Citigroup Economic Surprises for the G10 nations:

Source: Bloomberg

Citigroup Economic Surprises for Emerging Markets:

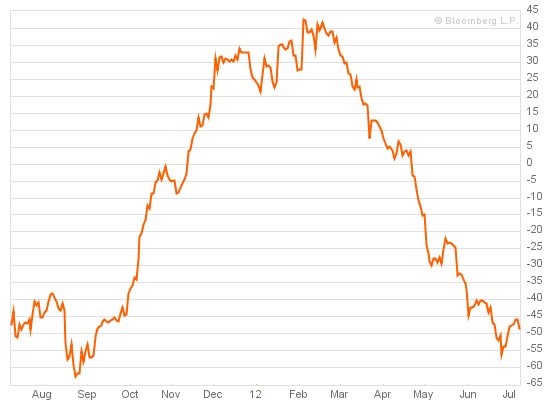

Source: Bloomberg

The message is one of a potential bottoming in June, but we need to see a clearer uptrend emerge for the G10.

Turning to leading indicators, the latest OECD data continues to show a weak picture in China and Europe, but the overall OECD nations area maintaining growth, albeit unimpressive.

Source: OECD

Source: OECD

Moving on to the Eurozone debt troubles, the pressure deflation in Spanish CDSs following the Eurozone summit outputs of the end of June has now been reversed and CDSs are back near to their highs.

Source: Bloomberg

Meanwhile the risk of systemic failure in the Eurozone is declining:

Source: Scott Grannis

The message is that more action is going to required to satisfy the markets on Euro debt but that with Spain, Italy and Greece equities priced at secular bottoms, they are prices for systemic failure which isn’t likely.

Overall in terms of the big 3 (economic surprises, leading indicators and Euro debt), we don’t yet see the kind of positive combined momentum that would support a big move up in pro-risk. However, the global policy response, in terms of rate cuts and stimuli, has yet to make itself fully felt and is unlikely complete. Last week we saw fresh UK QE, China, Euroland and Denmark rate cuts added to previous global moves. August 1st is the next FOMC outputs, where we will see whether the US adds any further stimulus.

So the question, I believe, is how pro-risk performs in this window where we see continued macro weakness but continued new global policy responses.

One other macro development is that of global wierding on agri commodities, which gives us a supply side push on prices, regardless of economic outlook. Record global temperatures in April and May have brought about droughts that have spurred grains to an almost 30% gain in the last month and have by association pushed up all softs. Now, agri commodities are looking overbought and due a rest. The severe weather continues but El Nino is expected to make a full return this summer which should improve conditions for drought-affected farming. It is therefore a question of how great the impact is on plantings and harvests before less extreme conditions return.

Turning to solar influences, sunspots and geomagnetism are working opposite ways. Sunspots continue to rise in a general upward trend towards next year’s solar maximum, and this should spur speculation and inflation. But, geomagnetism continues to be disruptive and the cumulative trend continues downwards, rather than pulling up in line with mid-year seasonality. I have updated all models this morning. Here is the medium term picture for the CRB commodities index showing that cumulative geomagnetism trend is still down:

There is the potential within that for a little upside into the end of next week, the 20th July, around the new moon, before we experience a bearish combination of a significant period of geomagnetism and a full moon around the turn of the month into August – which coincides with the FOMC. Disappointment out of the FOMC is the potential therefore.

Lastly, US earnings season began yesterday with Alcoa. JP Morgan report on Friday but the major earnings don’t really get going until next week. There’s usually a theme to US earnings season (it is sold off, or bought up). The out of season earnings and significant forecasts downgrades both suggest it could be a season offering a good beat rate, which could therefore be bullish for stocks. However, we will need to wait to next week at least to see if that is the case.

Thanks, John. Maybe the market’s correlation with sunspots and flux inverts around equinoxes and solstices ( http://time-price-research-astrofin.blogspot.com/2012/07/spx-vs-sunspots-solar-flux.html ).

Interesting chart, thanks

How does this correspond with last year?

Do you mean MiaGalaxia’s chart, or my stuff above Will?

Hi, MiaGalaxia’s chart.

I added another chart covering June – December 2011. I don’t have all sunspot-numbers for 2011 and earlier at hand. Therefore flux only.

http://time-price-research-astrofin.blogspot.com/2012/07/spx-vs-sunspots-solar-flux.html

Some years back I did some research on that matter (see DJI vs SS 2002-2003)

http://time-price-research-astrofin.blogspot.com/2012/03/djia-vs-sunspots.html

My observation (“low in SS = high in DJI”) obviously is not true for the entire chart. I now think the flip of correlation has to do with the 23.5 degree tilt of the Earth’s axis, that is equinoxes and solstices.

See also here

http://time-price-research-astrofin.blogspot.com/2012/03/moon-sun-vs-kp-index.html

Thanks

“Meanwhile the risk of systemic failure in the Eurozone is declining”

Well yes that is the current position of 2 Yr swaps, but where do you perceive to see them in the future?

Swaps are like VIX – a contrarian indicator. So I’d say that I would expect them to rise soon enough, which is bearish.

Swaps tend to follow the VIX quite well and the VIX is very low right now (chart here).

This is my proposed reason for the regular flip of correlation between astro-indicators (also ‘space weather’-data) and financial markets:

http://time-price-research-astrofin.blogspot.com/2012/07/reason-for-inversion-of-correlation.html

Hi Miagalaxia. That semi-annual seasonality of geomagnetism I believe is behind the seasonality of the stock market (page 11 of my Trading The Sun pdf), but that’s a positive correlation. I don’t quite follow how it is behind inversions.

Thanks, John. But is it really positive all along the year ? The influx of solar energy into the earths magnetic field should have different effects on the northern and southern hemisphere according to the declination of the sun.

http://www.astronomy.org/programs/seasons/

I try to illustrate my point:

The radio flux is a measure of the sun’s activity, but geomagnetism is the disturbance on the earth’s atmosphere, which is what studies relate to pessimism and depression in humans, and hence stock market returns. This is the relationship I meant:

Thanks, John. Sure, this is certainly true for the correlation between the ‘averaged’ market seasonality and the ‘averaged’ number of stormy days per month.

However, what I notice are temporary short-term flips in the stock market’s correlation with Sunspots or flux around equinoxes.

The same is true for correlations of the the medium-term Delta Cycle (1 lunar year).

Any idea?

Well sadly cycle inversions in general remain a difficult area. In previous posts/comments Jan and Will and I have all had a stab at why they might occur, along the lines of flipping over some kind of critical level or bears becoming ‘optimistic’ about their bearish positions whilst bulls step aside, etc. But these are best guesses. We see cycle inversions in various cycles, to which we can add yours, so I’ve no doubting them.

Thanks for your thoughts and hints, John. Much appreciated.

Here’s another example with the planetary A-index

and inversions within the time-frames listed in Cliver’s Table 2: