Certain key assets are finely poised as we enter December. The UK FTSE is once again attempting upside breakout from its long term triangle.

The German Dax is also back attacking key resistance. Yesterday it was repelled at this key level. I suggested yesterday it may need a couple of sessions’ consolidation before a breakout – and this is because it has already travelled a fair way since mid November on ‘one leg’.

The Nasdaq (and equally the Dow) is attempting to reclaim its 200MA (the SP500 is clear above). The Nasdaq remains in its neat cyclical bull channel, and stocks in general continue to display good breadth and cyclicals performance that are not suggestive of a top.

That said, a combined failure in the FTSE and Dax at upper resistance and the Nas and dow at their 200MAs would open up the possibility of a renewed leg down, and for the two US indices that would then look more like a major top had occurred.

I maintain a bullish outlook for equities into year end, due to positive seasonality (including Presidential), tame forecast geomagnetism, a lack of common cyclical bull topping indicators in the US indices, and renewed breakout attempts in the FTSE and Dax (typically resistance caves in under repeated attacks, the Hang Seng has already led the way, and by solar/secular history an upwards breakout at this point would be normal). We have a period now into and around the new moon of 13 December which should also be supportive. So let’s see if I am correct and all these indices break upwards.

Let me just list one or two other ‘important’ dates into year end. The Puetz crash window extends into the end of this week. The Mayan global transformation / apocalypse is 21 December, the last major Bradley turn is 22 December. The last full moon of the year is 28 December and the fiscal cliff deadline is the end of December. Out of those five, I am not convinced of the first three, but it does no harm to maintain awareness.

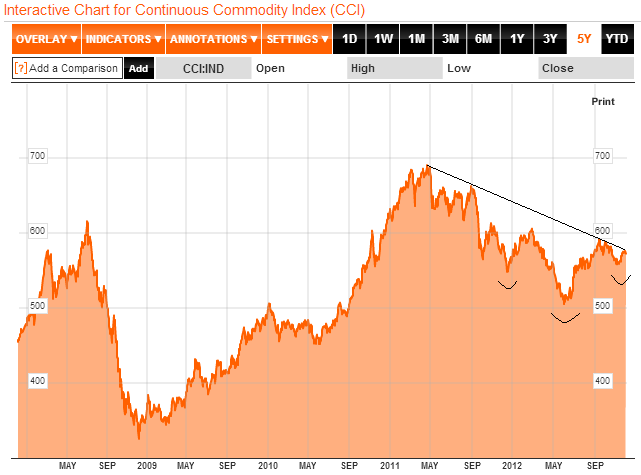

The finely poised position in key assets extends to commodities and Euro-USD. The broad CCI commodities index is at downsloping resistance in a potential bullish head and shoulders formation. Ditto the Euro-USD.

Source: Bloomberg

Combining stocks, commodities and Euro-USD, we have two clear paths forward: one, pro-risk breaks out (the correction in October / November was a correction in an ongoing cyclical bull), and two, pro-risk is repelled here and resumes downward (the rally in the second half of November was a relief rally in a new downtrend). As is usual when the markets are finely poised, some confusing and teasing action could occur this week, with both bulls and bears prematurely claiming victory before true resolution comes to pass.

Besides the reasons above, one other key reason why I favour a bullish year end for pro-risk, is the improvement in global leading indicators. Markit released many individual country PMI reports yesterday, including fresh growth in China (whether looking at official or HSBC data). Below is the combined global picture, and the theme is fairly clear: a distinct up-tick. This is echoed in Conference Board global leading indicators. The general improvement is not in doubt, the question is whether this is just a temporary relief rally in a continued downtrend, or whether leading indicators have bottomed out.

Source: Markit

Source: Markit

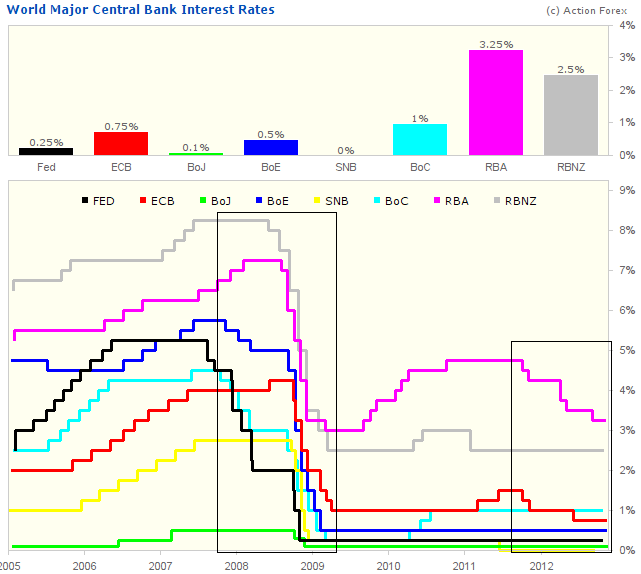

And here we get to the real key issue. By solar cycles, a growthflationary finale should occur into next year’s solar peak. By stock market history, cyclical stocks bulls end with excessive inflation and overtightening of rates. A cyclical stocks bear here and a tipping into global recession at this point into 2013 would mark an anomaly in both those historic indicators. It would be evidence that central bank actions in cutting rates and applying stimulus have been impotent in this cycle, and that too would also mark an anomaly in history, because historically interest rate cuts have had a positive impact on the economy between 9 and 24 months after cutting cycles, and Quantitative Easing has so far been shown to work its impact through in the two years following asset purchases. The two charts below show the renewed easing and stimulating efforts over the last 18 months – not as dramatic as in 2008-9 but nonetheless a fresh round of pro-action and intervention.

Source: Action Forex

Source: Action Forex

If the mechanism is not broken, and such action is not impotent, then we ought to see economic improvement occurring now and into next year. I believe this is the case, as currently global leading indicators are improving, PMIs are improving, and growth in narrow money suggests global industrial output will increase ahead. It is possible that we therefore do see that growthlationary finale next year and we do get normal cyclical stocks bull termination under conditions of excessive frothiness and an upswing in market rates. But one step at at time – first we need to see a couple of months of continued improvement in leading indicators to be confident that this is a new up trend and a normal positive impact lag to central bank actions together with normal buying/speculating/risk-taking behaviour into the solar maximum. If this does not occur and instead we topple over again in terms of leading indicators and key assets, then either (i) the triple historic anomaly would have indeed come to pass (‘it’s different this time’) or (ii) yet further central bank action and unorthodox policy tools are deployed soon ahead before we finally do get that growthflationary finale not too far from the solar peak.

Until evidence points otherwise, I side with it not being different this time and that we will see normal behaviour into the solar maximum, aided by lagged impacts from central bank actions, and normal conditions to come to pass for a cyclical stocks bull end. I believe the current technical action in risk assets is supportive of this, in that we see certain key stock indices pushing to break out, an absence of normal cyclical stocks bull topping indicators (such as breadth divergence and defensives outperforming) and gold in a renewed up trend back above its 200MA following an 11 month consolidation.