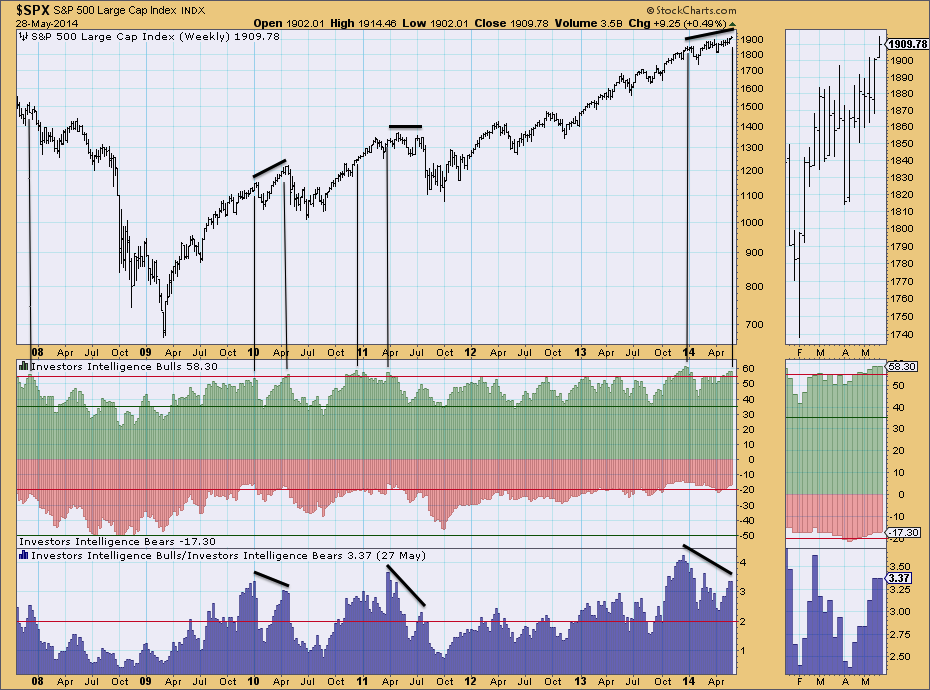

The Dow Jones Industrials stock index so far continues to honour both the May 13 DeMark price exhaustion high and the December 31 inflation-adjusted high, set against a backdrop of deteriorating breadth (top and bottom indicators):

Yesterday’s potential new moon reversal tantalisingly sets the scene for renewed declines, to keep all in tact.

Yesterday’s potential new moon reversal tantalisingly sets the scene for renewed declines, to keep all in tact.

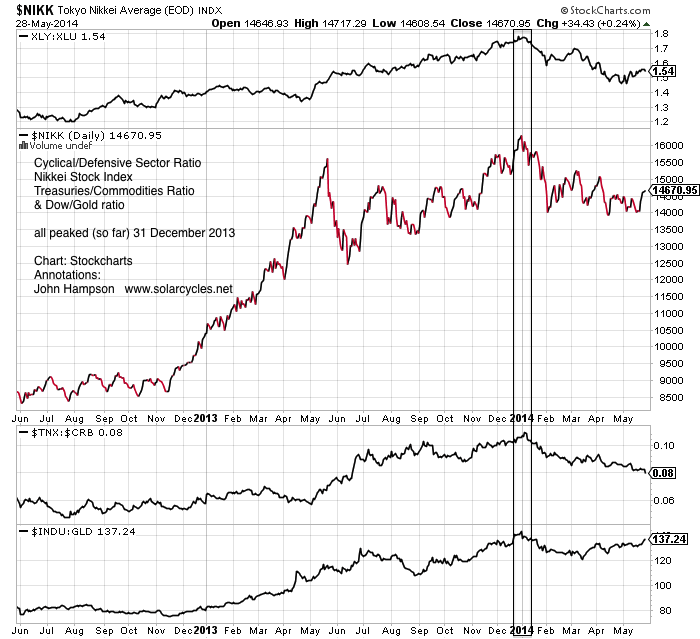

The relevance of the last-trading-day-of-the-calendar-year high is shown in the next two charts:

…and the Nikkei peaked again on 31 December 2013, as did various risk-on / risk-off ratios shown here:

…and the Nikkei peaked again on 31 December 2013, as did various risk-on / risk-off ratios shown here:

Just the Dow-Gold ratio is a little in danger now, which adds to the scenario: if the Dow stumbles again here, that 31 Dec peak will likely be maintained.

Time is ticking on US large caps, as various divergences are now mature, and so I have my doubts that a summer rally can be mustered here:

Source: Oppenheimer / Annotation: John Hampson Source: DecisionPoint / Annotations: John Hampson

Source: DecisionPoint / Annotations: John Hampson

In short, the Dow is within easy reach of taking out both the 31 Dec real high and the 13 May nominal high to invalidate the above, and yet those risk-on cross-asset peaks of 31 Dec have not been taken out some five months later. So are we seeing the last gasp of a topping process, or consolidation before an overthrow leg higher? The answer lies right ahead.

Thanks John ! Do you see the nice false move above 3245 🙂

Thanks John.

As I mentioned yesterday the pattern on DOW Trans daily chart has me intrigued at the moment and I believe it is foretelling us something.

Price is now being funnelled into a spike high that now has virtually no room left to move as price is being squeeezed between both the upper curving trend line begining from the Jan high to present and the lower curving trend line from the Feb low to present.

So it either it spikes higher( highly unlikely given the angle of the ascent) or it breaks lower.

And remember DOW Theory 101?

http://stockcharts.com/h-sc/ui?s=$TRAN&p=D&b=5&g=0&id=p71880678569

DeMark on Bloomberg yesterday – “a market over the past 43 years we’ve never seen before”:

With respect I had difficulty not laughing

out loud during that interview – constantly

hearing the word “adjustment” – so an

incorrect call is now called an adjustment.

With respect, as per previous I have pointed out that DeMark’s top calls for U.S. markets have been poor and the reason for it. And he himself has not shied away from stating so, so I don’t put him in the camp of those pundits who spin their calls after the fact.

Tom has been in the business for over 40 years and continues to be closely followed by some of the most highly regarded money managers on the Street. He has no need to “adjust” his incorrect calls in order to avoid responsibility. That’s sort of laughable at this stage of his career.

Demark has been calling for this kind of top since March of “last” year.

From tradetrekker.com blog yesterday:

With interest rates in US Treasuries already low, the search for yield is evident in junk bonds or high yield bonds. One representative is the SPDR High Yield Bond ETF (JNK). From the selloff back in May of 2013, JNK recovered all of the lost gains and is close to breaking the highs made a year ago. But there are warning signs through a pair of confluent price exhaustion factors: the daily TD Sell Setup for the JNK recorded a “9” on May 14th and is currently biding time. The weekly JNK can achieve a TD Sell Countdown “13” this Friday with a high of at least 41.53 and a close above 41.43. Should JNK “work off” the TD signals, and break out from the one year highs, risk appetite for equities should also continue.

The SPX broke out from the 1900 level from the last trading session last Friday. The next major inflection points come next week, when the ECB meets and the release of the US employment figures.

It’s all relative… http://scharts.co/1wrygoh

It’s all relative and it’s all about timing…

Hi John

Thanks for the continued articles. One small point, what would the 31 December ‘real Dow’ level be in today’s index?

Thanks

The VIX spending the last 4 days at new lows looks just like the VIX in 8/2000 right before the secondary top of the NDX. I hope you are right!

Ditto. Good observation John. I’ve seen exactly the same thing

John

Where can I find out when the next full / new moon is?

Duncan

Just look up lunar calendar 2014 and you will find the full calendar for this year

Thanks Will – very much appreciated

I find this website particularly good. http://Www.google.com I think it’s new. Anyone know if its reliable?

Bet you were the fool at school that thought asking a question was stupid. No stupid questions, just stupid people.

stupid people don’t laugh at clever jokes

On a session like this I dream about distant lands, hot rocks and appaloosa horses.

God please stir that water, I need waves.

Very subtle, but VIX is rising with SPX last 3 days.

uhahahahahahah….

tell me that a market really exists… why nobody is selling after disastrous gdp data? because the market does not exist, it’s a total fraud.

it goes up on bad news, more QE.

sometimes banana republic index with rampant inflation crashes too… this bubble instead is unstopable. Goldman calls for moaaaarrrrr

sp500: 40 points higher in few days…

waiting for what? 2000-2100

WOW!!!! just heard from trader on CNBC “theres no risk in equities” lol

talk about a top

Close but not yet….I am looking at next week for a top. We can let the bulls cheer and buy at the highs for a few more days…even if we don’t make higher closes, there will be chances to get short intraday as they try to stop every last bear out. By the VIX, it seems we are almost there, but the ECB will surely ease next Thursday and we will cheer for a while again.

Wonder if we will get a surprise by ECB due to the big win of anti-Euro parties in EU parliamentary elections.

