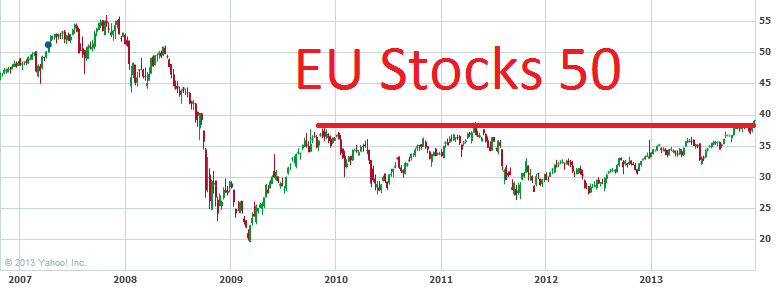

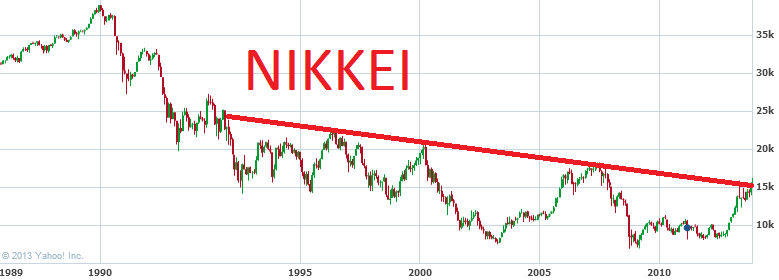

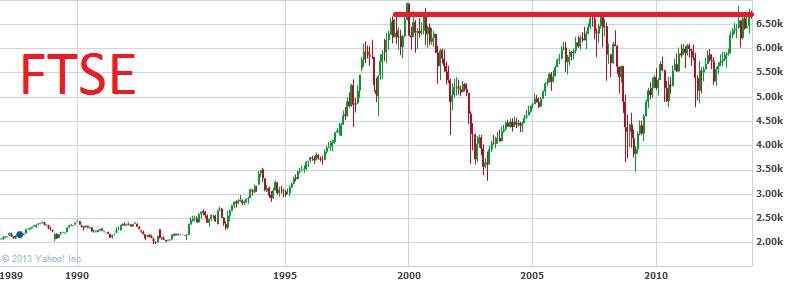

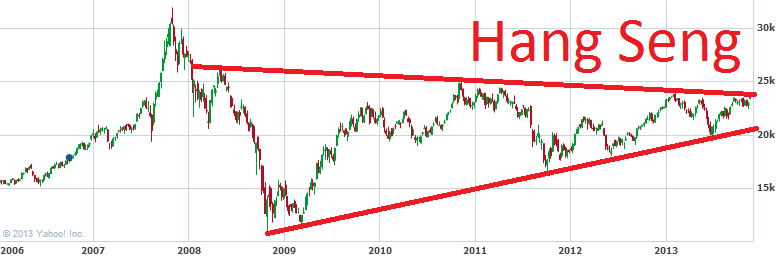

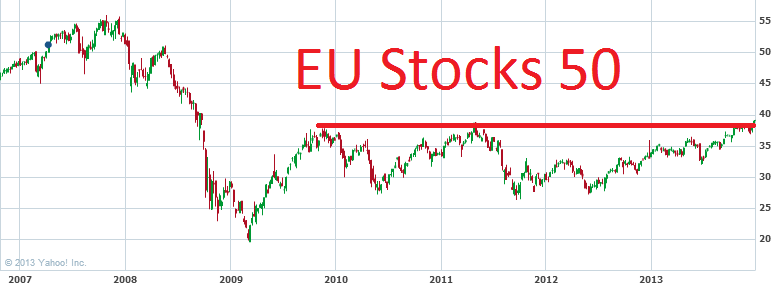

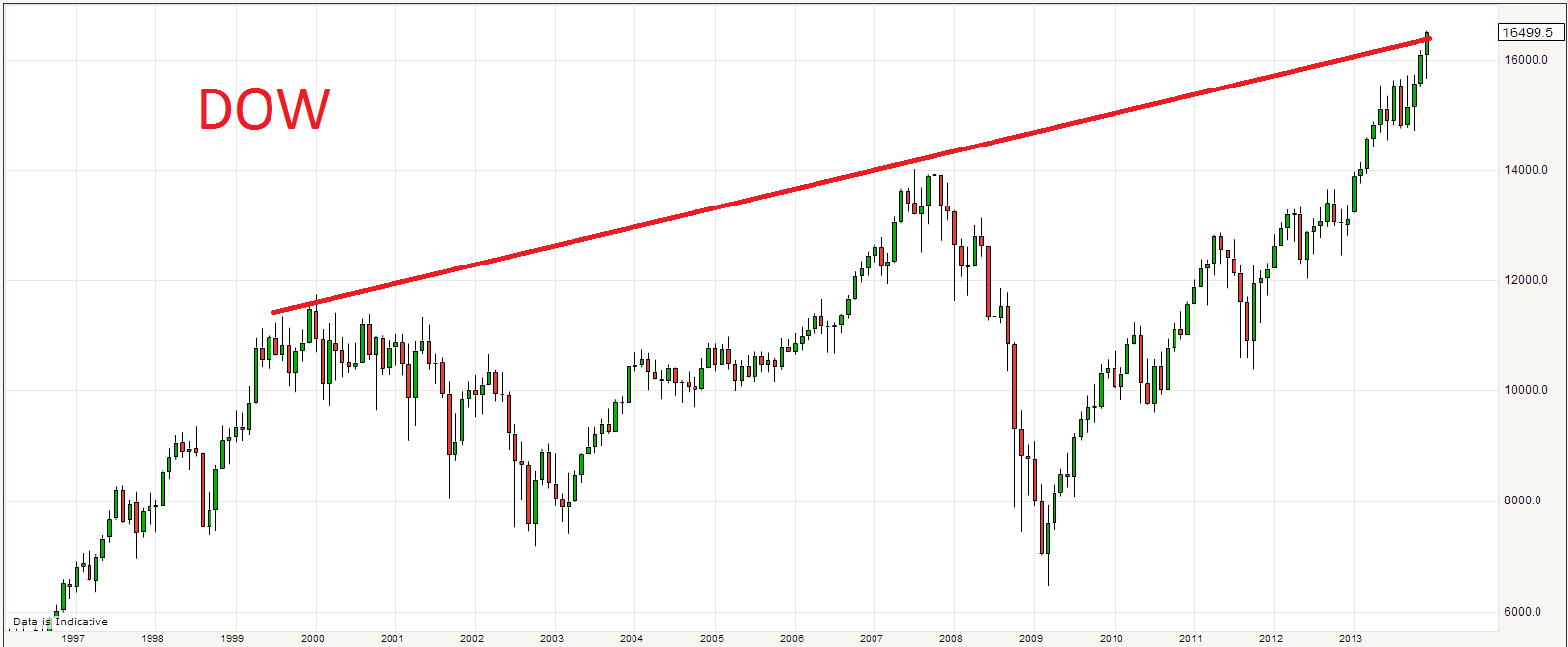

Major global stock indices at long term resistance levels:

Declining breadth in number of country indices participating in world equities rally:

Source: Moneymovesmarkets

US margin debt and investor credit balances at all-time record:

Rydex Nasdaq leveraged bull/bear ratio at all-time record:

Source: Sentimentrader

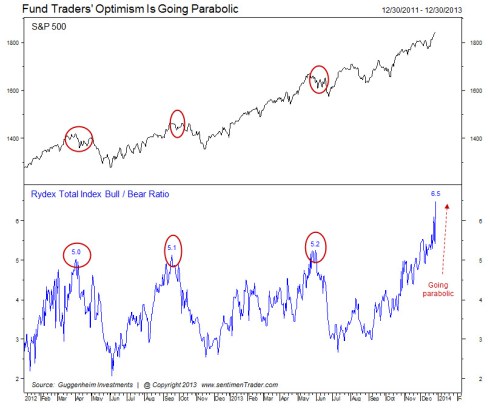

Rydex Total Index bull/bear ratio going parabolic:

Source: Sentimentrader

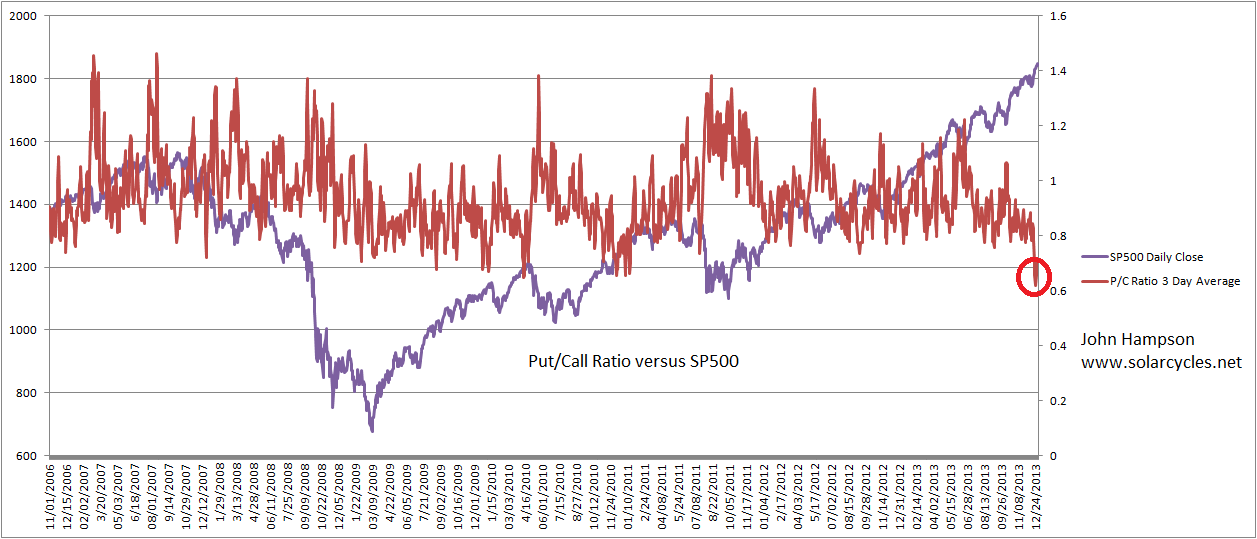

CBOE put/call ratio 3 day average at historic extreme:

Investors Intelligence Bullish at highest since October 2007, Bearish at lowest since March 1987:

Source: InvestmentU

Source: InvestmentU

Citigroup Panic/Euporia Model now 5 weeks above Euphoria threshold:

Source: Barrons/Citigroup

Source: Barrons/Citigroup

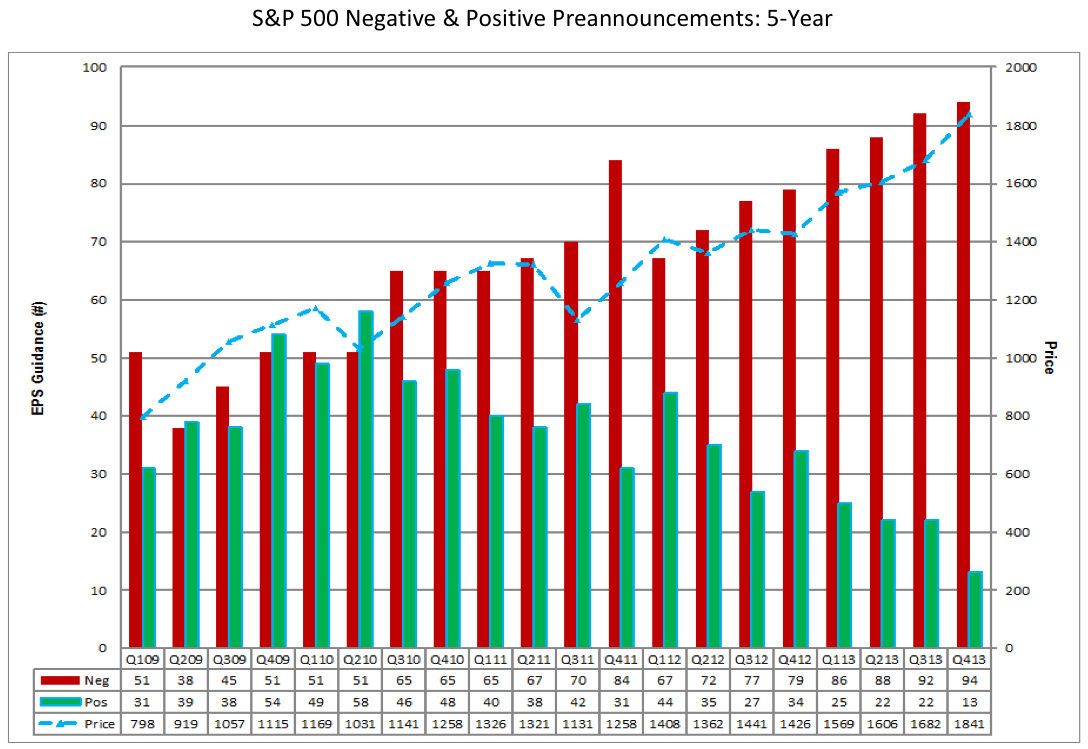

Earnings guidance for US Q4 most negative on record, and equities rallying on earnings disappointment:

Source: Business Insider

Source: Business Insider

Skew now at 133, still one of the highest readings on record.

US equities second highest market cap to GDP valuation outside of 2000, the 4th highest Q ratio valuation and 4th highest CAPE valuation in history.

My opinion really should not matter. Best of luck for 2014.

{kind=link}

You know what they say: “it’s not a question of if, but when.”

Thanks again for sharing all your great work, and best wishes for a great 2014 to you too!

Many thanks HighRev, and I very much appreciate the credit you gave me in your last post.

It was well deserved!

Your compilation of charts are getting better all the time. Good research John. Happy New Year

Thanks Paul

Happy New Year John. And, in due time.

Thanks Ryknow

John,

Is your expected downtrend in the stock market a correction within a secular bull market and will the bull market continue after the correction (crash)? Or is the expected downtrend a continuation within an ongoing secular bear market?

Jack

Coming up Jack in a new post….

Hi John,

I’ve found your site very informative for some time now. You are one of the few people who look for causal relationships for market performance (i.e. solarcycles, the new name of this blog).

Your more recent focus on demographics is timely. However, I’m not convinced that this information is useful for market timing as there are too many other factors to consider. Without question the markets are working against demographic headwinds but, I think that’s about as much as can be said with a degree of confidence. Forty years ago people were projecting the “Population Bomb” and now we have the “Demographic Winter”. As a believer in cycles, it seems odd to me that as wrong as their linear thinking was 40 years ago now they’re right. Maybe, but I’m not willing to bet a lot of money on it.

I happen to believe that there was a good deal of unanticipated technology improvements that helped mitigate the predicted consequences of the “Population Bomb”. And I have reason to believe that we will see more new technologies that will be directed toward mitigating the “Demographic Winter”. What I’m saying is new technologies can cause paradigm shifts. What once wasn’t possible or feasible now is and people may change their behavior based on the new possibilities. Given this belief I can’t take their predictions at face value, nor can I say how successful technology will be in fighting the demographic headwinds.

With respect to your recent postings, let me just say that when markets/indices are in the process of making all time highs (or new longer time highs) over a period of months, I would expect the readings we’re seeing. For me at least, such indicators/readings are warnings not to be too bullish. They could be a reason to sell and take profits. There’s nothing at all wrong with that but, for being short equities or equity indices; not yet.

One could say that since the S&P 500 peak on October 11, 2007 at 1,576.09, the index is up (@1848.26) 17.3% in over five years or about 3.46% per year. On this basis the market doesn’t appear to be overheated if one considers that the long term average gain is about twice as much. It is worthwhile to also consider how many people were buying back then versus on March 9th, 2009. So do I believe a prudent investor needs to be cautious now? Yes.

Lastly, I think it’s very significant that the Fed has a near $4 trillion balance sheet and it’s still growing despite the beginning of the “taper”. And it’s not only the Fed; it’s the ECB, the BoJ and others that are effectively doing the same thing. I don’t believe in the saying “this time is different”; in fact, I get very suspicious of people who claim that to justify their view. Let me just say that I don’t believe we’ve been here before in terms of global monetary policy and as a result, it’s dangerous to predict the future based on past trends.

The point was made many years ago by John Maynard Keynes; “Markets can remain irrational longer than you can remain solvent.”

With respect to your most recent post, I find it a little disappointing. Rolling out a bunch of indicators and saying that “My opinion really should not matter”? At least for me, the primary reason I visit your site is because I think your opinion matters!

Sorry for being so long winded. Keep up the good work that you generously share with us and best wishes to you and yours for 2014.

I appreciate your comments, thanks.

My opinion then… there are too many indicators of differing angles on the market at historic extremes, that have reliably in the past led to major drops. I believe the market will break and with hindsight this will look obvious. That’s what I meant.

Several people have made comments regarding market momentum being up, but anyone playing the long side still against that backdrop of elastic band stretched to historic extremes, is playing with fire (unless stopped and gains-protected). Sure, a prudent approach is to sell longs and wait for the turn.

Whether this is a deep correction or a new bear market, demographics are a potential key factor, if there is evidence that demographics were potent in the past AND are still potent today. So new post on that coming up.