1. MORE ON CRUDE OIL

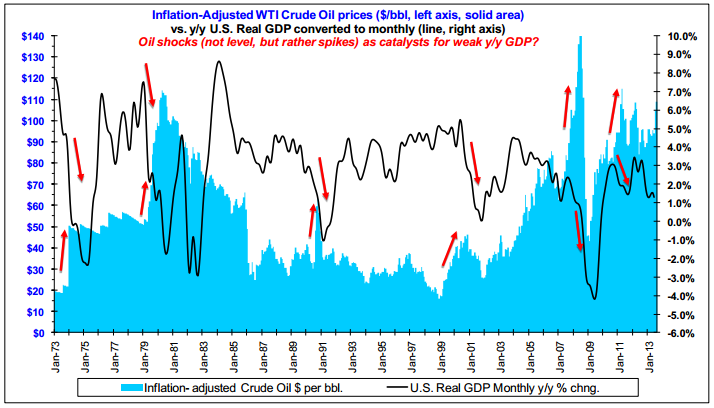

Here is a chart from Barry Bannister showing the impact of previous sharp moves higher in oil prices:

Source: Stifel

Source: Stifel

He suggests it is not the real oil price level per se but a ‘shock’ i.e. a big, fast move up in price that brings about a collapse in GDP.

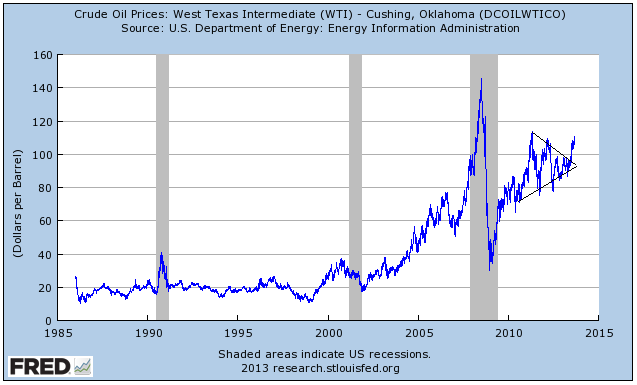

Here is the nominal view of crude:

Source: FRED

Source: FRED

From a technical perspective, the potential for such a swift rise is there, as crude has broken out of its triangular consolidation to the upside. A break above the 2011 high of $115, which is within reach, could be enough to produce the speculative spiral that has been behind previous parabolic rises.

Zooming in on the nearer term, a fairly messy range has developed over the last six weeks, with the contract buffeted about over Syria. With inventories still above historical averages it could be interpreted that there is a lack of appetite to buy higher than this range, and clearly there is a risk that this stalling in momentum gives way to a breakdown.

Source: Stockcharts

Source: Stockcharts

However, for now, the price continues to edge upwards and a bullish intraday reversal candle formed on Friday. So let’s see what happens this week.

2. DEMOGRAPHICS, TECHNOLOGICAL EVOLUTION AND CORPORATE PROFITS

What if exponential technological evolution more than offsets negative demographics? I.e. what if rising corporate profits thanks to technology-driven gains can spur the stock market higher, maybe exponentially higher?

Here are US corporate profits, which seem to suggest that could be happening:

Source: FRED

Source: FRED

Now take a look at wages as a percentage of US GDP:

Source: Business Insider / FRED

Source: Business Insider / FRED

The employment to population ratio has also fallen sharply. Companies are making more profits but employing less people and paying them less. Technology is one key factor in this: it is cheaper and more efficient for companies to increasingly employ tech over people. As we are concerned with the stock market, are the corporate profits what matter? Well, more unemployment and lower incomes means lower demand in the economy. Hence we have seen a consistent theme in recent earnings seasons of revenues disappointing versus earnings: companies not making profits through demand but through cost savings.

But now take a look at what has been to a large part responsible for the recent rises in corporate profits to all-time highs:

Source: Pyramis

Source: Pyramis

It is the government defecit. Government ‘spending’ (stimulus programmes, cutting overnight lending rate to banks to zero, etc) has been the major factor since the 2008 crisis in pushing up corporate profits. Those corporate profits are real, but at the expense of increasing public debt. So the US government wants to cut back QE when it can, and facing the debt ceiling again – another ‘fiscal cliff’ – it needs to cut back spending and make savings. It also wants to keep rates low, ideally lower than inflation, to reduce debt servicing and shrink the debt, so current rising yields are a threat. Extracing from that Richard Koo PDF again, Japan only fell into deflation once it had fallen off the fiscal cliff, following an attempted fiscal consolidation.

Additionally, drawing together several pieces of research, it turns out corporate profit levels are only important in stock market returns over long timescales, e.g. a 10 year view. Sentiment is the main market driver in any one year, and p/es are the main driver if trading say on a 2-3 year timescale. By my work p/es are relative to demographics. A p/e of 20 is not expensive if the demographic trends are strong and positive, and vice versa.

So, I can now come back to the opening question of whether tech evolution can push up corporate profits and in turn the stock market, and offset weak demographics. Tech can enable cost-cutting but this can be at the expense of people, resulting in lower demand in the economy, so it’s not just a simple win, it cuts both ways. Furthermore, recent record high corporate profits are shown to be mainly due to a transfer of wealth (debt) from the Government, and the risk to future earnings is in Government action to cut back QE and savings to deal with the debt ceiling. But ultimately, corporate profits don’t matter so much for the stock market, only in long term investing. Sentiment can push the market one way or the other ‘irrationally’ before p/es and demographics come into play, before corporate profits.

