Let’s now draw in the solar cycle. Here are US equity valuations by Q ratio versus solar maxima over the last century. A relation becomes apparent with secular lows and highs.

Source: D Short

We can see three that don’t fit so well. The 1929 stocks peak extended over a year beyond the SC16 peak, stocks sailed through the 1957 solar max and whilst the SC22 peak wasn’t so significant for US stocks it turned out the secular peak for the Nikkei.

Now for the three secular ‘lows’ on the above chart (SC15, 18 and 21) we can cross reference to long term commodity prices and see that they instead marked secular highs in hard assets. Similarly, the secular stocks highs of SC23 and SC20 maxima marked secular commodities lows.

Solar science reveals peaks in human excitement at solar maxima (e.g. clusters of war). In the financial markets this appears to translate as peaks in speculation (and in the economy in peak activity). Therefore, it appears that the asset in favour at the time is bid up to a secular peak and subsequent pop around the solar max (with the rare exception, as with any indicator or discipline). So what would make the favoured asset stocks rather than commodities or vice versa?

Solar science reveals peaks in human excitement at solar maxima (e.g. clusters of war). In the financial markets this appears to translate as peaks in speculation (and in the economy in peak activity). Therefore, it appears that the asset in favour at the time is bid up to a secular peak and subsequent pop around the solar max (with the rare exception, as with any indicator or discipline). So what would make the favoured asset stocks rather than commodities or vice versa?

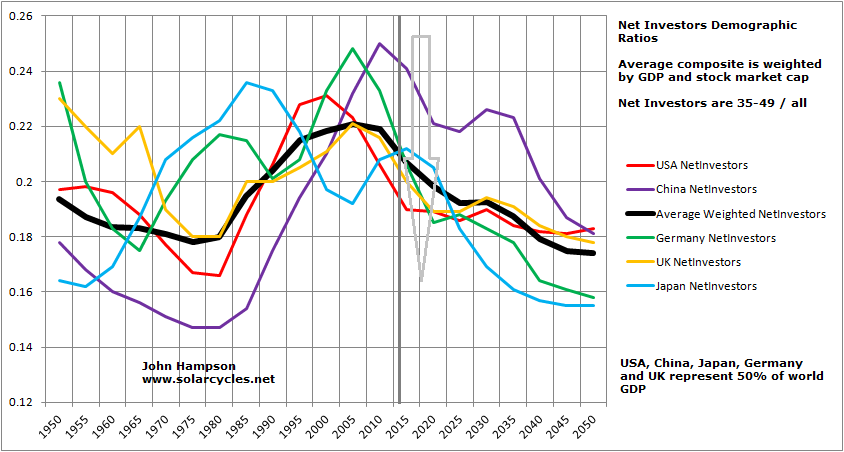

The evidence suggests it is demographics, namely that secular = demographic. The chart below reveals equity valuations tracking US demographics and gold moving in opposite directions. Therefore we see a secular peak in gold at the demographic low and a secular peak in stocks at the demographic high.

The picture is enhanced when we discover that solar cycles influence birth rates, which may account for why demographic peaks often tie in with solar peaks.

The chart below shows how Japanese demographics peaked out first in the late 1980s, which explains why Japanese equities made their secular peak at the 1989 solar max whilst other major nation stock markets continued to advance under positive demographics.

The current relevance of the chart is that the global demographic composite is definitively negative, and this is echoed in other demographic variants. Together they spell recessionary and deflationary pressures, which we are seeing in reality. But they also should be sinking equities and launching gold, which we are not (currently) seeing. More on that shortly.

