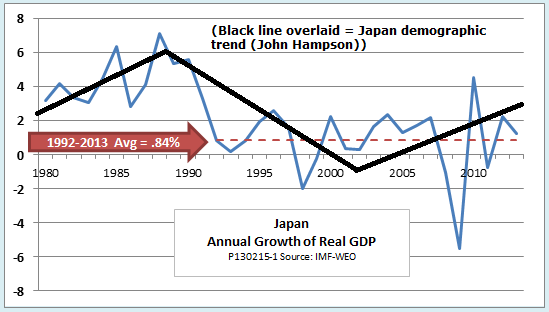

Here is the same for Japan: real GDP growth versus overall demographic trend.

Underlying Source: Economonitor

Underlying Source: Economonitor

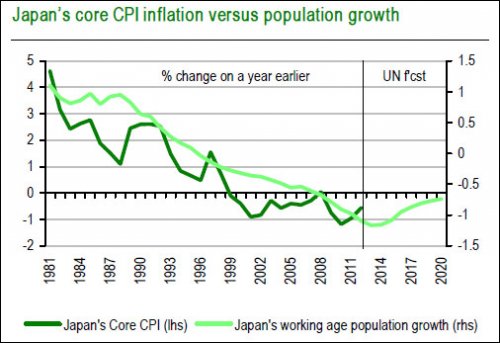

By demographics, Japan should be able to nurse along positive real GDP growth for the next few years. It should also be able to succeed in stopping price deflation:

Source: Andrew Cates

Source: Andrew Cates

Note that both should be feasible by demographics alone, without ‘Abenomics’. The demographic trends for Japan mean that we should see underlying growth, price stabilisation, and rising asset markets, which I believe will be touted as positive results of Abenomics when in fact largely written by the demographic change of trend.

3. JAPANESE EQUITIES

So is Japan a buy? Not all recent economic data has been supportive, but manufacturing and service PMIs are indeed in runs of positive growth, revealing underlying economic improvement. The Yen and Japanese bonds both dropped sharply following the launch of Abenomics but have since retraced some. However, the Yen now appears to have broken down out of a bear flag, whilst Japanese bond yields are shaping for a higher low and a potential push on from there. The Nikkei also consolidated following the big run up earlier in the year, but has now broken upwards out of two consolidation patterns shown:

The line you can see coming into picture at the very top is the 2-decade declining resistance, the containment of the long term bear. I believe a retest of this should be on the cards and I have decided to add to playing Japan equities on the long side. However, if US equities are in a multi-month topping process and soon to enter a new cyclical bear market, then I would not expect Japanese equities to go their own way, only rather to relatively outperform, which would mean decline less. Nonetheless, a new bull market in Japanese equities is belated relative to demographics and I feel happy here trying to make profits on the long side – expecting any downside is more limited than other markets – whilst still trying to assess where US and global stocks are headed. The supporting evidence for Japanese equities to rise should come in real GDP, real economic improvement, and indeed an underlying bid in Japanese risk asset markets. So I will continue to watch the data releases.

The line you can see coming into picture at the very top is the 2-decade declining resistance, the containment of the long term bear. I believe a retest of this should be on the cards and I have decided to add to playing Japan equities on the long side. However, if US equities are in a multi-month topping process and soon to enter a new cyclical bear market, then I would not expect Japanese equities to go their own way, only rather to relatively outperform, which would mean decline less. Nonetheless, a new bull market in Japanese equities is belated relative to demographics and I feel happy here trying to make profits on the long side – expecting any downside is more limited than other markets – whilst still trying to assess where US and global stocks are headed. The supporting evidence for Japanese equities to rise should come in real GDP, real economic improvement, and indeed an underlying bid in Japanese risk asset markets. So I will continue to watch the data releases.

4. USA

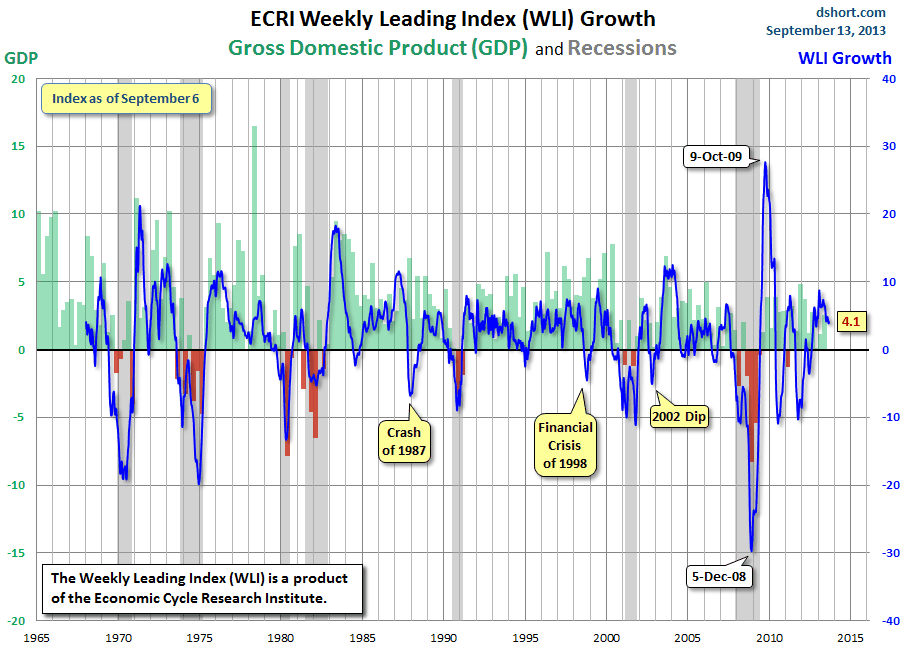

So back to the US. Here is the latest picture for ECRI leading indicator growth:

Source: Dshort / ECRI

Source: Dshort / ECRI

ECRI leading indicator growth fell beneath zero prior to each recession shown in grey. The break into the negative often historically occurred close to the stock market topping, with stocks typically being a leading indicator of the economy. We can see there have been several breaks beneath zero that did not give way to a recession, not least the fairly deep fall in 2011 that helped ECRI (incorrectly) announce a recession. However, my take on the current reading of 4.1 is that we should see this fall towards zero if we are to see a cyclical bear erupt in equities and a recession to occur ahead. This growth measure has been in a declining trend since early 2013, so to add weight to an equities top being formed, we should continue to see this dropping. For now though, this leading indicator, and other leading indicators (such as Recession Alert or Conference Board) point to continued economic growth into year-end.

Weak but sustained growth and low rates are typically a good environment for equities, which would be a framework for equities to move higher and reveal the consolidation since May as digestion in an ongoing cyclical bull. In supportive of this, the Nasdaq is now convincingly at new highs for this cyclical bull, and the Dax is back testing its high-to-date (which is also the all-time nominal high). If other indices break up and away from the ‘topping range’ then we would be looking to 2014 for a cyclical top as a multi-month topping process would have to start over. As noted in a recent post we have some evidence for a topping process in play since May, but also some normal signs missing. This should be resolved one way or the other soon.

5. COMMODITIES AND BONDS

Which brings me to the two main threats to the economy and the equities cyclical bull: excessive inflation from sharp rises in commodity prices and/or excessive tightening from rising rates in escalating bond yields. Bond yields in the major economies continue to rise albeit from low levels. If economic growth persists further and the Fed begins to taper QE then we could expect yields to continue to rise. Historically, the tipping point has been when 10 year treasury yields hit 6%, however today’s demographic and debt interest pressures mean that trouble level is likely to be lower.

Regarding commodities, the most important is oil, as quick major escalations in oil prices have historically correlated with tipping the economy into recession, due to its importance as an input in so many processes. Despite the slack and weakness in the global economy, crude prices have hung around the $100 level the last 3 years. A speculative move into this asset, for any number of reasons, could under current easy money conditions swiftly lead to $125 oil, which I believe would really test a demographically-challenged weak global economy.

On the flip side, the same demographic trends could further erode commodity demand and also limit the exit from bonds. Further commodity price drops, together with yields stabilising relatively low, would again provide the backdrop for equities to march on and economic growth to persist – unless the potency of the collective demographic downtrends drag the economy down into recession on their own.

If Martin Pring’s normal historic topping order is playing out, then we have seen the top in bonds already, we should now see evidence of equities topping and of a transfer in momentum to commodities which should make a peak last as the economy rolls over. This would imply yields and commodities rise despite demographics, and for my work this would be a better fit if the solar peak were still ahead at the turn of 2013/14, with commodities making a final and bigger peak in the months around that.

