I have enlightened myself again this weekend, and I feel just in time. More outlook changing research. These last 4 months or so have been a real leap forward in understanding, personally. So yes, some of my views have changed, parts of the site need updating, but let’s get to the important. Demographics not only dictate ‘secular’ bull and bear markets in stocks and real estate, but also play a major role in inflation, disinflation and deflation.

It is labour force growth or shrinkage playing a key role in price inflation. A swell of people aged 15-20 entering the workforce works up price inflation through spending, whereas more people entering old age relative to the work force is disinflationary through saving and disinvestment. There are correlations with inflation in labour force growth (15-60), young labour force percentage (15-40) and dependency ratios (inverted – old and young versus the working population), all of which are approximations of the same idea. It’s another simple but powerful mechanism, in the same way swells in the ‘investment’ age group produces equity bull markets.

Countries with ageing populations have generally experienced low inflation in recent years, whereas younger countries have experienced higher inflation, due to the resultant spending boom:

Source: Andrew Cates

Source: Andrew Cates

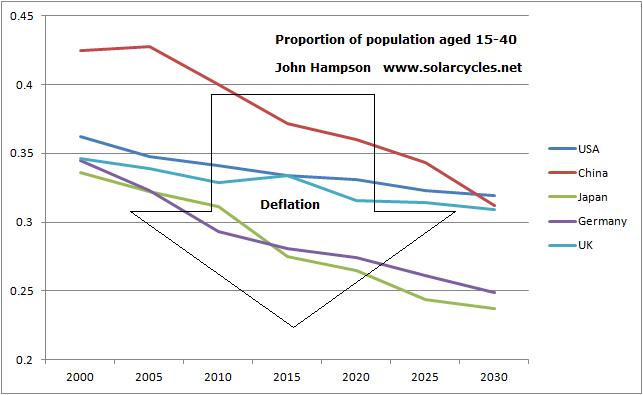

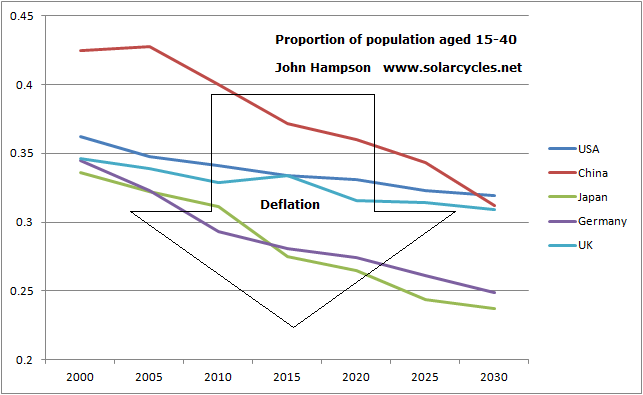

Japan’s proportion of 15-40 year olds has historically correlated with inflation levels:

Source: James Bullard

Source: James Bullard

Japan’s working force growth projection suggests Japan will not successfully reinstate inflation this decade, but will at least manage to change the trend as of around this year:

Source: Andrew Cates

Source: Andrew Cates

Here is the 15-40 year old ratio history versus inflation for the USA, also showing the correlation with inflation:

Source: James Bullard

Source: James Bullard

And two projections forward:

Source: James Goulding

The charts suggest the USA should be tipping from disinflation into deflation. That is, if we assume the Fed is powerless to stop it.

The charts suggest the USA should be tipping from disinflation into deflation. That is, if we assume the Fed is powerless to stop it.

Now look at dependency ratios for some of the main countries, we first see that collective trends historically matched broad global inflation history (nb: dependency ratios are not inverted in this chart):

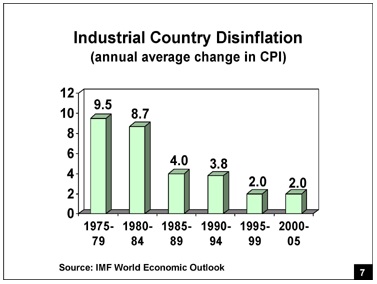

Dependency ratios collectively fell (i.e workforce proportions grew) between 1965 and 1980, which was a period of rampant inflation. Since then we have seen overall disinflation, and this is confirmed below:

Dependency ratios collectively fell (i.e workforce proportions grew) between 1965 and 1980, which was a period of rampant inflation. Since then we have seen overall disinflation, and this is confirmed below:

Looking forward, we see collective deflationary dependency ratio trends in the major nations, with the exception of India and Brazil (nb: dependency ratios are inverted in this chart):

Looking forward, we see collective deflationary dependency ratio trends in the major nations, with the exception of India and Brazil (nb: dependency ratios are inverted in this chart):

The alternative 15-40 ratio measure paints a similar picture of price deflation ahead for five of the most important economies:

This explains why ZIRP and QE have failed to bring about inflation in Japan and now the USA. These countries want to inflate, but the demographic trends mean the public just won’t spend sufficiently in the economy for it to happen. For the majority of the major nations, this is a problem going forward, as the demographic trends persist and worsen. For the global economy, this is a problem, because the combined GDP of Brazil and India and other smaller positive-demographic countries is much smaller than the combined influence of the USA, China and Europe.