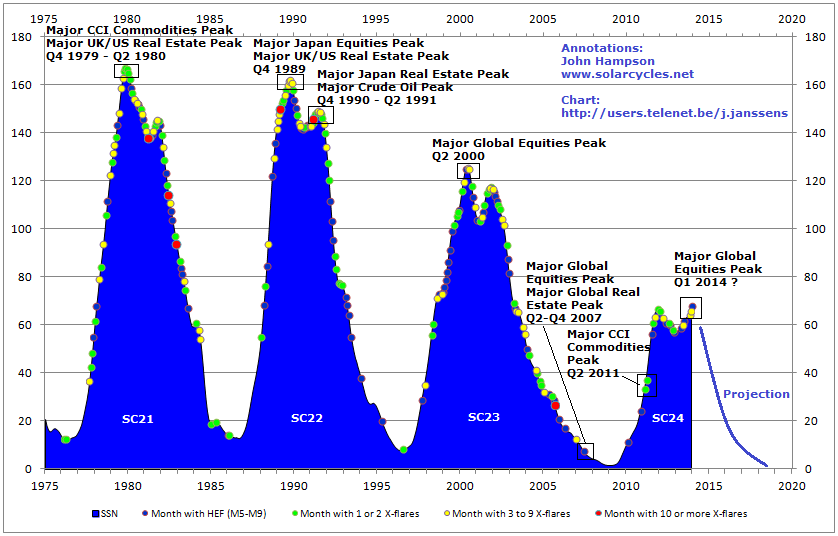

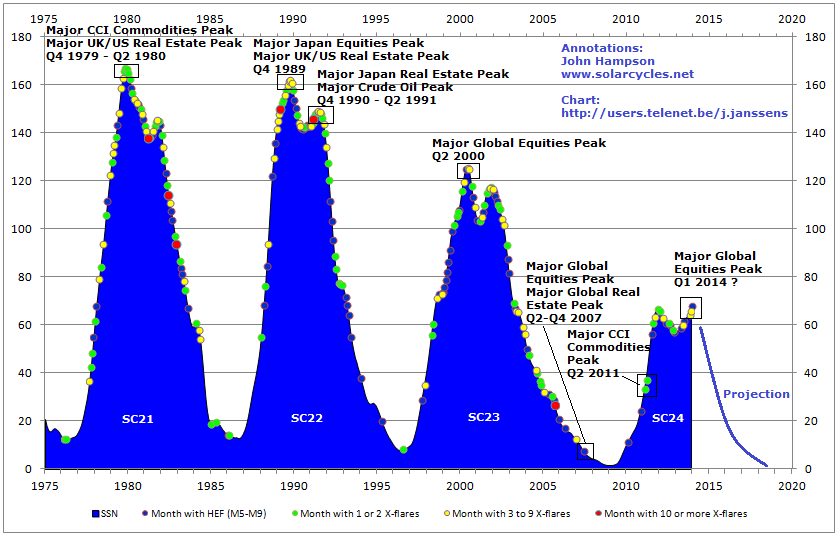

Solar cycles are long cycles, but armed with the above information we got the chance for a real time test with the SC24 max, which now appears to have been centred around April 2014 (smoothed max).

Two things were anomalous about the SC24 max. It was lower intensity (less sunspots overall) and it took longer to form (including a higher second peak).

The average duration between solar maxima is 11 years 1 month, but the SC24 max didn’t form until 14 years 1 month after the SC23 max, which makes it an outlier. Is this relevant? Well, a major commodities peak occurred in April 2011, exactly 11 years 1 month after the SC23 max.

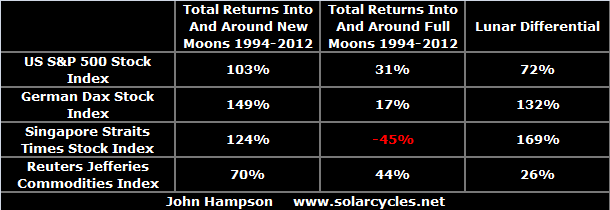

Tangent for a moment. Here is the influence of the lunar phase cycle on the markets: it makes for a fortnightly oscillation with distinct measurable returns over time.

The most plausible explanation is the influence of nocturnal illumination levels on evolving humans. Yet, the influence is still present despite living under artificial lighting for several generations. Therefore it would appear to be hardcoded to some degree: we oscillate internally with the moon cycle, to some extent. Might the solar cycle also be to some degree hardcoded? If so, that could be a factor in the major speculative commodities peak (and associated major stocks low) in 2011, i.e. human excitement to some degree peaked into the anticipated/internalised solar max.