In summary, I am still of the opinion that we do not have a new ‘secular’ bull market in stocks underway and that once ‘sentiment’ gives way, the collective demographic downdraft will help topple the economy and stock market. Action on QE and in response to the debt ceiling could be a catalyst for future corporate profit disappointment, which could help tip the sentiment. Crude oil, meanwhile, could do the job all on its own, if ‘some development’ provides the impetus for a speculation move into the commodity. Exponential technological evolution is a real phenomenon and I believe is ‘the great hope’ for humans to deal with the debt, resource scarcity, global wierding, demographics, overpopulation and other challenges. But I don’t see evidence that it can drive the stock market ever higher versus these phenomena in the shorter term.

thanks a lot for sharing all this very interesting stuff.

I appreciate it a lot

Thanks again

Hi John

Another thing to throw in the pot on this one – it might be that US companies with a high % of revenues from overseas markets might fare differently to those with a heavier weighting towards the US domestic market. Then of course it depends on which overseas markets … depends really on the real economies of those countries.

No definitive view here, a thought only.

Yes it’s a factor, hence I tried to crunch and weight the major economy demographics here: https://solarcycles.files.wordpress.com/2013/06/6jun20131.png

Hi John.

Your efforts are very inspiring and educational – thanks!

I personally only know 3 guys who’ve become wealthy through the stockmarket.

Two of them are ”old school” , meaning they had good salaries and reasonable frugal lifestyles, and bought a handful of stocks they knew well. Adding to their portfolio every month, reinvesting the dividends etc. etc.

As they started in the mid 1970’s they had the benefit of starting with a two deacade ride upwards.

I saw them sticking to their beliefs through both bottoms (2003 and 2009). They were shaken and pale but never gave in. That classic long term approach is probably the safest bet for any young person when approaching the market. Takes a very stubborn type of personality, but the market cannot relieve you of your portfolio if you never sell.

The third guy is a trader, and the way he’s made his fortune is by focusing on the ”internals” of the market – meaning price only. His view is that since the market is said to be on average six to nine months forwardlooking, we are more or less forced to focus on price alone. Plus the market is forwardlooking mainly in bullmarkets, and gets progressively less forwardlooking during bears, until a panic brings instant reaction without any forwardlooking ability at all.

That guy is also totally against using any technical indicators based on oscillators, they will work against you in any prolonged bullmarket. His approach is trying to trace where money flows, similiar in style to the site http://www.decisionmoose.com

Plus adding the smoothed combined price of a handful of well chosen major stocks as his own ”indicator”.

These 3 examples are perhaps what it boils down to, we can either lead reasonable normal lives and take the long and ”safe” ”never sell”-approach, or we can try finding our own personal trading method.

Depends on personality and interests.

So all your thoughts and research is much appreciated, John. Keep it up, and stay safe.

Sorry for this long rant! I will end by describing what an eyeopener it has been for me following the rise of the western markets since the 2009 bottom. Made it crystal clear how powerful the western banking system is – in sheer muscle power. It wields all the stealth economic powers of this world today (until it breaks, ofcourse), sitting on threehundred years of rules and regulations. The power of last recourse is the SWIFT system -the system by which official funds are transfered between nations. If any country stray outside the financial laws of this world they will be subject to threats of exclusion from the SWIFT system, facing being thrown back 70 years in time. This maintains the present system of finance (for better or worse) for any forseeable future (bar a major world war).

So that is what we have to work with – the present day fractional reserve banking system and how it interacts in markets globally. Influenced by various ”external” forces like sentiment, demographics, spaceweather, technology and on and on.

It’s all very interesting, but my conclusion is that we will always come back full circle and mainly be forced to focus on the ”internal” priceaction (while keeping eyes alert on ”external” forces).

Seems to me we’ve had a classic ”stockmarketclock” runthrough since 2009: first industrial metals shone, then financials had their day in the sun, and now consumables and ”bling” are accelerating. Notice how Sotheby’s (BID) is going exponential. When BID crashes it’s time to go short (right on the solar peak, perhaps)?

Regards and all the best!

Sigge

Thanks for your thoughts Sigge, always interesting to read who’s made enduring money how. I’d like to think I can trade the markets indefinitely now (based on some kind of idea of reaching a tipping point in knowledge and experience), but I guess you never know.

John: http://www.youtube.com/watch?v=9z4Kft47kBM

Stick to your system but do not get married to a view or theory.

Those charts of corp profits vs wages is a recipe for revolution. The chart of profits has a fived count but no top formation yet. And wages have a nice descending wedge, so maybe better times are ahead.

See what you mean, thanks Kent

All models updated. This Thursday is the full moon and the start of the lunar positive period at the weekend, and the geomagnetic trend moves to an upward slant looking out the next 3 weeks. I therefore speculate that we could see a slight pullback into the FOMC output on Wed, then taper-light delivered (sending a message of confidence in the economy whilst keep foot on QE and ‘leaving all options open’ talk to go with it), and a subsequent 2-week rally in risk assets.

Thanks, John, very kind of you