We can assess the odds of a bear market and recession ahead (with the former leading the latter), by amalgamating mutliple indicators. If you followed me on Amalgamator then you may recognise this as an exercise I’ve done before. I will mark in green those indicating no bear/recession ahead, red those that do, and leave black those in neutral territory.

1. Ten year treasury yields (over 6% is a historical marker of the end of cyclical stocks bulls) – currently less than 2%.

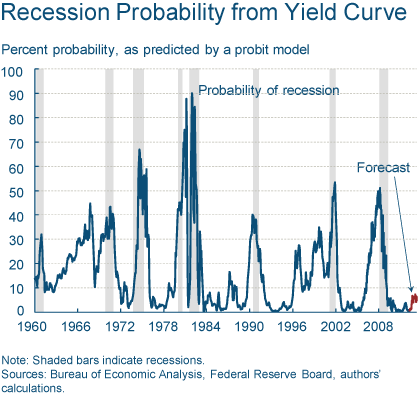

2. Yield curve / spread (if abnormal or inverted, may signal bear/recession ahead) – currently flattening but normal. Yield curve suggest negligible probability of recession.

Source: Fed Reserve Bank of Cleveland

3. Inflation rate (over 4% is a historical marker of the end of cyclical stocks bulls) – currently 2% official in the US but 5.5% by Shadowstats, so taking something inbetween as the reality, let’s mark that neutral. In Europe, official rates generally are between 2-3% and China 3.5%. Overall neutral.

4. Interest rate (overtightening of interest rates is a historical market of the end of cyclical stocks bulls and imminent recessions) – currently ZIRP in the US and negligible in the major economies.

5. Money supply and Velocity of money (both rising and positive for the most positive outlook) – in the US money supply is still in a rising trend but velocity is still falling; in the Eurozone the situation is the same; between them neutral.

6. Solar Cycles (predict secular asset peaks, growth/recessions and inflation) – one year from the solar peak we should see growthflation and pro-risk speculation as sunspots rise. A bear and recession here would be a historic anomaly.

7. Leading Economic Indicator composites of Conference Board, OECD and ECRI (trending positive or negative?) – Conference Board global LIs are mixed but weakening, OECD overall positive, ECRI for US neutral and close to zero. Overall neutral.

8. Manufacturing (this is a lead indicator, whereas GDP, income, employment and CPI are coincident or laggard) – US is weakening but still positive, Eurozone has turned negative, China still strong above 10%. Overall neutral.

Source: Calculated Risk

Source: Markit/Eurostat

Source: Taintedalpha

9. Dr. Copper (copper is a bell weather for the economy and markets) – in recent weeks copper has drooped and looks technically weak. Although the longer term trend is still in tact from around the start of the secular bull market in 2000, the near term prognosis from this Doctor is negative.

Source: TradingCharts

10. Dr. Kospi (the Kospi index is also a bellweather) – the Kospi has rallied the last couple of weeks but so far only a partial retrace of deeper falls. The 12-monthly picture is sideways. Overall a negative.

Source: Bloomberg

11. Stock Market Breadth (usually deteriorates and diverges from price into a stock market top). At the March 2012 top-to-date, we did not see the typical negative divergence in breadth that accompanies a major top, plus cyclical sectors displayed relative strength, unlike ahead of other previous major tops whereby they weakend some weeks or months ahead of the top.

12. Economic Surprises Index (is a lead indicator and also a mean reverting indicator – is it at a historic extreme, is it leading counter trend?) – Economic Surprises have typically oscillated between +50 and -50, and currently Surprises for the major economies are at -31, for the US alone -30. In the last couple of weeks they have attempted to flatten out somewhat, but until an upward trend develops, this is a negative.

Source: Bloomberg

13. Earnings (solid beat rates in both earnings and revenues, and future guidance) – in this last US earnings season quarter, the overall earnings beat rate came in around 62%, which is weaker than the historical average but better than achieved throughout 2011, whilst the spread between companies raising rather than lowering guidance was positive. Eurozone earnings upgrades versus downgrades are at neutral. Overall neutral.

Source: Thomson Reuters / Scott Barber

14. Seasonality (monthly seasonality, 4 year presidential cycle) – May to July has historically been positive, a period of lower seasonal geomagnetism. Specifically though in a US election year, a major bottom has been carved out in May-June, from which the market then rallied into the (November) election. That makes it a positive from here.

Source: Seasonalcharts

15. Bull Market Historic Internals and Historical rhymes (compare and overlay with historical precedents) – in my recent post ‘The Secular Position’ I showed that in the last 2 secular stocks bears / secular commodities bulls there were clear parallels to the current one, and that in the 1970s and 1940s our current position showed that we should be looking upwards for stocks, not downwards, in the bigger picture. Here is one more, showing the 1910s secular stocks bear / secular commodities bull – a similar picture, with some upside ahead in the next 12 months, and then some downside as the post-solar peak, post-commodity peak recession occurs. All 3 historic parallels show a positive picture for equities and commodities for the next 12 months.

Underlying Source: Stockcharts

16. Oil Price (the stock market was historically killed by a doubling of the oil price in a 12 month period) – the oil price has dropped by 10% in the last 12 months as measured at today’s price – that is a positive.

17. Real GDP growth YoY (dropping beneath 2% has invariably led to a recession) – currently just above 2% in the US, delicately poised. As the latest data marked a push up, this is neutral for now, but will be resolved one way or the other in the months ahead.

Source: Dshort

18. Stocks and commodities relative cheapness to bonds (compared to history) – currently stocks are in the historic neutral range in pricing versus bonds, whilst commodities are at extreme cheapness versus bonds. That’s overall postive for pro-risk.

19. Bond yields versus stock yields (long term government bonds yields should not exceed stocks yields by more than 6%). This has in fact inverted, with bond yields paying negative real returns.

20. Stock valuations (stocks p/es should be historically reasonable (historic US average 17)) – US currently 14, Germany 11, UK just under 10, China 7 – all historically reasonable.

21. Investor sentiment (II, AAII, Market Vane, etc, sentiment survey readings should not be overly bullish). AAII is at high bearish, which is contrarian bullish, whilst II is neutral to bearish. Overall positive for equities.

Overall, roughly half of the indicators are positive and do not support a bear and recession ahead. The remainder are mostly neutral with just three true negatives currently. Those kind of odds I will take.

To sum it up, the evironment is positive for pro-risk in terms of negligible interest rates, bonds pricing and dividends (compared to commodities and stocks respectively), and central bank supportive intervention. However, the weakening of leading indicators and economic surprises and the esclation of Euro debt has driven money again to safe havens, pending a natural improvement or central bank assitance. Should neither occur/work, then we would likely see a deterioration in the above picture and a greater likelihood of bear and recession ahead. This, however, would be anomalous to historic analogues, Presidential and solar cycles. Regardless, due to oversold/overbearish extremes in pro-risk (Euro, stocks, commodities), a period of mean reversion should come to pass. As we rally again upwards, we should print the divergences that were missing in March, if this is to be a major top. If we are not topping out here, then that mean reversion rally should be healthy in internals and accompanied by an upturn in leading indicators and surprises.

Opened a position long Euro v USD just now. Record public dollar bullishness dating back to 1999, to add to the other extremes. Holding off on other purchases until next week, due to the full moon.

While I am in some pain this morning, I am still firmly short CHF and JPY pairs. I am long the AUD and USD here against the CHF and JPY. A short USD position against AUD and CAD will follow on the back of any QE-confirmation by the Fed.

I will be adding to these positions as needed. I will close these positions once the BOJ and SNB throw in the towel, otherwise I believe they will hold critical levels (USD/JPY and EUR/CHF).

Five of your indicators are monetary which I lump into credit cycle data. It is all bullish. Being a bear, this is of great concern to me (not to mention the 60 year cycle). What I believe to be happening is the Japanese model. It used to take an inverted yield curve to stop the US economy and stock mkt so how could this clearly up sloping yield curve stop it.

After the 1990 top in Japan, the market and economy only went up when stimulus was in effect even if the credit cycle was still positive. So per Rogoff and Reinhart since 2008 we need stimulus or the economy will roll over. That’s my belief of what is happening now.

5

Kent

Again, I find your comment to be most astute, thank you

John,

It doesn’t appear you are alone in going long on the EUR/USD, according to the COT report from the CFTC. The Commercials are at an all time extreme high in net long positions on the Euro. Although this could change fairly quickly and doesn’t necessarily help in pin-pointing exact reversals, it does signal to me that the ‘smart money’ is pretty confident in the currency.

The weekly COT report gets released at about 3.30pm EST so it’ll be interesting to see how the figs differ this week.