Four demographic measures have been demonstrated to have a correlation with economic, stock market and real estate market performance: middle to young ratio (35-49 year olds versus 20-34 year olds), middle to old ratio (35-49 year olds versus 60-69 year olds), percentage of net investors (35-39 year olds versus the whole population), and dependency ratio when inverted (0-14 year olds plus 65s and over versus 15-64 year olds). Using the population pyramids based on the United Nations 2011 population data and projections I have modeled 24 countries on all four measures and you can see these charts on my new Demographics page HERE.

The data points are 5-yearly and I have modeled the period from 1995 through to 2050, so that we can see the trend leading into our current point in time and the projections forward. Based on the wider research on my site, my forecast is for a secular transition to a new K-Spring from the period around 2013’s solar maximum, namely that secular bull markets in bonds and commodities should give way to new secular bull markets in stocks and real estate in a gradual transition, with the first phase of momentum in stocks likely from around 2015 through to the next solar maximum of around 2025. By my recent analysis, not all major countries around the world will participate in secular stocks bulls in that period, as those with particular negative demographic trends are likely to miss out. The strongest secular stocks bulls should be in those nations with particularly positive demographics based on the four measures.

So let me cut to the conclusions from the data. Those countries with the strongest demographics 2015-2025 out of the 24 modeled are South Africa, Nigeria, Poland, Russia, India, Turkey, Brazil, India, Malaysia and Indonesia (with at least 3 out of 4 measures trending positive). Those countries with the weakest demographics 2015-2025, and likely to struggle to carve out secular bull markets in equities, are China, France, Spain, Germany, Italy, Australia/New Zealand and Canada (with at least 3 out of 4 measures trending negative). And lastly those that are in between (more ‘neutral’ demographics) are USA, UK, Mexico, Canada, UAE, Ireland, Vietnam and Japan.

Therefore, based on demographics, the best returns for equities are likely to come in East Europe, South America, South Asia, ASEAN and Africa. Unimpressive returns should be made overall in the ‘developed’ world, with Western Europe perhaps struggling the most. Out of the top 10 largest economies in the world, we might expect Brazil, India and Russia to play a greater role in pulling the world economy and stock markets along, whilst China, Germany and France may be dragging their heels.

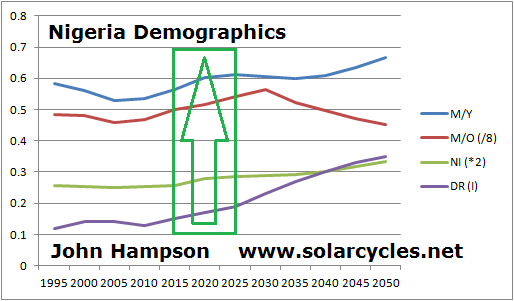

Compare Nigeria and France, at opposite ends of the demographic trend spectrum. Here is Nigeria, showing all four demographic measures (which have been scaled to share the same chart) trending positive between 2015 and 2025.

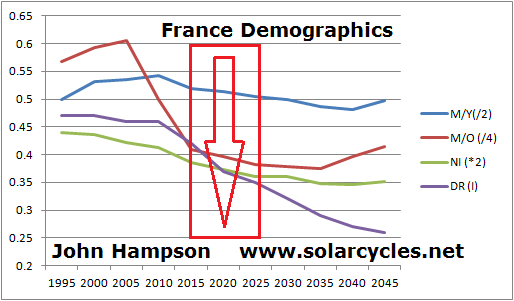

And here is France, with all four measures trending negative in the same period:

And here is France, with all four measures trending negative in the same period:

Some potential investment vehicles to capture the best demographics would be Spdr S&P Emerging Europe which is Russia(56%)-Turkey(23%)-Poland(13%), or Market Vectors Africa ETF with the two largest country holdings Nigeria and South Africa, or Advanced Frontier Markets ETF whose biggest holdings are Nigeria, Vietnam and Gulf countries, together with smaller holdings in many of the less accessible countries with better demographics. There are multiple investment options for the bigger countries such as India and Brazil. Beware ’emerging markets’ ETFs as they often include China, Taiwan and others.