This explains why ZIRP and QE have failed to bring about inflation in Japan and now the USA. These countries want to inflate, but the demographic trends mean the public just won’t spend sufficiently in the economy for it to happen. For the majority of the major nations, this is a problem going forward, as the demographic trends persist and worsen. For the global economy, this is a problem, because the combined GDP of Brazil and India and other smaller positive-demographic countries is much smaller than the combined influence of the USA, China and Europe.

So what’s likely to happen? The central banks of these countries are largely pushing on a string. They can’t force spending and investment, they can just use ‘carrot and stick’ tools to encourage spending and investment and discourage saving and cash. The evidence suggests that disinflation should continue. The risk is that disinflation turns into deflation, as the demographic trends suggest. The global economy is at risk of falling into a new recession, or even depression. It explains why the recovery since 2009 has been spotty and weak. The central banks will likely have to persist with ZIRP and QE and perhaps also deploy other unorthodox tools, but which would likely have the same lack of potency. If deflation takes hold, then debts would grow, savers and currency holders would be beneficiaries, and investment would become unattractive because future prices would be lower. Risk asset markets would fall.

So why are equity markets so strong currently? We have disinflation and low growth, together with the ZIRP and QE easy money conditions. Whilst the former two conditions hold, then speculation is encouraged by the latter two. It would take a plunge into recession and deflation to generate the exodus out of stocks, and it is such a development that a couple of analysts that I respect are touting (e.g. Russel Napier, using the Q ratio, predicts the SP500 to bottom at 400 in 2014). With this new research, I now understand why.

But could this benign status quo continue, with low growth and pro-speculation conditions, with the central banks acting together to maintain such conditions? Well, I would repeat that all they can do is encourage and discourage through their limited toolkit. They can’t force. The demographic trends are now united negative in USA, China and Europe, which provides a powerful downward pressure. There are less new investors coming to market, and more leaving. So how can stocks keep rising? I suggest the answer lies in the current margin debt situation:

Source: NY Times

Stock market participants have increasingly borrowed and leveraged in the market. So it’s not more investors but the same investors buying more and more on credit, and as the graphic shows, when margin debt reached over 2.5% of GDP previously, the stock market fell into a cyclical bear subsequently.

Here is the correlation between the S&P composite p/e ratio and the middle-old demographic ratio for the USA, with projection:

It suggests a fair p/e of around 10 by next year. As of Friday’s close the p.e was 18.4. A shrinking of p/e can be achieved either by stocks holding up nominally but strong inflation eating away at the valuation, or it can be achieved by stocks tanking under no-inflation or deflationary conditions. By the demographic projections further up the page, the second option appears likely. This would also mean US stocks could be in for severe falls ahead.

It suggests a fair p/e of around 10 by next year. As of Friday’s close the p.e was 18.4. A shrinking of p/e can be achieved either by stocks holding up nominally but strong inflation eating away at the valuation, or it can be achieved by stocks tanking under no-inflation or deflationary conditions. By the demographic projections further up the page, the second option appears likely. This would also mean US stocks could be in for severe falls ahead.

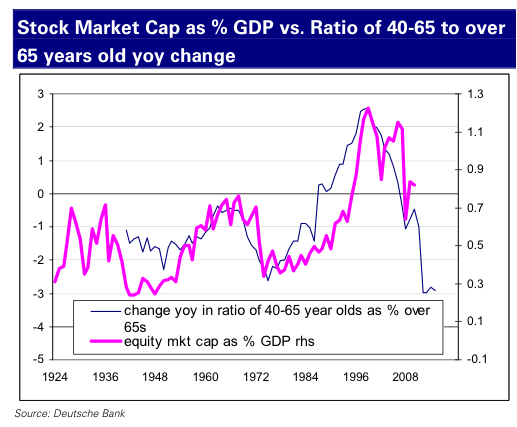

Deutsche Bank produced the next chart which shows US market cap as a percentage of GDP versus middle-old demographics. SMC as %GDP is a valuation measure for the stock market and the second chart below shows where we currently stand, which is very much overvalued versus the demographic forecast in the first chart:

Source: Business Insider

Source: Vector Grader

Again this suggests the US stock market should be in for sharp falls, both real and nominally, because the demographics don’t support inflation. I therefore believe US stocks should be a good shorting opportunity ahead, together with Europe and China. However, I still think Japan is set to do well as a long equities bet. The pick up in labour force growth for Japan, shown higher up the page, from this year looks set to change the deflationary trend even though true inflation looks set to remain elusive. So that suggests at least stabilisation in the economy. However, equity prices could grow much stronger, in line with the M/Y ratio:

The next two years is a particularly good demographic period for Japan as middle-old and net investors measures also rise. Plus Japan is playing catch up to demographic trends that turned up as of around 2002. I maintain that Japanese stocks took off then but were pulled back by the global crisis of 2007/8. So, the question is whether they would again be dragged back by a new global recession and a stocks bear in most of the major nations. I don’t think they would be immune, but I would still expect them to outperform and eventually deliver their demographic fulfillment. Plus, there is a chance of a fast speculative boom. Current monetary conditions encourage bubbles, and the new Japanese government has upped the ante by saying it will buy equities as part of its reflationary policy. With speculative behaviour also at peaks around solar maxima, I think there is a chance Japanese equities could go crazy, and so I will maintain long Japanese equities and add on any further retreats.

Now one more demographic correlation, this time with government bonds. This work by Credit Suisse is the same simple idea: the ratio of those who are predisposed to buying government bonds to those who are really not determines the long term path of bond yields:

Source: Credit Suisse

Source: Credit Suisse

For the US and Europe we see a change in demographic trend has taken place over the last 10 years which should see outflows from bonds going forward, and yields therefore rising. The US changed trends first, which suggests treasuries are belatedly falling to trend now, and that the flows out of treasuries are justified.

If a sharp cyclical bear does occur in equities, then we would have a similar deflationary shock to 2008. In that experience, most assets were sold off as people needed to raise cash to pay for losses elsewhere. Gold did not escape. It was government bonds that were the recipient of the money flows. Would they be this time?

Let’s turn to gold. Historically, gold has performed well when demographics have been in negative trends. I recently showed that the Dow-gold ratio had bottomed and topped very closely with demographic turns in both the USA and UK. Below, the same p/e demographic ratio as shown further up the page but with the gold price added also shows the inverse correlation:

Source: Glenn Morton

Source: Glenn Morton

You may read that in the 1970s gold rose as an inflation hedge, in the 2000s gold rose under disinflationary conditions, and gold also performed as a deflation hedge in 1933. Gold is touted as a hedge against systemic risk and financial market instability, as hard currency or as a store of value under conditions of negative rates or currency dilution. What I would suggest is that gold is the go-to, the default investment, under certain demographic conditions, i.e. ‘negative’ demographic conditions. When demographic trends are counter equities and real estate and government bonds then gold becomes attractive by default. This ‘last resort’ status is reflected in gold’s real performance over time, namely it goes nowhere in the long term.

When equity p/es are declining under m/o demographics, and stock market interest is in decline due to m/y and net investor demographics, but labour force growth demographics are inflationary, then we have disinvestment in the stock market but price inflation in the economy. This was the 1970s, and reflects the broad collective downtrends in demographics amongst the major nations at the time. Gold and commodities outperformed.

When equity p/es are advancing under m/o demographics, and stock market interest is increasing due to m/y and net investor demographics, and yuppie/nerd demographics are pro bonds, and labour force growth demographics are price disinflationary, then we have investment in the stock market and bond market and price disinflation in the economy. This was 1980-2000 for most of the major nations, although Japan changed demographic trends circa 1990 and went its own way. Equities and bonds outperformed.

From 2000 to current, we saw some divergence in demographics. For the USA, equity p/es were declining under m/o demographics, stock market interest was in decline due to m/y and net investor demographics, and labour force growth demographics were disinflationary, so we had disinvestment in the stock market (secular bear market) and price disinflation in the economy. However, Europe largely retained positive demographic trends until mid-decade and China until around 2010. China’s conditions were price inflationary, and as the biggest consumer of commodities, commodities had a demand story. Some have suggested that gold performed well in the 2000s under disinflationary conditions, i.e. that it is a beneficiary under disinflation, which may be true. However, the picture is muddied because of the price inflationary China demographics which could equally have been the story for gold’s rising, partnering with commodities again.

Which brings us to now and the next few years ahead. We see more united demographic trends again. For the USA, China and Europe, equity p/es should be declining under m/o demographics, real estate interest should be declining under m/o and dependency ratio demographics, stock market interest should be in decline due to m/y and net investor demographics, yuppie/nerd demographics should be counter government bonds, and labour force growth demographics should be price deflationary. So we should see disinvestment in the stock market and bond market and price deflation in the economies of these countries. What would be the winner under such conditions? I believe it has to be gold, as the default, go-to asset again. I suggest this would be the difference to 2008, as government bonds have changed trends and with ZIRP still making cash unattractive, money has to flow somewhere. If the solar maximum is ahead this year and this deflationary shock happens 2013-2014 with gold the recipient, then we would once again produce a secular peak close to the solar maximum.

What about commodities? I am not sure if commodities as a whole would be winners in such a deflationary shock. I have my doubts, because the demand story should be on the wane, and they are a class for inflationary trends. I believe the question is whether they collectively would become a speculative target, rather than an economic demand target. If equities are close to topping then commodities could go outperform here in the historically-usual pattern of topping last as the economy rolls over. However it would be done so most likely on speculative interest, rather than tight inventories. Geopolitical or climate events could play a part, particularly as the solar maximum has historically inspired protest, revolution and temperature peaks. The solar maximum has also historically seen speculative climaxes, so the potential for commodities as a class to rise is possible, particularly if oil took off. However, I am now very much open to the alternative, which is that the price deflationary demographic trends, particularly in China, take down commodity prices from here, and precious metals perform alone. I am therfore going to refrain from adding any more to my long commodity positions for now, and watch developments.

In short, I think calls that gold’s bull market is over are premature, as it is the counter-demographic go-to asset. Equities are on borrowed time due to counter demographic performance and margin debt. Collective demographic trends in USA, China and Europe are not in favour of stocks or real estate, nor pro-government bonds. Price deflationary trends are in place, which means falls are likely to be hard in nominal terms for risk assets. Commodities may not escape this, unless they are initially speculated to a peak and then join the falls. We don’t really have a precedent for such a coming together of trends, but I believe gold should be the winner as bonds, equities and real estate are counter demographic and cash is unattractive under ZIRP. I want to short stock indices from USA, China or Europe, but want to play long Japan, as it is the demographic exception. Brazil and India are also positive-demographic, but are not likely to escape a sell-off. I want to add long there post-falls. I will remain short treasuries and long precious metals.

I stated at the top of the post that I believed this analysis to be just in time. By that I mean I suspect equities could fall hard at any time, and that’s the position I want to add to my portfolio: short stock indices. I can now see more of a case why US equities could be in an eiffel tower formation and about to collapse. So I am going to add short without delay. If China liquidity and emerging market issues don’t escalate this week and set off sharp declines, then I would ideally still like to see a more regular topping process with another attempt at highs before rolling over, over the next couple of months.

excellent John 🙂

I agree that we see a speculative bullmarket top, that is not supported by demographics etc, but the “story” from FED… and the impression that FED can solve anything.

And we need some kind of shock to break this bubble, just like any other bubble.

And it should happen within ~6months

My projection for Shanghai is pointing down until September (and then possibly more after a bounce).

And for crude oil it also suggest weakness the coming months.

I think the sunspot cycle failed in its last attempt to make solar maximum this summer, but cannot rule out another “attempt” around September (allthough the tidal cycle says NO), or in March 2013 (allthough my wobble-cycle says NO).

At this peak in May, both tide and wobble were very favorable, but the Sun did NOT impress… and was very suggestive that there is no more power left.

Looking at my market cycles I see two likely outcomes, and next ~2 weeks should decide

-either we fall further next weeks, which will indicate collapsing cycles and a downtrend to December. And that should break the bubble

-or the cycles manage to lift us to August-September, and probably top out with a left-translated bearish cycle, and start a downtrend.

Right now I favor the first one, with collapsing cycles… but the most common pattern is perhaps the flatter top and alternative two.

So next ~2 weeks we either need a bullish game changer to stop the liquidations we see in many markets and currencies.

Or see some event that causes panic.

If we get neither, I am not sure what the market will do without triggers…

JAn 🙂

As I showed yesterday, the Norewgian currency started to crash against USD last week. The Norwegian media has written that this is good for stocks, making them relative cheap, and is favorable for exporters.

But they cannot have studied the correlation… which obviously shows that a falling currency typically suggest that foreigners escape the Norwegian market, and the stockmarket goes down.

When looking at the Norwegian25 index, it was near ATH… but that is because of dividend-adjustment. The price-index in blue shows that Norwegian stocks are well below the 2011-top

Also the price index is below 200MA, has broken trend-support, and is close to getting a declining 200MA

When looking at issues above 200MA, we see a top in March, and diverging top in May

So the currency is suggesting a possible selling pressure from foreigners, and the stocks/index is showing weakness and is close to really start breaking down.

Something must stop this very soon, or we see accellerating selling.

Adding some statistics

Here are number of days in Norway, without a -7% retracement OR a 80-day low.

We are near record levels since 1997, and to reset this indicator we need to drop another ~2% to test/break the April low.

And if that happens, it will be very difficult to recover. Unless it happens very quickly, and then rallies strong on some kind of bullish news…

Many thanks Jan

Terrific work John/ Jan. FWIW I’m seeing the second of two scenario’s Jan paints as being more favourable, based on FTSE price, pattern and time (see link.)

http://thedarklordblog.wordpress.com/2013/06/23/latest-ftse-musings-revisited/

This coming week should provide clues.

Thanks TDL. Yes your pic would be my favoured.

some kind of bounce should come soon… however Norway first has some unfinished downside.

-if Norway sells off next days, I will get a buy-setup, together with the cycles that turn up

-if Norway bounce up next days, I will look for a bearflag-pattern that stays below 50MA, and then crash deeper in ~1 week (againt the cycles)

So in a way, down is good next days (as long as it is not armageddon, but a quick wash-out/bottom formation)

The 1987-analog for SPX would also suggest that we shouldnt crash yet, but try to hold up, and trap more bulls. If SPX sells off too quickly, we rather get capitulation, than trapping bulls and panic-buildup.

Hi John,

Thank you for the excellent analysis. For US equity, which ETF’s would you use to short equity? TIA

CT

CT I’m using a spreadbet short – something local to my part of the world – maybe US traders can recommend a short ETF

Thanks John and your contributors – all very interesting.

http://www.amateur-investor.net/Weekend_Market_Analysis_June_22_2013.htm

Thanks Fiona. That megaphone now seems achievable.

You are some kind of genius for me 🙂 Another absolutely phenomenal production :)) I wouldnt suprise if You got banned for publishing more :)) You are crushing “insiders secrets” 🙂

Thanks Grzegorz!

John, excellent analysis. Now you have me pondering whether the relationships of the typical 60’s US family is much different from the current (50 years later). Are our “old” not much better off than the old of the 60’s and in that sense won’t be such a “drag” on the spending habits of the working population? Certainly the invention of assisted living and popularity of “independent retirement” living should ease the situation as well. Of course the old are living longer and healthcare costs are skyrocketing, so it’s probably a wash in the grand scheme of things.

