Firstly, trailing 12m p/e valuation. This chart clearly shows this measure is a rather useless tool, and can be disregarded:

Source: D Short

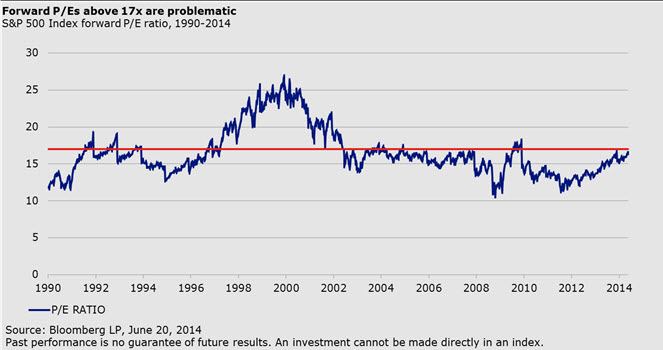

Secondly, forward p/e (12m) valuation. This measure is based on expectations and guidance from companies and analysts. Under- and over-estimating is common for a myriad of reasons (some deliberate, some unrealistic), so this measure lacks reliability and produces another poor chart:

Source: Invesco

Thirdly, dividend yield valuation. Also a valuation measure with problems, due to companies increasingly having moved away from paying dividends in favour of share buybacks:

Source: Vector Grader

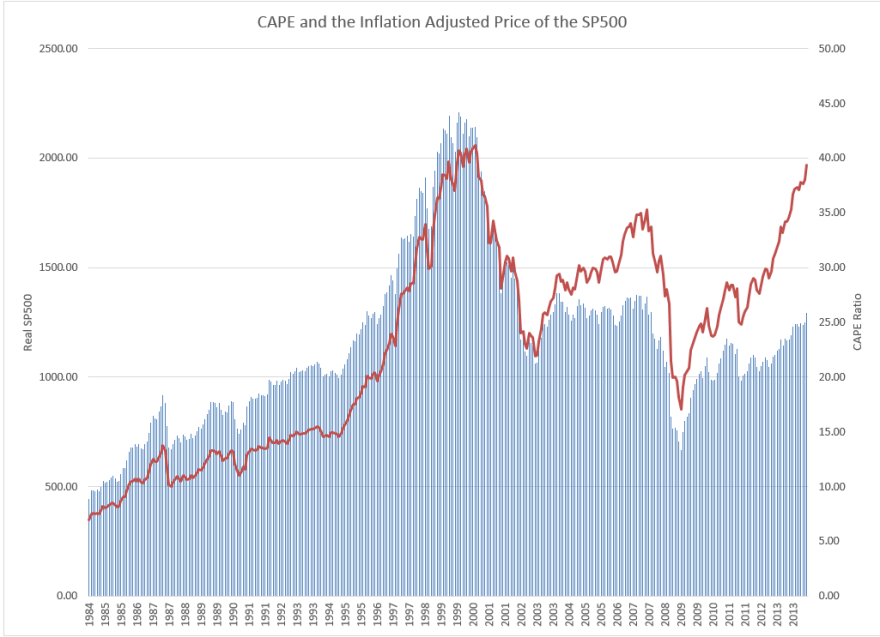

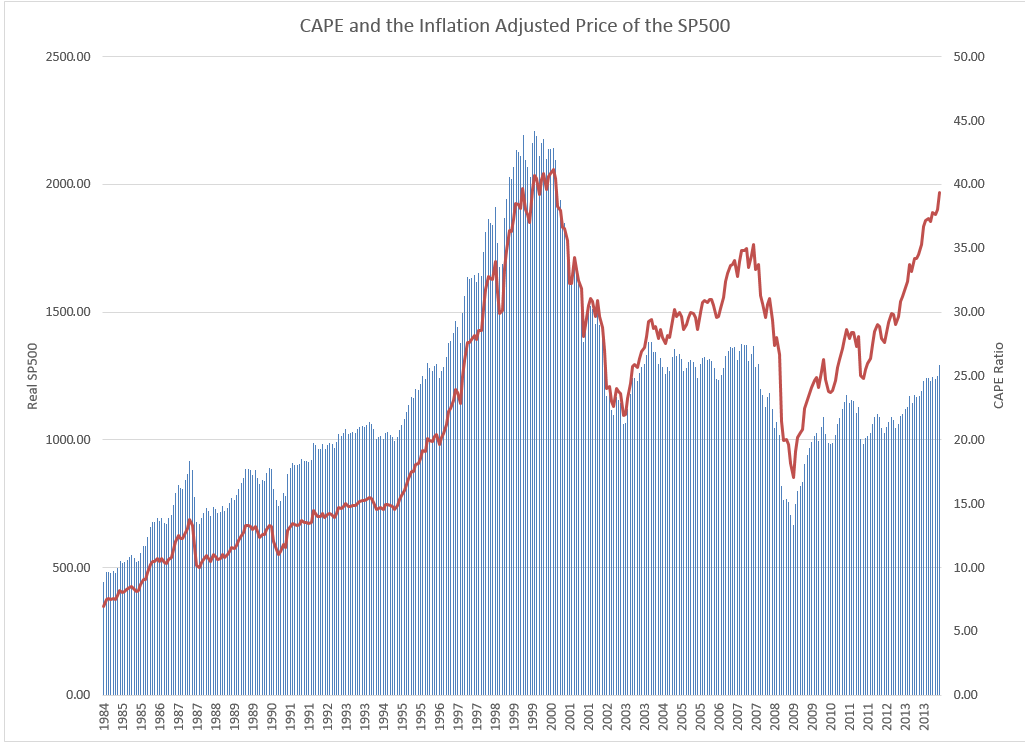

Fourthly, CAPE (or Shiller) valuation. Takes the last 10 years earnings inflation adjusted, and is much more reliable, with a 0.9977 historic correlation with the real SP500:

Source: D Short

By CAPE valuation the SP500 is in the 93rd percentile of all historic valuations.

However, the last couple of years have seen the real SP500 diverge from CAPE, suggesting an additional degree of exuberance is in play:

Source: Lucretalk

This is resolved by using, fifthly, the Crestmont p/e. Similar to the CAPE but uses a different method of normalising the EPS, which makes for an even tighter fit including that additional recent exuberance. By Crestmont p/e US stocks are in the 98th percentile historically:

Source: D Short

Source: D Short

Sixth, the Q Ratio. This is a totally different approach based on the market divided by the replacement cost of all its companies. It, however, produces a similar compelling result historically, and estimates stocks to be in the 97th percentile historically, cross-referencing with Crestmont:

Source: D Short

Source: D Short

Seventh: Market Cap to GDP. We can add in Warren Buffet’s preferred valuation measure as additional confirmation of the extreme historic over-valuation:

Source: D Short

Source: D Short

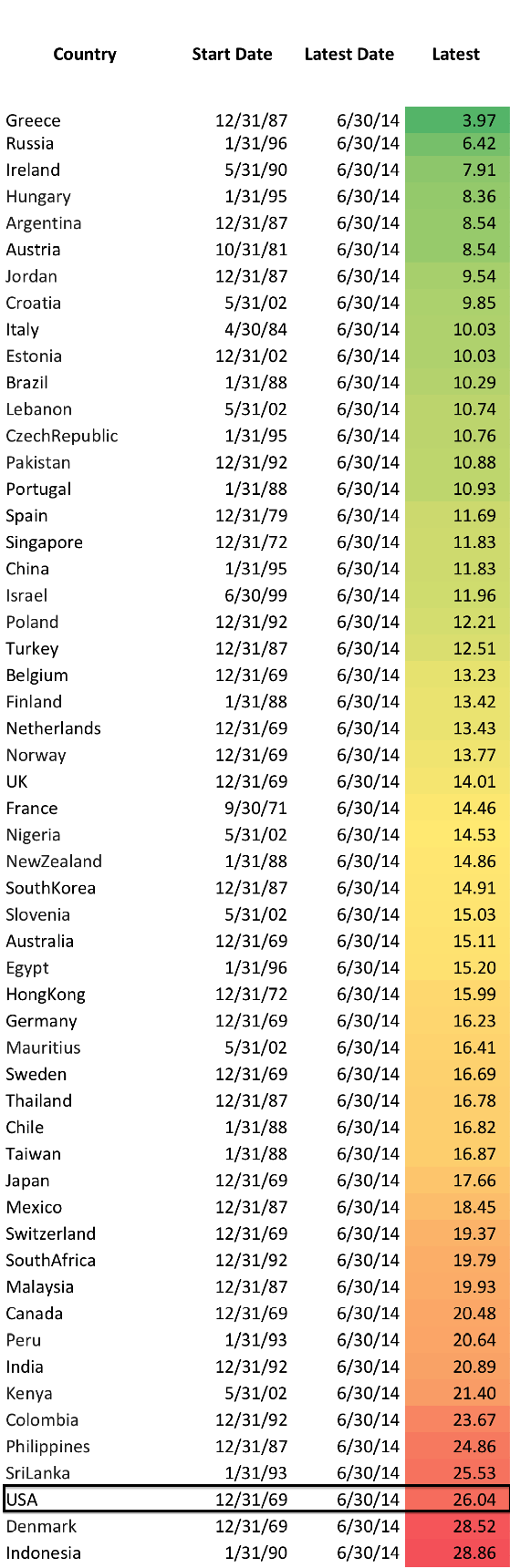

Using the level playing field of the CAPE measure, we can see how the US’s valuation stands up relative to other countries:

Source: Seeking Alpha

By this comparative measure, US stocks are again extremely expensive, almost the dearest in the world.

Now we need to draw in demographics. Here are treasury yields and SP500 CAPE versus their respective US demographic trends:

Source: Barclays

Source: Barclays

The implication is that market valuation has to be assessed in the context of demographics. An expensive market will get more expensive if there is a swelling population of the age that would buy stocks (or bonds), and vice versa.

US demographic trends argue for lower valuations ahead, lower real stock prices:

Therefore, the extreme valuations in US stocks, both relative to history and relative to other countries (with more favourable demographics) argue for a bear market. There is no demographic tailwind to take them to even higher valuations.

The question is, why have US stocks run up so far?

Is it the aggression and support of the Fed? If so, then with QE scheduled to end in October, the market should be readying to fall. But, as per my recent post, I rather believe ‘Fed policy trumps all’ has been the mantra for the mania rather than the driver.

Is it the relative economic performance versus Europe and Japan, including its progress from energy importer to exporter? The problem is that all that is priced into the valuations, i.e. price has nonetheless run up far beyond earnings.

Is it the safe haven perception of US equities and the US dollar? Perhaps.

Is it the propensity for US companies to equity buybacks or for US investors to draw on loans and margin, both propelling prices higher? Could be.

Or is it that US stocks began the process still elevated following 2000’s biggest mania of all time? The valuation charts show this to be so.

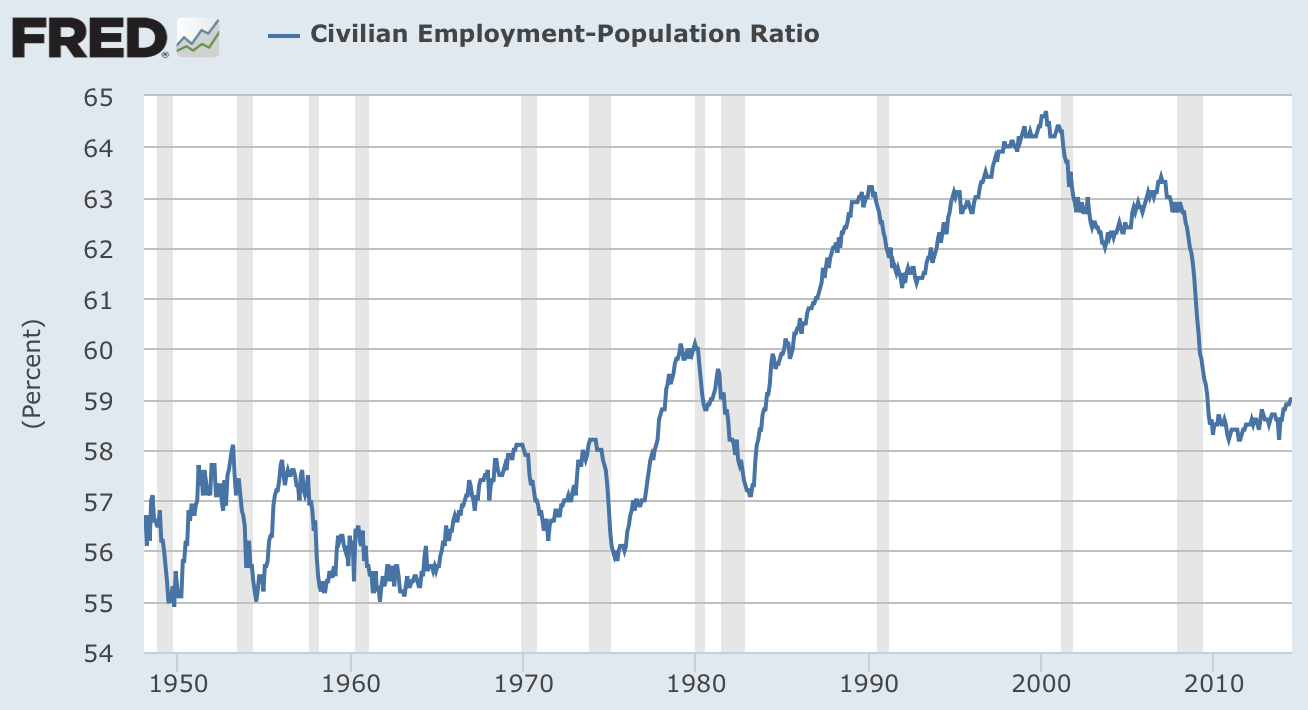

I believe I can explain the mania of the last 18 months with the solar cycle. The sunspot maximum has driven the speculation to take US equities to these dizzy valuations and cast doubt on the secular bear progression since 2000, as the current bull has been given an exuberant last leg into 2014’s solar max (see my recent Last 18 Months post). However, now that we are through the smoothed solar maximum, the combination of valuations (CAPE, Crestmont, Q ratio and market cap to GDP) and demographics argue for a new bear market at hand within an ongoing secular bear to take us to the kind of washout valuations that 2002 and 2009 so far failed to deliver. Rather, we have stair-stepped our way down since 2000 in alternating cyclical bulls and bears, and we can see this in other economic measures:

Source: D Short

Source: Fat-Pitch

Source: Fred

Source: Fred

Demographics and valuations both argue for another step (or even steps) down lower from here.

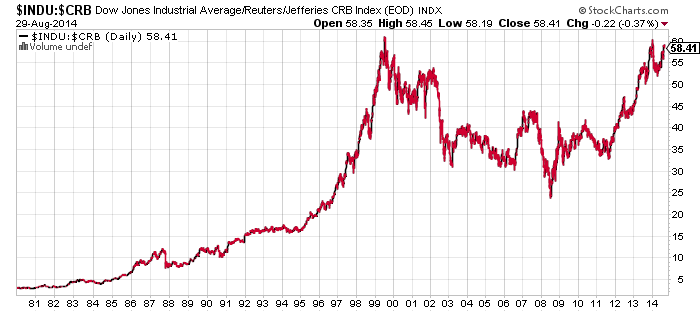

One more valuation measure to finish: we can look at US stocks pricing relative to commodities and relative to bonds. In both regards US equities are now at the same extreme relative pricing as 2000’s peak.

Source: Stockcharts

Therefore, by CAPE, Crestmont, Q ratio and market cap to GDP; by relative expensiveness to commodities and bonds; by relative valuation to other stock markets around the world; and all in the context of demographics: I believe US equities are very clearly a major SELL.

Nice writeup – thanks John

http://www.zerohedge.com/news/2014-08-30/its-settled-central-banks-trade-sp500-futures

cud this be a reason you are not taking into account

I’m very surprised Telegraph released this anti market article, btw John they nicked one of you graphs. I see the banking casino racket is back in full swing.

http://www.telegraph.co.uk/finance/markets/11066137/Spectre-of-1929-crash-looms-over-FTSE-100-as-traders-take-on-record-debts.html

Only just clicked on the clip above the telegraph article after I posted this.

It’s does bring it home when outlined in video format. Joe public got sucked twice in 10 years while fat cats get out.

Doubt they will get off as light as they did before.

Still surprised this been released through a mainstream media channel………

George Orwell — ‘Journalism is printing what someone else does not want printed: everything else is public relations.’

Andre’

Yes, I have read Cowan’s Pentagonal theory, as well as the 4-Dimentional book. In fact, they were the first astro analytics applied to markets that I read. At the time I new absolutely nothing, so it was a challenge. There is a lot to learn and so little time! They are a must read for those that are interested in astro finance.

So much to learn, so little time. So right 😉

Andre/SJC,

I am more curious on these dates (Oct 5 to Oct 19) can you further elaborate? I also see correction around this period as per pattern i follow.

P.s.

Steve, the lunar wobble is new to me and I am trying to find the input for this analysis. May I ask where you get the data on sun/node aspects? Can’t seem to find a decent table on the net. And my software only shows the mean node.

Thanks,

André

Steve,

forget this question; found it.

Steve, my tool says the sun will be conjuct the north node (=opposite south node) from oct 5 until oct 19. And they are both in Libra.

Anyway, thanks for showing me this direction.

Andre’

Yes, the Oct 5 to Oct 19 works for Sun-Moon conjunction in Libra. Those dates have an orb of 7*, while the Oct. 9 & ~Oct 15 have an orb of 3*. Oct. 12 is exact. I use Solar Fire, but there are lots of good software available (some free).

Steve, I understand. It seems like it’s the time between the lunar eclipse and the midpoint between lunar/solar eclipse.

André

And part of the Lunar Wobble is also the 90* (and 270*), 180*. Although not part of that Lunar Wobble, I think it is useful to be aware of 120*(240*).

Steve,

Thanks; very interesting. With an orb of 4* my tool gave your dates in october, so I’ll have to be more aware of my orbs. October 12 the degrees match almost exactly, so that one is clear as well. Thanks again

Thanks John. Very Good Job.

The pattern is maturing. But it still allows for one more small 5 legger up.

And it may make one more shallow dip to “about” 1985 before finishing the final small 5 legger up. Rather than predict where the dip will go however ( 1985ish), I watch the 5 leg ( c:4) dip to see when it is complete. And the following 5 leg rally to see when it is complete. ( Sometimes the 5th wave is a failure). 2015 to 2030 is possible with 2015 to 2025 more likely. But again, the pattern tells when it is over rather than a prediction of price level.

Great article John.

I mentioned in the previous thread that I had just finished watching 40 odd minutes of Martin Armstrong ramble on about how he is right and everyone else that sees it differently is basically DUMB.

What is most interesting given the global market valuation charts is how MA keeps stating that foreign investors will flood into the US markets because there no other options.

I have no doubt that some of his models are useful but I also have no doubt that he likes an eachway bet and telling EVERYONE how good he is.

One such model is his ECM which by the way is pointing to a turn this week. He has stated himself that this COULD mark a turn in any direction in any capital market.

So he has pretty much covered himself here. If the markets shoot higher, he was right, if the markets turn down down, he was right.

I guess what I am saying is that whilst his model might work to indicate minor and major turining points,he just doesn’t know how exactly to interpret it.

What I find hard to handle is his pontificating and arrogance. I have been reading MA since the early 90’s and he MOST DEFINITELY is not right all the time, despite his self delusional belief that he is.

@Allan, I’ve only recently (6 months) been introduced to Martin Armstrong’s blog and like you noticed his propensity to fit his ‘theories’ after the fact. Worrying to think that many Central Bankers listen to him a lot…according to him.

purvez, a lot of double speak and contradiction. He talks about the rampant manipulation by the major banks and then derides anyone if they mention possible gold manipulation.

I have seen his computer array models change “after” they were wrong. In other words they were predicting increased volitility and a trend change on particular week/s and then after it didn’t occur a later array the he posted was completely changed.

I know for a fact because I kept a copy of the original on file. He says that they update regularly to reflect changes but what us is that after the fact?

Everyone has the benefit of hindsight.

Here, here Allan.

He’s an annoying g#t at times!

May be annoying but he has kept me out of gold and in the equity market for the last 3 years so very happy.

Looks like high base breakout.

Adding to SPX long at SPX 2007

Another powerful advance for the DAX,

and yet another new ATM high on the SPX in prospect.

MA ECM model is a global model not based on market data. It’s complexity and historical perspective of order in all things is beyond any one persons comprehension. The computer’s projections are not his “opinion”. He will tell you long term projections are much more accurate than short term. Decades ago the computers selected 2014 as a Cycle of War turning point, quite accurately.

What many fail to see is the effect of globalization on the world and markets. It is all about capital flows and how capital moves. In this age of digital money, capital reacts and moves faster than ever. The euro experiment is reaching its final curtain call. With German imposed austerity, increased taxes, 10% wealth confiscation, sociol failure, massive unemployment etc, no wonder capital is fleeing the country, landing in the US markets. Then there is Japan. And it looks like the Chinese will be allowed to invest outside their own country soon.

There is a minor turn date this week on the ECM. It does not portend a major change, nor does the US market line up with this date. After this time period, the model will offer more clarity on direction. MA has posed several scenarios of what might be coming… One of which is a cycle inversion. This would give us the correction many are looking for. But when? Maybe not for years. The business cycle is in full swing and most are banking on the prez cycle next year. Big money usually wins.

The computers are projecting a volatile Oct/Nov. And Gold? Jan/Feb 2015 bottom at $1000, just to wash everyone out. Says $2000 this fall is bs. We shall see.

Alexa, take his computer arrays with a grain of salt. As I have said I have seen them change from what they were originally predicting after it turned they were wrong. Not just once either.

I find him to be extremely condescending and arrogant. His ECM has merit though.

@Allen, @Alexa, whilst I struggle with MA’s writing style (and grammar) and most of his short to medium term stuff the one thing that does resonate is his thoughts on Capital Flows. Until I started reading his blog I hadn’t thought of it in those terms but now I do tend to think in terms of Capital Flows and quite a bit of what happens in the world starts to make more sense.

I think as you both recognise there is some value to what he says as long as you don’t follow him pedantically.

Alexa,

I would like to use your good post, and the comments of others, to segue into a topic that may have relevance to work John and others have done on this site and get any feed back; but first a set up:

I have been following MA for about 1 year. As with so much in life, there is much about MArmstrong that I both agree and disagree with. I believe his views on republics and democracies are flawed (probably heavily influenced by his own experience with the legal system), and I agree with the comments of some here that MA tries to have it both ways on conspiracies and market manipulation (doesn’t exist on Gold, but does on banks),… But for me he is at his best when discussing that there is a battle to the death between Socialism (and the required support of Crony Capitalism) and Free Market Capitalism (not Crony Capitalism), the history of money/capital, the idea that everything is related economically (driven by self interest), that Capital Flows are critical, and government corruption is driving a Cycle of War (others broke the ground on this long before, but he has re-popularized it).

John has been eloquent in his argument that Solar/Geomagnetism is an important driver of human emotion and the resulting economic condition, and that a major trend change is (has) occurring(ed). Yet, the S&P has continued to rise. But that is focusing on only one part of the puzzle. If there is an impact of Solar Cycles/Geomagnetism on emotions, then should it not impact the emotions globally? From that perspective, John’s linkage has been (sun) spot on. Europe, and the Middle East are emotional and economic disasters (and/or getting worse since late Winter 2014), ditto for Russia, South and Central America, and southern Asia. The Chinese may lead economically in the future (if they embrace free market capitalism), but first they have a few bubbles to deal with, and because of popular demands, the Chinese will be loosening capital controls to allow capital to invest elsewhere. Others may disagree, but the economic performance of America is becoming more sub-par to capability. Everywhere the air has the whiff of deflation, high unemployment, and discontent (or outright violence).

What if the Solar/Geomagnetic (and Lunar) impacts have taken hold, as articulated by John, but those effects first impact the weakest link. As assets are liquidated, and capital strives to ‘get off the grid’ in Europe, Russia, Middle East,… out of emotional fears…where does it go? High end London real estate? The German stock market (“dissolve the Euro and give resurrected German Marks for German assets”)? High end New York and Florida real estate? And if you want to move some real money, the S&P 500 and T-Bonds are the only real option (at higher prices). Is it possible to have certain markets doing very well, while other markets collapse? When/how to measure that sequencing impacting domestic markets? Lots of questions, no ideas.

I guess that I am making the argument that Johns views have already been proved correct, that the weakest economic/social structural dams are in the process of breaking, resulting in a flood of capital rushing down to the next reservoir, creating the next bubble. When/how will we know that all the capital that can flee, has?

Back in the late 80s… Martin Armstrong’s track record was terrible… he lost billions for his clients and was caught stealing his investors’ money… he is very stubborn and rather than admit his guilt, stayed in prison claiming it was all a conspiracy against him…. fact.

bs – he was a political prisoner held hostage by the INJUSTICE DEPARTMENT; serving the longest “contempt” sentence ever given an individual in US history.

no trial, no due process, no bill of rights…

anyone who supports what happened to him is the worst kind of useful idiot.

Let his track record speak for itself. In the early 90s he called for gold to make a run to a monster top in 2000.

The fact that he writes so esoteric imo is a front for being full of poo

And landing on the moon was a giant conspiracy as well…. lmao. Ripping off billions from his Japanese clients was theft on a grand scale. MA should still be behind bars for not cooperating. Of course the reason he didn’t cooperate… he was GUILTY! I see he has fooled the gullible – too bad so many stupid people.

Thanks all.

6 out of the top 10 world’s economies made negative or zero Q2 real GDP growth: Japan, Germany, Italy, Brazil, France, Russia

Dear John,

Many thanks for sharing your research with us. I share your views and it is scary that despite all the money printing, growth has been missing. Unfortunately, for the bulls, this means more money printing, giving them even more reasons to buy into the market. Warped, but this is how the market functions these days.

Yes, this is just crazy. I keep moving my trailing stops up, but I just don’t see why we need to short right now vs through a series of stops. Perhaps I gave up picking the top. I am sure someone will get it — not sure if the prize is that great in the bigger picture though. It is not a binary event of getting the peak or not, but a marathon for the next year or two.

This sell off in gold looks really sus too. Smells like a huge “bear trap” to me

VIX is up 7%. Either stocks go up or VIX goes up, but both can’t go up.

something about the end of August/beginning of september which brings out the worst/best in speculators. USD/Yen hitting important falling trend lines, Biotech running out of steam, Precious metals looking poised. Daily sun spots have been 12-14 on both solar discs combined these past 3-4 weeks so the speculative fever has had a cause. Slowly we are dropping into high single digits which should bring relief.

Just want to say how much I appreciate the group sharing the views of Armstrong.

Dittos! on all the above posts! Someone has also suggested that he’s redeeming his points on his ‘get out of jail free’ card. (:-) The inference is that he’s a mole or plant for the cartels.

ECB meeting / news set for Thursday and markets are widely set up for dissapointment here.

Germany runs the show in The E.U. Period.

The ECB is completely and totally powerless as “there is no EUR bond” and you can’t go printing money on behalf of a dozen individual countries. Ridiculous to even consider!

The EU Zone actually values and “respects” the purchasing power of their currency ( if that’s even possible of a fiat ) and with real rates “already negative” anyone thinking The ECB comes out with some kind of “market saving silver bullet” is kidding themselves.

Germany will never have it.

EUR and GBP as oversold ( and obviously / inversely USD overbought ) as possible, before the rubber band snaps the other way.

Sitting right in front of peoples faces, and so blatantly obvious,.

Imagine a world where GBP tanks and what? USD takes the main stage as a “currency of choice”?

USD is a currency of “necessity” ( as the worlds reserve and needed for international trade ) not one of choice.

Who in their right mind “wants” to hold/buy USD?

Not this gorilla.

Right on the point Forex Kong!

There is no Euro bond now, but couldn’t the ECB create one? (That is, if Germany would allow it.) The irony is that we could be facing a monumental deflationary storm where printing would soften the blow or even prevent it. But printing is becoming politically unfeasible, so we will just have to see whether the deflationists turn out to be right.

Stock market bulls have to explain how the disappointment from the EU meeting Forex Kong described and the snapback from USD/JPY (not tomention the strong US PMI that eviscerates any argument for more QE and zero rates in the US) can possisbly drive stocks higher.

If the market keeps going up irrationally, they don’t have to explain anything. Explaining means you think the market is behaving rationally.

That’s a fair point, but when I am bullish on something I have a narrative that supports being bullish,. I think this is typical. Technical traders don’t require a narrative, but if we recall the media stories in early 2000 and 2007-08, various narratives were put forth to support the bull market in stocks (and in 2007, housing). Most people are not TA traders who have no need for a supportive narrative. Also, there is no such thing as “irrational”–choices and behaviors drive markets, and those decisions are quite rational to those making them.

Charles, you might have answered your own question: Technical traders don’t require a narrative. And neither do all the individual investors who have missed much or all of this bull run. Well, maybe they do, but it’s a simple one: Stocks always go up over the long term, just get in and hold on. So the technical traders get buying the trend, the mom and pop investors keep coming back into the market, story or no story, and up we go.

There are lots of narratives right now. I disagree with all of them, but they are there, and so the market can keep going up until we put in a parabolic high.

1) Rates are zero

2) Rates are not even high yet, so early in recover.

3) China is awesome

4) China is slowing, but reform is coming

5) More China credit, and there is no risk as all backed by government and trillions of surplus.

6) Most hated stock rally ever, so cannot be peak

7) Presidential cycle just getting started

8) No inflation yet.

9) Wall of worry.

10) Crop yields are abundant

11) Rates mean higher P/E…P/E+inflation indicator fits history so well and shows cheap cheap cheap.

12) We need all bears to capitulate. There is still Chanos and Hussman and Ackman.

13) Crashes do not happen with VIX so low. VIX low means early in bubble.

14) Volumes low => 1996 type of market. Again crashes don’t happen without volatility, volume and euphoir.a

15) Millennial are not invested. Retail is not invested. How can there be a bubble.

16) Taxi drivers and shoe shine boys not giving out tips.

17) Markets don’t peak at round numbers. We tend to blow through 2000.

18) Sell in may over soon…buy for year-end rally.

19) Funds that were underweight now need to catchup etc.

20) Who will sell and pay taxes? So buy! Because even the best timer less taxes loses to buy-and-hold.

I can probably continue for 100 more…again I am not saying I agree with even one of these points….

Bulls need to reclaim SPX2000 at the close to keep this party going imo.

Hi John,

Need to study closer but initial comments. Q Ratio needs to “double” in current climate and the following “Is it the aggression and support of the Fed? If so, then with QE scheduled to end in October, the market should be readying to fall.” Q Ratio needs inflation to adjust for buybacks which should not count anymore in the Q Ratio if you get what I’m trying to articulate. Housing starts, housing prices and loan refi’s will be first to fall in quantity. Will affect commodities and jobs. Drought, you haven’t focused on AT ALL lately John 🙂 is going to get worse. Winter in US due to solar barycenter to be colder each passing year with El Nino muted. On your quote, the Fed financed the buybacks. Rates are locked in ont hsoe debts. Basic accounting principle of issuing stock to raise captial cheaper then if debt is more expensive. The companies owning their own stock, locking in low rates, is not going to “fall”. Only the ability to service the debt via reducing revenue is going to trigger such a free fall.

Overall, not doubting your point and conclusions but your data is based on old data in times when dollar and interest rates were different and it was cheaper to issue stock and pay dividends. Use this fact and take the data and look at triggers for slowing down money velocity, not deflation or inflation, and you got your recessionary triggers that will make companies want to cook the books and mess around with those cheap loans. Even then, they may be so cheap, the company may not ever sell the stock but do reverse splits, further raise share prices.

Housing and commodities are the keys. Drought, and agriculture yields per acre of producible land. We’re getting into the Economics aspect, but I don’t see the correction coming unless MBS issuances cease to exist with QE buybacks from banks.

Hopefully providing some meat for the bones you clearly have nailed down as central tenets. I helped you see the demographics angles before, now need to look at commodity consumption/production versus waning solar cycle strength in tandem. :o)

http://www.cnbc.com/id/101963821

Fed policy re-enforcing recession? Hilarious how out of touch they are.

Will there be disappointment from the ECB?,

the consensus should be well aware of what capacity

the ECB can work within.

Draghi has discussed further extraordinary measures,

so plans are in place for further action.

In terms of narratives for further rises,

there are multiple reasons, some of which a

previous poster outlined.

For me, the most powerful are ZIRP and

US earnings and dividends continuing to grow.

I do not see waterfall declines with US earnings

continuing to increase.

A temporary sentiment shift can take a few % off

markets very easily and does not require any

change in fundamentals, just perception.

@Phil from everything I’ve read it would seem that US earnings and dividends are growing due to cheap money. Companies are borrowing for share buy backs and also to pay dividends with. Profits in absolute terms are declining or are stagnant.

Ergo ZIRP is the cause of the above two. So in a way you are right about it being powerful.

Target hit. Closed all SPX longs at SPX2009.

@Duncan, please would you share with us how you arrived at SPX2009 as a target? Thanks.

http://m.bbc.co.uk/news/world-europe-29042561

Nicely done Duncan.

The positive news on Ukraine this morning

significantly reduces the possibility of any

short term sell off.

BBC:

“Mr Putin’s spokesman, Dmitry Peskov, told Russian news agency Ria-Novosti: “Putin and Poroshenko did not agree a ceasefire in Ukraine because Russia is not party to the conflict, they only discussed how to settle the conflict.””

Reversal anyone?

Have a look at this http://ourfiniteworld.com/author/gailtheactuary/ The conflict between USA/EU and Russia has a long way to go because it is about declining resources and increasing production costs worldwide. Energy is an important missing factor here (along with Solar and Demographics) when analysing markets longterm.

This could be it,, market shooting up on the back of UK data and the cease fire in the donbass part if ukraine only. Why bomb the hell out of an area the plays a big part of ukraine GDP, especially as you will need it when you take over.

But Russia RIA has just released that there is no agreement from Russia on a cease fire as it’s not directly involved, talks now move to anti Kiev rebels.

I’m afraid this is far from over.

Also market betting ECB will launch a QE bazooka, I think the market may well be disappointed tomorrow if he draws out a pea shooter. ECB talks but rarely acts.

Do I think the market will rise today and tomorrow-? Yes, but this just could be the parabolic stage.

I dare not call a top but I have a very small bet with a friend on who buys dinner on these figs being the top range or the next 2 years.

SPX 2039-2051

FTSE 6935-6985

Dow 17400-1750

There are more tops called here than by the late Sid Waddell –

king of the darts commentators.

LOL

Of course we should all know by now that geopolitical events don’t have long term implications on markets right?

Ha ha, ok we will see, enjoy the rise, I’m hoping to get a free dinner.

That ceasefire did not last long.

http://news.socialdashboard.com/ukraine-quickly-backtracks-after-announcing-cease-fire-deal-with-putin/

For me Ukraine has the potential to provide

a catalyst for a short term sell off,

that was the only reason I mentioned it.

That negative then becomes a positive on any

type of resolution/compromise, as this morning’s

price action shows.

And that is what appears to be missing atm,

one defining factor that alters sentiment.

+10y falling trend line hit in usd/yen at 104.85 plus 61.8% retracement double test at 105.44. Should be important for the risk off/short stocks trade if it holds.

Click to access swissquote_2014_09_02.pdf

I have to be honest, from a bear perspective the following chart REALLY concens me.

http://stockcharts.com/h-sc/ui?s=$INDU&p=D&b=5&g=0&id=p29874431713

And from a weekly perspective:

http://stockcharts.com/h-sc/ui?s=$INDU&p=W&b=5&g=0&id=p94931686276

As bearish as I am over the longer term it would take nothing to break that double top on the daily and propel the DOW to 18k target and if it did break it, within perhaps a week or two.

As mentioned by someone here before, we have the bigget IPO in history on the 16th.

A lot of brokers stand to make big $ if it is a huge success.

Thanks for all the comments and input

the last one closes the door they say.

Judging from the price action in biotech, Chinese peer baidu, use/yen we are looking a substantial mass herding which will end badly – anybody remember the gold bubble 3 years ago?

Very good! Thank you,John.

I like this article!

Thanks

Thank you John for this great post! Just one comment: if you take the Shiller’s CAPE and multiply it by a long term rate (e.g. 10y, Shiller has a GS10 in his xls data sheet), you get a bond vs equity yield ratio. At the moment we are at 0.62 (10y yield is 62% of the SP500 yield) in the low part of the historical range (1870-now). You have to go back to the early ’70s to get to hit a similar level. I am not arguing that the equity market is not expensive in its own history, but it does not look expensive compared to such low rates. The distortion in equities is a consequence of the anomaly in rates in my opinion.

Thanks. In the 30s we had ultra low bond yields but equities still peaked out at high CAPE, in the 80s we had ultra high bond yields but equities still rallied from low CAPE and outperformed. So it doesn’t seem we need to net rates.

I have never seen a market that refuses to go down like this. I am usually early but never this early. If new highs presses on, I just have to follow my discipline and get out. Perhaps the next drop will be it, but I will wait for that to happen.