I believe evidence in support of or against this could become clearer as soon as next week, watching the markets’ reactions to the FOMC output. Some mild tapering is being widely touted as a done deal, but the size and the wording we don’t know. Regardless, I expect a big reaction in the markets and it will be telling how commodities, precious metals and the US dollar, fare afterwards. If commodities are going to make a final big rally then the tentative uptrend of the last couple of months should cement and a US dollar breakdown out of its long term triangle (see HERE) would be a great partner for such a development.

6. TRADING

We are over 3/4 of the way through the year and my PnL is currently showing my worst year of performance to date since going full time, due to the run against commodities longs this year, particularly precious metals. This would repair itself if commodities did begin an uptrend in the last couple of months and now continue into year end, but it could yet go worse if they are in a bear market since 2011 and have further falls ahead. So I have decided to use the Autumn to do what I can to make sure of a good result by year-end. This means I am going to add shorter term trading to my game in this period, whilst running the more medium-term-focused global macro positions. Short trades are something I’ve done before, but not for some time due to success (and personal preference) with the longer term methods. So, I just wanted to share with you that this is what I’m going to be doing different. I am looking for liquid markets that I can play more aggressively for quick gains. So I am looking for candidates amongst the major markets that I can play confidently repeatedly either long or short (i.e. fundamentals/technicals align in favour of one way or the other), and this will include increasing exposure if movement goes the other way. One such play-thing is going to be the Nikkei on the long side, as mentioned above. I am going to pour over some other markets (stock indices, commodities, fx) to find others that I consider suitable, so will share when I decide. You may disagree with my choices and indeed the method, but I’m just sharing what I’m doing, and will let you know the results.

One last thing. Almost all my money is in sterling and I am looking to transfer this to Euros, now I am in Austria. The EUR-GBP exchange rate has therefore become part of my daily watch. A one cent movement in either direction makes a massive difference when considering the amount I am going to be transferring and getting this ‘right’ is as important as my other trading, in terms of the impact on my wealth. So I’ll share my current thoughts, but if any reader is more of a regular in the FX market, please step forward and share your knowledge.

EURGBP has been in a large declining channel since the start of 2009, with the last 3 year snippet shown below. In July of this year the Euro tried to break out, as the Eurozone recovery became more apparent, but it turned out to be a fake-out, and recently UK economic data has surprised to the upside, which has helped not only turn it back down into the channel but also break down beneath the rising Euro support shown. The Pound is fairly overbought now versus the Euro and EURGBP spent last week trying to base. However on Friday there was a further breakdown in favour of the Pound, taking the pair beneath 84. The latest UK inflation data is out this coming week which should influence the pair one way or another, however I believe that ultimately the Euro can drop further here against the Pound, given the technical developments and the change in the fundamental backdrop, and I’m going to hold out for 82- at this point and will review.

On Reuters CRB (CCI) monthly chart I see a possible Falling Wedge which is different compared other analysts who see a sHs-pattern in commodities. Time will tell which is correct.

http://stockcharts.com/h-sc/ui?s=$CCI&p=M&b=5&g=0&id=p88275313805&a=270378628&r=1379180521310&cmd=print

We see some strength in Shipping which is related to activity in Asia/China.

Baltic Dry Index.

http://stockcharts.com/h-sc/ui?s=$BDI&p=D&b=5&g=0&id=p25770303638&a=242567014&r=1379180656887&cmd=print

Marine Shipping Index.

http://stockcharts.com/h-sc/ui?s=$SHX&p=W&b=5&g=0&id=p13918833544&a=315112164&r=1379180728642&cmd=print

Shanghai is ripe for a move to the upside.

http://stockcharts.com/h-sc/ui?s=$SSEC&p=W&yr=7&mn=0&dy=0&id=p07703444182&a=218762234&r=1379187449012&cmd=print

Thanks Niels

Market Vectors Steel.

http://stockcharts.com/h-sc/ui?s=SLX&p=D&b=5&g=0&id=p27539448245&a=278297229&r=1379240985756&cmd=print

Interesting stuff John. I have been thinking a lot about the Demographic ideas and not sure I buy into the theory in the sense that many countries are extending the years people have to work before retirement and people are living longer so pension fund capital is not necessarily being eroded. Not sure necessarily that the “older” generation necessarily only spend all their capital. I think a lot of it is sort of recycled to their children that continue the Ponzi process with more capital. Some of them just continue investing their assets in the stock market too. One could argue elegantly that the more older people the more speculation you can get as these people have more time to devote to the market than younger people busy at jobs. I think the only thing QE does is change sentiment. There is nothing real about the stock market than sentiment. Economics or whatever has nothing to do with it in my opinion. That is just stuff politicians use to convince people of their views. I only believe in sentiment which ultimately shows up in price. I do not believe the crash in Japan and the years it went down has anything to do with demographics but just sentiment. People got badly burnt after the crash and it took many years for the ponzi process to start i.e. change the mood. In the west QE has worked because it scares people of hyperinflation – in Japen they started the process too late. What I think is more pertinent is how a generation and the older generation reflects asset classes i.e. teaches their children. Ex. In the Nordics we have the mantra of residential assets. The older generation made a lot of money here so they tell their children to buy a flat etc. It is considered fail safe. It is not based on demographics but ultimately “belief”. Than various “funny-mentals” are used to rationalize the beliefs and feelings. Humans only use logic and reason to justify their emotional decisions. All decisions are based on emotion and then logic and reason is used to justify those decisions. That is why I only believe in trading that is mechanical based on price. We are not trading some economy but we are trading beliefs and if there is enough belief the market goes up. The sun may alter our excitability as you are arguing but weather there are more or less people participating in speculation I do not think matters really – if prices go up more people get sucked into to that market whore anyways because of GREED. Seldom have I been able to find strategies were volume is a predictive indicator per say. It is predictive of large moves but they can be both positive or negative. If anyone has other views of this then pls let me know. There is no sane economic argument to be made for why Facebook for example is trading at crazy multiples but it does so based of people’s belief based on GREED and FEAR and that is what is real not what one thinks or the funnymental economics. Larry Pasevento says a good thing: Trade what you SEE – NOT what you THINK.

Thanks Robert. Research backs up what you say: with up to a 1 year view sentiment drives prices; up to a 5 year view p/es (that’s demographics by my assessment); up to a 30 year view corporate profits.

I definitely concur there is a way to profitably trade the markets using trade what you see and not what you think, going with sentiment, playing the middle part of a move not trying to call tops or bottoms. However, it’s just not for me. It’s the puzzle of trying to work out the global macro and predict the future that inspires me. Tops and bottoms can indeed be picked, and my methods have been profitable. If they ceased to be I would change. But ultimately, what you say rings true: my reason and logic justifies my emotional decisions.

I like this

Yes. Everyone needs his own style and figure out the puzzle for themselves in my view. There is no other way. This is a good video.

I think sentiment drives it all on all time frames in the sense that price affects fundamentals and not the other way around. Soros calls it the reflexive process.

Interesting vid

I hate being too sweet, so I would like to disagree with you guys about those ’emotions’. That the emotion comes first, then beliefs, then logic. The word emotion is quite empty for me. We humans have three brains inside our heads : reptilian, mammal and logical neocortex. The reptilian guy is the most important and will overrule two others. The reptile wants to eat, have power, have a female. It will allow the logic to try to get them. When it has all he wants – food, power, females, he will allow the mammal to be sociable and care more about the others. When not, it becames a bad reptile. Emotion is only a physical messenger of its will. Its will is in our subsconcious beliefs. For example, we meet a guy who, we reckon, wants to do harm. There is fear in us, it eliminates our goodness and forces the logic to act as it dictates. But firstly, there must be in us the concept of danger, concept of death, of a loss, realities or visions that we want to avoid. We must know or imagine how a dangerous guy behaves like. But everybody is a bit different so the perception of danger varies. Now, you will think I am crazy – we can convince the reptilian that death is good. That there is no danger. When the Russian soldiers defending Stalingrad in 1942 were told there is no land behind them, only in front of them and that there is no return, guess what they felt. RELIEF.

But the deepest truth about trading psychology I got from watching…a TV program about dogs. Dogs and their owners. Dogs cause problems, are agressive, possesive, depressed and erratic only when they are in charge – pack leaders. Many owners allow their dogs to lead. But when dogs are forced to be subject to a leader (owner), to have confidence in them, they lose all their bad habits and behaviour stemming from inside of them. It means they are not in charge anymore, so their master’s will is what they believe and what they feel. The only reason why traders have problems with discipline, or behave in trading not like they want and later they regret, reason why traders experience so called fear, greed, hope and ignorance, it’s because they are in charge of trading, of their strategy and choices and their aim is to have a profit, to win with the market.

How often do you hear traders say ‘I am only an office worker who click at buy and sell button when I must’? Most seem to make money thanks to their intuition, intelligence, patience and host of other advantages. So, hear my deepest truth about psychology of trading :

I am an office worker, slave to my strategy. I have a total confidence in it. I have nothing to say, to object. I don’t make money and I don’t lose it. My strategy does it for me. It says when to scale out, when to take profit. I don’t feel anything,

I am as aware, tense and deep as when shopping on a Saturday morning. When I have running profits, I have to stay, hold and add, although its boring and takes my time. My reptile sleeps at my feet, it has nothing to say, its not in charge.

This is my own personal opinion and everybody is welcome to disagree. I hate to responsible for opinions of others:)

Nice post desperate

Sorry , its despe, not desperate

What about a nice easy name like Peter or John2?

superb !

Thanks Vic

There is nobody on this planet that can know what QE can or can not do or the results not even Big Ben. Every moment in the market is unique and it all depends on how traders ultimately behave based on emotion. It is dangerous to get married to an idea or view regardless of how logic it may appear, you only need one black swan to prove that not all swans are white. I thought that printing money was crazy and still think so but I have come to the point to just disregard it completely. It is irrelevant to make money in the markets. I think it is irrelevant to whether it causes the markets to go up or not. And especially the way I FEAL about it. There is no scientific way to argue that it is the cause of rising markets or that it will not work or has any effect whatsoever. We might believe so and it makes us fear but ultimately I think it just confuses traders and investors so better just disregard it.

wonderful job thanks a lot

just want to share my view, which is similar to your I would say

http://www.francescomaggioni.com/secular_outlook.php

Thanks Francesco, interesting reading round your site

Thanks John for the article and you guys for your input. I read you with pleasure which makes me a bit uncomfortable. It’s easy to read, agree or disagree, however, a bit more difficult – although much more powerful – is to think and analyse for ourselves. My best discoveries came from my thinking; my system is thoroughly the result of my experience and my research. In the past, I tried to enhance my knowledge about the price action by reading some reputable TA books. Unfortunately, they caused a regress in my trading and I spent a year to undo the false beliefs they managed to sneak into my brain. Now, I can only laugh at them. Basically, those guys writers try to make a forecast based on some ‘in-chart’ elements, or behavior of an indicator below. With air of authority and seriousness, they fail to notice that in the very same chart there are one or two instances of the same element not working as they say it should. Besides, all their elements are shown with the benefit of hindsight, not how they look when they start to develop; the early recognition is more important than the way the ‘final result’ looks. Also if you let mr Right Shedlock and mr Wheatherman Faber poison your mind with their follies, you would need a year or two to shake it off.

For me, forecast is a dangerous thing in the market. It’s useful to try to forsee, to form a personal bias, against which we read the subsequent price movement more clearly. But it cannot obscure our tape reading, and reacting to it. If we make a forecast to form a firm belief and produce a roadmap, we will not react properly to what is happening, in case our forecast is not right. I do have a collection of my DJIA day types, a colorful monthly grid with open types, daily ranges, how HTF looks like. I know how many ‘open test drives’ and ‘open drives’ we had in August. I know I must expect a trending last hour on a news day, or a range after a trend day. But this all doesn’t constitute a forecasting system for me, it’s only to show me how different days, trends and developments can be. Ideally, I don’t know where the price goes before the session starts. True, within 3 minutes I can asses with 80% accuracy what kind of open this is, and after 3 first 5m candles what day type this is. It’s a guessing system, probabilities assesement. I must say that somehow it looks similar to what John Hampson is doing with all his data, demographic, solar,technical and fundamental factors. John has a probable outcome, but also has other scenarios and keeps an eye on the developments. And let’s be honest, John is a skilled technician, too. He simply focuses on the most important element of the price action, the break-out. A break-out (whether from wedge, island, level) is the beginning of a change in the market, and charts are nothing more than the depiction of series of changes in the market. You’re right John, it’s good to use a preferred strategy. Top and bottom picking is a specialty like others. I once traded along a guy who was doing exactly this in daytrading S&P. I mean, he was looking at a moving market for hours only to anticipate an entry against the flow. Decisions to enter based on price, his own levels and moving average of ticks. I couldn’t stand it! A drive offers me entries with the flow, I will never wait for the end of it. If it turns, I will jump in again in the other direction, but it must start first. The guy is doing very well and trades for 8 hours a day. I trade from 1 to 2 hours, only sometimes all day long.

(So much for the myth that day trading is more time consuming than HTF)

Many thanks Despe