Of course it doesn’t help that our “young”, while declining in terms of birthrates, are costing a lot more nowadays in terms of private tuition (starting in kindergarten!), whereas in the 60’s kids were raised in a much more of a “Lord of the Flies” fashion (go play outside and don’t break anything). And when all else fails, there’s always the margin debt “Piggy bank” (pardon the pun). While it’s at historically high levels, I can’t say that there’s any basis for calling 2.5% high in absolute terms. 1987 seemed like a peak, but the ratio certainly broke out higher and doesn’t really have a natural mean reverting level. Is gambling not the epitome of misunderstanding the difference between employment and purpose? But I’m getting a bit off on a tangent now.

Just sharing some things that have me pondering. Excellent analysis. Looking forward to future research 🙂

Good points Alex, thanks for your input

Hampson has changed his tune!

Jungian synchronicity, probably! (Discovering just in time ). An amulet, a guide, or magic potion will be given to a true seeker to make sure he succeeds in his quest.

I like that!

China’s sharp rise in their Libor (Shibor?) Probably is the start of an old fashioned credit crunch. It is a mad scramble to get funds to meet overextended obligations for debt service, inventories, payroll,, etc. This just started and they usually last 9 months to a yr. This would explain the deflationary aspects of last week. Sell any and everything to raise cash. How could this be with so much liquidity. The banks won’t lend to anybody who really needs it. I think this could very well be the bursting of the China bubble. May we live in interesting times.

Opened short Hang Seng and CAC and added to Dow short this a.m. But just starter positions as protection. Would ideally like to see (and favour) a push back up as part of a more normal topping process, with which to add bigger short higher.

John, You should be careful shorting China, almost no bulls on China and all articles and experts are bearish, it is quite unusual for Emerging Markets to be below their all time highs for 5 years (since 2008), when over the long term emerging markets average 15% annualized. Emerging Markets went up 50% in 1977 and 54% in 1978 as the US markets were flat and commodities took off. Jim Rogers as of June is starting to buy China shares again.

In 1916 and 1946 no one expected inflation from the low 1% levels but both went to 20% inflation quickly as commodities peaked. Deflation followed those periods of high inflation with considerable deflation in 1920/1921 that lead to a depression and deflation in the early 1950s.

There is a lesson further back in history from 1860 to 1865, when US printed massive amounts of money, and the resulting increase in commodity prices with a blow off top in 1864. and then deflation in 1865 to 1867

John, Harry Dent’s original book The Great Boom Ahead is a good read (came out 1990/91 I believe) regarding demographics effect on the stock mkt, real estate, jobs, etc. Don’t bother with any of the books that came after that is all he was trying to do after the original was sell books.

From amalgamator to solar, from slolar to demographicycles…anyway, John is still on the fundametal/filter side of the markets, while his best gains come from simple trend following, which can be done by respecting the price action only. Combining smart fundamental analysis and smart chart reading is the recipe for best gains.

The problem with fundamentals is that you can always find and interpret fundamentals in a way that supports whatever positions you happen to have in the market.

Somebody who was long gold in February could cite negative real interest rates and ongoing QE as a reason why inflation and gold should rise further. Somebody who was short gold could argue that negative real rates have never last long historically and that QE would eventually be stopped as reasons why gold should fall soon.

And both were using the same “fundamentals”.

That’s what you see time and again in blogs discussing fundamentals.

At the end of the day, our profits (or losses) come only from “price”, and price often moves against the known fundamentals for long periods of time.

Many people criticize technical analysis because it has no basis in fact like fundamentals do. Fundamentals do appeal to logic. My snide reply to this is yes, the only thing worse than technical analysis is fundamental analysis. Look at the gold bugs, the governments are stilll printing money like crazy, therefore fundamentally it must go up, not to mention China and other central banks are buying.

I think technical trading has a similar aspect : market bias. For whatever reason – gut feeling, strong conviction, chart perception – a trader may stick to a scenario which is against the current market condition. Some may even experience a wishful market bias – because they have a position in the market, want to make a quick buck or get back the losses. Unfortunately the number of TA tool doesn’t help a trader in it: more indicators and filters means more confusion and bias in interpretation. One classic example : Anthony Cherniawski. Since 2009 Tony has been seeing a stock market crash, top, pop&drop, broadening top and plenty of reasons to short the markets and to stay short. His TA may appeal to wannabe technical traders, but to be honest I never saw in the charts what he did. It is also important – now when I share my opinion – not to read what others do and think. It will get into your mind and interfere with market interpretation, if you want it or not. Jesse Livermore begged his best friends and best traders not to give him their opinion about the market.

Yes, that’s right. Every approach, fundamental, cyclical, TA, other… has this potential problem with confirmation bias (wikipedia has a fairly good article on it).

And that’s also why taking in too much outside opinions (from friends, blogs, cnbc,..) adds to that problem. When listening to these outside sources we tend to pick up and remember those items that support our own opinion/position, while negating/avoiding those that go against us. Thus we become more entrenched in our belief in a certain market outcome.

Succes in the market does not only depend on having a very good system or model, but more so on how quick we are to realize when our good model has it wrong. The more entrenched we are in a certain belief (e.g. based on all the confirmation we have picked up from other sources), the slower we become in altering position when our model fails.

I think Bob Prechter is one of the most clear examples of somebody who has “been marrried” to his system, racking up losses for years on end while continuing to repeat his calls for the next great depression to start. Of course, if one continues to predict the same thing long enough, then one is going to be right eventually. But that’s like the proverbial broken clock.

Also I believe that people are criticizing TA for another reason : manistream well known TA is no good. All those indicators don’t work on their own, buying when it rises or selling when it is falling (=has fallen) doesn’t work either. H&S, flags, triangles on their own have 50% rate of success and profit potential which is not necessarily higher than risk. I have in my arsenal 6 types of trend waves, 5 types of corrections, few types of ranges, 4 types of my own inter-move chart patterns, few types of wave ending…and everyting must be placed in the contexts of higher time frame, action/reaction, range contraction/range expansion.The only indicator I use is Standard Deviation, but soon I won’t need it – I calculate ATR, Market Profile and Chopinness Index roughly by loooking at the price.

There is always a danger in projecting past trends into the future. The demographics that John lines out have worked in the past, but that doesn’t imply that they will keep working the same in the next decades.

To get into that question one has to ponder why and how it has worked. A large group 20-34 vs 40-54 has historically created more inflation. Why? It is not so much because the 20-34 spend more, it is because they borrow to spend. The 20-34 borrow for buying a home, a car or for studying. The 40-54 group is generally paying down its debts and trying to build a nest egg before retirement.

Now, we have to understand that it is not the Fed that increases money supply, it is private entity borrowing that increases money supply (when a loan is created the bank creates the money). And subsequently it is paying down debt that decreases the money supply (the money is destroyed when the loan is payed back).

If you have more borrowing than paying back, then there is an increasing money supply and thus increasing inflationary pressure. That’s what you usually have if there are more 20-34 than 40-54. If there is more paying down debts than new loans taken out, then you have a disinflationary/deflationary environment. That’s what you typically have when there rather few 20-34 vs 40-54.

Governments may try to fill the gap by borrowing and spending more when the private sector is in paying down debt mode, and that’s what budget deficit and QE are all about. But when governments reach the ceiling of how much they can reasonably borrow, then they are forced to stop (see Greece, Spain, etc…). At that point serious deflation can set it.

The continued working of demographics depends on the 20-34 continuing to behave like in the past. Is that the case? Well, I read recently that only some 70% of the 20-30 folks are bothering to get a driving license (a multi decade low), and more of them are continuing to live with their parents well beyond age 30. Does that tell us that the 20-34 group is borrowing for a first home or car, like their parents did? Clearly, it doesn’t. And that means that the current 20-34 group is not increasing money supply and inflation as their parents did. This group is more apparently interested in the latest smartphone, than in a car or home. Of course, that can change too.

So, the habits of the new young people are currently more deflationary. And the governments in the West have reached the ceiling of possible borrowing (especially in Japan and Europe), also setting the stage for inevitable deflation.

The US can (and probably will) continue to try more QE for several more years, and it will probably fail to generate significant inflation. Because inflation needs shortages/bottlenecks. We currently don’t have any, no labor shortages and also no commodity shortages. So, the QE money has nowhere to go but into stocks. Interest rates may rise a bit, but will not really go high given the ongoing deflation. If deflation gets worse than bonds could actually do reasonably well for several more years. And gold? It may go up or down. It will go up only if they get even more aggressive with QE and make real interest rates even more negative. Otherwise look for gold to fall below the cost of production (~$1100) first. That will prompt some miners to close mines or halt construction of new ones, which would then set the stage for higher gold prices later on (say 2020s)..

The european map of youth jobless rate is also telling in this context: http://bilbo.economicoutlook.net/blog/wp-content/uploads/2013/06/EU_Youth_UR_2012_Map.jpg

These young people are going to remain traumatized by this inability to find jobs for quite a while. So, even if the economy improves many of them are likely to be very careful with their money and will avoid debt.

Notice how countries that stayed out of the EU (Iceland, Norway, Switzerland, Turkey) are clearly doing better.

There are just so many variables in economics, it will be different but the pattern is usually similar. I believe the 4th Turning deals with how each generation reacts to the economic circumstances they grew up in. The really interesting thing is the world is facing an end to population growth in this century, probably more now than later as well. So all the patterns (cycles) we are just learning from the past few centuries, will change significantly. One of my favorite sayings come to mind, by the time I learn the rules, they change the rules!

What a great saying, but I do disagree about variables being multiple. I do believe there is one, we just have not found the least common denominator yet. All variables assumed are indirect observations, none of which change the one variable itself. They are derivatives and integrals of one another. I guess it would be like proclaiming the presence of a black hole but not being able to observe it. I do believe the one variable exists, like a black hole, and is biological in origins with a scientific component (for any one thinking I was getting theological.)

M2 and M3 are not tied directly to consumer desire (or lack of) to acquire things. M3 does incorporate the debts. Your points are correct for a gold standard concern and why it would be bad to revert. Deflation won’t occur, they’ll just change the currency system, aka change the rules as Kent said. I know for younger generation here in U.S.A., the student loan debts are slowing things down for some, but one instrument of debt (student loan) versus car loan and a mortgage is still debt.

More lending creates more deposits, which do add to M1, M2 and M3. M3 is M2 + very large deposits.

Despite trillions of QE, the M3 money supply has stayed about flat at the 15 trillion level since early 2009. See: http://www.shadowstats.com/charts/monetary-base-money-supply

QE increases the monetary base, but that doesn’t mean the money supply in the economy goes up. It will go up only if more loans are created.

Bill Mitchell’s blog is good place to learn more about the workings of monetary policy. I do not subscribe to all the ideas presented there, but it has good pieces about QE and why it fails to create inflation. http://bilbo.economicoutlook.net/blog/?p=10733

@ Danny,

“when a loan is created the bank creates the [velocity of] money”

Credit is not included in any monetary supply calculation.

We’re speaking to deposits of which credit instruments are promissory for future cashflow.

Supply doesn’t need to increase every time somebody issues a debt instrument because supply is traded for GDP.

The same M2 and M3 can remain the same whilst the “velocity of money” can increase or decrease. Your example on credit appetite and demographics changes the velocity, potentially GDP, but not the supply.

Liquidity only needs to increase during lack of trust exercises such as determining how much fits under your mattress (velocity of withdrawal). Demographics does not factor in here nor does credit.

Your example about demographics impacts the two types of inflation through aggregate demand (though you emphasize one in/deflation type) vis-a-vis supply and demand.

Bernake and co. have on more then one occasion informed that government policy is key to the demand equation also. Seeing policies contradictory to growth is one reason QE and Twist won’t have the full impact it could of had.

But creating a new loan also creates a new deposit, and that deposit gets added to M1, M2 and so on.

E.g. you borrow $1 million to buy a home. The bank puts the loan on its books and gives you a $1 million check to pay for the home. The person who sold you the home puts the $1 million in his own bank. That’s a new deposit that increases the money supply by $1 million. That’s what fractional reserve system is about. This has nothing to do with money velocity, this is about the money multiplier. See: http://bilbo.economicoutlook.net/blog/?p=14620

@ Danny – read the blog entry just for fun. I know how fractional reserve banking works. It’s how bankers turn a profit and then some (ergo CDO’s versus Mama and Papa loans).

We’ll have to agree to disagree to avoid hijacking John’s forum.

I am thinking banks are corporations and follow most likely GAAP accounting standards. Yes, they have to handle deposits and borrow on inter bank and from fed. A new Mortgage Backed Security (MBS) or credit card or other instrument of debt does not create new money. Customer deposits are a liability to the bank as the MBS note. The MBS is purchased using existing money and transferred to an account then lent out. The concept of a deposit is often confused. The QE/Fed role with MBS is re-bubbling real estate as we read this, just not realized until MBS is refinanced or asset is sold to pay off note.

http://ideas.repec.org/p/fip/fedgfe/2005-43.html

In GDP and more general terms…

Need to apply velocity of money here because the house didn’t just come out of thin air. Wages had to be paid so workers could fuel their bodies with food to have energy to work. Lumber and steel had to be made. Physical land is acquired. So your $1 million dollars created out of thin air concept is not true. That $1 million is broken up and paid on invoices to multiple companies who then turn around and pay their wages and suppliers and on and on. That is velocity, not multiplier. Demographics is the de/accelerant of the said velocity.

On an existing older home, assuming its been paid off, all you are doing is re-liquidating the past value already flowed through with velocity. Same is true when you find money once lost and found or stored in a mattress. It’s still a promissory to pay to satisfy a debt of perceived value; it just has been unaccounted for in M2/M3 for a long time while in that shoe box.

If all MBS are paid off, does M2 and M3 shrink dramatically? No, because assets still have stored perceived value (supply and demand)

QE in the U.S. is the most misunderstood thing by most investors, the press, and common folk. Part of that has to do with a need to have not just economics but accounting knowledge applied. Running a business does provide a different viewpoint. Why has money supply stayed flat? It hasn’t, it’s just not liquidated yet. Rising home prices and stock prices are such examples. In addition, most QE is held as the emergency capitalization requirements (stress testing) and not in circulation. This emergency liquidity is there for demands of money in stored value. When assets of stored value are liquidated (foreclosure), you increase money supply because the transaction isn’t so simple as a journal entry. Demand drops, due to banks not taking on risk, not having liquidity, but stored value, and new MBS cannot be made, prices for real estate drop. That’s why the fed acquires MBS to bailout banks and stabilize prices. It’s a 1:1 trade. No new money leaves, the fed just acquires the bad asset MBS and increases their capital requirements. Bank can’t relend on that loss, but they also are no longer liable in their journal entries for it. Removing the liability improves position to work with other stable banks and investors to borrow money (LIBOR) to turn around and re-lend at a higher rate of return.

http://useconomy.about.com/od/glossary/g/mortgage_securi.htm

Shadow stats only covers one type of inflation using different starting/reporting points in time. The purchasing power gauges are accurate vs the b.s. in CPI, but it’s not real inflation. It’s supply and demand manipulation.

On the small chance that a huge demographics boom or bust takes place, you may have a recession or awesome economy but the derivatives markets don’t equate to money supply. Supply can remain constant and the economy can suck due to changes in demand.

I will say one thing, CDO’s and MBS’s were in effect increasing liquidity without effecting money supply because they were not issued by the FOMC. That’s why we had the 2008 crisis. The velocity of money (liquidity changing hands) had caught the Fed with its pants down due to lack of oversight.

You should look at the velocity M2 graphic I posted yesterday to see correlation to overall economic conditions. This would be good to overlay on top of geomagnetism trends.

Norway has soon got rid of the flies in the soup (met downside target), og I am getting a bunch of potential buy-signals around Wednesday

However, if this is a crash, they may be short-lived, or fail…

The largest drawdowns in Gold Miners (BGMI) since 1970 were about 66% ending 1976, 72% ending in 1982, 74% ending in 2001, and 70% ending in 2008. Were are currently at a 65% drawdown in 2013. We are close to capitulation and a strong buy – regardless of a secular gold bull vs. bear market scenario.

Also, the CCI and CRB only dropped about 30% after the 1980 commodity top. And about the same amount after the 1951 commodity top. We are close to 30% down from 2011 in the CCI and CRB. So even if 2011 was the ultimate top, there is not much risk at this point.

Gold bubble popped in 1980 = gold stocks down 72%

Commodity bubble popped in 1980 = CCI and CRB down 30%

Doesn’t seem like much risk at this point speculating that a commodity/gold bubble is still in our future.

Hi Justin

Useful info.Thanks

Please tell us how long it took after the bottoms to make some money……years?

regards

bob

After the 1976 bottom Gold miners went up over 600% to 1981, and after the 1982 bottom they went up over 150% to 1983, and after the 2001 bottom they went up about 150% to 2003 and the 2008 bottom they went up 200% to the 2011 top.

If we are still in a long term gold bull (which I expect we are) they one could expect amazing returns in the future. The above are for Larger Cap Miners. Junior miners like the GDXJ ETF – would have even better returns.

John, excellent post. Some waves specialist (I think it was Neely) says that when humans realizes how the waves behaves, the behavior starts to change as too many people would try to take advantage of this.

Regarding inflation, I lived in South America in the late 80’s, Argentina, Brazil, Peru, etc. had hyperinflation days. My personal view is that inflation these days only happens in protected economies/countries. In those days, prior to globalization, there were import quotas, high import taxes, and some goods were prohibited to import. All the money stays in the economy and the money rotation speed increases. How did all these countries stop the hyperinflation? They just opened their economy.

Today, with open economies, money just flows out.

Thank you all.

Have updated all models this morning. The lunar positive period starts tomorrow but the geomagnetic trend still has a downward bias over the next 3 weeks.

HI John

Once again great job and i always look forward to reading your analysis and the comments from the other smart people following your site. Thank you for sharing your work! I have a question regarding Japan. Kyle Bass has studies the demographics of japan and has said – to short japan, he invited 80 of the smartest people he knows and tried to argue against this view of the demographics of japan causing the economy and the currency from falling. He has given a time frame of 18 to 24 months from now. He also said common investors can’t take part in this because the investments are very complex and he requires 5m min to invest with him. My question is if you and Kyle are looking at the same data why the different stance. I believe you are very intelligent and ask you to compare your’s and his view and i am sure other readers will look forward to seeing you analysis proving Kyle wrong or changing you mind on Japan. I know from reading you site you have no problem with going with whatever the outcomes suggests. Thanks in advance.

Fwiw, John Mauldin shared research a couple of weeks ago, and it listed Japan among the 5 countries with the worst demographics situation for the next decade (together with Hungary, France, Greece and Italy). Here is a copy: http://www.businessinsider.com/mauldin-mortgage-in-yen-2013-6

Thanks Nick. He’s been bearish on Japan for several years, betting on the yen to collapse in a sovereign debt crisis due to their world record debt-to-GDP plus ageing demographics. I certainly believe there is a chance of a bad outcome for Japan, and I have mentioned that before. And I do not suggest the demographics are anything like Brazil or India. However, Japan has a window of demographic respite (I haven’t seen Bass anywhere drill down into the demographic measures and detail), coupled with an overdue pick up in the stock market (was at p/b sub 1 late last year, demographics had already turned), and I am using a spreadbet on the nominal index, which means a dropping yen would normally mean rising stocks and my trade gaining (it is not diluted by the yen). If Japan started to lose control I won’t hang around (unprecedented Abenomics and debt). But theses are the facts: my demographic detail reveals the next couple of years to be the best demographic point for Japan (by next decade it looks bad again) and not only that but has been supressed overly long. So this is the window for gains, and I think a good chance of strong gains.

John, this is a great posting. Seems like the casual reader thinks you are moving away from solar cycles as a driver or influence over demographics. Not sure if saw my previous comment from another posting but it would great to apply globalization to this. I think Japan will be hindered by their export markets but consumption locally will keep it from being overly bad. May help prevent hyperinflation from their QE. Cheers.

Thanks wxguru. Solar cycles are one of the main causes of demographic waves, through birth rate influence, so if anything it’s a just a better understanding of solar influence. Given the globalisation, I think global demographics, of the main economic nations, are what’s important. Hence I tried to combine and weight. China has just joined USA and Europe in a united demographic down. I now consider the hyperinlation outside chance as remote.

Awesome analysis in this article. Brilliant.

Thank you

*analog*

gold miners (GDX) circa 2009-2013 vs us equity (DOW) circa 1970-1974

-if true, GDX should bottom out fairly soon and start a multi-year rally.

Norway made a quick close just below 200MA, and has been ~250 days above.

Empirical data suggest we should close at least 2% below 200MA, and probably much more.

Either with or without bounce, and this time we bounced. Normally not any long bounce… perhaps over before the weekend…