Interesting (but lengthy) analysis of volatility by Marketfield:

Recent weeks have been characterized by an extreme lack of volatility within a

number of key trading instruments. Most clearly this has been the case with the

overall SPX index, although it has also been witnessed within a number of

important commodities (gold and crude oil) and key interest rates (most clearly

the 10 year treasury note). Our strong suspicion is that this lack of volatility is

itself an artifact of market activity with the lack of natural yields available

leading to the use of “volatility farming” as an alternative source of return to

merely clipping coupons.

Thus for a period of time we have seen a cycle whereby volatility selling acts to

constrict sharp moves in key prices, which in turn discourages trading capital

from entering a range bound market. This further depresses the volatility of

prices which is in turn reflected in lower implied volatility encouraging a further

sale of option premium. This effect of this can be seen on the attached chart

which shows a series of VIX curves from May 2013 to May 2014. The last few

months have seen a steady progression towards lower implied volatility while

the most recent curve (light blue) has seen a particularly pronounced collapse at

the front end of the curve.

Although such cycles are hard to break, in our experience they do eventually

give way to much more violent markets. Although the general expectation is for

this to involve a sharp move to the downside this does not have to be the case.The point to understand is that the blind selling of volatility serves to prevent a market moving in its originally intended direction. Since volatility selling often

takes place at the end of a cycle it can prevent a market from recognizing a clear

deterioration in fundamental conditions. This was certainly the experience in

2007 and once the SPX finally broke its tourniquet in late February things were

arguably never the same again although it took another 8 months before the

overall index recognized this fully.

This time around things feel somewhat different. Instead of an FOMC imposing

tight monetary policy for a number of quarters (the yield curve was inverted as

early as June 2006) we have one promising to maintain post-Lehman generosity

for several more quarters and to limit rate increases for a number of years after

that. Furthermore both economic data and corporate earnings continue to look

healthy. We would therefore be more open to the premise that this period of

volatility constriction is preventing the market from moving higher and that the

eventual violent break will be to the upside. Certainly the evidence suggests that

a combination of a flat overall index and substantial under-the-surface volatility

has forced substantial amounts of capital to the sidelines, and while overall

sentiment could not be described as overly bearish it feels far removed from that

which normally would be associated with a market that remains right up against

an all-time high.

Stephanie Pomboy

“At some point the Fed is going to have to taper the taper”

One of the few widely respected economists outspoken enough to admit that QE has become the SOLE driver of the economy.

We all know it Steph, without cheap easy money this economy would be “stuffed”.

At some point the market collapses and the Fed does the only thing it knows how to do. And at THAT point gold explodes as people lose complete confidence in the Fed’s ability to contain the rot.

Great article

http://online.barrons.com/news/articles/SB50001424053111903301904579561672621644240

It is, Allan. Did you watch her informative presentation on YouTube (I posted on previous thread)? Pomboy is an amusing (in a good way) presenter and a smart lady.

No I will check it out. Thanks. She is definitely one very astute lady and I like her frankness very much. Tells it the way it is.

John

if this is indeed a fakeout top; today is key. It will form the weekly and monthly candlesticks on both the SPX and DAX as a breakout if we do not retrace today.

Duncan

why do i get the feeling they want to scare the bears again .

PS ± ESTX50 still 3245

Hi John, I’ve run some numbers for solar investing in the S&P 500, Commodities & 3-month bills since 1872.

Going long the S&P between minima and maxima and then switching into interest-bearing cash would have earned 5.7% real total return annualised, against 6.7% for buy & hold.

Holding commodities instead of cash between maxima and minima lowered the return to 4.0%.

Where switching based on solar cycles has paid off nicely is in terms of risk, lowering volatility from 14.3% for B&H to 7.8%.

Does this tie in with your findings for the DJIA?

Dominic, this is quite interesting. If you overlaid a simple moving average (say 200-day or longer) to your buy-sell rule, would returns improve?

Gary, good question, I will investigate. My guess is no. You can read my findings to date here: http://picarda.org/2014/05/30/sunburnt-sp/

Dom, I would change your focus to the potency of solar maxima to time speculation peaks (not all bull markets are solar inspired – the cycle is 11 yearly). Around now is the solar max and we see a host of topping indicators in equities, as the theory predicts. Now the question is how potent it is as a timer of the actual market top. The last 4 solar cycles were very exact in their timing, as we might expect in a world increasingly fast and global response, and I believe it will turn out similar.

Hi John, thanks for your thoughts. I will check out the relationship to tops and bottoms, although I am little concerned with spotting these, being a trend-follower rather than a predictor. I don’t think the results vs buy-and-hold are by any means disastrous. The lowered risk is definitely worthwhile. My main issue is not with the respectable results but with the theory behind it, about which I am sceptical.

Trader Vic: “In my 50 years in this business of reading the tape, I can tell you with great certainty that every time there is negative news the Fed comes in, via the banks, and manipulates the stock market higher in order to keep the appearance of strength….

Today we had this 1 percent decline in GDP and there should have been some downside response to that. Under normal conditions there certainly would be. Shortly after the GDP news release we had Fed official Jeff Lacker saying that GDP in the second quarter ‘will bounce back.

But why does a Fed official have to come out and support the market with his comments? You see, Eric, the whole game plan is pushing the markets higher. So there is no question there is Fed buying in the markets, being done through the banks, to keep the markets stable.”

Jazzman, Be careful ;). I brought up the subject of Fed intervention weeks ago and it wasn’t well received by some.

At the time I mentioned that in all my years of reading the tape I was certain that intervention was obvious. And I stand by that conviction today.

Allan, just checked the COMEX Silver COT, Swap Dealers long and Managed Money short are both now record high. Either it is similar to 2013 April (prior to the huge crash) or 2013 July (short squeeze).

http://www.quandl.com/OFDP/FUTURE_COT_228-COMEX-SILVER-Futures-Commitment-of-Traders-data-from-CFTC

Thanks, Allan. When one studies the history, it is safe to say that the world is not ruled and governed by groups of honest people whose aim is to benefit the populace, therefore we can surmise these economic/market events are manipulated or managed to various degrees. 🙂

FED intervention has not stopped countless

previous bear markets and severe corrections.

The next bear market will be highly corrrelated with

the next recession and earnings compression –

as is always the case.

Corrections only require sentiment

changes so are more difficult to foresee.

Some evidence suggests the 2008 financial collapse was actually ‘allowed’ such that the consequence led to the ‘plan’, e.g. TBTF banks growing even bigger, huge wealth transfer through QE backdoor, etc.

Ugly Yellen says there is no bubble… so let’s the party goes on.

‘The markets ARE manipulated, once you as a small investor come to agree with this statement then you can take the necessary steps to prevent yourself from being wiped out by ALWAYS keeping this in mind that Manipulated markets WANT you to act in a certain manner at certain times, they want you to buy into the latter stages of a bubble as the manipulators distribute, and the market manipulators want you to SELL into Market Bottoms and early bull rallies when the manipulators are accumulating.

Who are the market manipulators ? Today it is the Investment banks, investment funds, CEO’s (stock options) and last but not least HEDGE FUNDS that created the stocks bubble through leverage of X20 or more that subsequently bankrupted the banks that were driven insane by short-term greed with trillions of dollars of liabilities which have NOW been fraudulently dumped onto the tax payers. I have not heard a single story of a hedge fund manager losing money, not one! They have BANKED their profits ! The losers are their investors who held on and the banks who leveraged them up to the tune of tens of trillions, and in the final instance the Tax payers who are being FORCED to bail out the bankrupt banks to the tunes of tens of trillions!{…..}

One needs to always have at the FRONT of their mind, (not the back) that the MARKETS ARE MANIPULATED’

Nadeem Walayat.

Personally I don’t buy stories about the FED buying the market. The FED engineers bubbles through the back door.

simply as it is. we can not disagree with these statements. starting from this point of view, EVERY analisys shouldbe taken with caution because trillion of dollars could be put in or out from the market to cause incredible bubbles and crashes. But the final goal is to drive the market higher in the long term. So, short positions on the indexes are in most cases a loser game. At this point a smart investor should be flat or holding a small position. There are never “one life chance” in the market, and surely not the enter eavily short

http://stockcharts.com/articles/decisionpoint/2014/05/rydex-cash-flow-undermines-market-rally.html

Baa Corporate bond yield at 4.69%

$TNX at 2.46%

Ratio of 190%

In 2000 and 2007, the ratio dropped to 130% (credit stress and/or Fed tightening) and that “triggered” a stock market melt-down.

Currently, there is no credit stress and/or Fed tightening….a correction? Sure it is possibly……but a melt-down should not be expected..

The Fed is now heavily suppressing interest rate, the once reliable indicators such as credit spread, yield curve, etc. are thus not reliable in the current economic environment.

The SPX is clearly in an “over-shoot” condition until it breaks….but I don’t see the FED will stop suppressing interest rate anytime soon..

True, so maybe this time is not the interest rate that will break the stock market.

Transports have hit its quarterly measured in a time basis at two degrees. Last quarter is usually red or with a tail. This is last quarter with 4 weeks to go. Should be interesting June for bearish folks.

Chart:

05/30/2014 Over the coming two weeks, I expect the indices to make a strong push higher but I’ve been saying that for a month or two now. Once of these times I’m going to get it right. Bulkowski

By most accounts, 2000 was supposed to be the start of a secular stocks bear market – yet it has resulted in significant new highs. The secular commodities bull market since 2000 was supposed to peak along with the solar peak – yet commodities peaked several years before any current/forthcoming solar maximum. So has the markets’ relationship with solar cycles broken down?

Prior to 2000, there were only three occasions when it was worth buying commodities in favour of US equities – 1907, 1930 and 1972 (see the chart by Barry Bannister on page 14 of John’s Trading The Sun guide). Solar cycles 14, 16 and 20 were in play during those years. SC14 and 16 were familiar weak cycles, similar to the current SC24. But SC20, although not particularly weak in terms of sunspot numbers, was a sililarly long-duration cycle. It had a strikingly similar pattern to SC14 and 16 – a gently rounded plateau followed by a final miniature peak: http://www.solen.info/solar/cycl20.html

During 1907, money started to move significantly from stocks to commodities and US stocks lost half their value. The end of the SSN plateau was at month 64 of SC14, and the Panic of 1907 was at month 68.

The 1929/1930 switch into commodities also saw US stocks drop by more than half. That crash was at month 73 of SC16, and coincided with that final miniature SSN peak.

Interestingly, the 1972 switch also coincided with that final peak at month 88 of SC20. However, it was around ten months later before SP500 commenced its decline from 120 to 62.

We are now at month 67 of SC24. If sunpot numbers start to drop off the plateau around now (as they did during SC14), then we could imminently see money moving into commodities from stocks and a 50% decline in the US indices. If the sun behaves as it did during SC16 and 20, then we might have to wait another 6 to 18 months. During that wait, SP500 could easily reach 3000 after a summer correction this year.

The sun’s overall magnetic field is still persistenly weak, and in fact probably still weakening further, as predicted by cyclical models. They don’t predict any strengthening ans associated decrease in sunspots until early 2015…

Thanks Mark for your valuable update. Even I think market will go up – up to End 2015 after summer correction in 2014 but when will we see summer correction of 2014 :-(? I have read several dates in June and July .. Lets see.

Regardless of the best similarity in structure overlay, aligning the first near 100 sn peaks renders a final peak in 2015. For sc16 that would coincide with mid2015. With sc14 thered be a sub100 peak late in 2015. What r the chances of peaking past 2015?

For SP500 to reach 3000 by next year we need new buyers or more leverage – I don’t think that’s possible, see my new post. As for commodities taking over as the new speculative target, I am watching developments. They have lost upward momentum the last couple of months, so need to regain soon if they are to. China, biggest demand source, peaked demographically circa 2010, so commodities may have peaked on the front end of the SC24 max in 2011. Collective demographics are recessionary and deflationary so any rally in commodities is going to need to be speculative. For that reason I don’t see a big or long rally, and what happened so far in 2014 may have been it (gold aside). It will be clear once stocks fall, how they react.

S&P at the resistance line connecting Dec 31th, March 7th and April 4th tops. Nasdaq100 at double top. This should be formidable for at least few days so maybe just a small ray of light in the dark, long Bear Tunnel …

And gold possibly in bottoming process, Friday and today’s action are promising

Mark, let me echo Jigs sentiment about your post.

There do seem to be consistent parallels between SC14 and SC16 and correlated price movements in the metals.

However, during SC20 the cycle had already peaked and headed down throughout

the massive bull run in gold during the 70’s.

Jigs/Joseph/eclectic – it seems there are many uncertainties about SC24, as yet unanswered!

Mount Wilson Observatory were measuring solar polar magnetic field strengths during SC20. I don’t think their raw data is readily available online, but this chart of Tim Channon’s model shows it in rough graphical form (the blue Composite data line): http://daedalearth.files.wordpress.com/2011/03/hcs-vs-barycentre-a.png

It shows that the solar dipole reversed 1967/1968 (difficult to say exactly due to the long timescale), but most interestingly shows that it then reversed backwards towards zero again before suddenly regaining strength late 1971/early 1972.. It looks like it was this surge in strength that led to the switch into commodities, and the stocks crash several months later.

You can see in Channon’s chart how his model predicted correctly that something similar would happen following SC24’s dipole reversal. Here is what has happened to SC24 so far: http://wso.stanford.edu/gifs/Polar.gif

So I think that is further evidence that we need to see a significant surge in field strength measurements before the current attitude to speculation alters. There’s no sign of that happening yet, but then again these field strength measurements are subject to a smoothing process (similar to SSN) so there’s six months of uncertainty.

And of course even similar weak solar cycles are still that little bit different to each other!

Thanks all