Here is a chart showing the relation of between live cattle prices and solar cycles. It can be seen that cattle futures peaked very close to the last 3 secular commodities solar peaks of 1917, 1947 and 1979. This suggests cattle prices should peak close to the next anticipated secular commodities solar peak of Feb/Mar 2013.

Source: Sergey Tarassov

If we bring cattle futures prices up to date in the chart below, we can see that prices have been accelerating upwards since 2010, which appears in line with historic behaviour as sunspots pick up.

Source: TradingCharts

Both the EU and the US are forecast to produce lower meat output in 2012 and 2013, as farmers rebuild herds amongst tight supply and strong demand (from countries such as Russia and Turkey). It is not expected that supply in cattle will catch up until 2014.

Therefore, by solar cycles, cattle prices should rise into next year’s solar peak, and the demand-supply situation supports this happening. Prices have been rising quite consistently and strongly already however, and may not give traders an easy entry point.

Turning to corn, we see a similar strong relationship between prices and solar maximums for the last 3 secular commodities solar peaks of 1917, 1947 and 1979. Again, this suggests corn prices should rise into next year’s anticipated secular commodities solar peak.

Source: Sergey Tarassov

Corn futures prices took a dip after their early 2011 peak and perhaps offer a better entry point currently, particularly as current droughts from Mexico to Argentina are expected to shrink corn stockpiles to a five-year low. However, whilst shrinking inventories are expected to push up prices over the next 6 months, record planted acres are expected to make for bumper harvests later in the year. The wildcard in this is the weather.

Source: TradingCharts

Now according to new NECSI research, investor speculation rather than regular demand-supply factors was instrumental in the two food price spikes of 2008 and 2011, and furthermore, they predict a third speculation-driven spike by 2013.

Source: NECSI

Source: NECSI

This fits very well with what I have previously written regarding the influence of rising sunspots into the solar maximum inspiring human behaviours of buying, risk-taking, and money circulation. The drive to speculate makes for risk excesses in either stocks or commodities into solar peaks, and into 2013 we see evidence that speculation will peak in commodities, with the history in cattle and corn prices above adding to that.

Turning to equities, there is a historically similar route map in the 2000s so far to that of the 1850s, i.e. a historical rhyme. If we amalgamate that with other such close historical rhymes, such as 1887, 1923 and 1906, the ‘average’ route map looks like this:

Source: Sergey Tarassov

That fits very well with my own findings in how the stock market performed into previous solar commodity peaks, namely overall flat, and also that the low is likely to be around 2014, but a higher low than in 2009. It also fits with a recession 2013-2014 and stocks starting a new secular bull in 2014, as a lead indicator before the recession ends.

The next two charts are spectrograms for the Dow Jones Industrials index stretching back in time, the first being older and the second more recent. These capture all the actual cycles, based on real major turns, and layer them over each other. Where we see spikes, these represent the biggest confluences of the same time cycles.

Source both: Sergey Tarassov

Forget theoretical cycles, here we are seeing what actual cycles are observed repeatedly in this index, and there is a notable confluence of a cycle of 3.5 years in both charts. Now the current cyclical stocks bull began in early 2009, and 3.5 years later would be late 2012, which if turned out to be the cyclical top, would again fit very well with topping out ahead of the solar peak and recession, and diverging from commodities at the end, which go on to a parabolic top at or following the solar peak.

Another notable confluence on the above two charts shows that there is a cycle at work lasting 9-12 years, which happens to be the length of a solar cycle. Based on my work, we would expect to see the solar cycle visible in such an analysis, and that is a very close fit.

Which brings me to this link, which is CXO Avisory’s piece finding no notable correlation between the sunspot cycle and stock market returns. They demonstrate different approaches to finding a consistent relationship between the two, and find none. Well, if I took a similar approach to this chart of mine below it would average out at a negligible correlation too.

But that’s because the cyclical bull from 2003 to 2007 is not related to sunspots. If I look specifically at returns from solar minimums to solar maximums then I get something more persuasive, with an average 70% return in that 3-5 year period.

And to demonstrate the difference, here are the returns for the other period, down from the solar maximum to the next solar minimum:

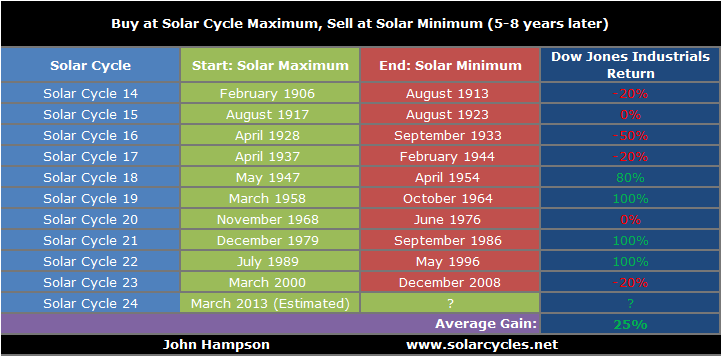

That’s an average 25% return in that 5-8 year falling sunspot period, compared to a 70% in the 3-5 year period of rising sunspots. Not only is that a substantial difference, but the 5-8 year period is significantly longer than the 3-5 year period, and in fact the difference in average returns per year is 18% in the rising sunspots period versus 4% in the falling sunspots period.

So whilst I do not deny CXO’s results, I suggest the issue is in what they are looking for. The relationships between sunspots and the financial markets lie in solar peaks, and not only that but alternating with commodities in pro-risk speculative peaks that correlate with solar peaks. Furthermore, the spectrogram further up the page displays evidence of a cycle in stocks around the same length as the solar cycle, supporting this peak/turn relationship, but CXO’s analysis is looking for a close relationship at all times rather than up into and around solar peak turns.

In short, if we consider that rising sunspots inspire human risk-taking, buying and speculation, but that other factors would also drive people to similar behaviour, then in periods of negligible sunspots we might get strong cyclical bull markets for other non-sunspot related reasons.

There’s a nice chart here that support’s your thesis:

http://finance.fortune.cnn.com/2011/04/28/the-coming-commodity-price-nightmare

Have you looked back to other solar cycles and commodity prices eg 1948 and 1885?

John

Broadly speaking I’m restricted to the last 100 years because of data availability.