Some potential investment vehicles to capture the best demographics would be Spdr S&P Emerging Europe which is Russia(56%)-Turkey(23%)-Poland(13%), or Market Vectors Africa ETF with the two largest country holdings Nigeria and South Africa, or Advanced Frontier Markets ETF whose biggest holdings are Nigeria, Vietnam and Gulf countries, together with smaller holdings in many of the less accessible countries with better demographics. There are multiple investment options for the bigger countries such as India and Brazil. Beware ’emerging markets’ ETFs as they often include China, Taiwan and others.

If my primary forecast plays out for a secular commodities peak then a cyclical stocks bear and mild recession before a momentum ‘go’ point as of 2014-15 then the opportunity to load in to these stock markets may not be until then. However, I may be wrong with the timeline of developments, and not all markets will take off at the same point, so another consideration would be which of those positive-demographic markets are currently ‘cheap’ and therefore unlikely to be at risk of much price downside. The cheapest current by p/e include Turkey 12, Poland 10, and Russia at 5.6 with a 4.6 yield. Alternatively, Japan’s stock market appears to have technically broken into a new secular bull already and is belatedly catching up with demographics which turned upwards (not all 4 measures) as of around 2005, so I suspect could already be a buy.

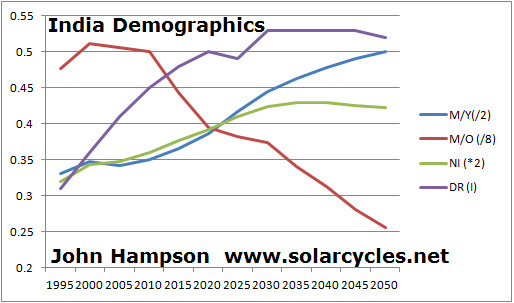

Many of the ’emerging’ markets in the positive demographic list look similar to this, India’s combined chart:

Three positive trends and one negative, with the negative being the middle-old ratio. This is because until recently people in relatively poorer nations rarely reached old age. In the first half of this century they should see an increasing amount of people reaching old age and therefore the ratio versus the middle aged goes from negligible to something of significance. Nonetheless, the old age populations in these developing nations largely does not become problematic until much further out, unlike the large relative numbers reaching old age in many developed countries as of now.

Three positive trends and one negative, with the negative being the middle-old ratio. This is because until recently people in relatively poorer nations rarely reached old age. In the first half of this century they should see an increasing amount of people reaching old age and therefore the ratio versus the middle aged goes from negligible to something of significance. Nonetheless, the old age populations in these developing nations largely does not become problematic until much further out, unlike the large relative numbers reaching old age in many developed countries as of now.

Great post. Thank you for sharing.

Thanks Cesar

Thank you John… covering such a wide breadth of factors effecting markets and your integrative perspective is not merely remarkable. It is a gift. So smart… much appreciated…

Thanks HVA

“Those countries with the weakest demographics 2015-2025, and likely to struggle to carve out secular bull markets in equities, are …Canada…”

“And lastly those that are in between (more ‘neutral’ demographics) are…Canada…”

???

Apologies – Canada is in between – rather than bad.

All solar models updated this morning.

May want to check this out John. Milken Inst. Global Conference – Investing in African Prosperity:

Thanks

John,

What is your take on volatility? We are at historical lows here and its been going down for a long time. Do you think it might explode going forward?

Thanks.

Yes, interesting. Long the volatility index ought to come good, but just as per short equities, it’s about getting the timing right. Volatility stayed low for 4 years in the 90s and again in the 00s. Can’t yet totally rule out a new secular stocks bull is underway (though I think unlikely) which would keep the measure depressed.

Excelent post. I also think that the demographics is also the reason for Peru’s economic growth, probably for another 15 years.

Thanks

Politics that can alter demographics. Soros loses the argument which only shows his real intentions.

http://www.project-syndicate.org/commentary/soros-versus-sinn–the-german-question