Source: Stockcharts

The case for that increases if we look at ‘leveraged’ commodity silver. The same kind of parabolic blow off as in 1980 occurred.

It would make the secular commodities bull 2000-2011 a mirror of the 1968-1980 bull, namely one solar cycle in length and set against a secular stocks bear, and both in keeping with demographic trends of the time. The implication would then be that commodities are now in a secular bear and stocks are in a new secular bull.

But let’s now look at the real experienced solar max of April 2014. From 2011 to 2014 stocks rallied strongly and since the start of 2013 displayed characteristics of a mania. A snapshot at April 2014 reveals many typical signs of a major market peak: extremes in valuation, sentiment, allocations and leverage; record negative earnings guidance and economic surprises all negative in the major nations; divergences in money flows and various risk-off measures; outperformance of defensive sectors and bonds; etc. At the time I gathered together 40 indicators all with different angles on a telltale top in stocks. Really, the evidence could not have been better for a speculative mania into the solar max.

However, as we passed through the real solar max, it was commodities that fell again, rather than stocks. An oil-heavy commodity index, used for emphasis, shown here:

Source: Stockcharts

Indeed, by the end of March 2014 large speculators had amassed an all-time record long position in the CRB commodities index, suspiciously right at the solar max. So we have a potential case here for commodities to have effectively made a double secular peak between the ‘average’ and ‘real’ solar maxima.

But… things get more complicated when we look under the hood at equities. Stocks:dollar, stocks:bonds, volatility, breadth and various other measures not only resemble previous major peaks but occurred together very close to the real solar max.

We are now waiting to see whether these will be repaired or whether nominal equity prices now fall in line. If the latter, then we have the evidence that speculation in equities peaked at the real solar max. At the same time, gold has been forming a technical bottom in recent months together supported by washout sentiment and allocation levels, which after a 4 year bear suggest it is ripe to break into a new bull. Which brings us back to demographic trends being aligned to stocks declining and gold rising: this angle on what happened would argue that the anomaly in hardcoded/real solar max produced a second speculative peak against demographic trends and in stocks, only for demographic trends to now reassert themselves (stocks complete the secular bear, as suggested in the last post, whilst gold goes to new highs).

As alluded to in the last post, the closest fit historically to the current time was the peak of 1937: a solar maximum and speculative peak against a backdrop of low rates and easy conditions. Equities peaked out at high valuation (see Q ratio chart at top of page for SC17), following a front-running of prices to an expected return to normal growth that didn’t materialise. If there was any doubt this isn’t being repeated today, take a look at how analysts continually expected bond yields to rise over the last several years. Reality (demographics) has persistently denied them.

Source: Mike Sankowski

Source: Mike Sankowski

In 1937, both equities and commodities rallied into the solar max of April and both topped out around then, falling sharply for the next 12 months with both deflation and recession occurring.

Stocks didn’t make a real (inflation adjusted or valuation) bottom until 5 years later.

Which brings me back to the unfinished business in equities and the prediction by both demographics and valuations:

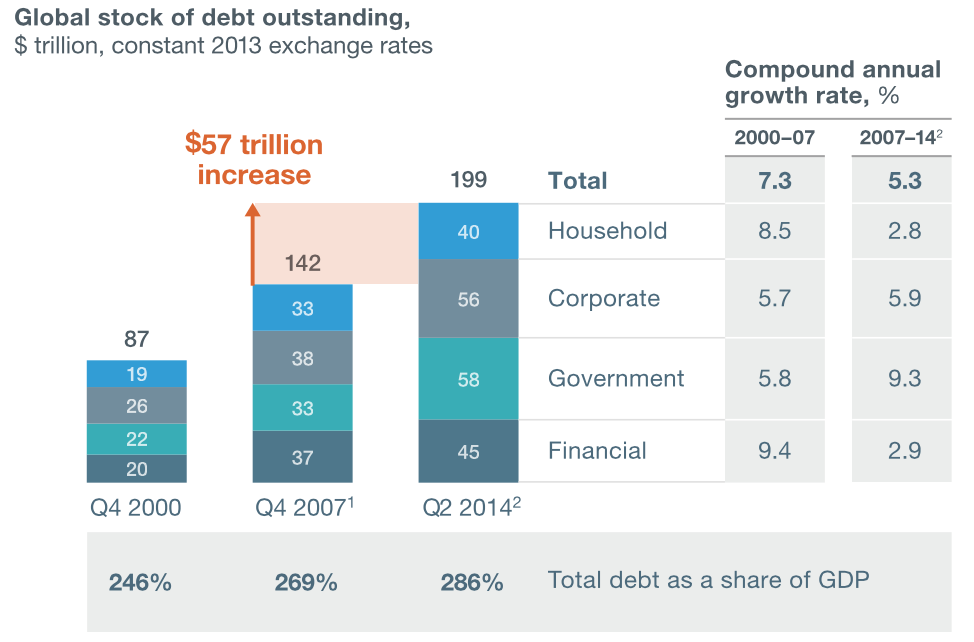

In summary, from all the topping indicators in equities, stocks should now break into a bear market, tipping the fragile world economy fully into both deflation and recession. There should be a feedback looping between the two, taking stocks down to much more appropriate washout valuation levels, whilst crises breed crises again in the economy. As in 1937, it should kick off under easy monetary conditions, limiting the toolkit of central banks, but also as then, central banks will likely resort to unorthodox (and probably ruthless) tactics. Systemic breakdown is a real risk again, with debt levels greater than in the Great Recession (hat tip Sinuhet).

Source: McKinsey

Commodities (particularly industrial) should sink again too, but likely for shorter and shallower (in line with demographic pressures, as per 1937, and understanding their existing slide since 2011). However, I expect gold to break away and rally as real money. It’s not an easy call due to the limited history of gold free-floating and performing under deflationary conditions. But ultimately I maintain it is the anti-demographic ultimate safe haven, and should regain favour particularly as central banks are currently doing their best to corrupt the money mechanism with QE and ZIRP.

If I’m wrong? Well, this is where we get to the ultimate conundrum. If stocks are instead in a new secular bull (and commodities made their secular peak in 2011, doubled down in 2014) then the appropriate investments/trades are really the opposite of if they are on the cusp of a new devastating bear in an ongoing secular bear. Long stocks and short gold versus short stocks and long gold. I have been able to make cases for both in the last two posts, but I have also shown the flaws in both.

Ultimately it’s a game of probabilities. When all crunched together I see it as most likely that 40 topping indicators and an under-the-hood peak around the smoothed solar max of last year should produce an imminent meaningful correction in stocks unless those divergences start to be repaired. That would be the telling clue. Fitting with that I see gold’s technical basing as likely to produce a meaningful rally. From there I would expect to see serious troublespots emerging in the global economy (defaults, etc) and the meaningful correction in equities turn into a fully fledged bear. However, if the secular stocks bull scenario were to turn out true, then indicators should point to a recovery in equities before we hit such problems.

I have to end on a sobering note. If we do see a global bear market and recession here, then the damage will be immense. No capacity to reduce rates, QE proven to be a failure, record debt levels and increasing under deflation, and no demographic upturn in sight for some time. Accordingly, central bank response would have to get tough, such as penalising any saving, imposing capital flow controls or protectionism. The potential for civil unrest, war or systemic breakdown would increase. The outlook would be very uncertain but surely bleak for the majority of people for the period ahead. It would really be in mankind’s interest for the new secular stocks bull scenario to be true. However, both the debt and demographic problems that we now face can both be traced back to the second world war. They have been a long time growing and attempts to conceal or water down their impact cannot go on indefinitely. Printing money to buy your own debt is normally the end game, so it’s not realistic to expect ‘muddle through’ can keep going. It comes down to the complications of gauging how the end game plays out.

Probably philosophic comments aren’t this sites bag. Anyway here goes. You could ask why people have or don’t have children, why are they optimistic or pessimistic at different times. In my opinion most thoughts are collective. We are much more Lemming like than we like to think. Collective consciousness guides what happens and the criminal manipulation of the ruling class will not change what the mass mind feels. Onlywhen it is safe to borrow and take risk will the economy grow. This collective mind is boundless and influenced by events in space as much as here on earth. John is correct in the details – lets see how it plays out.

Does socialism, big government and the erosion of family values result in smaller families?

John,

What you describe is very typical w5 behavior. Solving the debt problem by creating more debt can only happen in w5. Strong divergences are also typical for w5.

Some people think the 19 year cycle ended in 2007. But the Qe-madness only started in 2008, kicking off w5.

My own theory is that the 19 year cycle was up until now. This is not based on curve fitting but on causal relations with solunar events. If this happens to be correct it would explain what we are seeing. It would also indicate time is up. The exact date for this long cycle would be June 16th.

No trading advice; just my thoughts.

Soon we’ll know.

André

in the bear market scenario you describe John: “central bank response would have to get tough, such as penalising any saving, imposing capital flow controls or protectionism…”

how dangerous do you think it is to hold cash and where would the safest place be to put money, gold, property etc

I think Russell Napier knows best in that area. He predicts strong-arming into government bonds, limitation or prevention of capital flows out of the country, and effective confiscation of cash as they do all they can to get the economy going, and gold to regain favour. We also know money is a game of confidence and central banks are doing all they can to undermine that confidence. Personally, I think right now cash seems prudent whilst we see where things are headed, as it’s agile. But it’s not clear which currencies will do well from here, so holding in more than one currency seems prudent too. Under a deflationary recession stocks, real estate and industrial commodities should all decline. Gold arguably should be the outperformer, and cash should rise in value, but likely some currencies will be punished. For me both hard and useful assets appeal under that scenario too. Got to think what’s important.

Fascinating analysis in this post.

I’m sure the bear is just around the corner, given a year long topping process has already occurred.

I think the bear will be short and sharp (couple of years) and that the ECB will use gold to save the system, and keep the Euro zone together.

Then we’ll enter an inflationary cycle which will see the world change in many ways, all for the better. But so much turmoil to get through and out the other side.

Good luck to us all.

GM, a “couple of years” is considered long. Well at least Yellen defines a couple as more than two? 1929 was three years, 2000 was three years, most crashes are 1-2 years.

6/15 7:43 adding another price target – 2094. (targets are 2094 and 2100)

6/15 9:39 Lab 7442 showing current wave with overshoot to 2073 and next high at 2102. http://www.ustream.tv/channel/7442-analytics

When 2081 is reached, one of 2 things happen – either upwave to 2100-2102 starts or overshoot happens before upwave begins.

am leaving early today – the big picture Spiral is up to 6/20 (I believe the high will be in 6/18) and then down to 7/2.

time stamp for the above is 6/15 10:52 ET

Peggy, just to confirm, you are quoting Eastern Time in your time stamps?

yes

Thanks for the great follow up, Peggy.

Thanks Peggy

This is the time. From 2015 to 2016 (bottom), if my estimates are right, global economies ´ll enter in a recession and US indices could have a severe corrections, similar to 1917 or 1921, +- -0,76 fib. In Europe about -50% gains.

Thanks for your effort, John

Sunday, June 14 is Mars conjunction (Mars — Sun — Earth). Mars being on the exact opposite side of the solar system from earth has maximum effect. Mars has the effect of lower prices imo and based upon a quick look at previous 20 years of data.

Lunar Chord:

Phase: bullish new moon week

Distance: bearish, distance of moon is increasing all week

Declination: bearish, next 3 days

Seasonals: weak tomorrow, strong Tuesday to Friday

Summary: am short the SP500 at this time but going to cash as new moon and op ex week are not good shorting environment. This said tomorrow “could be” one of those new moon sell offs of size.

JH, the markets are certainly frustrating. Even though SP500 and DAX are down, the high fliers that ought to correct, such as IBB/IWM are still above their moving averages. I am torn between following the signal from SPX/DAX/TRAN versus the stubbornness of IBB/IWM/SHCOMP.

How are you positioned? Is the strategy to wait and see if the internals somehow correct themselves, before putting a larger position?

JLi, if others such as IWM are holding strong and even still rising while SPX has been declining since late May, then this is a sign of strong bullish divergence. Those leaders will continue to lead even more strongly if/when SPX gets out of its funk and rallies.

Keep in mind that IWM essentially traded close to flat for the entire 2014 year while SPX soared during that same time period.

What is the difference between a bullish divergence and a bearish divergence anyway? There are others who say that TRAN is lagging, and so it is a bearish divergence.

Obviously the bullish divergence is an indicator of further upside and vice versa for bearish divergence.

Another example is how NDX took out the Feb 2015 high convincingly in Apr, whereas SPX only retested that same high. This foreshadowed in the future that technology stocks were poised to outperform traditional stocks and this is indeed the case. SPX close today is -1.6% from its Feb 2015 peak whereas NDX close today is -0.8%.

The Nikkei outperformed the SPX 1/1990. Would that be a bullish divergence? Because it then tanked from there.

On a slightly different timeframe, just went long DAX at 10986 as I deem it a tradeable bounce potentially. Stop below LOD.

J

“The average duration between solar maxima is 11 years 1 month, but the SC24 max didn’t form until 14 years 1 month after the SC23 max, which makes it an outlier. Is this relevant?”

There were at least two lengthy periods during the past 1600 years, covering at least ten solar cycles, where the max-to-max duration averaged 14 years (one of which was the Maunder Minimum – so get ready for colder temperatures).

There is nothing particularly unusual about the timing of SC24: it is just a typical weak cycle – so typical in fact, that it is not easy to distinguish it from the others. The charts shown by Chien-Jen under the previous post illustrate just how typical it is.

VIX confirms the significant top. But another is needed, at least a genuine double top, but not for some several months, maybe years for much higher.

I am confused if you are saying SPX topped or VIX topped.

Reason for bearishness until 8/10. 6 out of 11 times if you had shorted the sp500 two months before Venus inferior conjunction (this year 8/10/2015) with a 10% profit target you would have hit the target. The other 5 times 3 were break even, and 2 were 10% losers. The next benefit of this strategy, if long taken when 10% target achieved would be outperform buy and hold by 6 times 10% times 2 (short and long combined profit) or 120% minus 20% loser or 100%. Not bad considering this is 16 years or 182 months and this strategy only represents 22 months of the total. Conversely, from inferior conjunction of Venus forward is bullish. Having a bearish bias until 8/10 has some astro basis.

On a astro viewing note, Venus appears super bright and high in the sky at dusk and slowly falls to the western horizon. For the next two months it will fall each night by 2% until on 8/10 it will set at the same time as the sun. No, the sun isn’t eating the planet, it just looks that way.

thanks, great info—is that called heliacal setting of Venus, what happens in Aug?

Exactly so. One of the most important 2 months of about a 16 month cycle is about to unfold. Of all of the planets Venus has the size to really effect things, Mercury has effects but Venus imo even more.

I found the data in this article most troubling. People seem so fixated on the GDP and other economic numbers and it seems to be that GDP for one and inflation for another are political vehicles and so distorted that is hard to make much of them.

I certainly trust the cycles of the sun and the moon and the planets MUCH more than the engineering that seems to have been done on these government statistics…

Below is an eye opening analysis on GDP, Earnings and markets data from 1871. The results are astounding to me if not terribly scary. Would love to know your thoughts….

As always thanks for your great work,

http://mcm-ct.com/blog/imaginary-numbers-part-2-the-shattering-mirror-of-the-centrally-planned-monster/

I wanted to add one thing…when I was referring to find the data in “This article” troubling i am referring to the article about GDP and US data….not yours. Although, I have a feeling of significant doubt with regard to the veracity of implications that derive from potential highly inaccurate data represented in the US GDP and CPI data. Just wanted to make sure to say that…

I am most interested in the cycles that are in play because it seems to me that the data and the markets are being significantly influenced by special interests. Cycles are likely to influence these actors even though it seems that they do not know it yet.

6/15 10:15 back in the office. significant changes as per Lab 7442 Live – next target is 2041. Downtrend begins again at 6:50 ET. Lab 7442 is the expert, not me. http://www.ustream.tv/channel/7442-analytics

Peggy – Are we still in a uptrend? Your posts on Monday indicated Spiral big picture was indicating an uptrend till 6/20. Is this still the case?

6/16 7:57 6/20 is the larger cycle high. The short term cycles pinpoint the high. The next bounce (target 2083 on the September contract) should be the larger cycle high and is due in by 6/18

6/16 9:46 Spiral update 2084 high. Next target 2063, 2059.

6/15 10:22 Update from Lab 7442 – they are the experts, not 6:50, target 2041

http://www.ustream.tv/channel/7442-analytics missed 2094 target by 4 points.

correction – they are the experts, not me. Downtrend begins by 6:50 tomorrow.

11:58 Lab 7442’s next short term price target for the es mini Sept contract is 2058

Peggy, what time zone is the 11:58? 6:50?

Forget my question about time zones – I see it was asked and answered above.

Retailers continue to implode. What is hard to understand about what is happening?

Multi-national comglomerates commenced destroying the middle class in the late 80’s. Wages growth is all but non-existent and corporations continue to borrow and buyback creating the illusion of growth, whilst real investment languishes.

For all the prognosticators bagging the crap out of socialism, quite clearly capitalism has and is a failure as well.

I don’t pretend to know what the answer are but what I do know is that unbridled capitalism will never ever work because greed eventually takes control.

Maybe a mix between the two is the best solution.

The USA, which was once on the right path, is now a failed experiment.

Hello JH

Patterns are my game.

Your first chart sc15, sc16 ,sc17 is one group.

Then you have sc18,sc19,sc20 the next group.

Then you have sc21,sc22,sc23 the last group.

This would make sc24 the start of the next group.

Sc24 peak(yellow1.12) the blue line (quarterly data) should drop back down to or below 0.57.

Sc25 and sc 26 would then be like sc19 sc20.

Just looking for patterns.

That is what you projected in part 1.

Average of the four valuation indicators.

The groups of 3 work in with the 30 to 60 interest rate cycle.

T. Boone Pickens says oil will go up and over 100 in 2016. I think you are insane.

T Boones prediction record is very bad. He even still claims he was right about peak oil. He was totally bankrupt being correct but years early on natgas.

Valley

Check this site out please.

http://www.thedanielcode.com/display.php?nav=news

If you have time look at his last 3 recordings

Then look at his article

Click to access Correction_Cometh_S&P_in_a_Cocked_Hat.pdf

Also with the tides it is important to get the ocean temperature

Hat tip for the ocean temperature suggestion. The Daniel Code looks really interesting as well. Thanks, Ricksbiz

Hello Kent

This guy does the gan master time and a lot more.

http://www.phillipjanderson.com

Rickbiz, thanks.

JH

This is how gravity works and why solar cycles work.

Gravity squeeze not only the earth but the sun.

The sun gets squeeze and shoots out solar flairs by gravity of the planets.

The people on earth are constantly under pressure by gravity.

Some times more than other times.

When under pressure (galaxy contracts)the brain produces more chemicals to relive the pain in the body. Then when the (galaxy expands) exuberant.

People have more endorfanes, dopeameans ect.

That’s why cycles work

Allan

A monetary system will only ever work for a relatively few. Getting rid of that is key, there is no other way.

J

Allan

Regarding your comment above that Capitalism has failed and that the US is a failed experiment….

I would like to put forward an alternative point of view. Capitalism, imo, didn’t fail but was ‘brought down’ by socialism which was introduced somewhere along the line into the US. It’s the ‘Govt knows best and we need hand outs’ mentality (socialism) that caused the US to fail.

Now if you were to argue that Capitalism’s tendency towards greed led to the ‘deliberate’ introduction of Socialism to keep the Sheeple in place then that would be difficult to argue against.

Thanks all. Another post is out.

A contrarian view of the economy and interest rates from Goldman:

http://www.valuewalk.com/2015/06/goldman-forecasting-two-rate-hikes-in-2015/

Great write up John. Don’t agree on hard wired hypothesis being visible light though. I believe it could be just something in cellular biology and protein structures in our bodies.