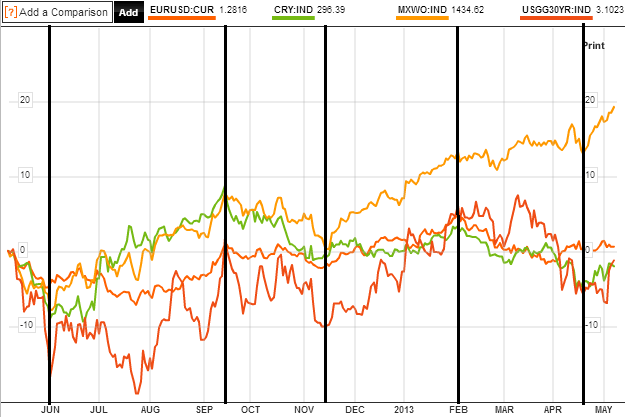

Here is the latest picture for pro-risk proxies. A new uptrend appears to have begun in late April, following an overall downtrend since the turn of February (equities traded overall sideways).

Source: Bloomberg

Source: Bloomberg

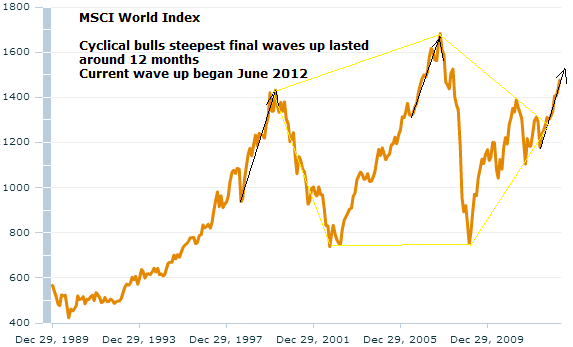

Developments are still very much in keeping with 5-models-in-alignment (this post), and if their collective forecast holds good then the next and final top should be June/July for equities. As it happens, the last two cyclical bulls in equities ended with a steep wave up lasting around 12 months:

Source: MSCI

The current wave up began June 2012 and so its termination around June 2013 would fit with the last two cyclical bulls and also the 5-models prediction.

A top right here in equities appears unlikely as divergences in breadth have been largely rectified over the past couple of weeks, which combined with breakouts in US and German stock indices, looks good for further near term gains. Plus the overall geomagnetic trend remains upward, looking out to the end of May.

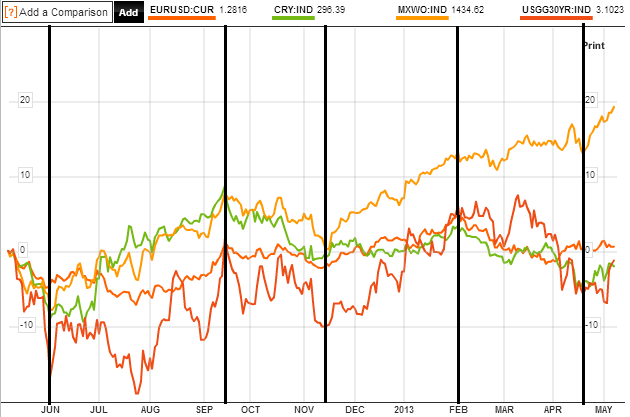

Note on the Bloomberg chart the sharp upturn in treasury bond yields over the past week, and this is also reflected in action in German bunds, UK gilts and even Japanese bonds, despite the government’s doubling of QE:

Source: Bloomberg

An interesting development. Recall the close relationship with money velocity, and the potential basing that has been occurring in both over the last 12 months. We need to see follow through on this if it is to be meaningful.

Another interesting development is in crude oil:

Crude failed at an upwards breakout attempt in mid-April, but then failed at a breakdown attempt, and has now completed a reversal of a reversal back to the top of the large triangle. Can it break out this time?

Meanwhile gold has partially retraced its falls and we see how it shapes from here. Some kind of W-base would be normal, i.e. a second low. If that is a higher low, then that would be bullish for gold.

Central banks are acting supportively for gold. Their combined gold purchases came in at record levels in 2012, and they continue to ease, devaluing currencies and cash, with both the Australian and Eurozone central banks cutting again in the last couple of weeks:

Source: Action Forex

Source: Action Forex

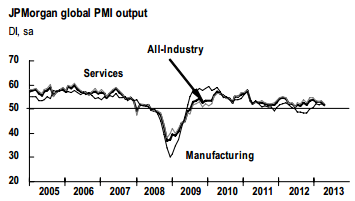

This is in response to a weakening that we have seen in economic surprises and leading indicators. Here is the latest global PMI reading, still positive (i.e. growth) but weaker than last month:

Source: Markit

Source: Markit

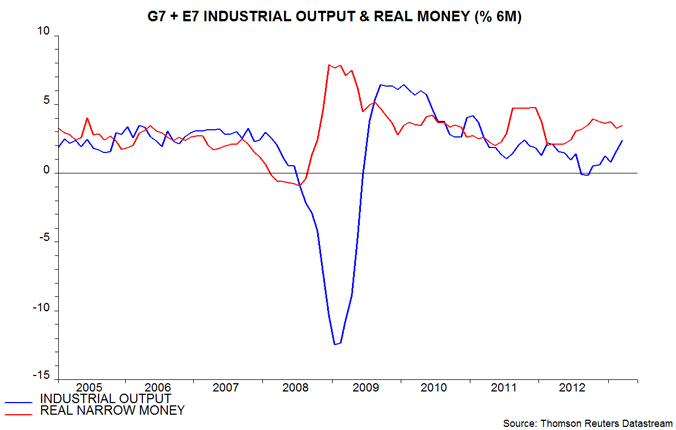

However, there are reasons to be optimistic for a renewed strengthening ahead in the global economy. Falling commodity prices over the last 6 months should have pulled down input costs giving the economy a boost. Plus, narrow money is still positive as a leading indicator of industrial production (normally by 6 months):

Source: Moneymovesmarkets

Source: Moneymovesmarkets

Furthermore, breaking down narrow money trends, emerging markets look set to outperform developed markets from here, which should produce a strengthening in emerging market industrial production:

Source: Moneymovesmarkets

Source: Moneymovesmarkets

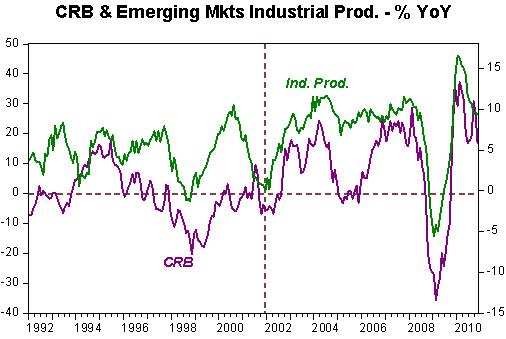

And there is historically a correlation between commodity prices and emering markets industrial production:

Source: TheFaintOfHeart

Agricultural commodities could also benefit from continued global wierding extremes. In the US, 60% of the country is in drought or dangerously dry, it is the second coldest Spring start on record, but then there is record breaking heat in the Southwest and record high river levels in the Midwest. Drought, flood, freeze and bake – really an ideal mix to decimate crops. And returning to crude, geopolitics have the potential to push oil higher if hostilities in the MiddleEast continue to escalate.

The other potential driver for commodities is the normal rotation into cyclicals at the end of a bull run. Money should switch out of defensives into oil and industrial commodities, amongst others.

One step at a time as always, but I see improving chances of my primary scenario coming good, namely that a solar-maximum inspired inflationary peak and secular commodities peak lies ahead. Sunspots have been in a solid uptrend of late, and if there is a correlation between rising sunspots into a solar maximum and speculation in the markets then speculative behaviour has certainly been in evidence. The primary scenario likelihood would be much further enhanced if treasury yields can continue to rise and with them money velocity, plus if oil can break upwards out of its triangle, and the outperformance in emerging markets and commodities takes hold. We need to see a renewed strengthening in economic data, particularly leading indicators, to provide the backdrop for speculation into risk assets. Inflation will follow if yields, velocity and commodities all rise.

In the near term I see good chances that pro-risk can rise together into June/July, so I am holding all positions for now. However, the lunar positive period ends on Monday so there is higher risk of a correction or consolidation in the subsequent fortnight.

Thanks John. Your recent posts on demographics have been fascinating. By the way, Buffett is getting bearish on bonds too, so that is some support for your short position:

“Bonds are priced artificially because you’ve got some guy buying $85 billion a month. That will change at some point, and when it does, people are going to lose a lot of money,” Warren Buffett.

Cheers Rob

Not convinced Gold has made a decent low at the moment. It was not a rounded base low, and when Gold rallies sharply out of a spike down, it loses momentum and falls lower from there.

Gold miners and silver have made rather weak retracements so far too.

I think crude prices will be an important tell of the intermediate outlook. It’s interesting that prices have tapped the upper trend line three times already this year, which is a divergence from the 2010/11/12 petro business cycle theory. If crude can break up it would lend good evidence to your growthflationary finale thesis.

John,

I am thinking about putting calendar spread slowly. May be 1/5th at a time as we start seeing this theory pan out.

So we can sell some jun/july options and hold on aug/sep option.

Do the reverse for commodity. Do you have any etf in mind which will be best suited to play. How about GLD,SLV or ?????

Oil useage is down. It was over 50% of energy in the US and now around 33%. Supplies are rising sharply. The question is when.

Thank you guys. Yes an upward break in crude against a backdrop of high inventories would be something, if it occurs.

Which ETF? Gold should be the leading asset if this is to be the conclusion of K-winter. But most commodities should participate if my solar-secular finale prediction is to occur.

C-Pu sees the commodities rally: http://www.financialsense.com/contributors/chris-puplava/easy-depressed-when-no-one-loves-you

Not the first I have read on this, but still interesting given reference to demographics

http://www.telegraph.co.uk/finance/comment/10044456/China-may-not-overtake-America-this-century-after-all.html

Thanks wxguru

Great info, just please don’t short treasuries for your own sanity. Play the move through indirect sources. 30-year should drop below 2 within the next two years, and people have continued shorting through the down trend. Wait to 2014-2020 to start any treasury shorts.

Too late Sam! I am short treasuries – though not a full position at this point. But drawing on (secular/solar) history a repeat would be that the top is already in – whilst acknowledging there should be another bounce circa 2014. We’ll see.

Bonds look very similar to gold last year. Hanging around or just below a flattened out 200 day moving avg after a prolonged secular bull mkt. It’s certainly in a position to break down and the last week has been bearish. That would mean the markets have somehow taken over. That would be a shocking paradigm shift to all the bulls and the hedge fund boys.