Let’s start with Economic Surprises. G10 nations:

Source: Bloomberg / Citigroup

And Emerging Markets:

Source: Bloomberg / Citigroup

The message is one of improvement in actual data versus expectations.

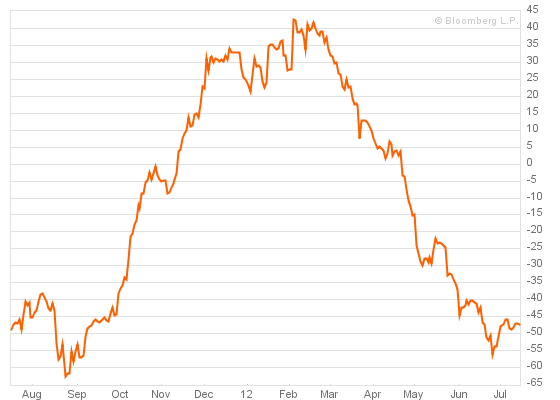

Next, leading indicators. Here is the latest Conference Board summary:

Source: Conference Board

The message is one of continued negativity. ECRI US leading indicators made an uptick on Friday but one week doesn’t make a trend, and it came on the heels of another ECRI media appearance reaffirming their call that the US is in recession. Scott Grannis made a compelling case in response as to why the US isn’t in recession here.

Next, Euro debt. Here are Portugal, Greece, Spain and Italy CDSs:

Source: Acting Man

And here France, Belgium, Japan and Ireland:

Source: Acting Man

There has been general improvement since the Euro summit outputs, in that French, Spanish and Italian CDSs have all fallen back the last 4 weeks. Only Greek CDSs are notably rising again.

Now let’s turn to geomagnetism and sunspots. All models have been updated this morning. There was a big geomagnetic storm the last 2 days (circled on the chart below) and there is another siginificant episode predicted all the way through from the 27th July to the 4th August.

This is higher geomagnetism than is seasonally expected, and the result is that my short and medium term models continue to trend downwards. There is neutral pressure into this Thursday’s new moon but thereafter downward pressure erupts.

On the flip side, sunspots continue their general trend upwards which is a positive.

Next, US earnings. Goldman report today and we will see other big names this week. Only one third of companies have beaten estimates so far, but we need to see the bigger volume of reports this week to get a better feel of the beat rate. So far though, earnings are a negative.

Turning to central bank intervention, Bernanke is scheduled to speak today and the markets are again looking for clues as to whether more stimulus is likely. August 1 is the next FOMC outputs. Otherwise, central banks around the world continue a theme of more easing and stimulus, but there is a new threat to this in that soft commodities have been sharply acccelerating, particularly grains. In emerging markets especially, this is likely to translate into inflation in H2 2012, which may impede further easing. So let’s finally turn to agri commodities.

Soft commodities, particularly grains, have been experiencing a supply-side push due to global wierding. The global climate report for June is in and it was the hottest global June on land on record, as shown below. This follows the hottest May on land on record and the second hottest April on land on record.

Source: NOAA

In July so far, the heat and drought extremes persist. El Nino should develop as the summer progresses which could ease these issues, but El Nino also brings it own problems. For now, grains are surging in price and are threatening their previous two major highs of 2008 and 2010/11. Danske predicts that the UN food price index will accordingly shoot up in H2 2012 to a new high. If that occurs, it will be highly significant in support of a secular commodities peak ahead rather than already occurred in 2011.

Source: Danske Bank

So let me summarise. Economic surprises and Euro debt both appear to be turning in favour of pro-risk. Meanwhile, leading indicators continue to point red, but global policy responses also continue, with the likelihood that at some point leading indicators will improve as a result. However, recent soft commodity price rises may be about to close the window on easing. US earnings gather pace this week and by Friday we should have a better feel for whether they are likely to be a drag on the markets over the next few weeks. Geomagnetism is currently higher than is seasonal, and should be a downward pull on pro-risk after the end of this week. Sunspots, however, continue to rise in an overall trend, and should encourage speculation into commodities.

Trading-wise, I am leaning towards a little more upside in pro-risk into this Thursday’s new moon, due to the technical picture on most charts. Should that occur, I will take some profits off the table. The FOMC is an unknown, however Bernanke could telegraph his intentions as early as today. If he sticks with no further action then the markets may protest again.

I have focussed on the macro today, but technical indicators continue to show excess bullishness in treasuries and dollar and excess bearishness in the Euro (plus a positive divergence) and excess bearishness in precious metals. What this means is that a move the other way is ripe, subject to supportive developments. In other words, some evidence of improvement in leading indicators, some dovish noises from Bernanke or some big US earnings beats could all set the scene for a more enduring pro-risk rally. Without improvement in these three areas, the danger is the current pro-risk rally tops out again.

Morning John

An interesting few days ahead.

As we discussed the other day my model suggests downward pressure into the 18th July down towards 1332 or lower whilst the lunar wave suggests upward pressure into the 19th. Now, in fact, last Friday we did fall into the 20’s and so I bought back my bear(posted on my blog) so things could just about satisfy both if we rally above 1373 by the 19th.

It seems that if we get to the 19th and we are at these levels or lower(1358) then we have an unusual inversion, and recent analysis suggests it is better to buy on the next full moon rather than now – which could be much lower. If we can get to that date at 1373 or higher then the normal rhythm is in place and continuing improving macros will be supportive of pro risk.

The top of this rising,expanding wedge is about 1390.

Cheers Will.

Gary also reminded me of the 28/7 Bradley date: